|

시장보고서

상품코드

1910568

바닥재 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Floor Covering - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

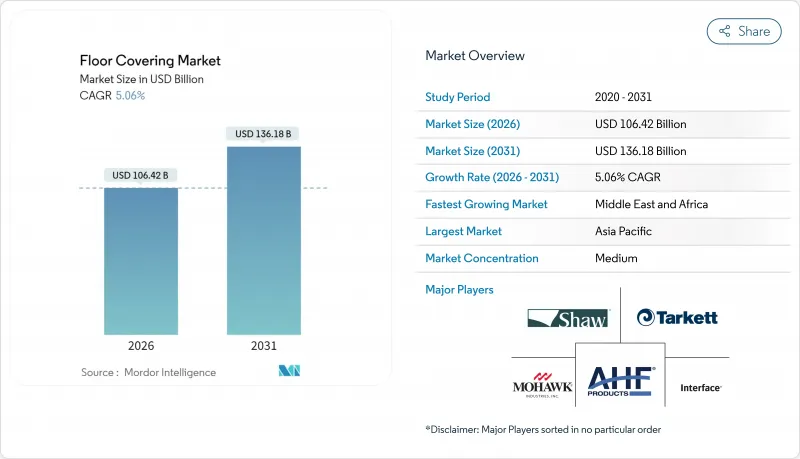

세계의 바닥재 시장은 2025년 1,012억 8,000만 달러로 평가되었으며, 2026년 1,064억 2,000만 달러에서 2031년까지 1,361억 8,000만 달러에 이를 것으로 예측됩니다. 예측 기간 중 (2026-2031년) CAGR은 5.06%로 예상됩니다.

북미의 견조한 주택 개수 수요, 아시아태평양에서의 대규모 프로젝트 활동, 중동 전역에서의 호스피탈리티 건설의 회복이 결합되어, 고품질이며 수명이 긴 바닥재에 대한 수요를 지지하고 있습니다. 리지드 코어 방수 판자나 PVC 프리 탄성 바닥재와 같은 기술 혁신에 의해 용도의 폭이 넓어져, 공급업자는 습기가 많은 지하실에서 교통량이 많은 상업 통로까지, 설계상의 큰 타협 없이 대응할 수 있게 되었습니다. 제조업체 각사는 관세 리스크 회피, 리드 타임 단축, 엄격한 VOC 배출 규제에 대응을 목적으로 미국의 생산지를 확대하고 있습니다. 이 전략은 국제 운송 혼란에 대한 공급망의 내성을 강화하는 것입니다. 전자상거래는 증강현실(AR) 시각화 툴과 소비자용 직송 물류를 융합시킴으로써 구매 프로세스를 변화시키고 있으며, 홈센터 체인은 가상디자인 상담과 클릭 앤 콜렉트 서비스의 도입을 촉진하고 있습니다. 경쟁 차별화는 환경인증으로 이행하고 있으며, 재생재배합 및 회수재활용 프로그램이 기업조달 사양의 결정적 요소가 되어 LEED, BREEAM, WELL 기준이 일상적으로 참조되게 되었습니다.

