|

시장보고서

상품코드

1940800

베트남의 렌터카 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Vietnam Car Rental - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

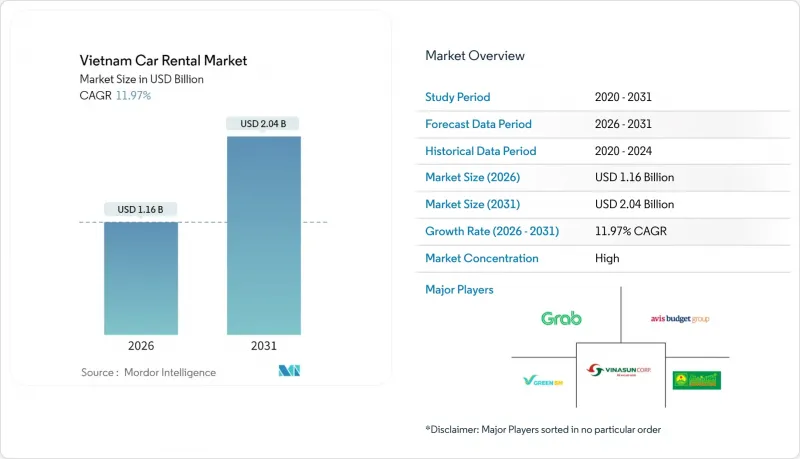

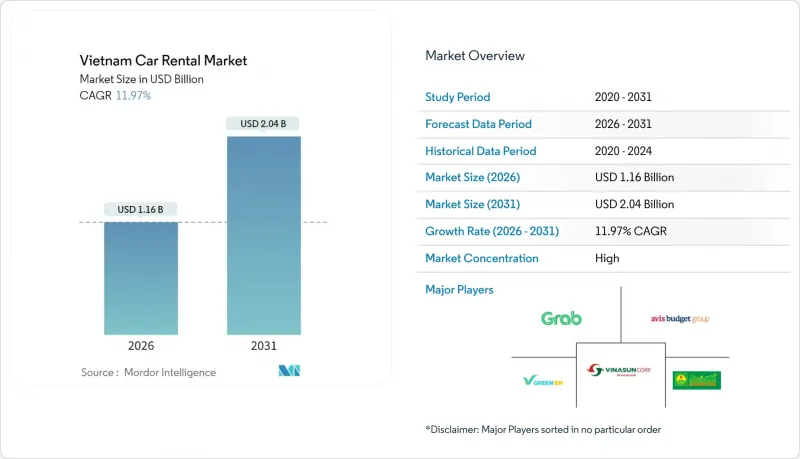

2026년 베트남의 렌터카 시장 규모는 11억 6,000만 달러로 추정되며, 2025년 10억 4,000만 달러에서 성장이 전망됩니다.

2031년까지 20억 4,000만 달러에 달할 것으로 예상되며, 2026-2031년 연평균 복합 성장률(CAGR) 11.97%로 성장할 것으로 전망됩니다.

레저 및 비즈니스 여행 증가, 급속한 도시화, 정부의 청정 이동성 정책이 이러한 확장을 뒷받침하고 있습니다. 2024년 마지막 4개월 동안 해외 입국자 수가 68.3% 급증했고, 국내 관광 지출은 팬데믹 이전 수준을 넘어섰으며, 단기 렌탈 수요를 증가시켰습니다. 베트남 인구의 13%를 차지하는 중산층의 가처분 소득 증가는 프리미엄 셀프 드라이브 옵션에 대한 수요를 불러일으키고 있습니다. 디지털화는 온라인 플랫폼을 통한 예약, 결제, 차량 운영의 효율화와 시장 인지도 확대를 통해 더욱 성장을 가속하고 있습니다. 마지막으로, 2027년까지 등록비 면제와 빠르게 확대되는 공공 충전 네트워크를 기반으로 한 전동화 추진책은 전기차 서비스와 기존 렌탈 서비스가 공존하는 독자적인 경쟁 영역을 창출하고 있습니다.

베트남의 렌터카 시장 동향 및 분석

관광 회복이 레저용 렌터카 수요를 견인

2024년 1월부터 4월까지 외국인 관광객 수는 전년 동기 대비 68.3% 증가했습니다. 이러한 레저 수요의 급증은 자가용을 이용해 하롱베이, 중부 고원, 메콩강 삼각주를 여행하는 여행객 증가로 주말 및 휴일 예약률에 직접적으로 반영되고 있습니다. 베트남 정부가 2025년부터 2026년까지 추진하는 지속 가능한 관광 캠페인은 렌터카 회사의 차량 전동화 계획과 함께 환경 친화적 인 선택에 대한 고객의 선호와 정책적 인센티브를 결합하고 있습니다. 장기 휴가 증가와 도시 가족 단위의 로드트립 문화 확산이 연중 내내 수요를 뒷받침하고 있습니다. 렌터카 업체들은 휴가철 성수기에 주요 관광 노선에 차량 공급을 늘리고, 다이내믹 프라이싱(Dynamic Pricing)을 통해 계절적 수요 급증에 대응하고 있습니다. 여행 수요가 회복되면서 단기 렌탈 차량의 가동률은 이미 팬데믹 이전 최고 수준으로 돌아와 차량당 수익성을 높이고 있습니다.

중산층의 가처분소득 증가

베트남의 중산층은 2023년 인구의 13%를 나타낼 것으로 예측되며, 2024년 초까지 전년 대비 8.5%의 소매 매출을 증가시킬 것으로 예측됩니다. 가처분 소득 증가로 SUV에서 고급 세단에 이르는 프리미엄 렌터카 카테고리에 대한 새로운 수요가 창출되고 있습니다. 고객은 차량 상태, 브랜드 명성, 컨시어지 수준의 서비스를 중시합니다. 또한, 풍요로움의 확대는 주말 여행의 이용자 층을 넓혀 셀프 드라이브 여행을 가끔씩의 사치가 아닌 주류 레크리에이션으로 바꾸고 있습니다. 서비스 차별화를 위해 렌터카 업체들은 단계별 로열티 프로그램, 스마트폰으로 차량 잠금 해제, 카시트 등 무료 추가 옵션으로 대응하고 있습니다. 고급차 수요 증가는 수입업체들에게 높은 관세에도 불구하고 고급 모델을 조기에 도입하도록 유도하여 보다 다양한 차종 구성을 만들어내고 있습니다. 결국 소득 증가가 가격 탄력성을 완화시켜 사업자는 관세나 차량 교체로 인한 비용 상승분을 수요 감소 없이 전가할 수 있게 됩니다.

주요 도시의 교통 체증과 주차장 부족 문제

호치민시 통근자들은 매년 교통 체증으로 인해 많은 시간을 낭비하고 있으며, 이는 렌터카 이용률 감소와 연료비 증가를 초래하고 있습니다. 특히 1군과 하노이 구시가지의 주차 공간 부족으로 인해 고가의 야간 보관료가 발생하고 있으며, 사업자는 이를 흡수하거나 전가할 수 밖에 없습니다. 하노이시가 2030년부터 휘발유 차량 규제를 제안하는 등 정책 동향은 차량 구성 계획에 불확실성을 가져옵니다. ITS 프로그램을 통한 향후 교통체증 완화가 기대되는 한편, 단기적인 교통체증 대책으로 렌터카 업체들은 텔레매틱스를 활용한 경로 설정과 반납 지연 시 위약금 조항을 도입해야 하는 상황에 처해 있습니다. 배차 지연이나 주차 추가 요금 발생은 고객 만족도를 떨어뜨리고, 가격에 민감한 이용자를 다른 수단으로 유도하는 요인이 됩니다.

부문 분석

2025년 기준 베트남의 렌터카 시장의 59.88%를 온라인 채널이 차지할 것으로 예상되며, 이는 베트남의 전자상거래로의 빠른 전환을 보여줍니다. 160% 이상의 모바일 보급률로 여행자는 픽업 직전 몇 분이라도 차량을 확보할 수 있게 되었고, 통합형 전자지갑이 결제를 가속화하고 있습니다. 이 부문의 예상 CAGR 13.12%는 편의성과 비용 효율성을 반영하고 있습니다. 디지털 플랫폼은 지점 비용을 절감하고 가동률을 높이기 위한 동적 가격 책정 알고리즘을 지원합니다. 40.12%를 차지하는 오프라인 카운터는 여전히 노년층이나 특주 조건이 필요한 법인 예약에 대응하고 있습니다. 그러나 방문 고객 수가 감소함에 따라 지점 기반 모델은 수익률 압박에 직면하고 있으며, 기존 기업들은 클릭앤콜렉트 서비스와의 하이브리드화에 직면하고 있습니다.

기존 여행사들은 컨시어지 서비스나 개별 여정 계획으로 고객 충성도를 유지하는 반면, 온라인 스타트업들은 플래시 할인과 사용자 리뷰로 가격 중시층을 확보하고 있습니다. 플랫폼 사업자들은 데이터 프라이버시 및 결제 보안에 대한 규제 강화에 따라 암호화 기술 및 컴플라이언스 인증에 대한 투자로 신뢰를 유지하기 위해 노력하고 있습니다. 이러한 경쟁으로 베트남의 렌터카 시장은 서비스 품질, 차량 투명성, 이용 후 피드백 루프의 개선이라는 혜택을 누리고 있습니다.

2025년 단기 렌탈은 관광 회복과 기업 여행 증가에 힘입어 베트남의 렌터카 시장 규모의 61.10%를 차지할 것으로 예측됩니다. 주말 여행객이나 비즈니스 방문객들은 소유에 따른 번거로움, 교통 체증, 주차 공간 부족을 피할 수 있는 일 단위 계약을 선호합니다. 설날, 통일기념일 등 명절에는 이용률이 최고조에 달하고, 기업들은 공항과 관광지에 차량을 미리 배치해야 합니다. 이 부문의 CAGR 전망치인 13.05%는 2026년 600만 명의 방문객이 방문할 것으로 예상되는 베트남의 성장과 활발한 국내 여행 문화에 힘입은 결과입니다.

장기 렌탈은 38.90%의 점유율을 차지하며 사업자의 수익 안정성을 뒷받침하고 있습니다. 기업 고객, 주재원, 외교사절단은 풀 서비스 유지보수가 포함된 월정액 계약을 선호하며, 예산의 예측가능성을 높이고 있습니다. IFRS16의 적용으로 인해 차량 보유 차량이 운용리스로의 전환이 가속화되고 있습니다. 제공업체는 텔레매틱스를 도입하여 주행거리 제한 모니터링 및 예방 정비를 실시하여 잔존가치를 보호하고 있습니다. 외국인 직접투자 증가와 산업단지의 확장에 따라 장기 임대 수요는 기존 중심지에서 꽝닌, 동나이 등 지방으로 확산되어 지리적 분산이 진행되고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.10Vietnam car rental market size in 2026 is estimated at USD 1.16 billion, growing from 2025 value of USD 1.04 billion with 2031 projections showing USD 2.04 billion, growing at 11.97% CAGR over 2026-2031.

Growing leisure and business travel, rapid urbanization, and the government's clean-mobility agenda underpin this expansion. International arrivals jumped 68.3% during the last four months of 2024, and domestic tourism spending now exceeds pre-pandemic levels, lifting short-term rental volumes. Rising disposable incomes among Vietnam's 13%-strong middle class have spurred demand for premium, self-drive options. Digitization further fuels growth as online platforms streamline booking, payment, and fleet utilization while widening market visibility. Finally, the push for electrification-anchored by registration-fee waivers through 2027 and a rapidly scaling public charging network-creates a distinct competitive space where electric mobility services coexist with traditional rental offerings.

Vietnam Car Rental Market Trends and Insights

Tourism Rebound Drives Leisure Rentals

International visitor arrivals rose 68.3% during the first four months of 2024. The leisure surge translates directly into higher weekend and holiday bookings as travelers opt for self-drive journeys across Ha Long Bay, the Central Highlands, and the Mekong Delta. Vietnam's 2025-2026 national campaign for sustainable tourism dovetails with rental firms' plans to electrify fleets, aligning customer preference for eco-friendly choices with policy incentives. Extended public holidays and a growing culture of road trips among urban families sustain year-round demand. Rental operators increase fleet availability in peak vacation corridors, using dynamic pricing to capture seasonal spikes. As travel rebounds, occupancy ratios of short-term fleets have already returned to pre-pandemic peaks, lifting per-vehicle profitability.

Rising Disposable Incomes Among the Middle Class

Vietnam's middle class reached 13% of the population in 2023 and continues to expand, driving a retail sales increase of 8.5% year-on-year through early 2024. Higher disposable income unlocks new demand for premium rental categories-from SUVs to luxury sedans-where clients prioritize vehicle condition, brand cachet, and concierge-level service. Rising affluence also broadens the user base for weekend getaways, turning self-drive trips into mainstream recreation rather than occasional indulgence. To differentiate offerings, rental firms respond with tiered loyalty programs, smartphone-based vehicle unlock, and complimentary add-ons like child seats. Premium demand encourages importers to expedite the arrival of luxury models despite high tariffs, creating a more diverse fleet mix. Ultimately, income gains cushion price elasticity, allowing operators to pass on cost inflation from tariffs or fleet upgrades without eroding volumes.

Urban Congestion and Limited Parking in Major Cities

Ho Chi Minh City commuters lose more hours annually to congestion, eroding rental vehicle productivity and inflating fuel costs. Parking shortages, especially in District 1 and Hanoi's Old Quarter, lead to high overnight storage fees that operators must absorb or pass on. Policy moves such as Hanoi's proposed gasoline-vehicle restrictions from 2030 inject uncertainty about fleet composition planning. While the ITS program promises future relief, near-term congestion forces rental companies to adopt telematics-enabled routing and penalty clauses for late returns. Customer satisfaction suffers when pickups are delayed or parking surcharges appear, nudging price-sensitive users toward alternatives.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward App-Based and Online Bookings

- Government Smart-Mobility Sandbox Projects

- Sparse EV-Charging Network Outside Tier-1 Cities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Online channels underpinned 59.88% of the Vietnam car rental market share in 2025, spotlighting the country's rapid pivot to e-commerce. Mobile penetration above 160% enables travelers to secure vehicles minutes before pickup, while integrated e-wallets accelerate checkout. The segment's anticipated 13.12% CAGR reflects convenience and cost efficiency, as digital platforms slash branch overheads and support dynamic pricing algorithms that lift utilization. Offline counters, holding 40.12%, still serve older demographics and corporate bookings requiring bespoke terms. Yet branch-based models face margin compression as foot traffic declines, prompting legacy firms to hybridize with click-and-collect services.

Traditional agencies leverage concierge experiences and personalized itinerary planning to retain loyalty, whereas online newcomers court price-sensitive segments with flash discounts and user-generated reviews. Platform operators invest in encryption and compliance certifications to preserve trust as regulatory frameworks around data privacy and payment security harden. The Vietnam car rental market benefits from this competition as service quality, fleet transparency, and post-trip feedback loops improve.

Short-term rentals controlled 61.10% of the Vietnam car rental market size in 2025, buoyed by tourism rebound and growing corporate travel. Weekend trippers and business visitors embrace day-based contracts that avoid the hassles of ownership, congestion charges, and parking scarcity. Utilization peaks during public holidays such as Tet and Reunification Day, compelling firms to pre-position vehicles at airports and tourist hotspots. The segment's 13.05% CAGR outlook remains tied to Vietnam's projected 6-million-visitor milestone in 2026 and robust domestic vacation culture.

Long-term rentals, with 38.90% share, anchor revenue stability for operators. Corporate clients, expats, and diplomatic missions favor monthly contracts bundled with full-service maintenance, enabling predictable budgeting. IFRS 16 accelerates the shift, pushing fleets toward operational leases. Providers deploy telematics to monitor mileage caps and preventative servicing, safeguarding residual value. As foreign direct investment climbs and manufacturing parks proliferate, long-term rental demand spreads from traditional centers into provinces such as Quang Ninh and Dong Nai, diversifying geographic exposure.

The Report Covers the Car Rental Industry in Vietnam. The Market is Segmented by Booking Type (Online and Offline), Rental Duration (Short-Term and Long-Term), Application Type (Tourism and Leisure, Daily Commuting and Corporate and Expat Mobility), Vehicle Propulsion (Internal Combustion Engine, and More), and by End-User (Individual and Corporate). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Vietnam Sun Corporation (Vinasun)

- Mai Linh Group

- Green & Smart Mobility JSC (GSM)

- Grab Holdings Inc.

- Gojek Vietnam

- Avis Budget Group

- Enterprise Holdings

- Hertz Corporation

- Sixt SE

- Saigon Car Rental Co. Ltd.

- Thuexe.vn

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tourism Rebound Drives Leisure Rentals

- 4.2.2 Rising Disposable Incomes Among Middle Class

- 4.2.3 Shift Toward App-Based and Online Bookings

- 4.2.4 Electrification Push Via Green-and-Smart Mobility (GSM)

- 4.2.5 Corporate Fleet Outsourcing Post-IFRS 16

- 4.2.6 Government Smart-Mobility Sandbox Projects

- 4.3 Market Restraints

- 4.3.1 Dominance of Low-Cost Ride-Hailing and Motorbikes

- 4.3.2 High Vehicle Import Tariffs and Registration Fees

- 4.3.3 Urban Congestion and Limited Parking in Major Cities

- 4.3.4 Sparse EV-Charging Network Outside Tier-1 Cities

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Booking Type

- 5.1.1 Online

- 5.1.2 Offline

- 5.2 By Rental Duration

- 5.2.1 Short-term (Less than 30 days)

- 5.2.2 Long-term (Above 30 days)

- 5.3 By Application Type

- 5.3.1 Tourism and Leisure

- 5.3.2 Daily Commuting

- 5.3.3 Corporate and Expat Mobility

- 5.4 By Vehicle Propulsion

- 5.4.1 Internal-Combustion Engine (ICE)

- 5.4.2 Battery-Electric Vehicle (BEV)

- 5.4.3 Hybrid Electric Vehicle (HEV/PHEV)

- 5.5 By End-user

- 5.5.1 Individual

- 5.5.2 Corporate

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Vietnam Sun Corporation (Vinasun)

- 6.4.2 Mai Linh Group

- 6.4.3 Green & Smart Mobility JSC (GSM)

- 6.4.4 Grab Holdings Inc.

- 6.4.5 Gojek Vietnam

- 6.4.6 Avis Budget Group

- 6.4.7 Enterprise Holdings

- 6.4.8 Hertz Corporation

- 6.4.9 Sixt SE

- 6.4.10 Saigon Car Rental Co. Ltd.

- 6.4.11 Thuexe.vn