|

시장보고서

상품코드

1940645

영국 마루 커버재 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United Kingdom Floor Covering - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

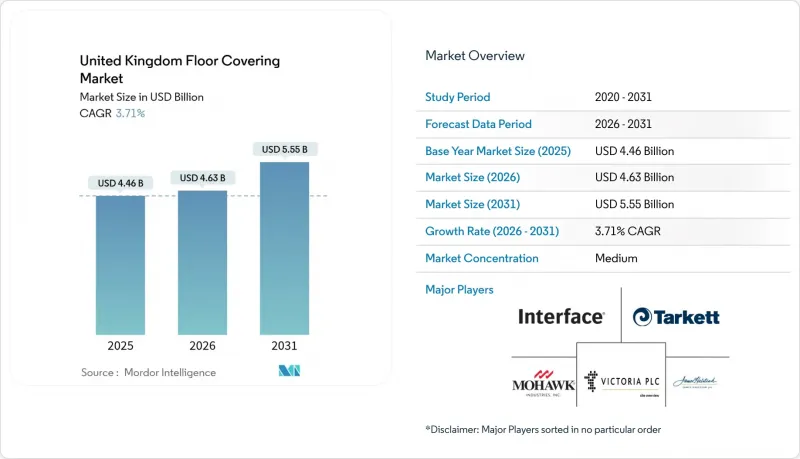

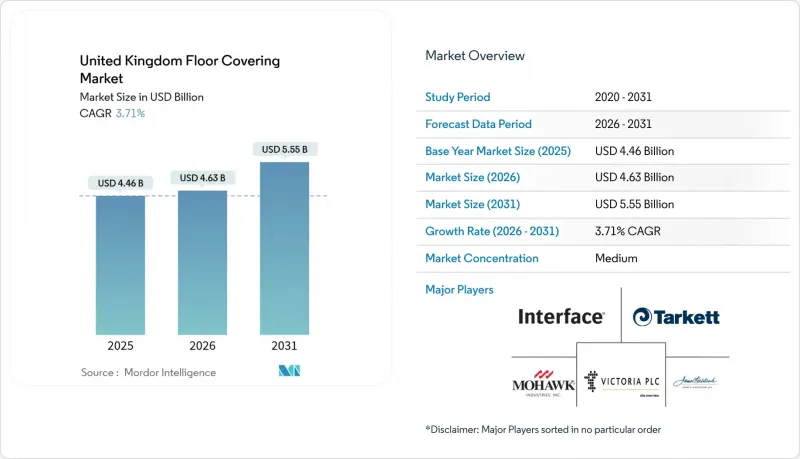

2026년 영국 마루 커버재 시장 규모는 46억 3,000만 달러로 추정되며, 2025년 44억 6,000만 달러에서 성장이 전망됩니다.

2031년에는 55억 5,000만 달러에 달할 것으로 예상되며, 2026-2031년 연평균 복합 성장률(CAGR) 3.71%로 성장할 것으로 전망됩니다.

이러한 꾸준한 상승세는 건설업의 재개와 소비자의 고급 바닥재에 대한 수요 변화로 인해 팬데믹 이후 변동기에서 안정적 성장기로 전환하는 업계의 추세를 잘 보여주고 있습니다. 주택 개보수, 상업시설 인테리어 공사, 정부 주도 개보수 프로그램 등 다양한 수요 기반이 시장의 회복력을 뒷받침하고 있습니다. 하이브리드 작업의 확산으로 모듈형 카펫 타일의 신규 수주가 증가하는 한편, 사실적인 질감과 낮은 유지보수성을 특징으로 하는 고급 비닐 타일(LVT)은 모든 부문에서 수요가 가속화되고 있습니다. 유통 경로가 온라인과 대형 소매점으로 이동하면서 제품 인지도와 가격 투명성이 높아졌고, 원자재 가격 변동과 인플레이션으로 인한 수익률 압박 속에서도 경쟁 심화가 가속화되고 있습니다.

영국 바닥재 시장 동향 및 분석

팬데믹 이후 주택 개보수 붐이 주택 수요를 견인합니다.

팬데믹 이후 주택 개보수 활동이 급증하면서 주거용 바닥재에 대한 수요의 변화가 계속되고 있습니다. 주택 소유자는 여러 기능을 수행하는 공간에서 편안함과 미적 감각을 우선시합니다. 이러한 추세는 초기 잠금에 의한 리노베이션을 넘어 시각적 매력과 기능적 성능을 모두 향상시키는 고급 바닥재 솔루션에 대한 지속적인 투자로 발전하고 있습니다. 2025년 카펫은 부활의 조짐을 보이고 있으며, 디자이너들은 침실, 거실 등 편안함을 중시하는 공간을 위해 풍부한 색상과 대담한 패턴을 선호하고 있습니다. 같은 공간에서 복합 바닥재로의 전환은 서로 다른 영역 간의 원활한 전환을 가능하게 하는 조화로운 제품 라인을 제공하는 제조업체에게 기회를 제공합니다. 이러한 행동 변화는 주거 공간의 개념과 사용 방식에 대한 근본적인 재조정을 반영하고 있으며, 다양한 바닥재 카테고리에 대한 지속적인 수요를 견인하고 있습니다.

대규모 공공 부문 리노베이션 계획으로 지속적인 수요 창출

의료, 교육, 공공 인프라의 정부 개보수 프로그램은 다년간의 프로젝트 주기를 통해 지속적인 바닥재 수요를 창출하고 시장을 안정화시킵니다. 이러한 다년간의 프로젝트 주기는 안정적인 조달 흐름을 보장하여 시장의 안정을 지원합니다. NHS 새 병원 계획과 전국적인 학교 재건 사업과 같은 이니셔티브는 공급업체에게 예측 가능한 수익 기회를 제공합니다. 의료시설 대응 및 교육시설용 바닥재 전문 업체들은 특히 수혜를 받을 수 있는 좋은 위치에 있습니다. 예를 들어, James Halstead PLC의 Polyflor 브랜드는 의료 및 교육용 탄성 바닥재 부문에서 사상 최대 매출인 1억 2,600만 파운드(1억 6,000만 달러)를 기록했습니다.

고인플레이션으로 소비자의 구매력 억제

지속적인 인플레이션 압력으로 인해 소비자들은 비필수적인 주택 개조를 연기할 수밖에 없었고, 잠재적인 수요의 강세에도 불구하고 바닥재의 임의 구매에 역풍이 불고 있습니다. 영국의 건축자재 가격 지수는 계속 변동하고 있으며, 바닥재 관련 자재에 대한 특정 영향이 전체 프로젝트의 경제성에 영향을 미치고 있습니다. 예산 중심의 소비자들은 프리미엄 기능보다 가치 제안을 우선시하는 경향이 강해지고 있으며, 이는 하이엔드 부문에 위치한 제조업체의 수익률을 압박할 수 있습니다. 이러한 움직임은 특히 주택 개조 시장에 영향을 미치고, 프로젝트 연기가 공급망 전체에 파급되어 소매업체의 재고 관리에 영향을 미칠 수 있습니다. 그러나 이러한 추세는 가격에 민감한 수요에 대응하면서도 품질 기준을 유지하는 비용 효율적인 솔루션을 제공하는 제조업체에게는 기회도 창출하고 있습니다.

부문 분석

2025년 영국 바닥재 시장에서 탄성 바닥재는 CAGR 5.93%로 확대되는 반면, 비탄성 바닥재는 42.95%의 시장 점유율을 유지할 것입니다. 특히 LVT(고급 비닐타일)는 사실적인 질감, 습한 환경에 대한 적응성, 빠른 시공성으로 주거 및 상업시설 모두에서 지지를 받으며 시장을 주도하고 있습니다. 시트 비닐과 VCT(비닐 컴포지션 타일)는 의료 및 교육 분야에서 입지를 유지하고 있으며, 코르크와 고무와 같은 틈새 소재도 특히 친환경 소재가 우선시되는 지속가능성을 중시하는 프로젝트에서 그 존재감을 드러내고 있습니다. 카펫과 러그는 대담한 패턴과 친환경적인 재생 원사를 특징으로 하는 카펫과 러그가 부활의 조짐을 보이고 있으며, 미적 감각과 지속가능성을 모두 추구하는 소비자의 변화하는 취향에 부응하고 있습니다. 도자기, 엔지니어드 우드 등 경질 바닥재는 고급스러운 매력을 유지하고 있는 반면, 중저가 라미네이트 바닥재는 시장 점유율이 하락하고 있습니다. 이는 소비자들이 내구성과 디자인 다양성이 향상된 리지드 코어 LVT를 선택하는 경향이 강해졌기 때문입니다.

수요 구조의 양극화가 진행되고 있습니다. 한편으로는 고급 개발 부동산을 위한 맞춤형 천연 소재가 제공되어 독점성과 고급스러움을 실현합니다. 한편, 고성능 합성 소재는 비용에 민감한 구매자의 요구에 부응하여 가치와 내구성을 동시에 만족시킵니다. 두 가격대에 걸쳐 있는 벤더들은 변동성 리스크를 줄이고, 프로젝트 내에서 더 넓은 지갑 점유율을 확보함으로써 경쟁 구도에서의 강인함을 확보할 수 있습니다.

2031년까지 리노베이션 및 리뉴얼 시장은 연평균 4.86%씩 성장하여 2025년 매출의 53.78%를 차지한 신축 부문과의 격차를 좁힐 것으로 예측됩니다. 이러한 성장은 주로 노후화된 주택 및 상업시설 소유주들이 공간 전체의 질적 향상을 위해 방음 및 방습 개선에 집중하고 있는 것이 주요 요인으로 작용하고 있습니다. 또한, 신속한 시공을 우선시하는 경향이 강화되고 있으며, 편의성, 효율성, 다양한 환경 적응성을 겸비한 루스레이 형식과 플로팅 시스템이 선택되고 있습니다. 한편, 임대용 분양주택(BTR)에서는 높은 입주자 회전율과 잦은 사용에도 견딜 수 있고, 장기간 기능성과 시각적 매력을 유지할 수 있는 내구성 및 청소가 용이한 마감재에 대한 수요가 증가하고 있습니다.

한편, 개발업체들은 신규 주택 프로젝트와 물류 시설에 고내구성 자재를 지정하고 있지만, 금리 상승의 영향으로 이러한 개발 속도는 억제되고 있습니다. 금리 상승은 전체 프로젝트의 타당성 및 재무 계획에 영향을 미칩니다. 개보수 공사의 경제성에 대응하기 위해 제품 엔지니어는 기존 바닥에 직접 시공을 최적화하고, 하부처리를 최소화한 SKU를 개발 중에 있습니다. 이를 통해 리노베이션 프로젝트에서 비용 효율성과 시간 효율성을 확보할 수 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액 : 달러)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.10United Kingdom floor covering market size in 2026 is estimated at USD 4.63 billion, growing from 2025 value of USD 4.46 billion with 2031 projections showing USD 5.55 billion, growing at 3.71% CAGR over 2026-2031.

This measured rise highlights a sector moving from post-pandemic volatility to steady growth as construction resumes and consumers trade up to premium surfaces. A broad demand base spanning residential renovation, commercial fit-outs, and government refurbishment programs underpins the market's resilience. Hybrid work patterns generate fresh orders for modular carpet tiles, while luxury vinyl tile (LVT) accelerates across segments due to realistic aesthetics and low upkeep requirements. Distribution shifts toward online and big-box retail channels are widening product visibility and price transparency, reinforcing competitive intensity even as raw-material cost swings and inflation challenge margins.

United Kingdom Floor Covering Market Trends and Insights

Post-pandemic home-improvement boom drives residential demand

The post-pandemic surge in home improvement activity continues to reshape residential flooring demand, with homeowners prioritizing comfort and aesthetics in spaces that now serve multiple functions. This trend extends beyond initial lockdown-driven renovations, evolving into sustained investment in premium flooring solutions that enhance both visual appeal and functional performance. Carpets are seeing a resurgence in 2025, with designers favoring rich colors and bold patterns for comfort-focused spaces such as bedrooms and living rooms. The shift toward mixed flooring materials within single spaces creates opportunities for manufacturers offering coordinated product lines that enable seamless transitions between different zones. This behavioral change reflects a fundamental recalibration of how residential spaces are conceived and utilized, driving sustained demand for diverse flooring categories.

Large-scale public-sector refurbishment pipeline creates sustained demand

Government refurbishment programs in healthcare, education, and public infrastructure create sustained flooring demand through multi-year project cycles that stabilize the market. These multi-year project cycles support market stability by ensuring steady procurement flows. Initiatives such as the NHS New Hospital Programme and national school rebuilding efforts provide predictable revenue opportunities for suppliers. Companies specializing in healthcare-compliant and education-grade flooring are particularly well-positioned to benefit. For example, James Halstead PLC's Polyflor brand reported record revenues of GBP 126 million (USD 160 million) from its healthcare and education resilient flooring segment.

High inflation constrains consumer spending power

Persistent inflation pressures force consumers to defer non-essential home improvements, creating headwinds for discretionary flooring purchases despite underlying demand strength. The United Kingdom construction material price indices show continued volatility, with specific impacts on flooring-adjacent materials affecting overall project economics. Budget-conscious consumers increasingly prioritize value propositions over premium features, potentially compressing margins for manufacturers positioned in higher-end segments. This dynamic particularly affects the residential renovation market, where project deferrals can cascade through the supply chain and impact retailer inventory management. However, the trend also creates opportunities for manufacturers offering cost-effective solutions that maintain quality standards while addressing price-sensitive demand.

Other drivers and restraints analyzed in the detailed report include:

- Growing preference for luxury vinyl tile transforms product mix

- Rising demand for modular carpet tiles reshapes commercial spaces

- Volatile raw-material prices pressure manufacturing economics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, the United Kingdom market for floor coverings is witnessing a 5.93% CAGR growth in resilient surfaces, while non-resilient options command a 42.95% market share. Leading the charge, LVT (Luxury Vinyl Tile) captivates with its lifelike visuals, adaptability to wet areas, and swift installation, making it a preferred choice for both residential and commercial applications. Sheet vinyl and VCT (Vinyl Composition Tile) maintain their foothold in healthcare and education sectors, alongside niche players like cork and rubber, especially in sustainability-driven projects where eco-conscious materials are prioritized. Carpets and rugs are making a comeback, spotlighting bold patterns and eco-friendly recycled yarns, which cater to evolving consumer preferences for both aesthetics and sustainability. While hard surfaces such as porcelain and engineered wood retain their premium appeal, mid-tier laminates are losing market share as consumers increasingly opt for rigid-core LVT, which offers enhanced durability and design versatility.

A bifurcated demand map is emerging. On one side, bespoke natural materials cater to luxury developments, offering exclusivity and high-end appeal; on the other, high-performance synthetics address value and durability, meeting the needs of cost-conscious buyers. Vendors positioned across both price ladders mitigate volatility and capture a broader wallet share within projects, ensuring resilience in a competitive market landscape.

By 2031, the replacement and retrofit market is projected to grow at a rate of 4.86%, narrowing the gap with the new-build segment, which commanded 53.78% of the revenue in 2025. This growth is primarily driven by the increasing focus of owners of aging residential and commercial properties on enhancing acoustic comfort and moisture control to improve the overall quality of their spaces. They are also prioritizing quicker installations, gravitating towards loose-lay formats and floating systems that offer convenience, efficiency, and adaptability to various environments. Meanwhile, build-to-rent schemes are driving a demand for durable, easy-to-clean finishes, which are essential for properties experiencing high tenant turnover and frequent use, ensuring these properties remain functional and visually appealing over time.

While developers are specifying high-capacity materials for new residential projects and logistics parks, the pace of these developments is tempered by rising interest rates, which impact overall project feasibility and financial planning. In response to renovation economics, product engineers are now crafting SKUs that are optimized for direct installation over existing floors and require less subfloor preparation, ensuring cost-effectiveness and time efficiency in retrofit projects.

The United Kingdom Floor Covering Market Report is Segmented by Product Type (Carpet and Rugs, Resilient Floor Covering, Non-Resilient Floor Covering), Construction Type (New Construction, Renovation & Replacement), End User (Residential, Commercial, Industrial & Public Infrastructure), Distribution Channel (B2C/Retail Channels, B2B/Contractors/Dealers), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Victoria PLC

- Interface Inc.

- Tarkett SA

- James Halstead PLC (Polyflor)

- Mohawk Industries

- Shaw Industries Group

- Forbo Flooring Systems

- Gerflor Group

- Milliken & Company

- Amtico International

- Karndean Designflooring

- Cormar Carpets

- Brintons Carpets

- Balta Group

- BerryAlloc (Beaulieu)

- Moduleo (IVC Group)

- Armstrong Flooring

- BSW Timber Group

- Junckers Flooring

- Johnson Tiles

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Post-Pandemic Home-Improvement Boom

- 4.2.2 Large-Scale Public-Sector Refurbishment Pipeline

- 4.2.3 Growing Preference for Luxury Vinyl Tile (Lvt)

- 4.2.4 Rising Demand for Modular Carpet Tiles In Offices

- 4.2.5 Government Incentives For Recycled Content Flooring

- 4.2.6 Expansion of Build-To-Rent Housing Projects

- 4.3 Market Restraints

- 4.3.1 High Inflation Dampening Discretionary Spend

- 4.3.2 Volatile Crude-Derived Raw-Material Prices

- 4.3.3 Skills Shortage In Specialist Installation Labour

- 4.3.4 Extended Commercial Leasing Cycles Delaying Fit-Outs

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Carpet and Rugs

- 5.1.2 Resilient Floor Covering

- 5.1.2.1 Vinyl Sheets & VCT

- 5.1.2.2 Luxury Vinyl Tiles (LVT)

- 5.1.2.3 Linoleum

- 5.1.2.4 Rubber Flooring

- 5.1.2.5 Cork Flooring

- 5.1.3 Non-Resilient Floor Covering

- 5.1.3.1 Ceramic & Porcelain Tile

- 5.1.3.2 Natural Stone

- 5.1.3.3 Hardwood

- 5.1.3.4 Engineered Wood

- 5.1.3.5 Laminate

- 5.2 By Construction Type

- 5.2.1 New Construction

- 5.2.2 Renovation & Replacement

- 5.3 By End User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial & Public Infrastructure

- 5.4 By Distribution Channel

- 5.4.1 B2C/Retail Channels

- 5.4.1.1 Home Centers

- 5.4.1.2 Specialty Stores

- 5.4.1.3 Online

- 5.4.1.4 Other Distribution Channels

- 5.4.2 B2B/Contractors/Dealers

- 5.4.1 B2C/Retail Channels

- 5.5 By Geography

- 5.5.1 England

- 5.5.2 Scotland

- 5.5.3 Wales

- 5.5.4 Northern Ireland

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Victoria PLC

- 6.4.2 Interface Inc.

- 6.4.3 Tarkett SA

- 6.4.4 James Halstead PLC (Polyflor)

- 6.4.5 Mohawk Industries

- 6.4.6 Shaw Industries Group

- 6.4.7 Forbo Flooring Systems

- 6.4.8 Gerflor Group

- 6.4.9 Milliken & Company

- 6.4.10 Amtico International

- 6.4.11 Karndean Designflooring

- 6.4.12 Cormar Carpets

- 6.4.13 Brintons Carpets

- 6.4.14 Balta Group

- 6.4.15 BerryAlloc (Beaulieu)

- 6.4.16 Moduleo (IVC Group)

- 6.4.17 Armstrong Flooring

- 6.4.18 BSW Timber Group

- 6.4.19 Junckers Flooring

- 6.4.20 Johnson Tiles

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

- 7.2 Rising Preference for Underfloor Heating-Compatible Floors

- 7.3 Increased Adoption of Waterproof And Spill-Resistant Flooring