|

시장보고서

상품코드

1850963

무역 관리 소프트웨어 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Trade Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

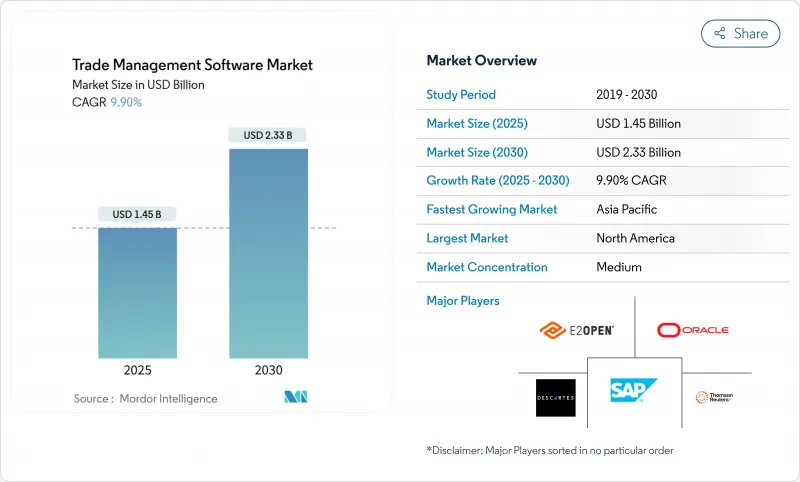

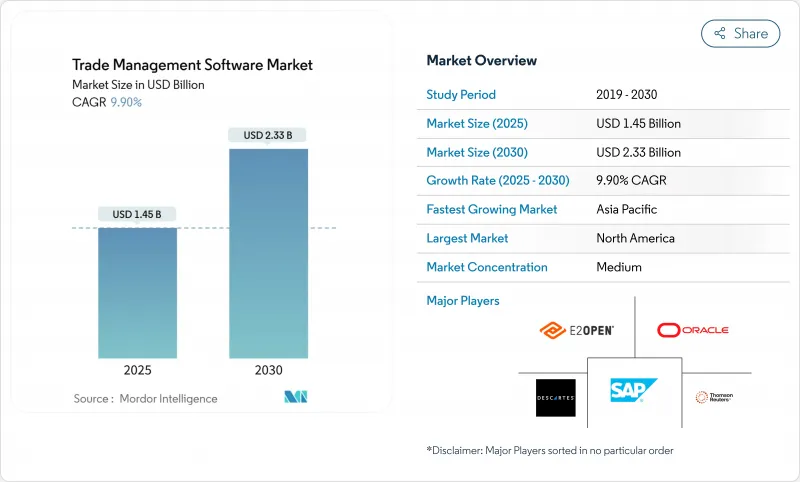

무역 관리 소프트웨어 시장의 2025년 시장 규모는 14억 5,000만 달러, 2030년에는 23억 3,000만 달러에 이르고, CAGR은 9.9%를 나타낼 전망입니다.

시장의 성장은 국제 무역 규칙의 강화, 관세 계획을 위한 디지털 트윈의 보급, 컴플라이언스 사이클을 단축하는 클라우드 퍼스트 아키텍처로의 명확한 전환으로 인한 것입니다. 미국의 첨단 컴퓨팅 품목에 대한 수출 규제 갱신과 유럽 연합의 탄소 국경 조정 메커니즘 등의 규제 변경으로 기업은 컴플라이언스 툴의 현대화를 강요받고 있습니다. 동시에 AI를 활용한 시나리오 계획 엔진이 스크리닝, 문서 작성, 관세 최적화를 통합한 플랫폼에 대한 수요를 끌어올리고 있습니다. 공급업체는 벌칙을 완화하고 항구에서의 체류 시간을 최소화하며 엔드 투 엔드 화물의 가시성을 유지하기 위한 실시간 분석을 강조합니다. 업계 재편도 대기업이 틈새 전문가를 인수함으로써 가속화되고 있습니다. 이는 세관, 물류, 재고, 지속가능성 리포팅을 상호 연결하는 단일 스택 시스템을 구축하기 위해 와이즈텍 세계이 2025년 E2open을 인수한 것으로 대표됩니다.

