|

시장보고서

상품코드

1836501

의료용 처방적 분석 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Healthcare Prescriptive Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

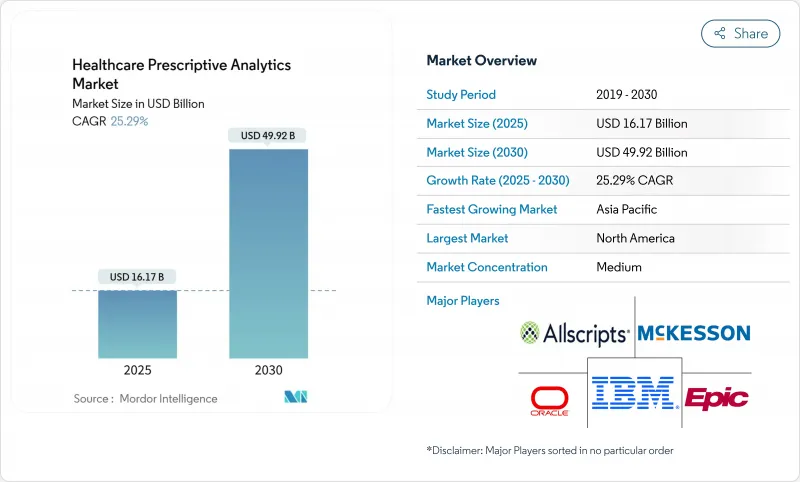

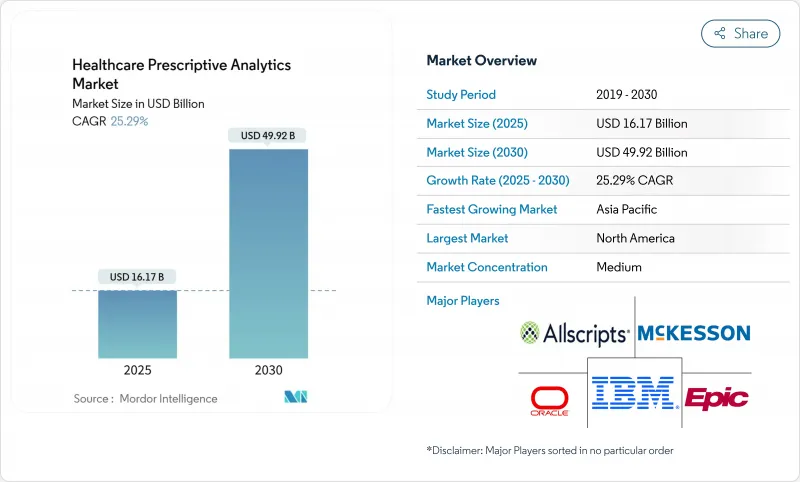

의료용 처방적 분석 시장 규모는 2025년에 161억 7,000만 달러에 이르고, 예측 기간 중(2025-2030년) CAGR은 25.29%를 나타내, 2030년에는 499억 2,000만 달러에 달할 것으로 전망됩니다.

성장을 뒷받침하는 것은 실시간 처방 혜택 의무화, 환자의 디지털 트윈의 급속한 보급, 일상적인 임상 워크 플로우에 대한 인공지능의 통합입니다. 고급 알고리즘과 임상 워크플로우에 대한 깊은 지식을 결합한 공급업체가 이점을 누리면서 클라우드 확장성, 하이브리드 배포 옵션 및 강력한 보안 프레임워크가 구매 결정을 형성합니다. 기존의 전자 의료진(EHR) 제공업체가 클라우드 네이티브 신규 진출기업과 경쟁하고, 인수 기세가 통합 분석 플랫폼으로의 전환을 보이면서 경쟁이 치열해지고 있습니다.

