|

시장보고서

상품코드

1636273

중국의 전기자동차 배터리 재료 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)China Electric Vehicle Battery Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

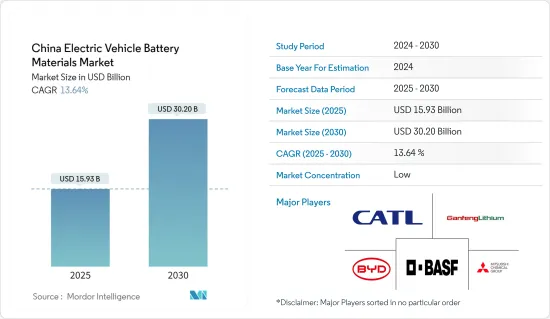

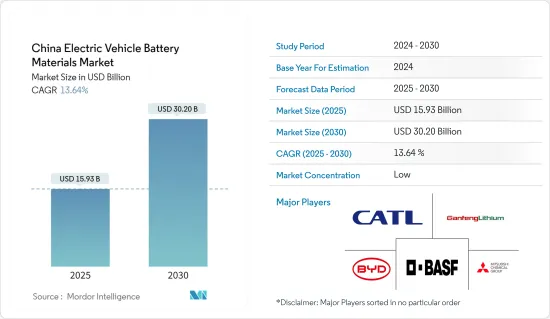

중국의 전기자동차 배터리 재료 시장 규모는 2025년 159억 3,000만 달러로 추정되며, 예측 기간(2025-2030년) 동안 13.64%의 CAGR로 2030년에는 302억 달러에 달할 것으로 예상됩니다.

주요 하이라이트

- 장기적으로는 전기자동차 판매 확대, 정부 정책 및 규제 등의 요인이 예측 기간 동안 중국 전기자동차 배터리 재료 시장의 가장 중요한 촉진요인 중 하나가 될 것으로 예상됩니다.

- 반면, 수입 원료에 의존하고 있어 가격 변동에 영향을 받기 쉬워 시장 조사에 부정적인 영향을 미칠 것으로 예상됩니다.

- 배터리 기술 발전에 대한 수요는 지속적으로 증가하고 있습니다. 이 요인은 향후 시장에 몇 가지 기회를 창출할 것으로 예상됩니다.

중국의 전기자동차 배터리 재료 시장 동향

시장을 독점하는 리튬이온 배터리 유형

- 세계 리튬 이온 전기자동차 배터리 시장은 기회와 도전이 뒤섞여 있는 역동적인 시장입니다. 리튬이온 이차전지는 주로 유리한 용량 대 중량 비율로 인해 다른 배터리 기술을 능가하는 보급률을 보이고 있습니다. 리튬 이온 이차전지는 긴 수명, 낮은 유지보수, 긴 수명 및 현저한 가격 하락과 같은 우수한 성능 특성으로 인해 그 보급에 더욱 박차를 가하고 있습니다.

- 리튬이온 배터리는 기존에는 동종 제품보다 높은 가격대에 판매되어 왔으나, 시장 선두 업체들은 규모의 경제를 실현하기 위해 투자를 하고 연구개발 노력을 강화해 왔습니다. 이러한 경쟁의 격화로 인해 배터리의 성능이 향상되었을 뿐만 아니라 리튬이온 배터리의 가격도 하락하고 있습니다.

- 최근 리튬이온 배터리와 셀 팩의 가격은 지속적으로 하락하여 최종사용자 산업에서 점점 더 매력적으로 변하고 있으며, 2022년에 일시적으로 상승한 후 2023년에도 배터리 가격은 계속 하락세를 이어갔습니다. 중요한 하이라이트는 리튬이온 배터리 팩의 비용이 14% 하락하여 사상 최저치인 139달러/kWh를 기록했다는 점입니다.

- 환경에 대한 관심이 높아지는 가운데 중국 정부는 전기자동차를 열렬히 지지하고 있으며, 탄소 배출 제로 목표를 달성하기 위해 노력하고 있습니다. 전기자동차의 저장 용량에 필수적인 리튬에 대한 수요는 매우 높으며, 세계 주요 기업들은 리튬 채굴을 강화하고 있습니다.