세계 무역 관리 소프트웨어 시장 동향과 통찰

클라우드 우선 배포로 컴플라이언스 비용 절감

클라우드 플랫폼은 On-Premise 하드웨어와 관련된 유지 관리 비용을 제거하고 총 소유 비용을 30-40% 절감하며 모든 규모의 기업에 고급 컴플라이언스 기능을 제공합니다. 컨텐츠를 자동으로 업데이트하면 규칙 세트가 항상 최신 상태로 유지되므로 사용자는 규제 변경에 45% 신속하게 대응할 수 있으며 벌칙을 35% 줄일 수 있습니다. 이 모델은 CIO의 86%가 2025년까지 퍼블릭 클라우드 워크로드를 재조정할 계획이며 유연한 호스팅 패턴에 대한 수요를 보여줍니다. 공급업체는 ERP 및 TMS 제품군에 신속한 API 커넥터를 제공하여 통합 기간을 단축하고 투자 회수를 가속화합니다. 이러한 이점이 결합되어 수출입 기업은 클라우드의 도입을 단순한 기술교환이 아닌 전략적인 테코로 취급하게 되었습니다.

수출규제 강화가 투자에 박차를 가한다.

2025년 1월 미국에서 시행된 첨단 컴퓨팅 품목과 AI 모델 가중치에 관한 규제는 라이선스 의무를 확대하고 감사 리스크를 높이고 있습니다. 유럽에서 논의된 유사한 조치는 컴플라이언스 부담을 더욱 증가시킵니다. 기업은 현재 실시간 제한된 파티 스크리닝, 동적 라이선스 워크플로우 및 변조 방지 감사 추적을 요구하고 있습니다. 2024년 컴플라이언스 위반에 대한 기록적인 처벌은 특히 반도체, 항공우주 및 이중 청소년 부문에서 업그레이드를 신속하게 진행하도록 이사회를 설득했습니다. 스크리닝, 관세 분류, 자동 생성 문서를 융합한 플랫폼은 수작업 체크를 줄이고 화물을 더 빠르게 이동시킬 수 있기 때문에 인기를 얻고 있습니다.

무역 규정 준수 데이터 사이언스자 부족

애널리틱스와 수출관리의 전문지식을 융합시킨 전문가에 대한 수요가 공급을 웃돌고 있습니다. 신흥 시장에서는 인재가 유출되고, 현지 기업은 외부 컨설턴트에 의존하지 않을 수 없게 되어 핀치를 맞이하고 있습니다. 인력 부족은 예측 듀티 엔진의 모델 구축 주기를 늘리고 도입 초기에 전체 기능의 채택을 제한합니다. 이에 대응하기 위해 공급업체는 가이드 워크플로우와 로우코드 툴을 통합하고 있지만, 노동력 격차는 급속한 스케일링 브레이크가 되고 있습니다.

부문 분석

솔루션 부문은 2024년 매출의 65.09%를 차지하며 제한된 당사자 스크리닝, 원산지 관리 및 관세 최적화를 자동화하는 도구에 대한 왕성한 수요를 반영합니다. 2024년 솔루션 무역 관리 소프트웨어 시장 규모는 9억 4,000만 달러로 수출업체가 오류를 줄이고 통관 워크플로우를 가속화하는 단일 대시보드를 요구하고 있기 때문에 확대가 계속되고 있습니다. Oracle, SAP 및 데카르트는 핵심 무역 데이터세트에 과세, ESG, 보안 워크플로우를 중첩합니다.

서비스 파트너는 설정, 변경 관리 및 사용자 교육을 관리합니다. 2025-2030년의 CAGR은 12.5%로 예측되고 있습니다. 공급자는 HS 코드 라이브러리를 유지하고 규칙의 진화에 따라 문서를 적응시키기 때문에 소프트웨어 + 서비스 번들을 구입하는 기업은 더 빠른 ROI를 보장할 수 있습니다. 권고 애드온은 CBAM 배출 공개 매핑을 지원하고 구독 지원은 24시간 365일 모니터링, 포털 유지 및 감사 지원을 다룹니다. 이와 같은 메커니즘을 통해 이전에 대규모 컴플라이언스 팀에 불과했던 전문 지식을 소규모 수입업체가 사용할 수 있습니다.

클라우드 도입은 2024년 지출의 68.53%를 차지하며, 2030년까지 15.3%의 연평균 복합 성장률(CAGR)로 성장하여 무역 관리 소프트웨어 시장에서 가장 큰 점유율을 유지할 것으로 예측됩니다. SaaS 구독은 자본 비용을 절감하고 모든 노드에서 규제 자동 업데이트를 제공합니다. 데이터 주권을 요구하는 은행과 방위 관련 기업 사이에서는 관리된 데이터를 On-Premise에 두고, 기밀성이 낮은 기능은 확장 가능한 클라우드를 경유하는 하이브리드 모델이 대두하고 있습니다.

한 업계 조사에 따르면 CIO의 86%가 2025년까지 일부 워크로드를 프라이빗 클라우드로 이전하여 대기 시간과 비용 최적화를 목표로 한다고 합니다. 공급업체는 퍼블릭, 프라이빗 또는 에지 노드에서 원활하게 작동하는 컨테이너화된 마이크로서비스를 출하함으로써 대응하고 있습니다. 항구의 에지 배포는 세관 체크포인트 근처에서 문서를 처리하므로 대기 시간이 단축되고 체류 시간이 단축됩니다. 이 멀티모달 아키텍처를 통해 기업은 컴플라이언스 컨텐츠를 설치 간에 리스크 허용도를 미세 조정하면서 동기화할 수 있어 대응 가능한 무역 관리 소프트웨어 시장을 확대할 수 있습니다.

무역 관리 소프트웨어 시장은 구성요소별(솔루션과 서비스), 도입 형태별(온클라우드와 On-Premise), 조직 규모별(중소기업과 대기업), 최종사용자 산업별(운송 및 물류, 소비재 및 소매, 제약과 생명과학 등), 지역별로 분류됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

북미는 2024년 무역 관리 소프트웨어 시장 수익의 40%를 유지, 세계 톱 클래스의 IT 인프라와 진행 중인 수출 규제 개혁이 뒷받침하고 있습니다. 미국에서는 2025년에 AI 모델의 가중치가 규제되기 때문에 기술, 항공우주, 반도체 수출업체는 실시간으로 라이선스 범위를 감사하는 대시보드 도입에 박차를 가합니다. 소매 기업은 조달 옵션과 관세 시나리오를 테스트하기 위해 디지털 트윈을 도입하고 새로운 공급망 보안 협정은 종합적인 컴플라이언스 엔진에 대한 수요를 강화하는 추가 보고서를 부과합니다.

2030년까지 연평균 복합 성장률(CAGR) 14.8%로 아시아태평양이 가장 급성장할 것으로 예측됩니다. RCEP의 관계 심화, 활황을 나타내는 국경을 넘은 전자상거래, 디지털 무역에 대한 정부 보조금이 투자를 촉진하고 있습니다. 중소기업은 수출업체 수의 대부분을 차지하고 있지만, 훈련을 받은 컴플라이언스 담당자가 없는 경우가 많습니다. 또한 싱가포르와 베트남과 같은 경제 지역에서는 단일 창 세관 포털이 공급업체의 API에 직접 연결되어 컴플라이언스를 준수하는 화물의 통관 시간을 단축하고 있습니다.

