|

시장보고서

상품코드

1692523

베트남의 금속 캔 포장 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Vietnam Metal Can Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

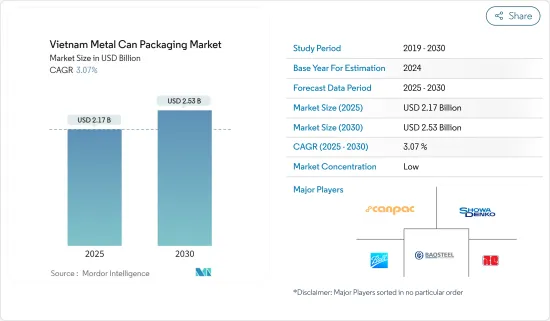

베트남의 금속 캔 포장 시장 규모는 2025년에 21억 7,000만 달러로 추계되며, 예측 기간 중(2025-2030년) CAGR 3.07%로 확대되어, 2030년에는 25억 3,000만 달러에 달할 것으로 예측됩니다.

맥주나 탄산음료 등의 알코올 음료와 비알코올 음료의 소비량이 증가하고 있는 것이, 이 나라에 있어서의 금속캔 수요 증가로 이어지고 있어, 베트남의 금속캔 포장 시장의 성장에 영향을 주고 있습니다.

주요 하이라이트

- 금속 캔은 강성, 안정성, 높은 장벽성 등 많은 이점이 있기 때문에 상품의 보관이나 장거리 수송에 빈번하게 사용되고 있습니다.

- 금속 캔은 단순하기 때문에 이 지역의 많은 소비자가 보내는 모바일 라이프 스타일에 최적인 패키지의 선택 중 하나입니다.

- 게다가 베트남의 라이프 스타일의 변화에 의해 소비자는 조리하기 쉬운 식품을 선택하게 되어 있습니다. 젊은층이나 혼자 생활의 소비자는 통조림 식품을 많이 소비하고 있습니다.

- 환경에 대한 우려가 최전선에 있는 동안 음료 회사에게 지속 가능한 패키지로 제품을 제공하는 것이 필수적입니다. PET병, 셀룰로오스 섬유 소재를 사용한 종이병, 유리병은 금속캔의 대체품으로서 사용되고 있어 업계에서의 성장에 과제를 줄 가능성이 있습니다.

- 금속 캔 포장 시장에서 큰 점유율을 차지하는 음식 식품 업계는 COVID-19의 대유행 속에서 거대한 수요를 눈에 띄었습니다.팬데믹은 소비 습관에 큰 변화를 가져왔습니다.

베트남 금속 캔 포장 시장 동향

베트남의 편의점 수요 증가

- 베트남 정부는 효율적이고 지속 가능한 산업을 발전시킴으로써 2030년까지 이 나라를 세계 유수의 수산가공센터로 만들 의향입니다. 수산물의 수출액 증가는 베트남산 냉동수산물의 포장에 대한 세계 수요의 높이가 베트남의 금속캔 포장 시장의 성장으로 이어진 것을 나타내고 있습니다.

- 어업은 베트남에 매년 10억 달러 이상의 수입을 가져오는 25개 품목 중 하나입니다. 수출은 1사분기에 전년 동기비 약 8% 증가한 20억 달러로 급증했으며, 이 성장은 주로 미국, 일본, 중국, 홍콩 등 매우 중요한 시장에서 수요가 높아지고 있습니다.

- 게다가 이전에는 신선 농산물 밖에 거래하지 않았던 많은 기업들이 가공식품에 많은 투자를 하고 있기 때문에 금속캔 패키지 수요가 증가하고 있습니다.

- 미국 농무성 대외 농업 서비스(USDA), 베트남 통계국, 베트남 공업무역성의 조사에 따르면, 베트남에서는 식품 제조업이 102.9%의 성장을 이루었습니다. 시장 점유율에 대부분은 Vissan, CJ CauTre, Ha Long Canfoco사 등의 노포 기업이 차지하고 있습니다.

- 베트남 포장 협회의 보고에 따르면 베트남 포장 업계에는 약 14,000개의 기업이 있으며, 그 중에서도 플라스틱 포장에 중점을 두고 있는 것은 9,200의 기업입니다. 운시, 빈즌, 동나이 등 주요 지역에 집중하고 있습니다.

음료 분야가 가장 큰 시장 점유율을 차지

- 음료용 금속캔은 맥주나 와인의 패키징을 비롯해, 국내의 음료 시장에서 큰 수요가 있습니다.

- 베트남에서는 다양한 제조 코팅 기술로 음료용 금속 캔 시장이 크게 확대되고 있습니다.

- 베트남의 와인 시장은 성장하고 있으며 호텔, 레스토랑 및 소매점이 세계 각국의 다양한 와인을 제공합니다. 베트남의 다양한 자유무역협정(FTA)으로 와인 시장 경쟁이 치열해지고 외국인 투자자의 생산 이전과 사업 설립을 유치하고 있습니다. FTA의 주요 목적은 수입품 관세를 크게 낮추거나 완전히 자유화함으로써 회원국 간 통합 시장을 창출하는 것입니다.

- 베트남 정부는 베트남의 민간 부문을 장려하기 위해 국유 기업에 대한 투자 비율을 낮출 계획이며 베트남 음료 산업에 대한 긍정적인 전망을 뒷받침하고 있습니다. 이는 베트남의 WTO 가맹과 CPTPP, EVFTA와 같은 많은 자유무역협정을 수반하는 것으로, 다국적기업의 음료분야에 투자를 유치하고, 베트남기업이 수출을 늘릴 기회를 창출하는 것을 목적으로 하고 있습니다. 음료 생산량 증가에 따른 기업의 투자 증가로 금속캔 수요가 확대되고 있습니다.

- 동남아시아의 중간층 증가와 소비자의 음료통에 대한 선호도는 금속캔 수요를 계속 증가시키고 있습니다. 베트남 음료 시장의 연간 생산량과 소비량 중 상당한 비율을 차지하는 것이 청량 음료, 인스턴트 티, 각종 과일 주스, 에너지 음료입니다. 베트남 통계 총국에 따르면 2022년 음료 제조로 인한 수익은 68억 5,564만 달러로 추정되고, 2023년에는 76억 9,183만 달러에 이릅니다.

베트남 금속 캔 포장 산업 개요

베트남의 금속 캔 포장 시장은 많은 주요 기업들이 지속적으로 최대 시장 점유율을 얻으려고 하기 때문에 단편화되고 있습니다. 시장의 주요 기업에는 Canpac Vietnam Co. Ltd, Showa Aluminum Can Corporation, TBC-Ball Beverage Can VN Ltd, Ball Corporation, Vietnam Baosteel Can Co. Ltd (Baosteel Group), Royal Can Industries Company Limited 등이 있습니다. 많은 시장 기업이 고품질의 금속 캔 패키징 솔루션을 개발하는 반면, 다른 기업은 업계의 요구에 부응하기 때문에 패키징 제품의 효율적인 재활용을 위해 노력하고 있습니다.

- 2024년 1월 베트남 호치민의 공예 맥주 양조장인 Rooster Beers는 인기의 Blonde와 Dark의 참신하고 슬림한 캔디자인을 발표했습니다. 세련된 캔 디자인의 도입이라고 하는 브랜드의 움직임은 이 출발을 강조하고 있습니다.

- 2024년 4월: 베트남에서는 '확장 생산자 책임'(EPR) 정책을 통해 생산자 및 수입업체는 자사 제품 및 포장의 일정 부분을 확실하게 재활용할 의무가 있었습니다. 재활용이 불가능한 경우 베트남 환경 보호(VEP) 기금에 자금을 기부해야 합니다. 천연자원환경부(MONRE)는 정령 08/2022/ND-PC에서 이러한 의무를 개설했습니다. 배터리, 윤활유, 타이어는 2024년 1월부터, 전기 및 전자 제품은 2025년 1월 1일부터, 수송 수단은 2027년 1월부터입니다. MONRE는 또한 2025년 1월까지 운송 수단의 폐기 규정을 제안하는 임무를 맡고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 업계의 매력도 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

- 시장에 대한 COVID-19의 영향 평가

제5장 시장 역학

- 시장 성장 촉진요인

- 베트남의 편의점 수요 증가

- 리사이클률 상승과 최종 사용자 제조 수요 증가

- 시장 성장 억제요인

- 플렉서블 플라스틱 등 대체 제품에 대한 수요 증가

- 시장 기회

- 베트남의 식품 캔과 음용 캔의 수출입 분석

제6장 시장 세분화

- 유형별

- 알루미늄 캔

- 스틸

- 최종 사용자별

- 식품

- 음료

- 화장품 및 퍼스널케어

- 의약품

- 페인트

- 자동차(윤활유)

- 기타 최종 사용자

제7장 경쟁 구도

- 기업 프로파일

- Canpac Vietnam Co. Ltd

- Showa Aluminum Can Corporation

- TBC-Ball Beverage Can VN Ltd(Ball Corporation)

- Vietnam Baosteel Can Co. Ltd(Baosteel Group)

- Royal Can Industries Company Limited

- Hanacan JSC

- Superior Multi-packaging Limited(SMPL)

- Kian Joo Can(Vietnam) Co. Ltd

- Nam Viet Packaging Manufacturing Co. Ltd

- My Chau Printing & Packaging Corporation

제8장 투자 분석

제9장 시장의 미래

JHS 25.05.07The Vietnam Metal Can Packaging Market size is estimated at USD 2.17 billion in 2025, and is expected to reach USD 2.53 billion by 2030, at a CAGR of 3.07% during the forecast period (2025-2030).

The rising consumption of alcoholic and nonalcoholic beverages, such as beer and carbonated drinks, is attributed to increased demand for metal cans in the country, thereby influencing the Vietnamese metal can packaging market's growth.

Key Highlights

- Due to its many advantages, such as rigidity, stability, and high barrier qualities, metal cans are frequently used to store and transport commodities across great distances. Metal cans constructed of steel and aluminum are the most popular in Vietnam. These materials have valuable qualities, such as being softer and lighter, which enable the makers to reduce logistics-related expenses.

- Because of their simplicity, metal cans are among the best packaging options for the mobile lifestyle that many consumers in the area lead. These can be carried or transported easily to outdoor sporting events, festivals, and beaches, whereas glass is typically forbidden because of its breakability. The affordability and recyclability of cans, the rising popularity of energy drinks, and the launch of new goods all contribute to the market's growth.

- Moreover, changing lifestyles in Vietnam are resulting in consumers opting for easy-to-cook food. The younger population and individually living consumers are consuming more canned food. These users have less time and are budget-restrained, thus opting for products with lower costs and higher convenience.

- With environmental concerns at the forefront, it becomes imperative for beverage companies to offer their products in sustainable packaging. Sustainability is a significant concern in the beverage industry. Many manufacturing companies are switching to eco-friendly packaging alternatives. PET bottles, paper bottles made with cellulose-fiber material, and glass bottles are used as an alternative to metal cans and can challenge their growth in the industry.

- The food and beverage industry, with a significant share in the metal can packaging market, witnessed huge demand amidst the COVID-19 pandemic. The pandemic brought a significant change in consumption habits. There has been an increasing need for packaged food products, meat, vegetables, and fruits.

Vietnam Metal Can Packaging Market Trends

Growing Demand For Convenience Food in Vietnam

- The Vietnamese government intends to make the country one of the world's leading seafood processing centers by 2030 by developing an efficient and sustainable industry. This should result in a higher export ratio of processed products and an increase in the value of Vietnamese seafood. The increasing export value of seafood has demonstrated that the high demand for packaged frozen seafood from Vietnam worldwide has led to the growth of the Vietnamese metal can packaging market. The growing urbanization in the country is expected to drive the demand for packaged food.

- The fishery is one of the 25 products that bring the country an income of more than USD 1 billion each year. The Vietnam Association of Seafood Exporters and Producers (VASEP) reported a strong beginning for Vietnam's seafood industry in 2024. Exports have surged to almost USD 2 billion in Q1, reflecting an 8% year-on-year uptick. This growth is primarily fueled by heightened demands from pivotal markets such as the United States, Japan, China, and Hong Kong. VASEP projects that by the close of 2024, Vietnam's seafood exports could hit a notable USD 9.5 billion, surpassing the previous year's figures.

- Moreover, the demand for metal can packaging is increasing with the growing investments by many businesses that previously only traded fresh agricultural products and have invested heavily in processed foods. Vietnam's rising population, income levels, changing cultural preferences, and new trade agreements opened the door to significant growth in the meat industry.

- According to the study by the USDA Foreign Agricultural Service, General Statistics Office of Vietnam, and the Ministry of Industry and Trade (Vietnam), food product manufacturing grew by 102.9 % in the country. There are nearly 6,000 enterprises operating in Vietnam's processed food industry. Most of the market share is held by well-established players such as Vissan, CJ Cau Tre, or Ha Long Canfoco.

- The Vietnam Packaging Association reports that Vietnam's packaging industry is home to approximately 14,000 enterprises, with a significant emphasis on plastic packaging, to which 9,200 enterprises are dedicated. The country boasts over 900 packaging factories, with a notable 70% concentrated in the southern region, particularly in key areas like Ho Chi Minh City, Binh Duong, and Dong Nai. Driven by swift economic and social advancements, a booming e-commerce sector, and advantageous free trade agreements (FTAs), Vietnam's packaging sector is poised for substantial growth.

Beverages Sector to Hold the Largest Market Share

- The beverage metal cans find significant demand in beer and wine packaging and other beverage markets in the country. The growing consumer awareness of the need to use green and environmentally sustainable products, the increasing recycling rate, and the reusability of metal cans are driving the market studied.

- In Vietnam, the market for beverage metal cans is expanding significantly due to the various manufacturing coating technologies. The steel and aluminum components meet secure, dependable, and hygienic beverage packaging standards. Metal beverage cans are affordable, practical, and anti-contaminating.

- The Vietnamese wine market is growing, with hotels, restaurants, and retailers offering various wines from around the world. Vietnam's diverse free trade agreements (FTAs) have made the wine market competitive, attracting foreign investors to relocate production or set up operations. The main objective of FTAs is to create an integrated market among country members by significantly reducing or fully liberalizing custom tariffs for imported products.

- Vietnam's Government has planned to decrease its stake in state-owned enterprises to encourage the country's private sector, supporting the positive outlook for Vietnam's beverage industry. This, accompanied by Vietnam's membership in the WTO and many free trade agreements such as CPTPP and EVFTA, aims to attract multinational companies to invest in the drink sector and generate opportunities for Vietnamese companies to increase exports. With the increasing investment by the companies as the production of the beverage increases, the demand for metal cans is growing.

- The growth of the middle class in Southeast Asia and consumers' preference for beverage cans continue to increase demand for metal cans. A significant percentage of the annual production and consumption of Vietnam's beverage market is soft drinks, instant teas, fruit juices of all kinds, and energy drinks. According to the General Statistics Office of Vietnam, the revenue from manufacturing beverages in 2022 was estimated at USD 6,855.64 million, and it reached USD 7,691.83 million in 2023.

Vietnam Metal Can Packaging Industry Overview

The Vietnamese metal can packaging market is fragmented owing to many key players continually trying to gain maximum market share. Some of the major players are Canpac Vietnam Co. Ltd, Showa Aluminum Can Corporation, TBC-Ball Beverage Can VN Ltd, Ball Corporation, Vietnam Baosteel Can Co. Ltd (Baosteel Group), and Royal Can Industries Company Limited. Many market players are developing high-quality metal can packaging solutions while others are making efforts toward efficient recycling of packaging products to cater to the industry requirements.

- January 2024: Rooster Beers, a craft brewery hailing from Ho Chi Minh City, Vietnam, unveiled a fresh, slim can design for its popular Blonde and Dark brews. While Rooster Beers has built its reputation on crafting traditional yet approachable beers, it is now charting a unique path, diverging from Western norms. The brand's move to introduce a sleek can design underscores this departure. With meticulously chosen design elements, the new cans exude a lively, contemporary vibe.

- April 2024: In Vietnam, the "extended producer responsibility" (EPR) policy now requires producers and importers to ensure the recycling of a set portion of their products and packaging. If they cannot recycle, they must contribute financially to the Vietnam Environment Protection (VEP) Fund. The Ministry of Natural Resources and Environment (MONRE) outlined these mandates in Decree 08/2022/ND-PC. Companies have specific deadlines to start recycling different items: batteries, lubricants, and tires from January 2024; electrical and electronic products from January 1, 2025; and means of transportation from January 2027. MONRE is also tasked with proposing disposal regulations for transportation by January 2025.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand for Convenience Food in Vietnam

- 5.1.2 Higher Recycling Rates Coupled with Higher End-user Manufacturing Demand

- 5.2 Market Restraints

- 5.2.1 Growing Demand for Alternative Products Such as Flexible Plastic

- 5.3 Market Opportunities

- 5.4 Import-Export Analysis of Food Cans and Beverage Cans in Vietnam

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Aluminum

- 6.1.2 Steel

- 6.2 By End User

- 6.2.1 Food

- 6.2.2 Beverage

- 6.2.3 Cosmetic and Personal Care

- 6.2.4 Pharmaceuticals

- 6.2.5 Paints

- 6.2.6 Automotive (Lubricants)

- 6.2.7 Other End Users

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Canpac Vietnam Co. Ltd

- 7.1.2 Showa Aluminum Can Corporation

- 7.1.3 TBC-Ball Beverage Can VN Ltd (Ball Corporation)

- 7.1.4 Vietnam Baosteel Can Co. Ltd (Baosteel Group)

- 7.1.5 Royal Can Industries Company Limited

- 7.1.6 Hanacan JSC

- 7.1.7 Superior Multi-packaging Limited (SMPL)

- 7.1.8 Kian Joo Can (Vietnam) Co. Ltd

- 7.1.9 Nam Viet Packaging Manufacturing Co. Ltd

- 7.1.10 My Chau Printing & Packaging Corporation