세계의 의료용 처방적 분석 시장 동향과 인사이트

건강 관리에서 빅 데이터와 AI 통합

의료 시스템은 전통적인 분석에서 유전체 데이터, 지속적인 모니터링 피드, 비구조화된 임상 노트의 속도와 복잡성을 처리할 수 없습니다는 것을 인식하고 있습니다. 대규모 데이터 파이프라인과 인공지능을 융합한 플랫폼은 현재 실시간으로 처방적인 권장사항을 제공합니다. 에픽 시스템즈가 2024년에 출시한 AI Trust and Assurance Suite는 임상 개발 전에 알고리즘의 성능을 테스트하고 모니터링하는 도구를 병원에 제공했습니다. 이러한 기능이 성숙함에 따라 임상의는 레트로스펙티브 보고서에서 환자별 위험 신호를 기반으로 치료를 개인화하는 요점 개입으로 전환합니다. 데이터 품질과 워크플로우 통합의 장애물이 해결되면 조기 도입 기업은 보다 높은 진단 정확도와 치밀한 치료 선택을 보고합니다.

비용 억제와 업무 효율화의 요구 증가

인건비는 병원 총경비의 50%에 육박하는 반면, 환자수는 불안정한 채로 있습니다. 처방적 분석 모델은 수익주기 타임라인을 단축하고, 인력 배치를 최적화하며, 공급망 낭비를 줄입니다. 미국 병원 협회는 미국의 건강 관리 지출의 25%가 관리 비효율성으로 인해 손실되었다고 추정합니다. 실시간 위치추적 시스템과 분석 대시보드를 결합하여 침대, 임상의, 고가치 장비를 추적하고 동적 자원 할당을 가능하게 합니다.

데이터 보안 및 규정 준수 문제

유럽 연합의 인공지능법은 현재 임상 AI를 고위험으로 분류하고 투명성과 모니터링을 의무화하고 있습니다. 동시에 2025년 3월에 승인된 유럽 의료 데이터 공간 규정은 환자의 프라이버시를 보호하면서 국경을 넘는 공유 규칙을 도입하고 있습니다. 이러한 프레임 워크는 컴플라이언스 장애물을 강화하고 공급업체는 감사 추적, 동의 엔진 및 비 식별 모듈을 분석 플랫폼에 하드 와이어로 연결해야합니다. 견고한 프라이버시 관리가 부족한 병원은 도입 지연과 잠재적인 처벌에 직면합니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

- 밸류 베이스 케어와 아웃컴 중시의 상환에의 인센티브

- 치료 최적화를 위한 환자 디지털 트윈의 상승

- 임상 현장에서 분석 인력 부족

부문 분석

임상 의사결정 지원 애플리케이션은 2024년에 가장 큰 수익을 창출했으며 의료용 처방적 분석 시장의 46.17%를 차지했습니다. 병원은 투약 실수를 줄이고 증거 기반 프로토콜을 표준화하기 위해 의사 결정 지원을 선호하며 미국 실시간 처방 혜택 프로그램과 같은 자금 지원 이니셔티브는 POC(Point-of-Care) 채용을 자극합니다. 조사 및 집단 건강 분석은 가장 급성장하는 애플리케이션이며, 지불자와 공급자가 적극적인 지역 수준의 개입으로 전환함에 따라 CAGR 27.18%를 나타낼 전망입니다. 2억 4,600만 명 이상의 비식별화된 기록을 보유하는 Epic Cosmos와 같은 포퓰레이션 규모의 데이터 세트는 질병 패턴을 모델링하고 공중 보건 활동에 정보를 제공하는 데 필요한 규모를 보여줍니다.

개인 수준의 의사 결정 지원과 집단 분석을 융합함으로써 조직은 매크로와 마이크로 렌즈를 통해 인사이트를 얻을 수 있습니다. 한 명의 환자와 전체 코호트의 케어 경로를 매핑하는 통합 플랫폼은 치료 개인화와 지역 건강 계획을 모두 지원하므로 점점 더 선호되고 있습니다.

2024년 의료용 처방적 분석 시장 규모의 64.39%를 서비스가 차지했고, 2030년까지의 CAGR은 26.78%를 나타낼 것으로 예측됩니다. 복잡한 규제 프레임워크, 레거시 EHR 환경, 임상의의 도입 장애물로 인해 기본 소프트웨어보다 도입 노하우의 가치가 높아지고 있습니다. 소프트웨어 라이선스는 여전히 필수적이지만 장기적인 권고 계약 및 관리 서비스 계약과 번들로 제공되는 경우가 많습니다. 하드웨어 지출은 교육 및 추론 워크로드를 지원하는 고성능 스토리지 및 GPU에 집중되어 있습니다.