- 2024년 7월, 중국 동부 산둥성은 1,000억 위안(약 138억 달러)을 투자할 계획을 발표했습니다. 이 야심찬 청사진은 전극 재료, 전해질, 배터리 셀, 조립에 이르는 산업 체인을 포괄합니다. 산둥성의 전략은 민간용 배터리의 다양화 및 품질 향상뿐만 아니라 연구개발 강화에 초점을 맞추고 있습니다. 산동성 정부는 지난시와 칭다오시를 지원하여 원자재 생산 및 배터리 조립 기업을 육성하여 현지 신에너지 자동차 제조업체의 수요를 충족시키고 있습니다.

- 2024년 2월, CATL은 1회 충전으로 1,000km(621마일) 이상 주행할 수 있는 획기적인 리튬인산철(LFP) 배터리를 발표했습니다. 이 혁신은 중국 내 원자재 수요를 확대할 태세를 갖추고 있습니다.

- 이러한 개발로 인해 리튬이온 배터리의 수요가 급증하여 향후 몇 년 동안 다양한 원료의 필요성이 높아질 것입니다.

전기자동차 판매 확대

- 중국의 전기자동차(EV) 배터리 재료 시장은 전기자동차 판매량 급증과 지속가능한 교통수단에 대한 국가적 노력에 힘입어 빠르게 성장하고 있으며, 전기자동차 보급의 세계 리더로서 중국의 필수 배터리 재료(리튬, 니켈, 코발트, 망간)에 대한 수요는 급증하고 있습니다. 이들 재료는 전기자동차 전력 저장의 핵심 기술인 리튬이온 배터리 제조에 매우 중요합니다.

- 중국의 전기자동차 판매 호조는 배터리 재료 시장의 주요 원동력이 되고 있습니다. 최근 몇 년 동안 중국 정부는 정부의 인센티브와 보조금, 이산화탄소 배출량 감축 및 대기오염 대책에 대한 강력한 정책 프레임워크를 통해 전기자동차 보급이 빠르게 진행되고 있습니다. 정부의 신에너지 자동차(NEV) 의무화는 자동차 제조업체에 일정 비율의 전기자동차 생산을 의무화하는 것으로, 이 기세를 더욱 가속화하고 있습니다.

- CATL은 급증하는 EV용 배터리 수요에 대응하기 위해 생산능력을 강화하고 있습니다. 또한, CATL은 연구개발에 많은 투자를 통해 비용 절감과 동시에 배터리 성능 향상을 목표로 하고 있습니다.

- 주목할 만한 움직임으로 CATL은 2024년 6월 테슬라와 전략적 제휴를 맺고 테슬라의 상하이 기가팩토리에 리튬이온 배터리를 공급하기로 약속했습니다. 이 제휴는 중국 배터리 제조업체와 국제적인 전기자동차 제조업체와의 관계가 심화되고 있음을 보여줍니다.

- 2023년 중국 전기자동차 부문은 전년 대비 약 22.7% 성장하고, 배터리 전기자동차 판매량은 약 540만대로 2019년 83만대에서 크게 도약했습니다.

- 중국 정부는 세제 혜택, 제조업체와 소비자 모두에 대한 보조금, 충전 인프라에 대한 투자 등 다양한 정책을 통해 전기자동차 부문을 지속적으로 지원하고 있습니다. 이러한 정책은 EV를 보다 저렴하고 편리하게 만들어 보급률을 높이고, 그 결과 배터리 재료에 대한 수요를 증가시키는 것을 목표로 하고 있습니다. BYD와 같은 기업들은 리튬 인산철(LFP) 배터리와 같은 새로운 배터리 화학제품을 개발하여 기존 리튬이온 배터리보다 에너지 밀도가 약간 낮지만 안전하고 저렴한 리튬이온 배터리와 같은 새로운 배터리 화학제품을 개발하고 있습니다. 이러한 발전은 EV를 대중에게 보다 친숙하게 다가갈 수 있도록 하는 데 매우 중요합니다.

- 중국의 전기자동차 배터리 재료 시장 전망은 매우 밝습니다. 정부의 지속적인 지원, 기술 발전, 전략적 산업 파트너십을 통해 중국은 세계 전기자동차 시장에서 리더십을 유지할 준비가 되어 있습니다. 주요 배터리 제조업체들의 지속적인 생산능력 확대와 지속가능한 관행에 대한 강조는 필수 재료의 안정적인 공급을 보장하고 EV 부문의 빠른 성장을 뒷받침할 것으로 보입니다.