세계의 바닥재 시장 동향과 통찰

급속한 도시화와 활황을 나타내는 리노베이션 활동

인도의 도시 인구만으로도 2025년까지 5억명을 돌파할 것으로 예측되고 있으며, 이 구조적 변화에 더해 북미 전역에서 주택 고령화가 더해져, 모기지 금리가 신축 물건공급량을 억제하는 가운데, 개수 지출은 고수준을 유지하고 있습니다. 기존 주택 재판매 사이클은 바닥재 업그레이드와 강한 상관관계에 있습니다. 이는 주인이 부동산을 판매할 준비를 할 때 일반적으로 오래된 카펫이나 누락된 타일을 교체하기 때문입니다. 상업용 부동산 소유자도 마찬가지로 하이브리드 오피스 전략에 대응하기 위해 직장 개수를 진행하고 있습니다. 이것은 파티션과 가구의 빈번한 재배치를 견디며 표면 마감의 무결성을 손상시키지 않는 바닥재를 요구합니다. 에너지 절약 개수에 연동한 지자체의 인센티브에서는 바닥재 교환 보조금이 건물의 외벽 개수 프로그램과 조합되는 경우가 많아, 저 VOC 접착제나 재생재 밑바닥재의 채용을 촉진하고 있습니다. 신흥 아시아태평양 도시에서는 지방자치단체가 고층 주택에 미끄러지지 않고 청소하기 쉬운 바닥재를 의무화하는 최저 생활기준을 추진하는 가운데 공영주택의 현대화가 가속화되고 있습니다. 이러한 동시 진행 동향이 안정된 기반 수요를 확보하고 신축 수요의 주기적인 침체로부터 바닥재 시장을 보호합니다. 풍부한 디자인과 신속 시공 시스템을 결합한 공급업체는 최소한의 가동 정지 시간이 중요한 소유자 거주 및 임대 물건 모두에서 수요를 포착하는 최적의 입장에 있습니다.

연질 표면에서 경질 표면으로 전환

소비자의 기호는 방수성, 내상성 및 신속한 위생 관리를 겸비한 표면재로 명확하게 시프트하고 있어 반려동물이나 아이가 있는 바쁜 가정에서는 경질 고급 비닐 타일이 사양 리스트의 가장 위로 뛰어올랐습니다. 이 경향은 개의 사육률 상승이나 오픈 콘셉트 인테리어 등, 생활양식의 변화를 반영하고, 액체의 유출이 방안을 자유롭게 퍼지는 환경에 대응하고 있습니다. 스톤 플라스틱 복합판은 오크나 히코리, 연마된 콘크리트를 모방하면서도 온도 변화 하에서 치수 안정성을 유지하기 때문에 선룸이나 반공조 지하실에의 적응 범위가 넓어지고 있습니다. 카펫 제조업체는 럭셔리한 쾌적성과 방음성이 유지관리상의 우려를 웃도는 고급 호텔 스위트용 프리미엄 브로드 룸 등, 틈새 이용 사례에 재배치를 진행하고 있습니다. 소매 구매자는 현재 독립적인 내압흔성 및 내오염성 시험을 통해 제품 내구성을 평가 기준으로 하고 있으며, FloorScore나 GREENGUARD 등의 인증이 최종 선정에 있어서 중요성을 늘리고 있습니다. 경질 바닥재의 점유율 확대에 따라 흡음성 바닥재와 유연한 트랜지션 스트립 등 부속품 시장도 인접 분야에서 급성장하고 있습니다. 시공업자는 접착제가 불필요한 플로팅 클릭 시스템에 의해 프로젝트의 회전이 빨라졌다는 보고가 있어 숙련 노동자 부족을 부분적으로 보완하는 이점이 되고 있습니다. 향후 3년간 디지털 잉크 인쇄에 의한 심미성의 점진적인 향상은 장식 사이클을 충족할 것으로 예상되며, 유지보수가 낮은 경질 포맷의 매력을 더욱 확고하게 할 것입니다.

원재료 가격 변동

2023년 이후 PVC 수지, 도자기용 점토, 활엽수재는 분기 단위로 20% 이상의 가격 변동을 경험하고 있어 계약 입찰에서의 이익률 예측을 복잡화시키고 있습니다. 수입 의존도가 높은 시장에서는 환율 변동이 상품 가격 상승에 박차를 가하기 때문에 유통업체는 운전자금을 구속하는 높은 안전 재고를 유지할 수밖에 없고, 영향이 가장 빨리 나타나게 됩니다. 수지 선물의 선매는 비용 헤지가 가능하지만, 디자인 사이클이 변화했을 경우, 재고 진부화의 리스크에 기업을 노출시킵니다. 가격 변동은 대체 소재로 전환하도록 촉구합니다. 예를 들어, 예산이 부족할 경우 고객은 오크에서 자작나무로, 또는 유약 세라믹에서 연마된 콘크리트 오버레이로 사양을 낮출 수 있습니다. 소규모 시공업체는 계약에 가격 개정 조항이 포함되는 경우가 드물기 때문에 불균형한 고위험을 흡수할 수밖에 없습니다. 이러한 영향으로 바닥재 시장의 단기 성장은 억제되지만, 아시아와 북미에서의 생산능력 강화 후 수급 균형의 정상화에 따라 장기 전망은 여전히 양호합니다. 다양한 공급원과 다년간의 원료 조달 계약을 체결하는 공급업체는 위험을 제한하고 사양 작성자를 위한 가격 안정성을 유지합니다.

부문 분석

2025년 시점에서 탄성 바닥재가 31.78%로 최고 점유율을 차지하고 신속한 시공과 내수성을 중시하는 개수 및 신축 계획에 있어서의 우위성을 확인했습니다. 이 카테고리 내에서는 석질 플라스틱 복합재가 CAGR 11.10%로 확대되어 바닥재 시장 규모를 견인하고 있습니다. 이 페이스는 기존의 표면재에서는 볼 수 없으며 작업 시간을 줄이는 클릭식 시스템이 뒷받침하고 있습니다. 세라믹 타일은 높은 기계적 부하를 견디는 도자기의 개선으로 공항과 쇼핑 센터에서의 적용 범위가 넓어져 18.23%의 점유율을 유지했습니다. 목재 느낌의 비닐 바닥재 진출에도 불구하고, 목질 바닥재는 8.42%의 기반을 유지. 특히 엔지니어드 바닥재는 진짜 화장판의 미관과 바닥 난방 기초에서의 치수 안정성을 겸비하고 있기 때문에 지지를 확대하고 있습니다. 라미네이트 바닥재는 제조업체가 엣지 베벨을 밀봉 처리해, 기존에 비닐만이 제공하고 있던 24시간 방수 보증을 실현한 것으로, 연간 6.18% 성장했습니다. 카펫 및 에이리어 러그는 설치 면적의 31.45%를 차지했지만, 거실에서는 경질 바닥재에 점유율을 양도했습니다. 그러나 카펫 타일은 오픈 오피스의 모듈식 설계로 높은 수요를 유지하고 있습니다. 지속가능성은 횡단적인 우선 과제이며, 공급업체는 순환형 경제 조달 가이드라인에 부합하는 재생 PET 안감 및 PVC 프리 내마모층 도입을 추진하고 있습니다. 성능 향상과 환경 규제의 융합은 제품 혁신이 바닥재 시장 전체의 범주 구성을 형성하는 주요 원동력임을 지속적으로 보장합니다.

리지드 코어와 디지털 프린트 기술의 급성장은 가격 체계를 근본적으로 변화시켜 중가격대 제품이 프리미엄 목재나 석재의 영역에 끼워넣을 수 있게 하고 있습니다. 이는 약간의 비용으로 질감을 재현할 수 있기 때문입니다. 브랜드 각사는 또한 목재 베니어판과 코르크 패드 사이에 광물 코어를 사이에 둔 하이브리드 플랑크 등 복합 소재의 채용도 진행하고 있습니다. 이것에 의해 단열성을 확보하면서 습기의 침입을 막는 것이 가능해집니다. 세계의 원재료 가격이 안정화되는 가운데 채석 대리석이나 단단한 재료에 대해 복합재의 비용 우위성이 확대될 가능성이 있습니다. 이로 인해 건축가와 주택 소유자의 가치 인식이 재조정됩니다. 지역적인 선호도는 여전히 존재합니다(유럽에서는 광범위한 오크 판이, 동남아시아에서는 광택이 있는 도자기 타일이 선호되는 경향). 그러나 온라인 시각화 도구는 점차 스타일 선택을 균질화하고 세계적으로 통일된 패턴에 대한 수요 증가를 촉진하고 있습니다. 세라믹 및 카펫 분야는 치열한 경쟁에 직면하고 있지만, 미끄럼 저항, 방음 및 방오 기술의 혁신으로 이러한 소재가 우위를 발휘하는 틈새 시장은 유지되고 있습니다. 향후, 재생 가능 소재의 사용이나 리사이클 물류를 제품 스토리에 짜넣는 능력이, 확대하는 바닥재 시장에 있어서의 점유율 획득을 좌우하는 요인이 될 것입니다.

바닥재 시장 보고서는 제품별(카펫 및 에이리어 러그, 목질 바닥재, 세라믹 타일 바닥재, 라미네이트 바닥재, 비닐 바닥재, 석재 바닥재, 기타 제품), 최종 사용자별(상업시설, 주택), 유통 채널별(홈 센터, 플래그십 점포, 전문점, 기타), 지역별(북미, 기타)로 분류되어 있습니다. 시장 예측은 사용 가능한 정보에 따라 금액(달러)으로 제공됩니다.

지역별 분석

아시아태평양은 2025년 37.10% 점유율로 선두를 차지했습니다. 이는 도시에서 지속적인 주택 수요 증가와 매년 수백만 평방미터의 세라믹 및 탄성 바닥재를 소비하는 대도시 지역의 교통망 확장에 의해 지원됩니다. 인도의 부동산 로드맵은 2030년까지 1조 달러 규모 시장을 상정하고 있으며, 고층 아파트, 지방 도시 소매 거점, IT 캠퍼스 로비 등 복합 바닥재 수요로 이어집니다. 중국에서는 거시건전성 정책에 의해 투기적인 건설 착공이 억제되고 있지만, 에너지 절약형 외관에 의한 낡은 집합 주택의 개수가 계속되고, 이에 따라 내부 바닥재의 교환도 실시되고 있습니다. 958억 달러 규모에 달하는 베트남의 건설 업계는 정부 인프라 지출을 배경으로 연률 7%로 성장하고 있으며, 지하철역 및 산업 훈련센터를 위한 타일 수요가 안정적으로 증가하고 있습니다. 동남아시아의 누적 GDP 성장률 4.5%는 관광업의 회복을 뒷받침해 디자인성을 중시한 복합 목재 판재를 채용하는 부티크 호텔 개발을 촉진하고 있습니다.

북미는 30.95%의 점유율과 4.15%의 연평균 복합 성장률(CAGR)로 이어져, 주로 리폼 수요가 견인합니다. 에너지 절약 개수에 대한 세제 우대 조치에 의해 주택 소유자는 단열 및 방수 기능을 갖추고, 바닥 난방 개수와 통합 가능한 바닥재에, 구식 카펫의 교환을 진행하고 있습니다. 국내 LVT 생산은 운임 변동 위험을 줄이고 USMCA 협정은 캐나다 제재소와 멕시코 적층판 공장 간 원재료 유통을 원활하게 하고 있습니다. 유럽은 27.85%의 점유율과 3.06%의 연평균 복합 성장률(CAGR)을 유지하며 독일과 이탈리아의 리노베이션 프로그램이 기반을 두고 있습니다. 양국에서는 보조금에 의해 저 VOC(휘발성 유기 화합물) 마감재가 촉진되고 있습니다. 반면, REACH 규정은 엄격한 화학물질 기준을 설정하고 있으며, 적합하지 않은 수입품 시장 퇴출을 가속화하고 있습니다. 중동 및 아프리카는 현재 가장 소규모이지만 8.05%라는 가장 빠른 CAGR로 두드러지고 있습니다. 사우디아라비아의 'Vision 2030'에 의한 접객 산업의 급성장이 NEOM 등의 거대 프로젝트로 바닥재 수요를 확대하고 UAE의 주택 계획에서는 사막의 모래에 의한 마모에 견디는 대리석 느낌의 비닐이 채용되고 있습니다.

건축 기준의 지역 차이가 제품 구성에 차이를 낳고 있습니다. 유럽에서는 바닥 난방 효율을 충족시키는 클릭식 세라믹 하이브리드가 주류인 반면, 북미에서는 지하실 개수용으로 와이드 플랭크 SPC가 선호됩니다. 물류 인프라도 수요를 좌우하고, 아프리카의 항만 능력 향상은 중량급 도자기 수입의 루트를 개척하는 한편, 고급 별장용으로는 현지 채석장산 석재가 여전히 비용 효율이 뛰어나고 있습니다. 통화의 안정성은 라틴아메리카 전역의 수입 라미네이트 재료와 현지산 하드우드의 채택 선택에 영향을 미칩니다. 다만, 보다 광범위한 남미의 데이터는 조사 범위 외이며, 여기에서는 상세하게 설명하지 않습니다. 전반적으로 지리적 다양화는 바닥재 시장을 지역 경기 침체로부터 보호하고 세계적으로 안정적인 확장 궤도를 확보하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 급속한 도시화와 활황을 나타내는 개수 활동

- 연질 표면 바닥재로부터 경질 표면 바닥재(LVT, SPC, 목재형)로의 이행

- 아시아태평양(APAC) 및 중동 및 아프리카(MEA) 시장에서의 건설 붐

- 리지드 코어 및 방수 기술의 제품 혁신

- 미국에서 LVT 생산의 국내 회귀(관세 완화책)

- 의료 및 교육 시설에서의 항균 처리 바닥재 수요

- 시장 성장 억제요인

- 원재료 가격의 변동성(염화비닐 수지, 활엽수, 도자기)

- 플라스틱계 바닥재에 대한 환경 규제의 강화

- 자격을 가진 바닥 시공 기술자의 부족

- 관세 및 무역 정책 급변에 의한 수입 공급망 혼란

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품별

- 카펫 및 에이리어 러그

- 나무 바닥

- 세라믹 타일 바닥재

- 라미네이트 바닥재

- 비닐 바닥재

- 석재 바닥재

- 기타 제품

- 최종 사용자별

- 상업용

- 주택용

- 유통 채널별

- 홈센터

- 플래그십 점포

- 전문점

- 온라인 스토어

- 기타 유통 채널

- 지역별

- 북미

- 캐나다

- 미국

- 멕시코

- 남미

- 브라질

- 페루

- 칠레

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 베네룩스(벨기에, 네덜란드, 룩셈부르크)

- 북유럽 국가(덴마크, 핀란드, 아이슬란드, 노르웨이, 스웨덴)

- 기타 유럽

- 아시아태평양

- 인도

- 중국

- 일본

- 호주

- 한국

- 동남아시아(싱가포르, 말레이시아, 태국, 인도네시아, 베트남, 필리핀)

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 나이지리아

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Mohawk Industries

- Shaw Industries

- Tarkett SA

- Interface Inc.

- Armstrong Flooring/AHF Products

- Beaulieu International Group

- Gerflor Group

- Mannington Mills

- Milliken & Company

- Forbo Holding

- Congoleum Corporation

- Swiss Krono Group

- Boral Limited

- Orientbell Tiles

- Kajaria Ceramics

- Grupo Lamosa

- Ragno Ceramics

- Victoria PLC

- Roppe Corporation

- Ege Carpets

제7장 시장 기회와 미래 전망

SHW 26.01.26The floor covering market was valued at USD 101.28 billion in 2025 and estimated to grow from USD 106.42 billion in 2026 to reach USD 136.18 billion by 2031, at a CAGR of 5.06% during the forecast period (2026-2031).

Robust residential renovation in North America, megaproject activity in Asia-Pacific, and recovery in hospitality construction across the Middle East collectively anchor demand for premium, long-life surfaces. Technological breakthroughs such as rigid-core waterproof planks and PVC-free resilient options broaden application versatility, allowing suppliers to address both moisture-prone basements and high-traffic commercial corridors without major design compromises. Manufacturers are increasingly localizing production in the United States to sidestep tariff exposure, compress lead times, and meet stringent VOC emission rules, a strategy that also bolsters supply-chain resilience against global shipping disruptions. E-commerce is reshaping purchasing journeys by merging augmented-reality visualization tools with direct-to-consumer logistics, which is motivating home-center chains to integrate virtual design consultations and click-and-collect fulfillment. Competitive differentiation is shifting toward environmental credentials, with recycled-content formulations and take-back recycling programs becoming decisive in corporate procurement specifications that now routinely reference LEED, BREEAM, and WELL benchmarks.

Global Floor Covering Market Trends and Insights

Rapid Urbanization & Booming Renovation Activities

Urban populations in India alone are expected to top 500 million by 2025, and that structural shift, combined with aging housing stock across North America, keeps retrofit spending elevated even while mortgage rates temper new-build volumes. Existing-home resale cycles correlate strongly with flooring upgrades because owners typically replace outdated carpet or chipped tiles when preparing a property for listing. Commercial landlords are similarly retrofitting workplaces to support hybrid office strategies, which requires surfaces that tolerate frequent reconfiguration of partitions and furniture glides without losing finish integrity. Municipal incentives tied to energy-efficient retrofits often bundle floor replacement grants with broader envelope-upgrade programs, stimulating adoption of low-VOC adhesives and recycled underlayment. In emerging Asia-Pacific cities, public housing modernization is accelerating as provincial authorities push minimum living-standard codes that mandate non-slip, easy-clean floor materials in high-rise dwellings. These simultaneous dynamics ensure a consistent baseline demand that cushions the floor covering market against cyclical dips in new construction. Suppliers that package pattern-rich visuals and rapid-install systems are best positioned to capture volume across both owner-occupied and rental properties, where minimal downtime is critical.

Shift from Soft to Hard-Surface Flooring

Consumer attitudes have swung decisively toward surfaces that combine waterproof integrity, scratch resistance, and quick sanitation, propelling rigid luxury vinyl tile to the top of specification lists for busy households with pets and children. The move reflects lifestyle shifts such as rising dog ownership and open-concept interiors where spills travel unimpeded across rooms. Stone plastic composite boards emulate oak, hickory, or polished concrete yet remain dimensionally stable under temperature swings, which widens their suitability for sunrooms and semi-conditioned basements. Carpet manufacturers are repositioning toward niche use-cases like premium broadloom for high-end hospitality suites where plush comfort and acoustic dampening outweigh maintenance concerns. Retail buyers now benchmark product durability through independent indentation and stain-resistance tests, elevating the status of certifications such as FloorScore and GREENGUARD in final selection. As the hard-surface share widens, accessory markets for sound-absorbing underlayment and flexible transition strips experience adjacent growth spurts. Installers report quicker project turnover because floating-click systems eliminate the need for adhesives, a benefit that partially offsets skilled-labor shortages. Over the coming three years, incremental aesthetic gains from digital-ink printing are expected to satisfy decor cycles, further cementing the appeal of low-maintenance rigid formats.

Volatile Raw-Material Prices

PVC resin, ceramic clay, and hardwood lumber have experienced price swings exceeding 20% within single fiscal quarters since 2023, complicating margin forecasting for contract bids. Import-heavy markets feel the pinch fastest because currency fluctuations compound commodity spikes, compelling distributors to hold higher safety stocks that tie up working capital. Forward-buying resin futures can hedge costs but expose companies to inventory obsolescence if design cycles shift. Volatility encourages substitution; for example, customers may down-spec from oak to birch or from glazed porcelain to polished concrete overlays when budgets tighten. Smaller installers absorb disproportionately high risk because their contracts seldom include escalation clauses. The net effect trims near-term floor covering market growth, although the long-run outlook remains positive as supply-demand imbalances normalize post-capacity additions in Asia and North America. Suppliers that negotiate multi-year feedstock agreements with diversified sources limit exposure and maintain price stability for specification writers.

Other drivers and restraints analyzed in the detailed report include:

- Construction Boom in Asia-Pacific & MEA Markets

- On-shoring of LVT Production in the United States

- Environmental Scrutiny of Plastic-Based Flooring

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Resilient flooring commanded the highest share at 31.78% in 2025, confirming its dominance in renovation and new-build schedules that emphasize fast installation and water resistance. Within the category, stone plastic composite is propelling the floor covering market size by expanding at an 11.10% CAGR, a pace unmatched by traditional surfaces and aided by click systems that cut labor hours. Ceramic tiles held an 18.23% share thanks to porcelain improvements that now withstand high mechanical loads, widening their fit for airports and shopping centers. Wood flooring retained an 8.42% foothold despite encroachment from wood-look vinyl, with engineered formats gaining traction because they pair genuine veneer aesthetics with dimensional stability across radiant-heat subfloors. Laminate grew 6.18% yearly after manufacturers sealed edge bevels to deliver 24-hour water warranties, a feature once exclusive to vinyl. Carpet and area rugs still covered 31.45% of installed square footage, but ceded living-room ground to hard surfaces, even though carpet tiles thrive in open-office modular plans. Sustainability is a cross-cutting priority, pushing suppliers to introduce recycled PET backings and PVC-free wear layers that qualify under circular-economy procurement guidelines. The convergence of performance upgrades and environmental mandates ensures that product innovation remains the principal lever shaping category mix across the floor covering market.

The surge of rigid-core and digital-print capabilities fundamentally shifts pricing ladders, enabling mid-tier products to encroach on premium wood or stone positions by replicating texture nuances at a fraction of the cost. Brands are also embracing mixed materials such as hybrid planks that sandwich mineral cores between wood veneers or cork pads, delivering thermal comfort while guarding against moisture ingress. As global raw-material prices stabilize, cost advantages may widen for engineered composites over quarried marble or solid hardwood, realigning value perceptions among architects and homeowners. Geographic preferences persist-Europe still favors wide-plank oak while Southeast Asia leans toward glossy porcelain-but online visualization tools are gradually homogenizing style choices, funneling incremental volume toward globally consistent patterns. Although ceramic and carpet segments face stiff competition, innovations in slip-rating, acoustic insulation, and stain technology preserve niches where these materials outperform. In the future, the ability to weave renewable content and recycling logistics into product stories will increasingly determine which brands claim a share of the growing floor covering market size.

The Floor Covering Market Report is Segmented by Product (Carpet & Area Rugs, Wood Flooring, Ceramic Tiles Flooring, Laminate Flooring, Vinyl Flooring, Stone Flooring, Other Products), End User (Commercial, Residential), Distribution Channel (Home Centers, Flagship Stores, Specialty Stores, and Other), and Geography (North America, and Other). The Market Forecasts are Provided in Terms of Value (USD), Based On Availability.

Geography Analysis

Asia-Pacific led with 37.10% share in 2025, buoyed by unrelenting urban housing growth and megacity transportation expansions that consume millions of square meters of ceramic and resilient surfaces annually. India's real-estate roadmap envisions a USD 1 trillion sector by 2030, translating into compounded floor demand spanning high-rise condos, tier-III city retail hubs, and IT campus lobbies. China continues to retrofit older apartment blocks with energy-efficient facades that bundle interior floor replacement, although macroprudential controls temper speculative building starts. Vietnam's USD 95.8 billion construction sector grows at 7% annually on the back of government infrastructure outlays, reflecting steady tile uptake for metro stations and industrial training centers. Southeast Asia's cumulative 4.5% GDP growth propels tourism rebound, spurring boutique hotel developments that specify design-forward composite wood planks .

North America followed at 30.95% share and 4.15% CAGR, driven mainly by remodeling; stimulus tax incentives for energy-efficient retrofits encourage homeowners to swap outdated carpet for insulated, waterproof planks that integrate with radiant-heat upgrades. Domestic LVT production dampens exposure to freight volatility, and USMCA provisions facilitate raw-material flows between Canadian lumber mills and Mexican laminate plants. Europe maintained a 27.85% share and a 3.06% CAGR, anchored by renovation programs in Germany and Italy, where subsidies promote low-VOC finishes; meanwhile, the REACH regulation sets stringent chemical thresholds that accelerate market exit for non-compliant imports. The Middle East & Africa, albeit the smallest region today, stands out with the fastest 8.05% CAGR as Saudi Arabia's Vision 2030 hospitality boom expands flooring footprints in giga-projects like NEOM, and UAE residential schemes utilize marble-look vinyl that survives desert sand abrasion.

Regional variance in building codes produces product-mix differences: Europe leans toward click-ceramic hybrids to satisfy underfloor-heating efficiency, while North America favors wide-plank SPC for basement remodeling. Logistics infrastructure also shapes demand; Africa's improving port capacity opens routes for heavyweight porcelain imports while local quarry stone remains cost-effective for luxury villas. Currency stability influences the adoption of imported laminate versus locally milled hardwood across Latin America, though broader South American data were outside our input scope and are not elaborated here. Overall, geographic diversification balances the floor covering market against localized recessions, ensuring a globally steady expansion trajectory.

- Mohawk Industries

- Shaw Industries

- Tarkett SA

- Interface Inc.

- Armstrong Flooring / AHF Products

- Beaulieu International Group

- Gerflor Group

- Mannington Mills

- Milliken & Company

- Forbo Holding

- Congoleum Corporation

- Swiss Krono Group

- Boral Limited

- Orientbell Tiles

- Kajaria Ceramics

- Grupo Lamosa

- Ragno Ceramics

- Victoria PLC

- Roppe Corporation

- Ege Carpets

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid urbanisation & booming renovation activities

- 4.2.2 Shift from soft to hard-surface flooring (LVT, SPC, wood-look)

- 4.2.3 Construction boom in APAC & MEA markets

- 4.2.4 Product innovations in rigid-core & waterproof technologies

- 4.2.5 On-shoring of LVT production in the U.S. (tariff mitigation)

- 4.2.6 Demand for antimicrobial-treated floors in healthcare & education

- 4.3 Market Restraints

- 4.3.1 Volatile raw-material prices (PVC, hardwood, ceramics)

- 4.3.2 Environmental scrutiny of plastic-based flooring

- 4.3.3 Shortage of certified floor-installation labour

- 4.3.4 Tariff/trade-policy shocks disrupting import supply chains

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product

- 5.1.1 Carpet & Area Rugs

- 5.1.2 Wood Flooring

- 5.1.3 Ceramic Tiles Flooring

- 5.1.4 Laminate Flooring

- 5.1.5 Vinyl Flooring

- 5.1.6 Stone Flooring

- 5.1.7 Other Products

- 5.2 By End User

- 5.2.1 Commercial

- 5.2.2 Residential

- 5.3 By Distribution Channel

- 5.3.1 Home Centers

- 5.3.2 Flagship Stores

- 5.3.3 Specialty Stores

- 5.3.4 Online Stores

- 5.3.5 Other Distribution Channels

- 5.4 By Region

- 5.4.1 North America

- 5.4.1.1 Canada

- 5.4.1.2 United States

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.4.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.4.3.8 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 India

- 5.4.4.2 China

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 South Korea

- 5.4.4.6 South East Asia (SG, MY, TH, ID, VN, PH)

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East & Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East & Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Mohawk Industries

- 6.4.2 Shaw Industries

- 6.4.3 Tarkett SA

- 6.4.4 Interface Inc.

- 6.4.5 Armstrong Flooring / AHF Products

- 6.4.6 Beaulieu International Group

- 6.4.7 Gerflor Group

- 6.4.8 Mannington Mills

- 6.4.9 Milliken & Company

- 6.4.10 Forbo Holding

- 6.4.11 Congoleum Corporation

- 6.4.12 Swiss Krono Group

- 6.4.13 Boral Limited

- 6.4.14 Orientbell Tiles

- 6.4.15 Kajaria Ceramics

- 6.4.16 Grupo Lamosa

- 6.4.17 Ragno Ceramics

- 6.4.18 Victoria PLC

- 6.4.19 Roppe Corporation

- 6.4.20 Ege Carpets

7 Market Opportunities & Future Outlook

- 7.1 Circular-economy take-back & recycling platforms for post-consumer LVT

- 7.2 AI-guided virtual design tools that shorten specification-to-install cycle for commercial projects