Duke Health와 같은 의료 시스템은 분석 공급업체와 여러 해에 걸친 파트너십을 맺고 전문적인 전문 지식을 활용하면서 내부 부담을 완화하고 있습니다. 이러한 서비스 지향 모델은 모델 거버넌스, 워크플로우 재설계 및 변경 관리에 대한 지속적인 지침을 병원에 제공합니다.

지역별 분석

북미는 2024년 세계 매출의 40.81%를 창출했습니다. 미국은 2027년까지 완전히 배포될 예정인 실시간 처방 급여의 의무화를 통해 전자 처방 워크플로에 분석 규칙을 직접 통합함으로써 페이스를 잡고 있습니다. 미국에서는 이미 62만 명 이상의 처방 의사가 실시간 처방 혜택 도구를 사용하고 있습니다. 캐나다의 주 의료 프로그램은 데이터 상호 운용성에 투자하고 멕시코의 민간 병원 체인은 증가하는 운영 비용을 수용하기 위해 분석 기능을 갖춘 수익주기 플랫폼을 도입하고 있습니다.

유럽은 데이터 프라이버시와 모델의 투명성을 선호합니다. European Health Data Space는 연구자와 임상의가 국경을 넘어 익명화된 데이터 세트를 교환할 수 있도록 2차 데이터 이용을 위한 안전한 환경을 구축하기 위해 8억 1,000만 유로를 할당합니다. 독일, 영국, 프랑스는 병원의 디지털화와 AI의 시험적 도입에 국가 예산을 충당하고 있습니다. EU 인공지능법에 대응함으로써 알고리즘에 의한 권장 사항을 모두 기록하는 감사 대응 플랫폼에 대한 수요가 높아지고 있습니다.

아시아태평양은 가장 급성장하는 지역으로 CAGR 30.68%를 나타낼 전망입니다. 중국 지방정부는 AI를 강화한 병원 시스템에 보조금을 내고 고령화가 진행되는 일본은 원격의료와 분석에 대한 투자를 촉진하고 인도의 National Digital Health Mission은 데이터 교환 인프라를 맡는다. 호주와 한국은 종단 데이터세트에 의존하는 정밀의료 프로젝트에 자금을 제공하고 있으며, 싱가포르는 지역 AI 거버넌스 프레임워크의 실험실 역할을 합니다. 브라질의 2024년 임상 연구법은 디지털 건강 연구의 승인을 가속화하고 분석 벤더를 라틴아메리카로 끌어들였습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 도입

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 헬스케어에서의 빅데이터와 AI의 통합

- 비용 억제와 업무 효율화의 요구 증가

- 밸류 베이스 케어와 아웃컴 베이스의 상환에의 인센티브

- 치료 최적화를 위한 환자 디지털 트윈의 상승

- 실시간 처방전 급여(RTPB)의 의무화에 의한 POC(Point-of-Care) 분석의 촉진

- 만성질환 부담의 급증

- 시장 성장 억제요인

- 데이터 보안과 HIPAA/GDPR(EU 개인정보보호규정) 컴플라이언스의 과제

- 임상 현장에서의 분석 인력 부족

- 의사의 신뢰를 방해하는 모델의 설명 가능성의 한계

- 초기 투자비용 높이

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모·성장 예측(단위 : 달러)

- 용도별

- 임상 의사 결정 지원

- 재무 분석

- 행정/운영 분석

- 연구 및 인구 건강 분석

- 제품별

- 하드웨어

- 소프트웨어

- 서비스

- 배포 모델별

- On-Premise

- 클라우드 기반

- 하이브리드

- 최종 사용자별

- 의료 제공자

- 의료 보험사

- 제약 및 생명과학 기업

- 정부 및 공중보건 기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Allscripts Healthcare Solutions

- Oracle Corporation(Cerner Corporation)

- IBM(Merative)

- McKesson Corporation

- MedeAnalytics Inc.

- Optum Inc.

- SAS Institute Inc.

- Verisk Analytics Inc.