중국의 전기자동차 배터리 재료 산업 개요

중국의 전기자동차 배터리 재료 시장은 반분할되어 있습니다. 이 시장의 주요 기업(무순)은 Contemporary Amperex Technology Co., Limited, BYD Auto, Ganfeng Lithium, BASF SE, Mitsubishi Chemical Group Corporation 등이 있습니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 소개

- 조사 범위

- 시장 정의

- 조사 가정

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 소개

- 2029년까지 시장 규모와 수요 예측(단위 : 달러)

- 최근 동향과 개발

- 정부 정책 및 규정

- 시장 역학

- 성장 촉진요인

- 전기자동차 판매 성장

- 정부 지원 정책 및 규정

- 성장 억제요인

- 원료 공급에 대한 의존

- 성장 촉진요인

- 공급망 분석

- PESTLE 분석

- 투자 분석

제5장 시장 세분화

- 배터리 유형

- 리튬이온 배터리

- 납축배터리

- 기타

- 재료

- 양극

- 음극

- 전해액

- 분리막

- 기타

제6장 경쟁 구도

- M&A, 합작투자, 제휴, 협정

- 주요 기업의 전략

- 기업 개요

- Contemporary Amperex Technology Co., Limited

- BYD Auto Co., Ltd.

- Ganfeng Lithium

- BASF SE

- Mitsubishi Chemical Group Corporation

- UBE Corporation

- Umicore SA

- Sumitomo Chemical Co., Ltd.

- BTR New Material Group Co. Ltd.

- Shanshan Co.

- 기타 저명한 기업 리스트

- 시장 순위/점유율(%) 분석

제7장 시장 기회와 향후 동향

- 배터리 기술의 진보

The China Electric Vehicle Battery Materials Market size is estimated at USD 15.93 billion in 2025, and is expected to reach USD 30.20 billion by 2030, at a CAGR of 13.64% during the forecast period (2025-2030).

Key Highlights

- Over the long term, factors such as growing electric vehicle sales and supportive government policies and regulations are expected to be among the most significant drivers for the China Electric Vehicle Battery Materials Market during the forecast period.

- On the other hand, the country's reliance on imported raw materials makes the industry vulnerable to price fluctuation, which is expected to negatively impact the market studied.

- Nevertheless, there is continued growing demand for advancements in battery technology. This factor is expected to create several opportunities for the market in the future.

China Electric Vehicle Battery Materials Market Trends

Lithium-ion Battery Type to Dominate the Market

- The global lithium-ion electric vehicle battery market is a dynamic arena, teeming with both opportunities and challenges. Lithium-ion rechargeable batteries are outpacing other battery technologies in popularity, primarily due to their advantageous capacity-to-weight ratio. Their adoption is further fueled by superior performance attributes, such as longevity, low maintenance, an extended shelf life, and a notable decrease in price.

- While lithium-ion batteries traditionally commanded a higher price point than their counterparts, leading market players have been channeling investments into achieving economies of scale and bolstering R&D efforts. This intensified competition has not only enhanced battery performance but also driven down lithium-ion battery prices.

- Recent trends show a consistent decline in the prices of lithium-ion batteries and cell packs, making them increasingly attractive to end-user industries. After a brief uptick in 2022, battery prices continued their downward trajectory in 2023. A significant highlight was the 14% drop in lithium-ion battery pack costs, reaching a record low of USD 139/kWh.

- Amid rising environmental concerns, the Chinese government is fervently championing electric vehicles, aligning its efforts with ambitious net-zero carbon emission targets. Lithium, a crucial component for EV storage capacity, is in high demand, prompting leading global companies to ramp up lithium extraction.

- In July 2024, Shandong province in eastern China unveiled plans for a substantial 100 billion yuan (USD 13.8 billion) investment. The ambitious blueprint encompasses an industrial chain spanning electrode materials, electrolytes, battery cells, and assembly. Shandong's strategy not only aims to diversify and enhance the quality of consumer batteries but also emphasizes bolstering R&D. The provincial government is backing Jinan and Qingdao cities to nurture companies in raw material production and battery assembly, catering to the demands of local new energy vehicle manufacturers.

- In February 2024, CATL introduced a groundbreaking lithium iron phosphate (LFP) battery boasting an impressive driving range of over 1,000 kilometers (621 miles) on a single charge. This innovation is poised to amplify raw material demand in China.

- Given these developments, the demand for lithium-ion batteries is set to surge, subsequently driving up the need for various raw materials in the coming years.

Growing Electric Vehicle Sales

- China's electric vehicle (EV) battery materials market is expanding rapidly, fueled by soaring EV sales and a national commitment to sustainable transportation. As the global leader in EV adoption, China's appetite for essential battery materials-lithium, nickel, cobalt, and manganese-has surged. These materials are pivotal for crafting lithium-ion batteries, the primary technology for EV power storage.

- China's booming EV sales are a primary catalyst for its battery materials market. In recent years, bolstered by generous government incentives, subsidies, and a robust policy framework targeting carbon emission reductions and air pollution combat, China has witnessed a meteoric rise in EV adoption. The government's New Energy Vehicle (NEV) mandate, compelling automakers to produce a specific percentage of EVs, further amplifies this momentum.

- Contemporary Amperex Technology Co. Limited (CATL), a frontrunner in battery manufacturing, is ramping up its production capacity to cater to the surging demand for EV batteries. Additionally, CATL is channeling substantial investments into research and development, aiming to boost battery performance while curtailing costs.

- In a notable move, CATL forged a strategic alliance with Tesla in June 2024, committing to supply lithium-ion batteries for Tesla's Shanghai Gigafactory. This partnership highlights the deepening ties between Chinese battery producers and international EV manufacturers.

- In 2023, China's electric vehicle sector grew by approximately 22.7% year-on-year, with battery EV sales soaring to about 5.4 million, a significant leap from 0.83 million in 2019.

- The Chinese government continues to support the EV sector through various measures, including tax incentives, subsidies for both manufacturers and consumers and investments in charging infrastructure. These policies are designed to make EVs more affordable and convenient, thereby driving higher adoption rates and, consequently, increasing the demand for battery materials. Innovations in battery technology are also shaping the market. Companies like BYD are developing new battery chemistries, such as lithium iron phosphate (LFP) batteries, which are safer and cheaper, although with slightly lower energy density than traditional lithium-ion batteries. These advancements are crucial for making EVs more accessible to the mass market.

- The outlook for the EV battery materials market in China is highly positive. With continued support from the government, technological advancements, and strategic industry partnerships, China is well-positioned to maintain its leadership in the global EV market. The ongoing expansion of production capacities by major battery manufacturers and the emphasis on sustainable practices will likely ensure a steady supply of essential materials, supporting the rapid growth of the EV sector.

China Electric Vehicle Battery Materials Industry Overview

The China Electric Vehicle Battery Materials Market is semi-fragmented. Some of the key players in this market (in no particular order) are Contemporary Amperex Technology Co., Limited, BYD Auto Co., Ltd, Ganfeng Lithium, BASF SE, and Mitsubishi Chemical Group Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Electric Vehicle Sales

- 4.5.1.2 Supportive Government Policies and Regulations

- 4.5.2 Restraints

- 4.5.2.1 Dependence on Raw Material Supply

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE ANALYSIS

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion Battery

- 5.1.2 Lead-Acid Battery

- 5.1.3 Others

- 5.2 Material

- 5.2.1 Cathode

- 5.2.2 Anode

- 5.2.3 Electrolyte

- 5.2.4 Separator

- 5.2.5 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted byr Leading Players

- 6.3 Company Profiles

- 6.3.1 Contemporary Amperex Technology Co., Limited

- 6.3.2 BYD Auto Co., Ltd.

- 6.3.3 Ganfeng Lithium

- 6.3.4 BASF SE

- 6.3.5 Mitsubishi Chemical Group Corporation

- 6.3.6 UBE Corporation

- 6.3.7 Umicore SA

- 6.3.8 Sumitomo Chemical Co., Ltd.

- 6.3.9 BTR New Material Group Co. Ltd.

- 6.3.10 Shanshan Co.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancements in Battery Technology