유럽은 2026년부터 완전히 시행되는 CBAM을 중심으로 무역 프로세스를 재구성하고 있습니다. 철강, 시멘트 및 알루미늄 수입업체는 임베디드 배출량을 추적하고 탄소 증명서를 구매해야 하므로 공급업체의 탄소 데이터와 통관 엔트리를 연결하는 시스템에 대한 투자를 촉진하고 있습니다. 디지털 트윈을 통해 계획 담당자는 탄소 지출을 최소화하는 조달 변경을 테스트할 수 있습니다. 한편 기업은 CBAM 데이터 세트를 Intrastat 및 Import Control System 신고와 단일 인터페이스로 통합하여 중복 작업 및 데이터 입력 실수를 줄이는 것을 목표로 하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 클라우드 퍼스트 도입으로 컴플라이언스 비용 절감

- 수출관리 체제 강화가 지출 촉진

- 옴니채널 물류와 3PL 통합의 대두

- 시나리오 가격 설정을 위한 관세 디지털 트윈

- ESG 연동 관세 우대 조치와 탄소 국경세

- 국경 간 무역 활동의 성장

- 시장 성장 억제요인

- 분산된 기존 IT로 시스템 통합 지연

- 무역준수 데이터 데이터 과학자 부족

- 중소기업의 도입을 위한 높은 초기 비용

- 지정학적 소프트웨어 제재로 인한 공급업체 봉쇄 위험

- 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 거시 경제 요인이 시장에 미치는 영향

제5장 시장 규모와 성장 예측

- 구성요소별

- 솔루션

- 벤더 관리

- 수출입 관리

- 송장과 세금관리

- 규정 준수 및 위험 분석

- 서비스

- 컨설팅

- 구현 및 통합

- 지원 및 유지 보수

- 솔루션

- 전개 모델별

- 클라우드

- On-Premise

- 조직 규모별

- 중소기업

- 대기업

- 최종 사용자 업계별

- 운송 및 물류

- 소비재 및 소매업

- 의약품 및 생명과학

- 에너지 및 유틸리티

- 국방 및 항공우주

- 전자 및 첨단 기술

- 기타 산업

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 러시아

- 스페인

- 스위스

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 싱가포르

- 베트남

- 인도네시아

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 나이지리아

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- SAP SE

- Oracle Corporation

- Thomson Reuters(ONESOURCE)

- Descartes Systems Group

- E2open LLC

- WiseTech Global

- Infor Nexus

- AEB SE

- Bamboo Rose LLC

- MIC Customs Solutions

- Livingston International

- Expeditors International

- Accuity

- 3rdwave

- Blume Global

- CargoSmart Ltd.

- Customs4trade

- Freightgate Inc.

- Aptean TradeBeam

- BluJay Solutions(K'rber)

제7장 시장 기회와 장래의 전망

SHW 25.11.11The trade management software market is valued at USD 1.45 billion in 2025 and is expected to reach USD 2.33 billion by 2030, translating into a 9.9% CAGR.

The market's growth stems from tighter international trade rules, widespread deployment of digital twins for tariff planning, and a distinct move toward cloud-first architectures that trim compliance cycles. Regulatory changes such as the U.S. export-control update on advanced computing items and the European Union's Carbon Border Adjustment Mechanism are compelling firms to modernize compliance tools. At the same time, AI-enabled scenario-planning engines are pushing demand for unified platforms that consolidate screening, document generation, and duty optimization. Vendors are stressing real-time analytics to lower penalties, minimize dwell time at ports, and sustain end-to-end shipment visibility. Industry consolidation is also quickening as larger players acquire niche specialists which is exemplified by WiseTech Global's 2025 takeover of E2open to build single-stack systems that interlink customs, logistics, inventory, and sustainability reporting.