- Epic Systems Corporation

- Health Catalyst

- Dimensional Insight

- Innovaccer

- Arcadia

- Clarify Health Solutions

- Change Healthcare

- Philips Healthcare

- Siemens Healthineers

- GE Healthcare

- Qlik

- Teradata

제7장 시장 기회와 전망

KTH 25.10.27The Healthcare Prescriptive Analytics Market size is estimated at USD 16.17 billion in 2025, and is expected to reach USD 49.92 billion by 2030, at a CAGR of 25.29% during the forecast period (2025-2030).

Growth is propelled by real-time prescription benefit mandates, the rapid uptake of patient digital twins, and the integration of artificial intelligence into everyday clinical workflows. Vendors that pair advanced algorithms with deep clinical workflow knowledge gain an edge, while cloud scalability, hybrid deployment options, and robust security frameworks shape purchasing decisions. Competitive activity intensifies as established electronic health record (EHR) providers race against cloud-native newcomers, and acquisition momentum signals a shift toward integrated analytics platforms.

Global Healthcare Prescriptive Analytics Market Trends and Insights

Integration of Big Data and AI in Healthcare

Health systems recognize that traditional analytics cannot process the velocity and complexity of genomic data, continuous monitoring feeds, and unstructured clinical notes. Platforms that fuse large-scale data pipelines with artificial intelligence now deliver prescriptive recommendations in real time. Epic Systems' 2024 release of its AI Trust and Assurance Suite gives hospitals tools to test and monitor algorithm performance before clinical deployment. As these capabilities mature, clinicians transition from retrospective reporting to point-of-care interventions that personalize treatment based on patient-specific risk signals. Early adopters report higher diagnostic accuracy and targeted therapeutic selection, provided data quality and workflow integration hurdles are addressed.

Growing Need for Cost Containment and Operational Efficiency

Labor costs approach 50% of total hospital expenses while patient volumes remain volatile. Prescriptive analytics models shorten revenue-cycle timelines, optimize staffing rosters, and reduce supply chain waste. The American Hospital Association estimates that 25% of U.S. healthcare spending is lost to administrative inefficiencies. Real-time location systems coupled with analytics dashboards keep track of beds, clinicians, and high-value equipment, enabling dynamic resource allocation that lowers operational expenses and frees capacity for higher-acuity cases.

Data Security and Compliance Challenges

The European Union's Artificial Intelligence Act now classifies clinical AI as high-risk, mandating transparency and oversight. Simultaneously, the European Health Data Space regulation approved in March 2025 introduces cross-border sharing rules while preserving patient privacy. These frameworks raise compliance hurdles, forcing vendors to hard-wire audit trails, consent engines, and de-identification modules into analytics platforms. Hospitals that lack robust privacy controls face implementation delays and potential penalties.

Other drivers and restraints analyzed in the detailed report include:

- Incentives for Value-Based Care and Outcome-Focused Reimbursement

- Rise of Patient Digital Twins for Therapy Optimization

- Shortage of Analytics Talent in Clinical Settings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Clinical Decision Support applications generated the most significant revenue in 2024, capturing 46.17% of the healthcare prescriptive analytics market. Hospitals prioritize decision support to reduce medication errors and standardize evidence-based protocols, while funding initiatives such as the U.S. real-time prescription benefit program stimulate adoption at the point of care. Research & Population Health Analytics is the fastest-growing application, expanding at a 27.18% CAGR as payers and providers shift toward proactive, community-level interventions. Population-scale datasets such as Epic Cosmos, which holds de-identified records for more than 246 million individuals, illustrate the scale required to model disease patterns and inform public-health actions.

The convergence of individual-level decision support with population analytics lets organizations derive insights across macro and micro lenses. Integrated platforms that map care pathways for single patients and entire cohorts are increasingly favored, supporting both treatment personalization and regional health-planning efforts.

Services accounted for 64.39% of the healthcare prescriptive analytics market size in 2024 and are forecast to post a 26.78% CAGR through 2030. Complex regulatory frameworks, legacy EHR environments, and clinician adoption hurdles make implementation know-how more valuable than the underlying software. Software licenses remain essential yet are frequently bundled with long-term advisory and managed services agreements. Hardware spending focuses on high-performance storage and GPUs that support training and inference workloads.

Health systems such as Duke Health have entered multi-year partnerships with analytics vendors to access specialized expertise while reducing internal burdens. These service-oriented models provide hospitals with sustained guidance on model governance, workflow redesign, and change management.

