|

시장보고서

상품코드

1687065

영국의 화물 및 물류 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)United Kingdom Freight and Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

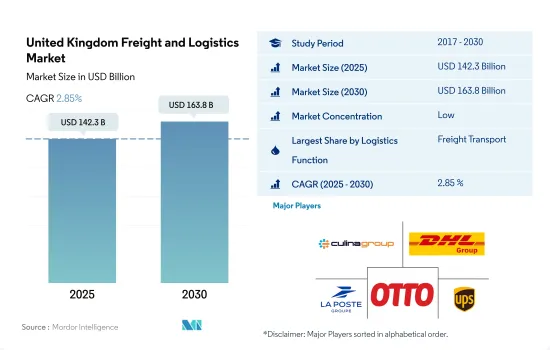

영국의 화물 및 물류 시장 규모는 2025년에 1,423억 달러로 추정되고, 2030년에는 1,638억 달러에 이를 전망이며, 예측 기간인 2025-2030년 CAGR 2.85%로 성장할 것으로 예측됩니다.

전자상거래, 인프라 개발, 기술 도입을 촉진하는 전략의 시작이 시장 수요를 견인하고 있습니다.

- 영국은 2040년까지 신형 대형 화물차의 제로 에미션 달성을 목표로 하고 있습니다. 예측에 따르면 영국 전기 트럭 시장의 2020-2026년 CAGR은 약 70%로 견조하며, 2026년 판매량은 2,167대에 이를 것으로 예측됩니다. 이 중 25대 중 22대가 중형 전기 트럭이 될 것으로 예상됩니다. 주목할만한 개발로서 아마존은 2022년, 이 회사의 배송 차량에 전기 대형 화물차(HGV) 5대를 도입해 연간 10만 마일을 주행시킬 계획을 발표했습니다. 이 노력으로 이산화탄소 배출량이 170톤 이상 삭감될 전망입니다. 영국은 장거리 전기 트럭에 전력을 공급하기 위한 전국적인 가선망의 구축에 적극적으로 임하고 있으며, 수송의 탈탄소화라는 2050년의 목표에 합치하고 있습니다.

- 전자상거래의 급성장은 영국의 운수 부문에 있어서 큰 기폭제가 되고 있습니다. 예측에 따르면 영국의 전자상거래 수익은 2025년까지 1,795억 달러에 이를 전망입니다. 2023년에는 의류와 가방 등 패션 제품의 전자상거래 매출이 크게 급증하였고, 53억 8,000만 달러 이상 증가하여 약 438억 9,000만 달러에 달했습니다. 이러한 상승세는 앞으로도 지속될 것으로 예상되며, 패션 시장의 전자상거래 판매로 인한 수익은 2025년까지 약 543억 6,000만 달러에 이를 것으로 예측됩니다.

영국의 화물 및 물류 시장 동향

소비자용 풀필먼트 센터 수요 증가로 영국 창고 수는 2027년까지 21만 4,000개에 달할 전망

- 2024년 5월 DP월드는 고객 경쟁력 강화를 위한 5,000만 파운드(6,092만 달러) 투자의 일환으로 코벤트리에 지금까지 가장 큰 창고, 59만 8,000평방피트의 시설을 개설했습니다. 이는 2023년 9월에 비스터에 개설한 27만 평방 피트의 음악 및 비디오 유통 창고에 이어, 영국의 물리적 음악의 70%, 홈 엔터테인먼트 제품의 35%를 취급합니다. DP월드는 지금까지 버튼 어폰 트렌트에 7만 5,000평방피트의 창고를, 런던 게이트웨이의 물류 허브에 23만 평방피트의 멀티유저 창고를 개설했습니다. 사우샘프턴과 런던 게이트웨이 허브와 함께 78개국에서 사업을 하는 DP월드는 세계 무역의 10%를 관리하고 있습니다. 이러한 이니셔티브는 이 부문에서 GDP 기여를 높일 것으로 기대됩니다.

- 영국의 대형 창고의 수는 급속히 증가하고 있습니다. 2027년까지, 세계 전체에서 5만 평방 피트 이상의 창고는 약 21만 4,000동이 될 것으로 예상되고 있습니다. 이러한 창고의 대부분은 전자상거래 풀필먼트 센터로서 기능하며, 2027년까지 전체 창고의 약 18%가 소비자용 풀필먼트용이 될 전망입니다. 이러한 증가는 무역 물류 허브로 운영되는 창고의 비율이 소비자용 풀필먼트 센터로 이동하기 시작하면서 전자상거래의 세계적 확대를 시사하고 있습니다.