Global Trade Management Software Market Trends and Insights

Cloud-first deployments cut compliance cost

Cloud platforms remove on-premise hardware and related maintenance outlays, lowering total ownership costs by 30-40% and extending advanced compliance functionality to firms of all sizes.Automatic content updates keep rule sets current, allowing users to react 45% faster to regulatory changes and cut penalties by 35%. The model aligns with plans by 86% of CIOs to rebalance public-cloud workloads by 2025, signaling demand for flexible hosting patterns. Vendors include rapid API connectors to ERP and TMS suites, shrinking integration timelines and speeding returns on investment. Together, these benefits push importers and exporters to treat cloud deployment as a strategic lever rather than a simple technology swap.

Tightening export-control regimes spur spending

The January 2025 U.S. regulations on advanced computing items and AI model weights broaden license obligations and heighten audit risk. Similar measures under discussion in Europe further enlarge the compliance burden. Firms now require real-time restricted-party screening, dynamic license workflows, and tamper-proof audit trails. Record penalties for non-compliance in 2024 convinced boards to fast-track upgrades, especially in semiconductor, aerospace, and dual-use sectors. Platforms that blend screening, tariff classification, and auto-generated documents gain traction because they cut manual checks and move cargo faster.

Shortage of trade-compliance data scientists

Demand for professionals who blend analytics with export-control expertise is outrunning supply. Emerging markets feel the pinch as talent migrates, leaving local firms to lean on external consultants. The scarcity lengthens model-building cycles for predictive duty engines and limits full-feature adoption in early deployment years. To counter, suppliers embed guided workflows and low-code tools, but labor gaps remain a brake on rapid scaling world.

Other drivers and restraints analyzed in the detailed report include:

- Rise of omni-channel logistics and 3PL integration

- Customs-duty digital twins for scenario pricing

- Fragmented legacy IT slows system integration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Solutions segment held 65.09% of revenue in 2024, reflecting intense demand for tools that automate restricted-party screening, origin management, and duty optimization. The trade management software market size for Solutions stood at USD 0.94 billion in 2024 and continues to expand as exporters seek single dashboards that cut errors and speed clearance workflows. Oracle, SAP, and Descartes are layering taxation, ESG, and security workflows onto core trade data sets.

Service partners manage configuration, change control, and user training. The Services slice is projected at a 12.5% CAGR from 2025-2030. Enterprises buying software-plus-service bundles secure quicker ROI because providers maintain HS code libraries and adapt documents as rules evolve. Advisory add-ons help customers map CBAM emission disclosures, while subscription support covers 24X7 monitoring, portal upkeep, and audit assistance. Collectively, this structure allows smaller importers to access expertise that once sat only in large compliance teams.

Cloud deployments captured 68.53% of 2024 spending and are forecast to grow at a 15.3% CAGR through 2030, sustaining the largest slice of the trade management software market. SaaS subscriptions cut capital cost and deliver automatic regulatory updates across every node. Hybrid models emerge among banks and defense contractors seeking data sovereignty, keeping controlled data on-premise while routing less-sensitive functions through scalable clouds.

An industry survey shows 86% of CIOs will repatriate select workloads to private cloud by 2025, aiming for optimized latency and cost. Vendors counter by shipping containerized microservices that run seamlessly on public, private, or edge nodes. Edge deployments at ports process documentation close to customs checkpoints, lowering latency and shrinking dwell time. This multi-modal architecture lets companies fine-tune risk tolerance while holding compliance content in sync across installations, thereby enlarging the addressable trade management software market.

Trade Management Software Market is Segmented by Component (Solution and Service), Deployment (On-Cloud and On-Premise), Organization Size (Small and Medium Enterprises and Large Enterprises), End-User Industry (Transportation and Logistics, Consumer Goods and Retail, Pharmaceuticals and Life-Sciences, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 40% of trade management software market revenue in 2024, helped by world-class IT infrastructure and ongoing export-control reforms. The 2025 U.S. controls on AI model weights spur technology, aerospace, and semiconductor exporters to install dashboards that audit license coverage in real time. Retailers deploy customs digital twins to test sourcing alternatives and tariff scenarios, while new supply-chain security pacts impose extra reporting layers that strengthen demand for comprehensive compliance engines.

