|

시장보고서

상품코드

1636275

아시아태평양의 전기자동차 배터리 재료 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Asia Pacific Electric Vehicle Battery Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

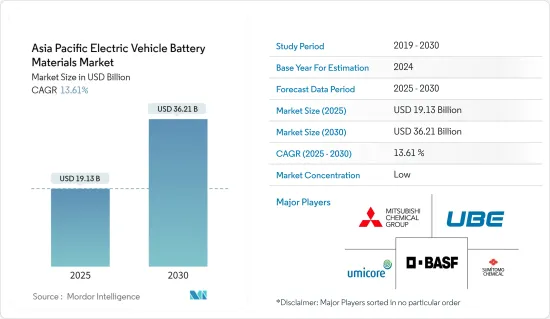

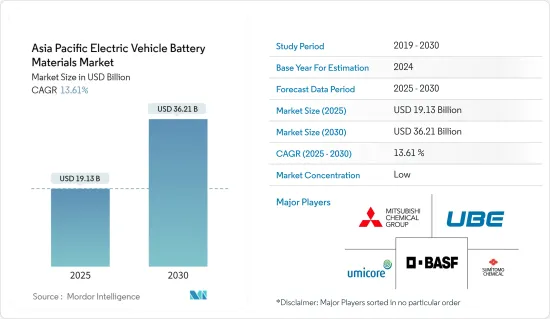

아시아태평양의 전기자동차 배터리 재료 시장 규모는 2025년 191억 3,000만 달러로 추정되며, 예측 기간(2025-2030년) 동안 13.61%의 CAGR로 2030년에는 362억 1,000만 달러에 달할 것으로 예상됩니다.

주요 하이라이트

- 중기적으로는 전기자동차(EV) 판매량 증가와 정부의 규제 및 정책이 예측 기간 동안 전기자동차 배터리 재료의 수요를 견인할 것으로 예상됩니다.

- 반대로, 신뢰성과 비용 효율성에 기인한 기존 자동차에 대한 선호가 확산되면서 전기자동차와 그 배터리의 판매에 도전이 되고 있습니다.

- 그러나 에너지 밀도 향상, 급속 충전, 안전성 향상, 수명 연장 등의 특징을 가진 배터리 기술의 비약적인 발전은 전기자동차 배터리 재료 시장 진입 기업들에게 큰 비즈니스 기회가 될 것으로 보입니다.

- 전기자동차의 급속한 보급에 힘입어 인도는 예측 기간 동안 아시아태평양의 전기자동차 배터리 재료 시장에서 가장 빠르게 성장하는 지역이 될 것으로 예상됩니다.

아시아태평양의 전기자동차 배터리 재료 시장 동향

리튬이온 배터리 타입이 시장을 독점

- 전기자동차(EV)용 리튬이온 배터리의 생산량 증가는 배터리 재료 시장에 큰 영향을 미치고 있습니다. 이러한 배터리 생산의 급격한 증가는 리튬 수요의 현저한 증가를 촉진하고 있습니다. 이 지역에서의 리튬 발견은 원료 비용에 큰 영향을 미치고 있습니다.

- 주요 시장 참여자들은 리튬이온 배터리 생산을 촉진하고 배터리 원료에 대한 수요 증가에 대응하기 위해 리튬 매장량 및 연구개발에 투자하고 있습니다. 이러한 지속적인 매장량 발견은 장기적으로 리튬이온 배터리 가격을 낮추는 데 도움이 되고 있습니다.

- 예를 들어, 배터리 가격은 2023년 139달러/kWh로 13% 이상 하락했습니다. 기술 발전과 제조 개선으로 배터리 팩 가격은 2025년에는 113달러/kWh, 2030년에는 80달러/kWh까지 하락할 것이라는 예측도 있습니다.

- 또한, 환경 문제가 대두됨에 따라 아시아태평양 정부들은 EV용 리튬이온 배터리 생산을 적극 지원하고 있습니다. 순 탄소 배출량 제로 달성에 관심이 많은 이들 정부는 전기자동차 수요 급증에 대응하기 위해 리튬이온 배터리 생산을 촉진하기 위한 여러 이니셔티브를 내놓고 있습니다.

- 예를 들어, 한국은 2023년 12월 EV용 배터리를 중심으로 배터리 산업을 강화하기 위해 향후 5년간 290억 달러의 투자 계획을 발표했습니다. 이 전략에는 배터리 공급망 다변화와 한국 대기업에 대한 세제 혜택이 포함되어 있습니다. 이들 기업은 필수적인 배터리 재료의 채굴권을 확보하기 위해 해외 진출을 지원하고 있습니다. 이러한 구상은 청정에너지의 대안인 리튬이온 배터리 생산을 확대할 뿐만 아니라 당장의 배터리 재료 수요도 확대할 것으로 보입니다.

- 또한, 리튬이온 배터리의 가격 하락은 수요 급증과 새로운 생산 공장 설립과 함께 이 지역의 배터리 원료에 대한 수요를 강화하고 있습니다. 최근 세계 주요 기업들이 이 지역에서 EV용 리튬이온 배터리 생산 확대를 위한 프로젝트에 착수하고 있습니다.

- 예를 들어, BMW는 2024년 2월 태국 라용에 새로운 배터리 공장을 건설할 계획을 발표했습니다. 이러한 움직임은 태국의 배터리 공급망을 강화할 것으로 예상되며, BMW는 태국을 EV용 배터리의 중요한 수출 거점으로 삼아 아시아태평양 시장에 더 폭넓게 대응할 계획입니다. 이러한 노력은 태국에서의 배터리 생산을 촉진하고 향후 몇 년 동안 리튬이온 배터리 재료에 대한 수요를 증가시킬 것으로 예상됩니다.

- 이러한 발전을 감안할 때, 리튬이온 배터리의 생산이 발전함에 따라 EV용 배터리 재료의 수요가 급증할 것이 분명합니다.

괄목할 만한 성장세를 보이는 인도

- 인도는 전기자동차(EV)용 배터리 재료 부문에서 중요한 위치를 차지하고 있습니다. 인도는 필수 소재의 안정적인 공급을 보장하면서 전략적으로 배터리 제조 역량을 강화하고 있습니다.

- 최근 몇 년 동안 인도는 지역 내 전기자동차 생산 현황에서 압도적인 힘을 가지게 되었습니다. 예를 들어, 국제에너지기구(IEA)의 보고서에 따르면, 2023년 인도의 전기자동차 판매량은 8만 2,000대로 2022년 대비 70.8% 급증하여 2019년 대비 119배의 놀라운 성장세를 보일 것으로 예상됩니다. 정부에서 여러 가지 이니셔티브와 프로젝트를 진행하고 있기 때문에 전기자동차 판매의 모멘텀은 앞으로도 계속될 것으로 보입니다.

- 인도는 리튬, 코발트, 니켈과 같은 핵심 소재의 안정적이고 윤리적인 공급을 확보하는 데 중점을 두고 있습니다. 그러나 이러한 노력은 큰 도전에 직면해 있습니다. 원자재 문제를 해결하기 위해 인도는 국내 매장량을 조사하고 국제적인 파트너십을 구축하기 위해 노력하고 있습니다. 인도의 초점은 전기자동차 배터리 재료의 급증하는 수요에 대응하기 위해 인도의 광물 자원을 활용하는 데에 있습니다.

- 주목할 만한 개발로 인도 지질조사국(GSI)은 2023년 2월 잠무-카슈미르 주 Salal-Haimana 지역에서 590만 톤으로 추정되는 리튬 매장량을 발견했습니다. 비철금속인 리튬은 배터리 에너지 저장 시스템 및 EV 애플리케이션에서 매우 중요한 역할을 하고 있습니다. 이번 발견은 전기자동차에 대한 급성장하는 리튬 수요를 충족시키고, 당분간 전기자동차 배터리 재료 생산을 강화할 수 있게 됐습니다.

- 인도의 주요 전기자동차 제조사들은 급증하는 전기자동차 수요에 맞춰 배터리 생산능력을 증강하고 있으며, 인프라와 기술 양면에서 막대한 투자가 필요한 상황입니다.

- 중요한 움직임으로, 오라 일렉트릭은 2024년 7월 타밀 나두(Tamil Nadu) 주에 위치한 기가 팩토리의 초기 단계에 1억 달러를 투자할 것이라고 발표했습니다. 이 시설에서는 국산 리튬이온 배터리를 생산할 예정입니다. 오라 일렉트릭의 전략적 목표는 내년 초까지 배터리 셀을 자체 생산으로 전환하여 현재 한국과 중국 공급업체로부터 탈피하는 것입니다. 이러한 과감한 투자는 EV용 리튬이온 배터리 생산을 가속화할 뿐만 아니라, 이 지역의 EV용 배터리 재료에 대한 수요를 증폭시킬 수 있을 것으로 보입니다.

- 이러한 발전으로 EV용 배터리 생산이 크게 증가하여 향후 몇 년 동안 EV용 배터리 재료의 수요가 급증할 것으로 예상됩니다.

아시아태평양의 전기자동차 배터리 재료 산업 개요

아시아태평양의 전기자동차 배터리 재료 시장은 단편적인 시장입니다. 주요 참여 기업으로는 BASF SE, Mitsubishi Chemical Group Corporation, UBE Corporation, Umicore SA, Sumitomo Chemical 등이 있습니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 소개

- 조사 범위

- 시장 정의

- 조사 가정

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 소개

- 2029년까지 시장 규모와 수요 예측(단위 : 10억 달러)

- 최근 동향과 개발

- 정부 정책 및 규정

- 시장 역학

- 성장 촉진요인

- 전기자동차 판매 성장

- 정부 지원 정책 및 규정

- 성장 억제요인

- 기존 자동차에 대한 의존

- 성장 촉진요인

- 공급망 분석

- 산업의 매력 - Porter's Five Forces 분석

- 공급 기업의 교섭력

- 소비자의 협상력

- 신규 참여업체의 위협

- 대체품의 위협 제품·서비스

- 경쟁 기업 간의 경쟁 관계

- 투자 분석

제5장 시장 세분화

- 배터리 유형

- 리튬이온 배터리

- 납축배터리

- 기타

- 재료

- 양극

- 음극

- 전해액

- 분리막

- 기타

- 지역

- 중국

- 인도

- 호주

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 기타 아시아태평양

제6장 경쟁 구도

- M&A, 합작투자, 제휴, 협정

- 주요 기업의 전략

- 기업 개요

- Sumitomo Chemical Co., Ltd.

- BASF SE

- Mitsubishi Chemical Group Corporation

- UBE Corporation

- Umicore SA

- Contemporary Amperex Technology Co. Limited

- Nichia Corporation

- ENTEK International LLC

- LG Chem

- Kureha Corporation

- 기타 저명한 기업 리스트

- 시장 순위/점유율 분석

제7장 시장 기회와 향후 동향

- 배터리 기술의 진보

The Asia Pacific Electric Vehicle Battery Materials Market size is estimated at USD 19.13 billion in 2025, and is expected to reach USD 36.21 billion by 2030, at a CAGR of 13.61% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, growing electric vehicle (EV) sales and supportive government policies and regulations are expected to drive the demand for electric vehicle battery materials during the forecast period.

- Conversely, the widespread preference for conventional vehicles, attributed to their reliability and cost-effectiveness, poses a challenge to the sales of electric vehicles and their batteries.

- However, breakthroughs in battery technology-boasting features like enhanced energy density, quicker charging, heightened safety, and extended lifespans-are set to unlock substantial opportunities for players in the electric vehicle battery materials market.

- Driven by surging electric vehicle adoption, India is poised to lead as the fastest-growing region in Asia Pacific's electric vehicle battery materials market during the forecast period.

Asia Pacific Electric Vehicle Battery Materials Market Trends

Lithium-Ion Battery Type Dominate the Market

- The growing production of lithium-ion batteries for electric vehicles (EVs) has notably influenced the battery materials market. This surge in battery production has driven a marked increase in lithium demand. Discoveries of lithium in the region have a pronounced effect on raw material costs.

- Key market players are channeling investments into lithium reserves and R&D, aiming to boost lithium-ion battery production and meet the escalating demand for battery raw materials. Ongoing discoveries of these reserves have been instrumental in driving down lithium-ion battery prices over time.

- For instance, battery prices saw a dip in 2023, settling at USD 139/kWh, marking a decline of over 13%. With the current trajectory of technological advancements and manufacturing improvements, projections suggest battery pack prices could further drop to USD 113/kWh by 2025 and USD 80/kWh by 2030.

- Moreover, in response to escalating environmental concerns, governments in the Asia Pacific are actively championing lithium-ion battery production for EVs. With a keen focus on achieving net-zero carbon emissions, these governments have launched multiple initiatives to boost lithium-ion battery production, catering to the surging EV demand.

- For instance, in December 2023, South Korea unveiled a USD 29 billion investment plan over the next five years to bolster its battery industry, with a spotlight on EV batteries. The strategy includes diversifying battery supply chains and providing tax incentives to major South Korean firms. These firms are being supported in their overseas ventures to secure mining rights for essential battery materials. Such initiatives are poised to not only amplify lithium-ion battery production as a clean energy alternative but also escalate the demand for battery materials in the foreseeable future.

- Additionally, the declining prices of lithium-ion batteries, coupled with a surging demand and the establishment of new production plants, are bolstering the demand for battery raw materials in the region. In recent years, top global firms have embarked on projects aimed at boosting lithium-ion battery production for EVs in the region.

- For instance, in February 2024, BMW unveiled plans for a new battery factory in Rayong, Thailand. This move is anticipated to bolster the nation's battery supply chains. BMW envisions Thailand as a pivotal export hub for its EV batteries, catering to the broader Asia Pacific market. Such undertakings are set to expedite battery production in Thailand and heighten the demand for lithium-ion battery materials in the years to come.

- Given these developments, it's clear that advancements in lithium-ion battery production and the surging demand for EV battery materials will continue to grow in the coming years.

India to Witness Significant Growth

- India is positioning itself as a key player in the electric vehicle (EV) battery materials arena. The nation is strategically bolstering its battery manufacturing capabilities while ensuring a steady supply of essential materials.

- In recent years, India has emerged as a dominant force in the regional EV production landscape. For instance, the International Energy Agency (IEA) reported that in 2023, India sold 82,000 electric vehicles, marking a 70.8% surge from 2022 and an astonishing 119-fold increase since 2019. With the government launching several initiatives and projects, the momentum in EV sales is set to continue its upward trajectory.

- India is placing a strong emphasis on ensuring a consistent and ethical supply of vital materials such as lithium, cobalt, and nickel. This endeavor, however, poses significant challenges. To tackle the raw material conundrum, India is delving into its domestic reserves and forging international partnerships. The nation's focus remains on harnessing its mineral wealth to cater to the surging demand for EV battery materials.

- In a notable development, the Geological Survey of India (GSI) unearthed lithium reserves estimated at 5.9 million tonnes in the Salal-Haimana region of Jammu and Kashmir in February 2023. Lithium, a non-ferrous metal, plays a pivotal role in battery energy storage systems and EV applications. This discovery is poised to satiate the burgeoning lithium demand for EVs and bolster EV battery material production in the foreseeable future.

- Leading Indian EV manufacturers are ramping up their battery production capabilities to align with the surging EV demand, necessitating substantial investments in both infrastructure and technology.

- In a significant move, Ola Electric, in July 2024, unveiled a USD 100 million investment for the initial phase of its gigafactory in Tamil Nadu. This facility is set to produce indigenous lithium-ion batteries. Ola Electric's strategic goal is to transition to its battery cells by early next year, moving away from its current suppliers in Korea and China. Such a bold investment is poised to not only expedite lithium-ion battery production for EVs but also amplify the demand for EV battery materials in the region.

- Given these developments, the trajectory of battery production for EVs is set for a significant boost, leading to a pronounced surge in demand for EV battery materials in the coming years.

Asia Pacific Electric Vehicle Battery Materials Industry Overview

Asia Pacific's electric vehicle battery materials market is fragmented. Some key players (not in particular order) are BASF SE, Mitsubishi Chemical Group Corporation, UBE Corporation, Umicore SA, Sumitomo Chemical Co., Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Electric Vehicle Sales

- 4.5.1.2 Supportive Government Policies and Regulations

- 4.5.2 Restraints

- 4.5.2.1 Dependence on Conventional Vehicle

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion Battery

- 5.1.2 Lead-Acid Battery

- 5.1.3 Others

- 5.2 Material

- 5.2.1 Cathode

- 5.2.2 Anode

- 5.2.3 Electrolyte

- 5.2.4 Separator

- 5.2.5 Others

- 5.3 Geography

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Australia

- 5.3.4 Japan

- 5.3.5 South Korea

- 5.3.6 Malaysia

- 5.3.7 Thailand

- 5.3.8 Indonesia

- 5.3.9 Vietnam

- 5.3.10 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Sumitomo Chemical Co., Ltd.

- 6.3.2 BASF SE

- 6.3.3 Mitsubishi Chemical Group Corporation

- 6.3.4 UBE Corporation

- 6.3.5 Umicore SA

- 6.3.6 Contemporary Amperex Technology Co. Limited

- 6.3.7 Nichia Corporation

- 6.3.8 ENTEK International LLC

- 6.3.9 LG Chem

- 6.3.10 Kureha Corporation

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/ Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancements in Battery Technology