|

시장보고서

상품코드

1937273

렌터카 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Car Rental - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

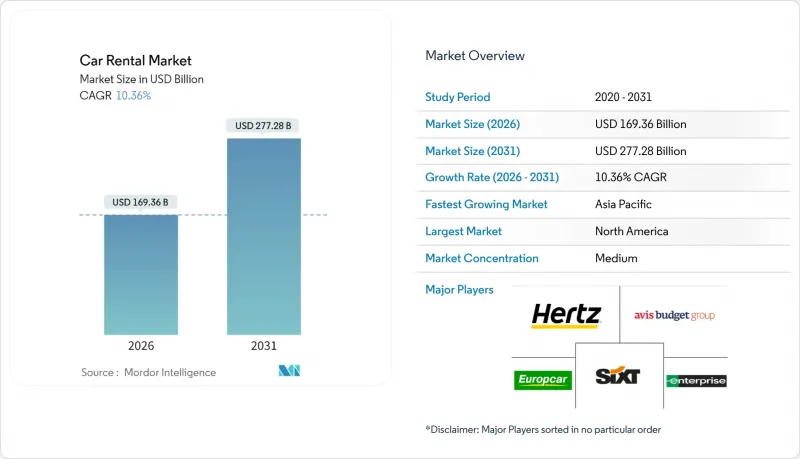

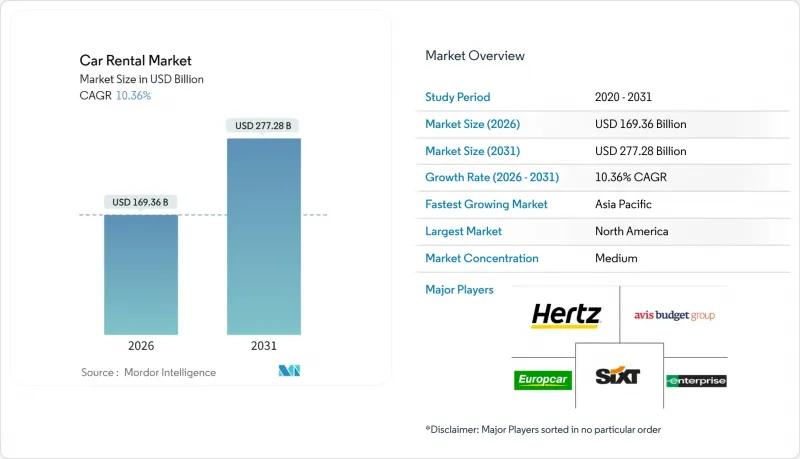

렌터카 시장은 2025년 1,534억 7,000만 달러로 평가되며, 2026년 1,693억 6,000만 달러에서 2031년까지 2,772억 8,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2026-2031년) 동안 CAGR은 10.36%로 예상됩니다.

이러한 성장 추세는 팬데믹으로 인한 침체기에서 확실한 회복세를 보여주고 있습니다. 신흥 국가의 가처분 소득 증가, 공항 인프라의 지속적인 확충, 디지털 예약 채널에 대한 접근성 확대가 지속적인 수요를 견인하고 있습니다. 각 사업자들은 다이내믹 프라이싱 엔진과 항공편 도착 정보, 고속도로 혼잡도, 지역 이벤트 등의 데이터를 연동하여 매출 확대를 꾀하고 있습니다. 한때 마이너로 여겨졌던 개인 간 플랫폼은 안전 보장 및 로열티 혜택을 강화하여 새로운 호스트를 생태계로 끌어들이고 있습니다. 차량 전동화는 여전히 불균등하지만, 일부 기존 기업의 손상 처리에도 불구하고 기업의 지속가능성에 대한 노력으로 저배출 모델이 꾸준히 조달되고 있습니다.

세계 렌터카 시장 동향 및 인사이트

팬데믹 이후 레저 여행의 빠른 회복

레저 승객 수는 코로나 이전 정점을 넘어섰고, 미국 교통보안청의 검사 건수는 전년 대비 10분의 1 미만으로 증가했으며, 유럽 공항에서도 비슷한 급증세를 보였습니다. 좌석 이용률 증가는 특히 하이브리드 근무로 인해 장기 체류가 가능한 주말에 렌터카 카운터 처리량의 직접적인 증가로 이어지고 있습니다. 여행자들은 더 일찍 예약하고 렌터카 이용 기간을 연장하는 경향이 있으며, 이는 일별 이용률 목표를 설정한 사업자의 거래당 매출 증가로 이어집니다. 비즈니스와 레저가 결합된 '브리즈아' 여행의 경우, 경영진이 사적인 날을 추가하므로 평균 임대 기간이 연장됩니다. 기업 회의가 정상화되면 평일 수요 밀도가 높아져 차량 계획 담당자가 주중에 자산을 보다 균등하게 배치할 수 있습니다. 아메리칸 익스프레스 월드와이드 비즈니스 트래블은 항공기의 용량 증가에도 불구하고 2025년까지 미국의 일일 요금이 소폭 상승할 것으로 예상하고 있습니다.

온라인 및 모바일 예약 플랫폼 보급 확대

디지털 채널이 고객 확보를 재정의하는 가운데, Avis Budget Group의 클라우드 네이티브 가격 시스템은 충성도 높은 회원을 위해 신속하게 맞춤화된 오퍼를 제공합니다. 모바일 앱은 체크인을 효율화하고, 보험 업셀링을 촉진하며, 원터치로 중도 연장을 가능하게 함으로써 카운터에 머무는 시간을 줄여줍니다. 원활한 결제 흐름은 로드사이드 어시스턴스 및 통행료 패키지의 교차 판매를 촉진하고, 부가 서비스 이용률 향상으로 이어집니다. 일부 도시의 Uber 이용자는 Uber 앱에서 직접 Turo 차량을 예약할 수 있게 되어 두 플랫폼이 원활하게 연동되었습니다. 이러한 움직임으로 인해월수백만 명의 활성 사용자가 Turo의 렌탈 유입 경로로 유입되고 있으며, 그 비용은 매우 적습니다. 예측 분석은 클릭 스트림과 비행 데이터를 수집하여 도시 간 수요 곡선을 정교화합니다. 이를 통해 사업자는 수요가 급증하기 전에 재고를 재조정할 수 있습니다.

라이드셰어링과 카셰어링 대체수단 보급 확산

앱 기반 라이드 셰어링가 지상 교통비 지출을 주도하고, 우버와 리프트와 같은 플랫폼이 도시 교통을 지배하는 가운데, 전통적 렌터카는 쇠퇴하는 추세입니다. 요금의 투명성, 현금 없는 결제, 그리고 교통 체증과 주차 문제로 골머리를 앓고 있는 도시 방문객들에게 '컨시어지 같은 운전자'라는 매력이 인기를 끌고 있습니다. P2P 플랫폼은 새로운 경쟁의 축을 형성하고 있습니다. 이 모델들은 공항의 양허료를 피할 수 있으므로 표면상 가격을 낮게 책정할 수 있습니다. 기존 사업자들은 우선 탑승 레인 설치, 화이트 라벨 제휴를 통한 도심에서의 존재감 회복에 대응하고 있습니다. 그러나 도시 지역의 일일 렌터카 사업은 온디맨드 대체 수단에 의한 구조적 압력에 계속 직면하고 있습니다.

부문 분석

2025년 기준, 오프라인 플랫폼은 렌터카 시장의 54.12%를 차지했습니다. 한편, 온라인 플랫폼은 예측 기간(2026-2031년) 동안 10.42%의 견고한 CAGR을 나타낼 것으로 예측됩니다. 이러한 변화된 상황은 기존 오프라인 매장의 존재감을 약화시키면서 역설적으로 중견 브랜드들조차도 세계 진출을 확대하고 있습니다. 로열티 회원의 편의성은 분명합니다. 사전 입력된 프로파일과 안전한 모바일 키로 카운터를 완전히 우회할 수 있으며, 보다 효율적인 경험을 할 수 있습니다. 또한 항공편 지연을 알려주는 푸시 알림을 통해 고객은 픽업 시간을 쉽게 조정할 수 있으며, 전반적인 만족도를 높일 수 있습니다. 스마트폰 접근이 제한된 지역에서는 오프라인 직접 이용이 여전히 중요한 역할을 하고 있지만, 인력 배치와 시설 비용으로 인한 높은 예약 비용에 직면해 있습니다.

디지털 트래픽은 항공사 앱, 호텔 플랫폼, 제3자 온라인 여행사와의 연계를 강화하여 모빌리티 옵션의 교차 판매를 촉진하고 있습니다. 이 통합은 고객 확보 비용을 절감하고, 보험 및 GPS 옵션과 같은 번들 서비스를 통해 추가 매출을 창출할 수 있는 길을 열어줍니다. 또한 이러한 거래에서 생성된 데이터 리소스는 차량 계획 담당자에게 도시 간 수요를 예측할 수 있는 인사이트을 제공하여 적시에 차량을 이동하고 유휴 일수를 줄일 수 있도록 합니다. 그 결과, API 퍼스트 전략을 채택한 사업자는 렌터카 업계의 이용률 지표에서 경쟁사보다 월등히 높은 이용률을 보이고 있습니다.

체험형 관광 동향에 따라 2025년에는 레저 여행객이 렌터카 시장의 55.68%를 차지할 것으로 예상되며, 예측 기간(2026-2031년) 동안 10.45%의 연평균 복합 성장률(CAGR)을 유지할 것으로 예측됩니다. 여러 도시를 돌아다니는 로드트립을 계획하는 가족 단위의 여행객들은 단체 여행에서 얻을 수 없는 자유로운 차량 조작과 짐의 유연성을 중요시합니다. 팬데믹 시기에 도입된 비접촉식 픽업 옵션은 혼잡한 셔틀버스를 피하고, 짐을 수령한 후 바로 주차장으로 이동할 수 있는 편리함으로 인기를 끌고 있습니다. 레저 이용자들의 우선순위로 높은 연비 효율과 넓은 적재공간이 상위권에 위치하여 크로스오버 모델로의 조달을 촉진하고 있습니다.

출장은 2019년 출장 건수가 회복세를 보이고 있으며, 하이브리드 근무제도를 통해 직원들이 유급휴가를 추가할 수 있게 되면서 평균 임대 기간이 연장되고 있습니다. 이러한 비즈니스와 레저의 융합은 평일과 주말 수요를 지원하고 매출 곡선을 평준화시키고 있습니다. 배출량 보고 기능이 통합된 프로그램 가능한 기업 계정은 지속가능성을 중시하는 기업을 유치하고, 기업 여행이 급감할 때에도 수요 회복력을 강화하는 데 도움이 될 것입니다.

지역별 분석

북미는 2025년 기준 렌터카 시장의 35.02%를 차지할 것으로 예상되며, 이는 성숙한 여행 인프라와 높은 자동차 소유 문화를 반영합니다. Avis Budget Group은 2023년에 120억 달러의 매출을 기록할 것으로 예상했습니다. 이는 공항 이용객 수 회복과 로열티 프로그램 재가입 증가에 따른 것입니다. 동적 가격 책정 엔진은 항공편 지연 데이터를 활용하여 막바지 예약 수요를 포착했습니다. 충전 인프라가 부족한 지방의 주간 고속도로를 따라 충전 인프라가 부족한 지역에서는 전기자동차 보급이 여전히 제한적이지만, 뉴욕과 로스앤젤레스와 같은 도심에서는 기업 고객들이 저공해차종 사용을 의무화하기 시작했습니다. 승차공유 플랫폼이 우세한 도시 지역에서는 경쟁이 치열해지고 있지만, 편도 주 간 이동은 여전히 렌터카가 주류를 이루고 있습니다.

아시아태평양은 예측 기간(2026-2031년) 동안 CAGR 10.62%로 확대될 것으로 예측됩니다. 중산층의 여행 수요 증가, 도착비자 발급 제도, 항공좌석 수의 활발한 증가가 시장의 모멘텀을 지원하고 있습니다. 기업 모빌리티는 2024년 태국에 10개 지점을 개설하고, 현재 일본내 97개 거점을 운영하는 등 적극적인 네트워크 확장을 추진하고 있습니다. 인도네시아, 베트남, 인도에서 두 자릿수 관광객 증가가 보고되고 있으며, 대중교통의 수용력이 부족한 상황에서 방문객들은 셀프 드라이브 솔루션으로 향하고 있습니다. 중국 전기자동차 제조업체는 렌탈 제휴를 통해 할인된 전기 크로스오버를 제공하고 관광 부문에 진출. 이를 통해 저비용으로 해외 브랜드 인지도를 높일 수 있는 길이 열렸습니다.

유럽은 정교한 시장인 동시에 치열한 경쟁이 벌어지고 있는 시장입니다. SIXT가 스텔란티스와 체결한 25만대 규모의 다년 계약은 반도체 부족 상황에서도 공급을 확보하는 동시에 회사의 전동화 로드맵을 추진하게 됩니다. 암스테르담시가 2025년 도입 예정인 제로에미션 구역으로 인해 사업자들은 고가의 주차공간을 전기자동차 전용으로 확보하려는 움직임을 보이고 있습니다. 대륙내 국경 개방으로 국경을 넘나드는 렌터카 사업이 확대되고 있지만, 도로 요금 체계의 차이로 인해 차량 추적이 복잡해지고 있습니다. 유로pcar가 애틀랜타와 댈러스 거점을 통해 미국 시장에 재진입한 것은 대서양 횡단 사업의 의욕이 다시 불타오르고 있다는 것을 보여줍니다. 한편, 라틴아메리카와 중동은 고속도로망 정비와 사우디의 '비전 2030' 관광 유치 등 유치 이벤트의 수혜를 받고 있지만, 환율 변동과 수입 규제로 인해 탄력적인 자본 배분이 요구되고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 개요

제4장 시장 구도

- 시장 개요

- 시장 성장 촉진요인

- 팬데믹 이후 레저 여행의 빠른 회복

- 온라인 및 모바일 예약 플랫폼의 보급률 증가

- 저가 항공사 확대로 인한 복합 교통 수요 창출

- 기업의 ESG 의무화로 전기차 렌탈 도입 가속화

- 데이터 기반 동적 가격 책정 도구를 통한 활용률 향상

- 신흥 시장의 공항 인프라 개선

- 시장 성장 억제요인

- 차량 호출 및 차량 공유 대체 서비스의 인기

- 급격한 전기차 기술 주기 속에서 증가하는 잔존가치 위험

- 공항 운영 수수료로 인한 운영자 수익 마진 압박

- 도심 지역 내 내연기관 차량에 대한 규제 제한

- 밸류체인 분석

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측(금액)

- 예약 방법별

- 오프라인

- 온라인

- 용도별

- 레저

- 사업

- 차량 유형별

- 소형차・이코노미카

- 소형 및 중형 자동차

- 표준형 및 대형 차량

- SUV 및 MPV

- 고급/프리미엄 자동차

- 렌탈 기간별

- 단기

- 중기

- 장기

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 아랍에미리트

- 사우디아라비아

- 터키

- 이집트

- 남아프리카공화국

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 및 분석

- 기업 프로파일

- Avis Budget Group Inc.

- Hertz Global Holdings Inc.

- Enterprise Holdings Inc.

- Europcar Mobility Group

- Sixt SE

- Localiza Rent a Car SA

- ALD Automotive

- Beijing CAR Inc.(CAR Inc.)

- GIG Car Share

- Lyft Rental

- Uber Rentals

- Silvercar by Audi

- Getaround

- Zoomcar

- Ola Drive

- Fast Rent A Car

- Bettercar Rental

- TT Car Transit

- Renault Eurodrive

- Shenzhen Supreme Car Rental Co., Ltd.

제7장 시장 기회 및 향후 전망

KSA 26.03.06The Car Rental Market was valued at USD 153.47 billion in 2025 and estimated to grow from USD 169.36 billion in 2026 to reach USD 277.28 billion by 2031, at a CAGR of 10.36% during the forecast period (2026-2031).

This trajectory confirms the sector's decisive rebound from its pandemic trough. Rising disposable income in emerging economies, continued airport infrastructure upgrades, and wider access to digital booking channels are steering sustained demand. Operators are capturing incremental revenue by matching dynamic pricing engines with data on flight arrivals, highway congestion, and local events. Peer-to-peer platforms, once considered fringe, have doubled down on safety guarantees and loyalty perks, drawing new hosts into the ecosystem. Fleet electrification remains uneven, yet corporate sustainability mandates have ensured steady procurement of low-emission models despite headline-grabbing write-downs at some incumbents.

Global Car Rental Market Trends and Insights

Rapid Rebound Of Post-Pandemic Leisure Travel

Leisure passenger volumes have eclipsed pre-covid peaks, with U.S. Transportation Security Administration screenings up less than one-tenth year over year and mirrored surges seen at European airports. Higher seat factors translate directly into stronger rental counter throughput, particularly on weekends when hybrid work allows extended stays. Travelers are booking earlier and keeping cars longer, a pattern that lifts revenue per transaction for operators employing day-based utilization targets. Bleisure trips lengthen average rental duration as executives tack on personal days. Normalizing corporate meetings add weekday demand density, allowing fleet planners to deploy assets more evenly through the week. Price resilience remains evident, with American Express Global Business Travel forecasting U.S. daily rates to inch up slightly across 2025 despite rising fleet capacity.

Growing Penetration Of Online And Mobile Booking Platforms

As digital channels redefine customer acquisition, Avis Budget Group's cloud-native pricing system swiftly tailors offers for its loyalty members. Mobile apps streamline check-in, upsell insurance, and permit mid-trip extensions with one tap, shrinking counter dwell time. Seamless payment flows encourage cross-selling roadside assistance, toll packages, and lifting attachment rates. Uber riders in select cities can now reserve Turo vehicles directly through the Uber app, seamlessly integrating the two platforms. This move channels millions of monthly active users into Turo's rental funnel, all at a marginal cost. Predictive analytics harvests clickstream and flight data to refine city-pair demand curves, allowing operators to rebalance inventory before peak surges hit.

Popularity Of Ride-Hailing And Car-Sharing Substitutes

App-based rides are taking the lead in ground transport spending, with platforms like Uber and Lyft dominating urban travel, marking a decline for traditional rentals. Fare transparency, cashless payment, and driver-as-concierge appeal to city visitors reluctant to navigate traffic and parking. Peer-to-peer platforms layer another competitive vector: These models dodge airport concession fees, allowing lower headline prices. Traditional operators have responded with fast-pass pick-up lanes and entering white-label partnerships to regain relevance in downtown corridors. Nonetheless, urban day rentals continue to face structural pressure from on-demand alternatives.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Low-Cost Airlines Creating Multi-Modal Travel Demand

- Corporate ESG Mandates Accelerating Adoption Of EV Rental Fleets

- Rising Residual-Value Risk Amid Rapid EV Technology Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, offline platforms commanded a 54.12% share of the car rental market. Meanwhile, online platforms are projected to experience a robust growth rate of 10.42% CAGR during the forecast period (2026-2031). This evolving landscape has diminished the prominence of traditional brick-and-mortar counters, yet paradoxically broadened the global reach of even mid-tier brands. The convenience is palpable for loyalty members: pre-populated profiles and secure mobile keys allow them to bypass counters entirely, streamlining their experience. Moreover, with push notifications alerting them to flight delays, customers can effortlessly adjust pick-up times, enhancing overall satisfaction. While offline walk-ups still play a role in areas with limited smartphone access, they grapple with higher booking costs due to staffing and facility expenses.

Digital traffic is increasingly converging with airline applications, hotel platforms, and third-party online travel agencies, now cross-selling mobility options. This integration reduces customer acquisition costs and paves the way for additional revenue through bundled services like insurance and GPS add-ons. Furthermore, the data reservoirs generated from these transactions provide fleet planners with foresight into city-pair demands, enabling timely fleet transfers and reducing idle days. As a result, operators adopting API-first strategies have significantly outpaced their competitors in utilization metrics within the car rental sector.

Based on experiential tourism trends, leisure travelers generated a 55.68% share of the car rental market in 2025 and will sustain a 10.45% CAGR during the forecast period (2026-2031). Families designing multi-stop road vacations prize vehicle control and luggage flexibility unavailable on group tours. Contactless delivery options introduced during the pandemic remain popular as they let renters proceed directly from baggage claim to parking bay, avoiding crowded shuttle buses. Higher fuel efficiency and spacious cargo areas rank at the top of leisure renters' preference lists, directing procurement toward crossover models.

Business travel is regaining 2019 trip counts, as the average length of rental has increased due to hybrid work policies that allow employees to add personal days. This blend of business and leisure supports weekday and weekend utilization, smoothing the revenue curve. Programmable corporate accounts that bundle emissions reporting help operators attract sustainability-minded firms, reinforcing demand resilience even if corporate trip volumes plateau.

The Car Rental Market Report is Segmented by Booking Mode (Offline and Online), Application (Leisure and Business), End User (Self-Drive Individual and More), Vehicle Type (Mini & Economy Cars, Compact & Intermediate Cars, and More), Rental Length (Short-Term, Medium-Term, and Long-Term), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America comprises a 35.02% share in the car rental market in 2025, reflecting mature travel infrastructure and a high vehicle ownership culture. Avis Budget Group posted USD 12 billion in 2023 sales as airport passenger flows regained momentum and loyalty program re-enrollments climbed. Dynamic pricing engines exploited flight disruption data to capitalize on last-minute bookings. Electric vehicle uptake remains tempered by charging deserts along rural interstates, yet corporate clients have begun mandating low-emission classes for city centers such as New York and Los Angeles. Competitive intensity is elevated in urban corridors where ride-hailing platforms maintain a stronghold, though rentals still dominate one-way interstate journeys.

Asia-Pacific is forecast to grow with a 10.62% CAGR during the forecast period (2026-2031). Rising middle-class travel, visa-on-arrival schemes, and vigorous airline seat growth underpin market momentum. Enterprise Mobility opened ten Thai branches in 2024 and now operates ninety-seven Japanese sites, illustrating aggressive network build-out. Indonesia, Vietnam, and India report double-digit inbound tourism growth, straining public transit capacity and directing visitors toward self-drive solutions. Chinese EV makers enter the tourist segment by offering discounted electric crossovers via rental partnerships, creating a low-cost path to overseas brand exposure.

Europe remains a sophisticated yet fiercely competitive arena. SIXT's multi-year deal for 250000 Stellantis vehicles secures supply amid chip shortages and advances its electrification roadmap. Amsterdam introduces zero-emission zones in 2025, prompting operators to reserve high-value parking slots for electric fleets. Cross-border rentals flourish on the continent's open internal borders, though differing road toll regimes complicate fleet tracking. Europcar's re-entry into the United States with Atlanta and Dallas outlets signals renewed transatlantic ambitions. Elsewhere, Latin America and the Middle East benefit from improving highway networks and inbound events such as Saudi Arabia's Vision 2030 tourism push, yet currency volatility and import restrictions require agile capital allocation.

- Avis Budget Group Inc.

- Hertz Global Holdings Inc.

- Enterprise Holdings Inc.

- Europcar Mobility Group

- Sixt SE

- Localiza Rent a Car S.A.

- ALD Automotive

- Beijing CAR Inc. (CAR Inc.)

- GIG Car Share

- Lyft Rental

- Uber Rentals

- Silvercar by Audi

- Getaround

- Zoomcar

- Ola Drive

- Fast Rent A Car

- Bettercar Rental

- TT Car Transit

- Renault Eurodrive

- Shenzhen Supreme Car Rental Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Rebound Of Post-Pandemic Leisure Travel

- 4.2.2 Growing Penetration Of Online And Mobile Booking Platforms

- 4.2.3 Expansion Of Low-Cost Airlines Creating Multi-Modal Travel Demand

- 4.2.4 Corporate Esg Mandates Accelerating Adoption Of Ev Rental Fleets

- 4.2.5 Data-Driven Dynamic Pricing Tools Boosting Utilisation Rates

- 4.2.6 Airport Infrastructure Upgrades In Emerging Markets

- 4.3 Market Restraints

- 4.3.1 Popularity Of Ride-Hailing And Car-Sharing Substitutes

- 4.3.2 Rising Residual-Value Risk Amid Rapid Ev Technology Cycles

- 4.3.3 Airport Concession Fees Squeezing Operator Margins

- 4.3.4 Regulatory Caps On Ice Vehicles In Urban Cores

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Booking Mode

- 5.1.1 Offline

- 5.1.2 Online

- 5.2 By Application

- 5.2.1 Leisure

- 5.2.2 Business

- 5.3 By End User

- 5.3.1 Self-Drive Individual

- 5.3.2 Chauffeur-Drive

- 5.3.3 Corporate Fleet Subscription

- 5.3.4 Peer-to-Peer Rental

- 5.4 By Vehicle Type

- 5.4.1 Mini & Economy Cars

- 5.4.2 Compact & Intermediate Cars

- 5.4.3 Standard & Full-Size Cars

- 5.4.4 SUVs & MPVs

- 5.4.5 Luxury / Premium Cars

- 5.5 By Rental Length

- 5.5.1 Short-Term

- 5.5.2 Medium-Term

- 5.5.3 Long-Term

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Egypt

- 5.6.5.5 South Africa

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Avis Budget Group Inc.

- 6.4.2 Hertz Global Holdings Inc.

- 6.4.3 Enterprise Holdings Inc.

- 6.4.4 Europcar Mobility Group

- 6.4.5 Sixt SE

- 6.4.6 Localiza Rent a Car S.A.

- 6.4.7 ALD Automotive

- 6.4.8 Beijing CAR Inc. (CAR Inc.)

- 6.4.9 GIG Car Share

- 6.4.10 Lyft Rental

- 6.4.11 Uber Rentals

- 6.4.12 Silvercar by Audi

- 6.4.13 Getaround

- 6.4.14 Zoomcar

- 6.4.15 Ola Drive

- 6.4.16 Fast Rent A Car

- 6.4.17 Bettercar Rental

- 6.4.18 TT Car Transit

- 6.4.19 Renault Eurodrive

- 6.4.20 Shenzhen Supreme Car Rental Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-Space Analysis & Unmet Needs