The Healthcare Prescriptive Analytics Market Report is Segmented by Application (Clinical Decision Support, Financial Analytics, and More), Product (Hardware, Software, and Services), Deployment Model (On-Premise, and More), End User (Healthcare Providers, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 40.81% of global sales in 2024. The United States sets the pace with mandatory real-time prescription benefit implementation scheduled for full rollout by 2027, which embeds analytic rules directly into e-prescribing workflows. Over 620,000 U.S. prescribers already use real-time prescription benefit tools. Canada's provincial health programs invest in data interoperability, and Mexico's private hospital chains deploy analytics-enabled revenue cycle platforms to counterbalance rising operating expenses.

Europe prioritizes data privacy and model transparency. The European Health Data Space allocates EUR 810 million to create a secure environment for secondary data use, enabling researchers and clinicians to exchange anonymized datasets across borders. Germany, the United Kingdom, and France devote national funding to hospital digitalization and AI pilots. Compliance with the EU Artificial Intelligence Act spurs demand for audit-ready platforms that log every algorithmic recommendation.

Asia-Pacific is the quickest-expanding region, advancing at a 30.68% CAGR. China's local governments subsidize AI-enhanced hospital systems, Japan's aging population drives telemedicine and analytics investment, and India's National Digital Health Mission underwrites data-exchange infrastructure. Australia and South Korea fund precision-medicine projects that rely on longitudinal datasets, while Singapore acts as a test-bed for regional AI governance frameworks. Brazil's 2024 Clinical Research Law accelerates approvals for digital health studies, drawing analytics vendors into Latin America.

- Allscripts

- Oracle

- IBM (Merative)

- Mckesson

- MedeAnalytics

- Optum

- SAS Institute

- Verisk Analytics

- Epic Systems

- Health Catalyst

- Dimensional Insight

- Innovaccer

- Arcadia

- Clarify Health Solutions

- Change Healthcare

- Koninklijke Philips

- Siemens Healthineers

- GE Healthcare

- Qlik

- Teradata

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Integration of Big Data & AI in Healthcare

- 4.2.2 Growing Need for Cost Containment & Operational Efficiency

- 4.2.3 Incentives for Value-Based Care & Outcome-Based Reimbursement

- 4.2.4 Rise of Patient Digital Twins for Therapy Optimization

- 4.2.5 Real-time Prescription Benefit (RTPB) Mandate Fuelling Point-of-Care Analytics

- 4.2.6 Surge in Chronic Disease Burden

- 4.3 Market Restraints

- 4.3.1 Data Security & HIPAA/GDPR Compliance Challenges

- 4.3.2 Shortage of Analytics Talent in Clinical Settings

- 4.3.3 Model Explainability Limitations Hindering Physician Trust

- 4.3.4 High Initial Investment Costs

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Application

- 5.1.1 Clinical Decision Support

- 5.1.2 Financial Analytics

- 5.1.3 Administrative / Operational Analytics

- 5.1.4 Research & Population Health Analytics

- 5.2 By Product

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.3 By Deployment Model

- 5.3.1 On-Premise

- 5.3.2 Cloud-Based

- 5.3.3 Hybrid

- 5.4 By End User

- 5.4.1 Healthcare Providers

- 5.4.2 Healthcare Payers

- 5.4.3 Pharmaceutical & Life-Sciences Companies

- 5.4.4 Government & Public-Health Agencies

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Allscripts Healthcare Solutions

- 6.3.2 Oracle Corporation (Cerner Corporation)

- 6.3.3 IBM (Merative)

- 6.3.4 McKesson Corporation

- 6.3.5 MedeAnalytics Inc.

- 6.3.6 Optum Inc.

- 6.3.7 SAS Institute Inc.

- 6.3.8 Verisk Analytics Inc.

- 6.3.9 Epic Systems Corporation

- 6.3.10 Health Catalyst

- 6.3.11 Dimensional Insight

- 6.3.12 Innovaccer

- 6.3.13 Arcadia

- 6.3.14 Clarify Health Solutions

- 6.3.15 Change Healthcare

- 6.3.16 Philips Healthcare

- 6.3.17 Siemens Healthineers

- 6.3.18 GE Healthcare

- 6.3.19 Qlik

- 6.3.20 Teradata

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment