|

시장보고서

상품코드

1850186

중국의 당뇨병 기기 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)China Diabetes Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

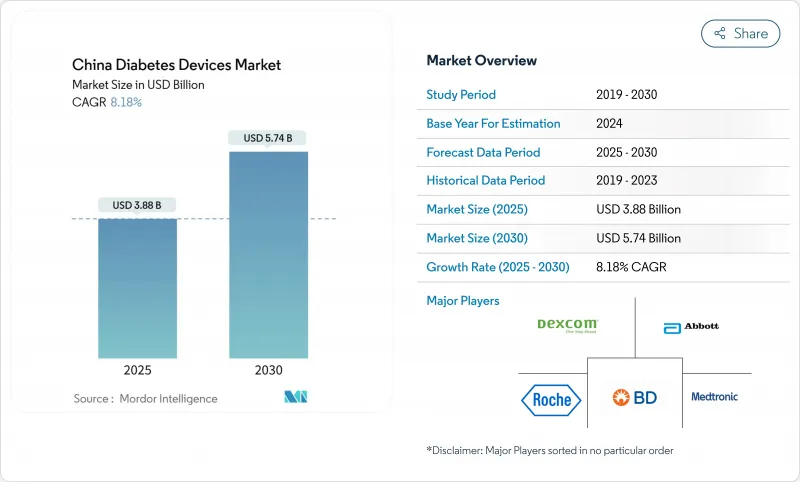

중국 당뇨병 기기 시장의 2025년 시장 규모는 38억 8,000만 달러, CAGR 8.18%로 성장하고, 2030년에는 57억 4,000만 달러에 이를 것으로 예측됩니다.

2024년에는 성인 당뇨병 인구가 1억 4,800만 명에 달했고 만성 질환 관리를 우선하는 '건강 중국 2030' 프로그램에 의한 지속적인 정책 지원이 성장을 지원합니다. 지속적인 포도당 모니터링(CGM) 시스템은 정밀도와 가격면의 이점을 결합한 국산 3세대 센서에 도움이 되며 기존 스트립 기반 검사를 대체합니다. 당뇨병 치료제의 보험 상환이 확대됨에 따라 모니터링 장비와 배달 장비에 대한 수요도 병행하여 높아지고 있으며, 디지털 치료 플랫폼이 충분한 서비스를 받지 못한 지역의 임상 결과를 개선하고 있습니다. 다국적기업과 현지기업에 의한 생산·연구개발시설에 대한 설비투자는 중국의 당뇨병 기기 시장 공급기반을 더욱 강화하고 있습니다.

중국 당뇨병 기기 시장 동향과 통찰

당뇨병 유병률 상승과 인구 고령화

중국의 당뇨병 유병률은 1980년의 1% 미만에서 2018년에는 12.4%로 상승했고, 2030년에는 1억 6,400만명에 달할 것으로 예측되고 있습니다. 도시화, 좌식 라이프스타일, 노인 인구의 확대(노인의 75% 이상이 적어도 하나의 만성 질환을 앓고 있음)로 의료기기 사용이 필요한 잠재적 사용자층이 계속 확대되고 있습니다. 연간 경제 비용은 10년 이내에 3,600억 위안을 초과할 것으로 예상되며, 효율적인 모니터링과 제공 기술에 관민 쌍방의 투자가 촉진됩니다.

정부의 헬스케어 개혁과 보험 적용 확대

2024년 국가상환약 목록(NRDL)의 갱신으로 15가지 품목의 당뇨병 치료제가 추가되어 자가 부담액이 즉시 낮아져 보완적인 장치의 도입이 촉진되었습니다. 도르자가리아틴(dorzagliatin)의 추가로 2024년 매출액은 2억 5,590만 위안(전년 대비 234% 증가)이 되었습니다. 농촌에서 인두불 시험을 통해 처방 기준이 개선되고 재정적 인센티브가 예방적 모니터링을 향하게 되었습니다.

첨단 의료기기의 고액의 자기 부담액

지속적인 포도당 모니터링과 인슐린 펌프 시스템은 상환 확대에도 불구하고 여전히 비쌉니다. 베이징의 고령 당뇨병 환자의 연간 약세는 이미 평균 12,186 위안(1,676달러)이며 장비를 업그레이드할 여지가 거의 없습니다. 펌프의 보급률은 0.5%에 그치고, 신흥국 시장에 대한 저렴한 제약이 부각되고 있습니다.

부문 분석

모니터링 장비는 2024년 매출의 60.21%를 차지했으며 중국의 당뇨병 기기 시장의 핵심 장비로서의 지위를 확고히 했습니다. CGM 매출은 2020년 8억 9,900만 위안에서 2030년에는 50억 3,200만 위안으로 급증할 것으로 예측되며, CAGR은 18.8%를 나타낼 전망입니다. 따라서 모니터링 장치의 중국 당뇨병 기기 시장 규모는 실시간 통찰력에 대한 소비자의 선호와 CGM 채택과 HbA1c 개선을 연관시키는 임상 증거로 시장 전체보다 빠르게 확대되고 있습니다. 자기 혈당 측정(SMBG) 장치는 특히 비용 의식이 높은 코호트에서 일상적인 검사에 필수적이지만 CGM 비용이 낮아짐에 따라 성장이 두드러집니다.

당뇨병 기기는 2025년부터 2030년까지 연평균 복합 성장률(CAGR) 9.10%로 성장할 전망입니다. 인슐린 펌프의 보급률은 2030년까지 0.5%에서 1.5%로 상승할 것으로 예상되며, 이는 신흥국 시장의 표준보다 여전히 낮지만 잠재 수요를 나타냅니다. 현재 해외 브랜드가 70% 이상의 점유율을 차지하고 있지만, 현지 제조업체는 블루투스 연결과 CGM 호환성을 펌프에 통합하기 시작하고 있어 조기 이익 획득을 목표로 하고 있습니다. 일부 병원의 조종사 테스트에서는 센서가 있는 펌프와 알고리즘 유도 투여를 결합하여 저혈당 에피소드가 2자리 비율로 감소하고 채택이 더욱 촉진되었습니다.

중국의 당뇨병 기기 시장 보고서는 기기 카테고리(관리 기기 및 모니터링 기기), 최종 사용자(병원 및 클리닉, 재택 관리 설정, 소매 약국 및 당뇨병 센터), 유통 채널(병원 약국, 소매 약국, 전자상거래/온라인 약국)으로 구분됩니다. 시장 세분화는 위 부문의 금액(단위: 달러) 및(단위: 단위)를 제공합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 중국에서 당뇨병 이환율의 상승과 인구의 고령화

- 정부의 헬스케어 개혁과 보험 적용 범위 확대

- 혈당 모니터링과 인슐린 투여에 있어서의 기술적 진보

- 가정용 기기의 저가격화

- 디지털 헬스와 원격 의료의 도입 확대

- 민간 및 공립 병원 인프라의 확대

- 시장 성장 억제요인

- 첨단 장치의 높은 본인 부담 비용

- 기기 사용에 관한 한정된 환자 교육 및 트레이닝

- 신규 기기에 대한 엄격하고 장기적인 규제 승인

- 저가의 규제되지 않은 제품과의 경쟁

- 가치/공급망 분석

- 규제와 기술 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 기기 카테고리별

- 모니터링 기기

- 자기 혈당 측정 장치(SMBG)

- 포도당 미터

- 테스트 스트립

- 란셋

- 연속 혈당 모니터링(CGM) 기기

- 센서

- 내구품(수신기 및 송신기)

- 관리 기기

- 인슐린 전달 장치

- 인슐린 펌프 장치

- 인슐린 일회용 펜

- 재사용 가능한 펜형 인슐린 카트리지

- 인슐린 주사기와 제트 주입기

- 모니터링 기기

- 최종 사용자별

- 병원 및 클리닉

- 재택 케어 환경

- 소매 약국과 당뇨병 센터

- 유통 채널별

- 병원 약국

- 소매 약국

- 전자상거래/온라인 약국

제6장 시장 지표

- 1형 당뇨병 환자수

- 2형 당뇨병 환자수

제7장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Roche Diagnostics

- Abbott Laboratories

- Sinocare Inc.

- Yuwell-Jiangsu Yuyue Medical

- Medtronic plc

- Dexcom Inc.

- Johnson & Johnson(LifeScan)

- Novo Nordisk A/S

- Becton, Dickinson and Company

- Ascensia Diabetes Care

- ARKRAY Inc.

- MicroTech Medical

- Lepu Medical Technology

- Tianjin MinFound Medical

- Sanofi

제8장 시장 기회와 장래의 전망

- 화이트 스페이스와 언멧 요구의 평가

The China diabetes devices market is valued at USD 3.88 billion in 2025 and is projected to reach USD 5.74 billion by 2030, reflecting an 8.18% CAGR.

Growth is underpinned by the country's 148 million-strong adult diabetic population in 2024 and by sustained policy support through the Healthy China 2030 program, which prioritizes chronic disease management. Continuous glucose monitoring (CGM) systems are displacing traditional strip-based testing, aided by domestic third-generation sensors that combine accuracy with price advantages. Broader reimbursement for diabetes medicines is spurring parallel demand for monitoring and delivery devices, while digital therapeutics platforms are improving clinical outcomes in underserved regions. Capital investment by multinational and local firms into production and R&D facilities further strengthens the supply base for the China diabetes devices market.

China Diabetes Devices Market Trends and Insights

Rising Diabetes Prevalence and Aging Population

Diabetes prevalence in China rose from below 1% in 1980 to 12.4% in 2018, and cases are projected to climb to 164 million by 2030. Urbanisation, sedentary lifestyles and an expanding older population-over 75% of older adults have at least one chronic disease-continue to enlarge the addressable pool of device users. Annual economic costs are expected to exceed RMB 360 billion within the decade, prompting both public and private investment in efficient monitoring and delivery technologies.

Government Healthcare Reforms and Insurance Coverage Expansion

National Reimbursement Drug List (NRDL) updates in 2024 added 15 diabetes drugs, immediately lowering out-of-pocket costs and stimulating complementary device uptake . Inclusion of dorzagliatin led to sales of RMB 255.9 million in 2024, up 234% year-on-year . Capitation payment pilots in rural counties have improved prescribing standards and redirect financial incentives toward preventive monitoring.

High Out-of-Pocket Costs for Advanced Devices

Continuous glucose monitoring and insulin pump systems remain expensive despite broader reimbursement. Annual medication costs already average RMB 12,186 (USD 1,676) for older diabetics in Beijing, leaving little room for device upgrades . Pump penetration stands at a modest 0.5%, underlining affordability constraints versus developed markets.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advancements in Glucose Monitoring and Insulin Delivery

- Growing Affordability of Domestic Devices

- Limited Patient Education and Training for Device Use

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Monitoring Devices generated 60.21% of revenue in 2024, cementing their status as the backbone of the China diabetes devices market. CGM sales are forecast to jump from RMB 899 million in 2020 to RMB 5.032 billion by 2030, registering an 18.8% CAGR. The China diabetes devices market size for Monitoring Devices therefore expands faster than the overall market, driven by consumer preference for real-time insights and by clinical evidence linking CGM adoption to improved HbA1c. Self-monitoring blood glucose (SMBG) devices remain essential for routine testing, especially in cost-conscious cohorts, but their growth plateaus as CGM costs fall.

Management Devices are set to grow at 9.10% CAGR between 2025 and 2030. Insulin pump penetration is expected to rise from 0.5% to 1.5% by 2030, still below developed-market norms but indicative of latent demand. Foreign brands presently hold more than 70% share, yet local manufacturers have begun integrating Bluetooth connectivity and CGM compatibility into pumps, positioning for quicker gains. In select hospital pilots, pairing sensor-augmented pumps with algorithm-guided dosing cut hypoglycemic episodes by double-digit percentages, further stimulating adoption.

The China Diabetes Devices Market Report is Segmented Into Device Category (Management Devices and Monitoring Devices), End User (Hospital and Clinics, Home-Care Settings, Retail Pharmacies & Diabetes Centers), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and E-Commerce / Online Pharmacies). The Market Provides the Value (in USD) and (in Units) for the Above-Mentioned Segments.

List of Companies Covered in this Report:

- Roche

- Abbott Laboratories

- Sinocare

- Yuwell-Jiangsu Yuyue Medical

- Medtronic

- Dexcom

- Johnson & Johnson

- Novo Nordisk

- Beckton Dickinson

- Ascensia

- Arkray

- MicroTech Medical

- Lepu Medical

- Tianjin MinFound Medical

- Sanofi

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Diabetes Prevalence and Aging Population in China

- 4.2.2 Government Healthcare Reforms and Insurance Coverage Expansion

- 4.2.3 Technological Advancements in Glucose Monitoring and Insulin Delivery

- 4.2.4 Growing Affordability of Domestic Devices

- 4.2.5 Increasing Adoption of Digital Health and Telemedicine

- 4.2.6 Expanding Private and Public Hospital Infrastructure

- 4.3 Market Restraints

- 4.3.1 High Out-of-Pocket Costs for Advanced Devices

- 4.3.2 Limited Patient Education and Training for Device Use

- 4.3.3 Stringent and Lengthy Regulatory Approval for Novel Devices

- 4.3.4 Competition from Low-Cost Unregulated Products

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory & Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Device Category

- 5.1.1 Monitoring Devices

- 5.1.1.1 Self-Monitoring Blood Glucose (SMBG) Devices

- 5.1.1.1.1 Glucometers

- 5.1.1.1.2 Test Strips

- 5.1.1.1.3 Lancets

- 5.1.1.2 Continuous Glucose Monitoring (CGM) Devices

- 5.1.1.2.1 Sensors

- 5.1.1.2.2 Durables (Receivers & Transmitters)

- 5.1.2 Management Devices

- 5.1.2.1 Insulin Delivery Devices

- 5.1.2.1.1 Insulin Pump Devices

- 5.1.2.1.2 Insulin Disposable Pens

- 5.1.2.1.3 Insulin Cartridges in Re-usable Pens

- 5.1.2.1.4 Insulin Syringes & Jet Injectors

- 5.1.1 Monitoring Devices

- 5.2 By End User

- 5.2.1 Hospitals & Clinics

- 5.2.2 Home-Care Settings

- 5.2.3 Retail Pharmacies & Diabetes Centers

- 5.3 By Distribution Channel

- 5.3.1 Hospital Pharmacies

- 5.3.2 Retail Pharmacies

- 5.3.3 E-commerce / Online Pharmacies

6 Market Indicators

- 6.1 Type-1 Diabetes Population

- 6.2 Type-2 Diabetes Population

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 7.4.1 Roche Diagnostics

- 7.4.2 Abbott Laboratories

- 7.4.3 Sinocare Inc.

- 7.4.4 Yuwell-Jiangsu Yuyue Medical

- 7.4.5 Medtronic plc

- 7.4.6 Dexcom Inc.

- 7.4.7 Johnson & Johnson (LifeScan)

- 7.4.8 Novo Nordisk A/S

- 7.4.9 Becton, Dickinson and Company

- 7.4.10 Ascensia Diabetes Care

- 7.4.11 ARKRAY Inc.

- 7.4.12 MicroTech Medical

- 7.4.13 Lepu Medical Technology

- 7.4.14 Tianjin MinFound Medical

- 7.4.15 Sanofi

8 Market Opportunities & Future Outlook

- 8.1 White-Space & Unmet-Need Assessment