영국 정부는 연료 가격에 큰 영향을 미치고 있으며 연료세와 부가가치세(표준세율 20%)가 가솔린과 경유가격의 대부분을 차지하고 있습니다.

- 2022년 8월 원유가격은 100달러 아래로 떨어져 1배럴 90.63달러로 1개월을 마쳤습니다. 2023년에는 가격이 더 내려 5월에는 배럴당 72.50달러까지 떨어졌습니다. 2024년 3월 영국 휘발유 가격은 리터당 평균 150.1페소로 2023년 11월 이후 최고치를 기록했습니다. 이는 중동 정세의 긴박화에 따른 유가 상승 및 파운드화 약세에 따른 것입니다. 전체적인 인플레이션율은 완화하고 있지만, 휘발유와 경유의 가격은 3월에 상승했습니다. 유가는 2024년 4월 이스라엘의 이란 보복 공격으로 급등한 후 하락했습니다.

- 2024년 6월 영국 정부는 2030년까지 제트 연료에 최소 10%의 지속 가능한 항공 연료(SAF)를 의무화할 계획을 확인했습니다. 현재 SAF는 희귀하고 기존 연료보다 비싸기 때문에 항공 분야에서 사용을 늘리기 어렵습니다. SAF는 세계 제트 연료의 0.1% 미만입니다. 정부의 SAF 의무화는 법제화 승인을 거쳐 2025년 1월에 개시될 예정입니다. 이는 2050년까지 항공기 순배출량 제로를 목표로 하는 2022년의 '제트 제로' 전략에 이은 것입니다.

영국의 화물 및 물류 산업 개요

영국의 화물 및 물류 시장은 단편화되어 있으며, 이 시장의 주요 기업은 Culina Group, DHL Group, La Poste Group(DPD Group, CitySprint(UK) Ltd. 포함), Otto Group(Evri Limited 포함), United Parcel Service of America, Inc.-UPS(Coyote Logistics 포함) 등입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 주요 요약 및 주요 조사 결과

제2장 보고서 제안

제3장 서문

- 조사의 전제조건 및 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 인구동태

- 경제 활동별 GDP 분포

- 경제 활동별 GDP 성장률

- 인플레이션율

- 경제성과 및 프로파일

- 전자상거래 산업의 동향

- 제조업의 동향

- 운수 및 창고업 GDP

- 수출 동향

- 수입 동향

- 연료 가격

- 트럭 운송 비용

- 유형별 트럭 보유 대수

- 물류 실적

- 주요 트럭 공급업체

- 모달 점유율

- 해상화물 운송 능력

- 정기선의 접속성

- 기항지 및 퍼포먼스

- 운임 동향

- 화물 톤수의 동향

- 인프라

- 규제 프레임워크(도로와 철도)

- 영국

- 규제 프레임워크(해상 및 항공)

- 영국

- 밸류체인 및 유통채널 분석

제5장 시장 세분화

- 최종 사용자 산업별

- 농업, 어업 및 임업

- 건설업

- 제조업

- 석유 및 가스, 광업, 채석업

- 도매 및 소매업

- 기타

- 물류 기능별

- 쿨리에, 익스프레스 및 소포(CEP)

- 목적지별

- 국내

- 국제

- 화물 수송

- 수송 모드별

- 항공

- 해상 및 내륙 수로

- 기타

- 화물 수송

- 수송 수단별

- 항공

- 파이프라인

- 철도

- 도로

- 해상 및 내륙 수로

- 창고 보관

- 온도 관리

- 온도관리 없음

- 온도 관리

- 기타 서비스

- 쿨리에, 익스프레스 및 소포(CEP)

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Advanced Supply Chain Group

- Americold(including Americold Whitchurch)

- Ballyvesey Holdings Limited(including Montgomery Transport)

- CMA CGM Group(including CEVA Logistics)

- Culina Group

- DACHSER

- Delamode Group(formerly Xpediator PLC)

- Deutsche Bahn AG(including DB Schenker)

- DHL Group

- DP World(including P&O Ferrymasters)

- DSV A/S(De Sammensluttede Vognmaend af Air and Sea)

- Europa Worldwide Group

- Expeditors International of Washington, Inc.

- FedEx

- GBA Logistics

- Gregory Distribution Ltd.

- Hellmann Worldwide Logistics

- Hoyer Group(including Hoyer UK Ltd)

- Huboo

- Kinaxia Logistics Limited(including Mark Thompson Transport)

- Kuehne Nagel

- La Poste Group(including DPD Group, and CitySprint(UK) Ltd.)

- Lineage, Inc.

- Maritime Group Ltd.

- Meachers Global Logistics

- Otto Group(including Evri Limited)

- Owens Group

- Pall-Ex Group

- PD Ports(owned by Brookfield Asset Management)

- Peel Ports Group

- Rhenus Group

- Samskip

- SITRA Group(including Abbey Logistics Group)

- Solstor UK Limited

- Swain Group

- Turners(Soham) Ltd.

- United Parcel Service of America, Inc.-UPS(including Coyote Logistics)

- WH Malcolm Ltd.

- Walden Group(including Moviantio)

- Whistl UK Ltd.

- Wincanton PLC

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Porter's Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(시장 성장 촉진요인, 억제요인, 기회)

- 기술의 진보

- 정보원 및 참고문헌

- 도표 목록

- 주요 인사이트

- 데이터 팩

- 용어집

- 환율

The United Kingdom Freight and Logistics Market size is estimated at 142.3 billion USD in 2025, and is expected to reach 163.8 billion USD by 2030, growing at a CAGR of 2.85% during the forecast period (2025-2030).

E-commerce, infrastructure development, and strategy launches will boost technology adoption are leading the market demand

- The UK aims to achieve zero-emission status for new heavy goods vehicles by 2040. Projections indicate a robust CAGR of nearly 70% for the UK's electric truck market from 2020 to 2026, with sales forecasted to hit 2,167 units in 2026. Of these, approximately 22 out of every 25 vehicles are expected to be medium-duty electric trucks. In a notable development, Amazon announced plans in 2022 to introduce five electric heavy goods vehicles (HGVs) into its delivery fleet, covering a distance of 100,000 miles annually. This initiative is anticipated to reduce carbon emissions by over 170 tonnes. The UK is actively working on establishing a nationwide network of overhead wires to power long-distance electric trucks, aligning with its 2050 goal of decarbonizing transportation.

- The rapid growth of e-commerce is a major catalyst for the UK's transportation sector. Projections indicate that e-commerce revenue in the UK will reach USD 179.5 billion by 2025. In 2023, revenue from e-commerce sales of fashion products, including apparel and bags, saw a significant surge, rising by over USD 5.38 billion to approximately USD 43.89 billion. This upward trend is expected to continue, with revenue from e-commerce sales in the fashion market projected to reach around USD 54.36 billion by 2025.

United Kingdom Freight and Logistics Market Trends

The UK's warehouse count is expected to reach 214,000 by 2027 due to a rise in demand for consumer fulfillment centers

- In May 2024, DP World opened its largest warehouse yet, a 598,000 sq ft facility in Coventry, as part of a GBP 50 million (USD 60.92 million) investment to boost customer competitiveness. This follows the September 2023 opening of a 270,000 sq ft music and video distribution warehouse in Bicester, handling 70% of the UK's physical music and 35% of home entertainment products. Previously, DP World opened a 75,000 sq ft site in Burton upon Trent and a 230,000 sq ft multi-user warehouse at London Gateway's logistics hub. Alongside its hubs at Southampton and London Gateway, operating in 78 countries, DP World manages 10% of global trade. Such initiaves are expected to boost the GDP contribution from the sector.

- The number of large warehouses in the United Kingdom is rapidly increasing. By 2027, there are expected to be around 214,000 warehouses larger than 50,000 square feet globally. Many of these warehouses are to serve as e-commerce fulfillment centers, and approximately 18% of all warehouses will be for consumer fulfillment by 2027. This increase suggests the global expansion of e-commerce as the proportion of warehouses operating as trade distribution hubs begins to shift in favor of consumer fulfillment centers.

UK government has a major influence on fuel prices, and both fuel duty and VAT (standard 20% rate) make up majority of the petrol and diesel prices

- In August 2022, the oil price dropped under USD 100 and finished the month at USD 90.63 a barrel. Prices dropped further in 2023, and by May, a barrel of oil was down to USD 72.50. In March 2024, petrol prices in the UK averaged 150.1p per litre, the highest since November 2023. This is due to rising oil prices due to Middle East tensions and a weaker pound against the dollar. Although overall inflation has eased, petrol and diesel prices increased in March. Oil prices have since dropped after spiking following Israel's retaliatory attack on Iran in April 2024.

- In June 2024, the UK government confirmed it plans to require at least 10% sustainable aviation fuel (SAF) in jet fuel by 2030. Currently, SAF is scarce and more expensive than traditional fuels, making it challenging to increase its use in aviation. SAF represents less than 0.1% of jet fuel globally. The government's SAF mandate, pending legislative approval, is set to start in January 2025. This follows the 2022 "Jet Zero" strategy aiming for net-zero emissions in aviation by 2050.

United Kingdom Freight and Logistics Industry Overview

The United Kingdom Freight and Logistics Market is fragmented, with the major five players in this market being Culina Group, DHL Group, La Poste Group (including DPD Group, and CitySprint (UK) Ltd.), Otto Group (including Evri Limited) and United Parcel Service of America, Inc. - UPS (including Coyote Logistics) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Demographics

- 4.2 GDP Distribution By Economic Activity

- 4.3 GDP Growth By Economic Activity

- 4.4 Inflation

- 4.5 Economic Performance And Profile

- 4.5.1 Trends in E-Commerce Industry

- 4.5.2 Trends in Manufacturing Industry

- 4.6 Transport And Storage Sector GDP

- 4.7 Export Trends

- 4.8 Import Trends

- 4.9 Fuel Price

- 4.10 Trucking Operational Costs

- 4.11 Trucking Fleet Size By Type

- 4.12 Logistics Performance

- 4.13 Major Truck Suppliers

- 4.14 Modal Share

- 4.15 Maritime Fleet Load Carrying Capacity

- 4.16 Liner Shipping Connectivity

- 4.17 Port Calls And Performance

- 4.18 Freight Pricing Trends

- 4.19 Freight Tonnage Trends

- 4.20 Infrastructure

- 4.21 Regulatory Framework (Road and Rail)

- 4.21.1 United Kingdom

- 4.22 Regulatory Framework (Sea and Air)

- 4.22.1 United Kingdom

- 4.23 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes 1. Market value in USD for all segments 2. Market volume for select segments viz. freight transport, CEP (courier, express, and parcel) and warehousing & storage 3. Forecasts up to 2030 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Logistics Function

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode Of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode Of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature Controlled

- 5.2.4.1.2 Temperature Controlled

- 5.2.5 Other Services

- 5.2.1 Courier, Express, and Parcel (CEP)

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Advanced Supply Chain Group

- 6.4.2 Americold (including Americold Whitchurch)

- 6.4.3 Ballyvesey Holdings Limited (including Montgomery Transport)

- 6.4.4 CMA CGM Group (including CEVA Logistics)

- 6.4.5 Culina Group

- 6.4.6 DACHSER

- 6.4.7 Delamode Group (formerly Xpediator PLC)

- 6.4.8 Deutsche Bahn AG (including DB Schenker)

- 6.4.9 DHL Group

- 6.4.10 DP World (including P&O Ferrymasters)

- 6.4.11 DSV A/S (De Sammensluttede Vognmaend af Air and Sea)

- 6.4.12 Europa Worldwide Group

- 6.4.13 Expeditors International of Washington, Inc.

- 6.4.14 FedEx

- 6.4.15 GBA Logistics

- 6.4.16 Gregory Distribution Ltd.

- 6.4.17 Hellmann Worldwide Logistics

- 6.4.18 Hoyer Group (including Hoyer UK Ltd)

- 6.4.19 Huboo

- 6.4.20 Kinaxia Logistics Limited (including Mark Thompson Transport)

- 6.4.21 Kuehne+Nagel

- 6.4.22 La Poste Group (including DPD Group, and CitySprint (UK) Ltd.)

- 6.4.23 Lineage, Inc.

- 6.4.24 Maritime Group Ltd.

- 6.4.25 Meachers Global Logistics

- 6.4.26 Otto Group (including Evri Limited)

- 6.4.27 Owens Group

- 6.4.28 Pall-Ex Group

- 6.4.29 PD Ports (owned by Brookfield Asset Management)

- 6.4.30 Peel Ports Group

- 6.4.31 Rhenus Group

- 6.4.32 Samskip

- 6.4.33 SITRA Group (including Abbey Logistics Group)

- 6.4.34 Solstor UK Limited

- 6.4.35 Swain Group

- 6.4.36 Turners (Soham) Ltd.

- 6.4.37 United Parcel Service of America, Inc. - UPS (including Coyote Logistics)

- 6.4.38 W H Malcolm Ltd.

- 6.4.39 Walden Group (including Moviantio)

- 6.4.40 Whistl UK Ltd.

- 6.4.41 Wincanton PLC

7 KEY STRATEGIC QUESTIONS FOR FREIGHT AND LOGISTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (Market Drivers, Restraints & Opportunities)

- 8.1.5 Technological Advancements

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 8.7 Currency Exchange Rate