The Asia-Pacific region is projected to grow the fastest, with a 14.8% CAGR through 2030. Deeper RCEP ties, booming cross-border e-commerce, and government subsidies for digital trade are driving investment. SMEs dominate exporter counts yet often lack trained compliance officers. Low-cost, multilingual cloud suites offering wizard-driven classification and instant certificates of origin fill the gap, and single-window customs portals in economies like Singapore and Vietnam link directly to vendor APIs, cutting clearance times for compliant shipments.

Europe is restructuring trade processes around the CBAM, fully enforced from 2026. Importers of steel, cement, and aluminum must track embedded emissions and purchase carbon certificates, prompting investment in systems that link supplier carbon data with customs entries. Digital twins allow planners to test sourcing changes that minimize carbon outlays, while enterprises aim to merge CBAM datasets with Intrastat and Import Control System filings inside a single interface, reducing duplicate effort and data-entry errors.

- SAP SE

- Oracle Corporation

- Thomson Reuters (ONESOURCE)

- Descartes Systems Group

- E2open LLC

- WiseTech Global

- Infor Nexus

- AEB SE

- Bamboo Rose LLC

- MIC Customs Solutions

- Livingston International

- Expeditors International

- Accuity

- 3rdwave

- Blume Global

- CargoSmart Ltd.

- Customs4trade

- Freightgate Inc.

- Aptean TradeBeam

- BluJay Solutions (K'rber)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-first deployments cut compliance cost

- 4.2.2 Tightening export-control regimes spur spending

- 4.2.3 Rise of omni-channel logistics and 3PL integration

- 4.2.4 Customs-duty digital twins for scenario pricing

- 4.2.5 ESG-linked tariff incentives and carbon border taxes

- 4.2.6 Growth in cross-border trade activities

- 4.3 Market Restraints

- 4.3.1 Fragmented legacy IT slows system integration

- 4.3.2 Shortage of trade-compliance data scientists

- 4.3.3 High upfront cost for SME adoption

- 4.3.4 Geopolitical software-sanctions risk vendor lock-out

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 Vendor Management

- 5.1.1.2 Import/Export Management

- 5.1.1.3 Invoice and Duty Management

- 5.1.1.4 Compliance and Risk Analytics

- 5.1.2 Services

- 5.1.2.1 Consulting

- 5.1.2.2 Implementation and Integration

- 5.1.2.3 Support and Maintenance

- 5.1.1 Solutions

- 5.2 By Deployment Model

- 5.2.1 Cloud

- 5.2.2 On-Premise

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By End-user Industry

- 5.4.1 Transportation and Logistics

- 5.4.2 Consumer Goods and Retail

- 5.4.3 Pharmaceuticals and Life-Sciences

- 5.4.4 Energy and Utilities

- 5.4.5 Defense and Aerospace

- 5.4.6 Electronics and High-Tech

- 5.4.7 Other Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Spain

- 5.5.3.7 Switzerland

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Malaysia

- 5.5.4.6 Singapore

- 5.5.4.7 Vietnam

- 5.5.4.8 Indonesia

- 5.5.4.9 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 Nigeria

- 5.5.5.2.2 South Africa

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Thomson Reuters (ONESOURCE)

- 6.4.4 Descartes Systems Group

- 6.4.5 E2open LLC

- 6.4.6 WiseTech Global

- 6.4.7 Infor Nexus

- 6.4.8 AEB SE

- 6.4.9 Bamboo Rose LLC

- 6.4.10 MIC Customs Solutions

- 6.4.11 Livingston International

- 6.4.12 Expeditors International

- 6.4.13 Accuity

- 6.4.14 3rdwave

- 6.4.15 Blume Global

- 6.4.16 CargoSmart Ltd.

- 6.4.17 Customs4trade

- 6.4.18 Freightgate Inc.

- 6.4.19 Aptean TradeBeam

- 6.4.20 BluJay Solutions (K'rber)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment