|

시장보고서

상품코드

2035116

CPaaS(Communication Platform-as-a-Service) 시장 : 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Communication Platform-as-a-Service (CPaaS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

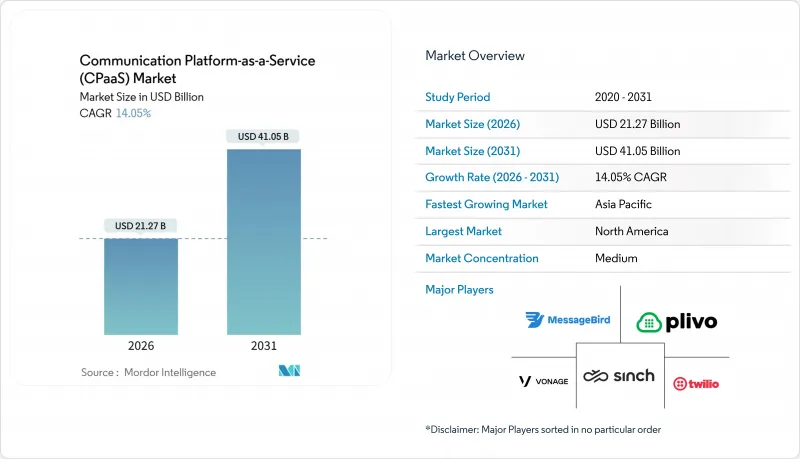

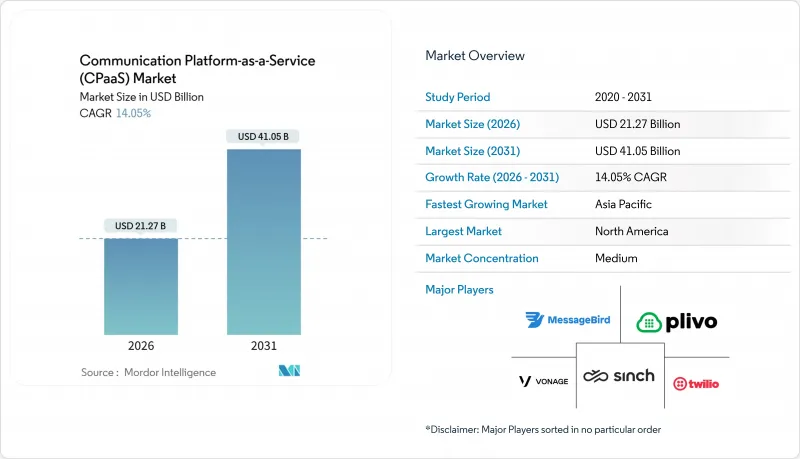

CPaaS(Communication Platform-as-a-Service) 시장 규모는 2026년에 212억 7,000만 달러로 예상되며, 2031년까지 410억 5,000만 달러에 이를 것으로 예측되며, CAGR은 14.05%로 추이할 전망입니다.

임베디드 음성, 메시징 및 비디오에 대한 수요가 증가함에 따라 고객 경험 아키텍처가 변화하고 있으며, 기업들은 모놀리식 컨택센터 스위트에서 디지털 워크플로우에 직접 통합할 수 있는 API 우선의 구성 가능한 레이어로 전환하고 있습니다. 이러한 변화를 촉진하는 세 가지 요인이 있습니다. 유럽의 PSD2와 같은 엄격한 인증 규정(예: 프로그래밍 가능한 일회용 패스워드(OTP) 흐름을 의무화하는 유럽 PSD2), 기업이 단일 벤더 관계로 통합해야 하는 상황, 소비자의 OTT 채팅 채널로의 전환, 통신사업자가 미션 크리티컬 워크로드를 위한 저지연 통신 경로를 확보할 수 있는 5G 네트워크 슬라이싱의 등장 미션 크리티컬 워크로드를 위한 저지연 통신 경로를 확보할 수 있는 5G 네트워크 슬라이싱의 등장입니다. 경쟁은 치열해지고 있지만, 시장 점유율이 15%를 넘지 않는 벤더가 없기 때문에 CPaaS(Communication Platform-as-a-Service) 시장에는 산업별 과제와 지역별 데이터 주권 요구사항에 대응하는 전문 기업에게 여전히 미개척의 비즈니스 기회가 남아 있습니다.

세계 CPaaS(Communication Platform-as-a-Service) 시장 동향과 인사이트

OTT 채팅을 중심으로 한 인게이지먼트

WhatsApp Business API만 해도 현재 월 1,000억 건 이상의 메시지를 처리하고 있으며, 그 규모 때문에 Meta는 2025년 7월에 대화 기반 과금 체계를 도입할 수밖에 없었습니다. 각 채널마다 고유한 승인 워크플로우와 컨텐츠 규칙이 존재하기 때문에 기업들은 WhatsApp, Telegram, LINE, WeChat, Viber와 턴키 통합을 유지하는 플랫폼으로 몰려들고 있습니다. 소매업체와 전자상거래 사업자들은 이러한 연동 기능을 활용하여 주문 확인, 배송 상태 업데이트, 반품 절차를 모두 채팅 스레드 내에서 자동화하여 웹 포털에 대한 의존도를 낮추고 있습니다. 여러 OTT 플랫폼에 대한 대응을 유지하지 못하는 CPaaS 벤더는 상품화된 SMS 전송으로 후퇴할 위험이 있습니다. 그럼에도 불구하고, 인도와 브라질의 데이터 현지화 규제로 인해, 제공업체는 지역별로 호스팅 노드를 유지해야 하며, 이는 복잡성과 비용을 증가시키고 있습니다.

로우코드/노코드 CPaaS 구축

Twilio Studio와 같은 비주얼 플로우 빌더를 사용하면 기술 지식이 없는 직원도 몇 분 안에 예약 알림 전화나 장바구니 이탈 캠페인을 설계할 수 있으며, 전담 개발자가 필요하지 않습니다. 신속한 프로토타이핑을 통해 중소기업의 판매 주기를 단축하고, 대기업은 엔지니어링 예산을 할당하기 전에 참여 아이디어를 시험적으로 도입할 수 있습니다. 예를 들어, 의료 사무 직원은 IT 부서의 개입 없이도 진료 후 SMS 후속 조치를 설정할 수 있습니다. 오케스트레이션 툴의 민주화는 진입장벽을 낮춰 CPaaS(Communication Platform-as-a-Service) 시장을 확대하고 있으며, 특히 중소기업이 심각한 개발자 부족에 직면한 아시아태평양의 신흥국에서 두드러지게 나타나고 있습니다. 미국의 TCPA(전화통신비밀보호법) 등 스팸 동의 규정을 준수하기 위해서는 여전히 안전장치가 필요하기 때문에 주요 벤더들은 빌더 내에 옵트인 관리 기능을 내장하고 있습니다.

국가별 A2P SMS 추가 요금

인도, 미국, 유럽 등 많은 지역의 통신사들은 기업용 SMS에 대해 건당 0.005-0.02달러의 요금을 부과하고 있으며, 대량 트래픽의 경우 수익률을 최대 25%까지 떨어뜨리고 있습니다. 인도의 블록체인 기반 DLT 플랫폼이나 미국의 10DLC 프레임워크와 같은 등록 시스템에서는 모든 템플릿에 대한 사전 승인이 의무화되어 있어, 시간적 제약이 있는 경보의 도입 주기가 길어지고 있습니다. 각 벤더들은 고객에게 추가 요금이 적용되지 않는 RCS 및 OTT 채널로의 전환을 유도하고 있지만, 선진국을 제외한 시장에서의 단말기 지원 단편화가 전환의 걸림돌로 작용하고 있습니다.

부문 분석

2025년 CPaaS(Communication Platform-as-a-Service) 시장에서 순수 전문 기업이 매출의 42.44%를 차지했습니다. 이러한 성장은 빠른 릴리스 주기, 통합 API, 캐리어 독립적인 라우팅으로 인한 세계 확장의 가속화에 기인합니다. 그러나 통신사 주도의 서비스는 2031년까지 연평균 복합 성장률(CAGR) 14.67%로 가장 빠른 성장세를 보이고 있으며, 기업용 모빌리티 계약 번들링과 시그널링 경로에서 중계가 필요 없는 직접 네트워크 액세스로 인해 이 부문에서 가장 빠른 성장세를 보이고 있습니다.

실제로 다국적 은행들은 옴니채널 혁신은 전문 벤더를, 국내 지연이 허용되지 않는 인증은 통신사 자회사를 이용하는 등 이중 소싱을 채택하는 경우가 많습니다. 하이퍼스케일 클라우드는 현재 네이티브 메시징과 음성 기능을 통합하여 전환 비용을 더욱 낮추고 있습니다. 그 결과, CPaaS(Communication Platform-as-a-Service) 시장은 하이브리드 형태로 전환되고 있으며, 기업들은 독립 벤더의 풍부한 API를 활용한 혁신과 모바일 네트워크 사업자가 제공하는 규제 대상 워크로드 를 결합하고 있습니다.

SMS 및 기존 A2P 트래픽은 2025년 기준 39.21%의 점유율을 유지했습니다. 이는 데이터 통신이 불안정한 상황에서도 모든 단말기가 문자메시지를 수신할 수 있기 때문입니다. 그러나 애플의 iOS 18이 2024년 네이티브 RCS 지원을 추가함에 따라 도입의 큰 장벽이 제거되어 2031년까지 RCS 시장은 CAGR 14.98%로 확대될 것으로 예측됩니다.

소매업체들은 현재 RCS 메시지 내에 상품 캐러셀과 빠른 답장 버튼이 내장되어 있으며, 일반 텍스트 SMS에 비해 탭 통과율이 3배나 높습니다. 일찍 도입한 기업들은 고객에게 독립형 앱 설치를 강요하지 않고도 더 높은 참여 지표를 확보할 수 있습니다. 그럼에도 불구하고, 보안을 중시하는 조직은 구두 동의가 필수적인 상황에서 음성 및 대화형 음성 응답(IVR) 흐름을 유지하고 있으며, 이는 단일 매체가 아닌 채널 포트폴리오가 CPaaS(Communication Platform-as-a-Service) 시장의 근간을 이루고 있다는 것을 보여줍니다.

'CPaaS(Communication Platform-as-a-Service) 보고서'는 CPaaS의 유형(퓨어플레이, 엔터프라이즈급 등), 통신 채널(SMS 및 A2P 메시징 등), API 서비스(메시징 등), 도입 모델(퍼블릭 클라우드, 프라이빗 클라우드, 하이브리드 클라우드), 기업 규모(중소기업 및 대기업), 최종 사용자 산업(IT 및 통신, 기타), 그리고 지역별로 분류되어 있습니다. 시장 예측은 금액(USD) 기준으로 제공됩니다.

지역별 분석

북미는 높은 클라우드 보급률, 스타트업 생태계, 하이퍼스케일러와의 근접성 등으로 인해 2025년 매출의 36.01%를 차지했습니다. 이 지역의 구매자들은 AI 기반 분석과 옴니채널 오케스트레이션을 우선순위에 두고 있으며, 이는 프리미엄 ARPU로 이어져 벤더의 수익성을 뒷받침하고 있습니다.

아시아태평양은 성장의 원동력이며, 인도, 중국, 동남아시아의 스마트폰 우선 경제권이 데스크톱 웹에서 모바일 참여로 빠르게 전환함에 따라 2031년까지 연평균 복합 성장률(CAGR) 15.90%로 급성장할 것으로 예측됩니다. 인도의 UPI(Unified Payments Interface)는 2025년 말까지 월 114억 건의 거래를 처리하고, 각 거래가 실시간 알림을 트리거하여 국내 CPaaS 플랫폼의 기준 트래픽을 증가시킵니다.

유럽은 PSD2 인증에 힘입어 견조한 수주 기반을 유지하고 있지만, 초기 컴플라이언스 대응 물결이 지나면 성장이 둔화될 것입니다. 남미, 중동 및 아프리카는 절대적인 수익에서 뒤쳐져 있지만, 사우디아라비아와 아랍에미리트에서는 공공 부문의 디지털화로 인해 성장이 가속화되고 있습니다. 아프리카에서는 통신망 커버리지가 낮기 때문에 당분간 SMS가 주류를 이루고 있으며, CPaaS(Communication Platform-as-a-Service) 시장 내에서 기존 채널의 수익 하한선을 지탱하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The Communication Platform-as-a-Service market size is USD 21.27 billion in 2026, and it is projected to reach USD 41.05 billion by 2031, advancing at a 14.05% CAGR.

Heightened demand for embedded voice, messaging, and video is reshaping customer-experience architectures, encouraging firms to swap monolithic contact-center suites for API-first, composable layers that plug directly into digital workflows. Three catalysts drive this shift: stronger authentication rules such as PSD2 in Europe, which require programmable one-time-password flows; the migration of consumers to over-the-top chat channels that enterprises must now unify under a single vendor relationship; and the arrival of 5G network slicing that lets operators carve low-latency lanes for mission-critical workloads. Competitive intensity is rising, yet no vendor controls more than 15%, so the Communication Platform-as-a-Service market still offers white-space opportunities for specialists addressing vertical gaps or regional data-sovereignty requirements.

Global Communication Platform-as-a-Service (CPaaS) Market Trends and Insights

OTT Chat-Centric Engagement

WhatsApp Business API alone now handles more than 100 billion messages per month, a scale that forced Meta to adopt conversation-based pricing in July 2025. Enterprises flock to platforms that maintain turnkey integrations with WhatsApp, Telegram, LINE, WeChat, and Viber because each channel carries unique approval workflows and content rules. Retailers and e-commerce players use these integrations to automate order confirmations, shipping updates, and returns entirely within chat threads, trimming web-portal dependencies. CPaaS vendors incapable of sustaining multi-OTT support risk falling back to commoditized SMS delivery. Even so, data-localization rules in India and Brazil compel providers to keep regional hosting nodes, adding complexity and cost.

Low-Code / No-Code CPaaS Build-Outs

Visual flow builders such as Twilio Studio let non-technical staff design appointment-reminder calls or abandoned-cart campaigns in minutes, removing the need for dedicated developers. Rapid prototyping shortens sales cycles for SMEs and lets large enterprises pilot engagement ideas before allocating engineering budgets. Healthcare clerical workers, for instance, can set up post-consultation SMS follow-ups without IT involvement. The democratization of orchestration tools is broadening the Communication Platform-as-a-Service market by lowering entry barriers, particularly in emerging Asia Pacific where small businesses face acute developer shortages. Compliance with spam-consent rules such as the TCPA in the United States still requires guardrails, so leading vendors embed opt-in management inside their builders.

Country-Level A2P SMS Surcharges

Operators in India, the United States, and much of Europe have imposed fees of USD 0.005-0.02 per message on enterprise SMS, eroding margins by up to 25 percentage points for high-volume traffic. Registration systems such as India's blockchain-based DLT platform and the U.S. 10DLC framework require every template to be pre-approved, lengthening onboarding cycles for time-sensitive alerts. Vendors are nudging customers toward RCS or OTT channels where surcharges do not apply, but fragmented handset support outside developed markets slows migration.

Other drivers and restraints analyzed in the detailed report include:

- AI-Powered CPaaS Automation and Analytics

- Telco 5G-Anchored CPaaS Innovation

- Enterprise Data-Residency Mandates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pure-play specialists captured a 42.44% revenue slice of the Communication Platform-as-a-Service market in 2025. Their growth stems from rapid release cadences, unified APIs, and carrier-agnostic routing that speed global expansion. However, telco-driven offerings exhibit the segment's quickest advance at a 14.67% CAGR to 2031, riding bundled enterprise mobility contracts and direct network access that eliminates a hop in the signaling path.

In practice, multinational banks often dual-source, using a pure-play vendor for omnichannel innovation and a carrier subsidiary for latency-critical authentication inside domestic borders. Hyperscale clouds are now embedding native messaging and voice, narrowing switching costs further. Consequently, the Communication Platform-as-a-Service market is tilting toward hybrid consumption, where enterprises mix API-rich innovation from independents with regulated-workload delivery from mobile-network operators.

SMS and traditional A2P traffic retained 39.21% share in 2025, in part because every handset can receive a text even when data connectivity is unreliable. Yet Apple's iOS 18 added native RCS support in 2024, clearing a major adoption hurdle and driving a 14.98% CAGR for RCS through 2031.

Retailers now embed product carousels and quick-reply buttons inside RCS messages, achieving tap-through rates triple that of plain-text SMS. Enterprises that move early gain richer engagement metrics without forcing customers to install standalone apps. Still, security-sensitive organizations retain voice and interactive-voice-response flows where verbal consent remains mandatory, confirming that a channel portfolio rather than a single medium underpins the Communication Platform-as-a-Service market.

The Communication Platform-As-A-Service Report is Segmented by CPaaS Type (Pure-Play, Enterprise-Grade, and More), Communication Channel (SMS and A2P Messaging, and More), API Service (Messaging, and More), Deployment Model (Public Cloud, Private Cloud, and Hybrid Cloud), Enterprise Size (SMEs, and Large Enterprises), End-User Vertical (IT and Telecom, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 36.01% of 2025 revenue due to deep cloud penetration, a dense start-up ecosystem, and proximity to hyperscalers. Regional buyers prioritize AI-driven analytics and omnichannel orchestration, translating into premium ARPU that props up vendor profitability.

Asia Pacific is the growth engine, forecast to surge at a 15.90% CAGR to 2031 as smartphone-first economies in India, China, and Southeast Asia leapfrog desktop web to mobile engagement. India's Unified Payments Interface processed 11.4 billion monthly transactions by late 2025, each triggering real-time alerts that inflate baseline traffic on domestic CPaaS platforms.

Europe retains a solid base order flow anchored in PSD2 authentication, but growth moderates after the initial compliance wave. South America, the Middle East and Africa trail in absolute revenue, though Saudi Arabia and the United Arab Emirates are accelerating due to public-sector digitization. In Africa, coverage gaps mean SMS dominates for now, sustaining a revenue floor for legacy channels inside the Communication Platform-as-a-Service market.

- Twilio Inc.

- Vonage Holdings Corp.

- Sinch AB

- Infobip Ltd.

- MessageBird B.V.

- Bandwidth Inc.

- Plivo Inc.

- 8x8 Inc.

- Voximplant (Zingaya Inc.)

- Voxvalley Technologies

- IntelePeer Cloud Communications

- Wazo Communication Inc.

- Avaya Inc.

- AT&T Inc.

- Mitel Networks Corporation

- Telestax

- CM.com N.V.

- Kaleyra Inc.

- Route Mobile Ltd.

- Telnyx LLC

- RingCentral Inc.

- Cisco Systems Inc.

- Link Mobility Group ASA

- TeleSign Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 OTT Chat-Centric Engagement

- 4.2.2 Low-Code / No-Code CPaaS Build-Outs

- 4.2.3 PSD2-Driven Programmable Messaging

- 4.2.4 Telco 5G-Anchored CPaaS Innovation

- 4.2.5 AI-Powered CPaaS Automation and Analytics

- 4.2.6 IoT and Edge-Integrated CPaaS Workloads

- 4.3 Market Restraints

- 4.3.1 Country-Level A2P SMS Surcharges

- 4.3.2 Enterprise Data-Residency Mandates

- 4.3.3 Stricter Anti-Spam and Consent Regulations

- 4.3.4 Growing Messaging/API Security and Fraud Risk

- 4.4 Industry Value-Chain Analysis

- 4.5 Industry Ecosystem Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.7.1 Serverless Deployments

- 4.7.2 Machine-Learning and AI-Enabled Contextual Routing

- 4.7.3 Omnichannel Conversational Bots

- 4.7.4 Advanced Security and Privacy Paradigms (Zero-Trust, STIR/SHAKEN)

- 4.8 Impact of Macroeconomic Factors on the Market

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Bargaining Power of Suppliers

- 4.9.4 Threat of Substitutes

- 4.9.5 Competitive Rivalry

- 4.10 Pricing and Business-Model Analysis

- 4.11 Comparative Analysis of CPaaS vs UCaaS vs Traditional Deployments

- 4.12 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By CPaaS Type

- 5.1.1 Pure-Play CPaaS

- 5.1.2 Enterprise-Grade CPaaS

- 5.1.3 Telco-Driven CPaaS

- 5.1.4 Service-Provider-Based CPaaS

- 5.1.5 Hybrid CPaaS

- 5.2 By Communication Channel

- 5.2.1 SMS and A2P Messaging

- 5.2.2 Voice and IVR

- 5.2.3 Video and WebRTC

- 5.2.4 Email

- 5.2.5 Push and In-App Notifications

- 5.2.6 Rich Communication Services (RCS) Messaging

- 5.3 By API Service

- 5.3.1 Messaging APIs

- 5.3.2 Voice APIs

- 5.3.3 Video APIs

- 5.3.4 Authentication and Security APIs

- 5.3.5 Rich Communication Services (RCS) APIs

- 5.4 By Deployment Model

- 5.4.1 Public Cloud

- 5.4.2 Private Cloud

- 5.4.3 Hybrid Cloud

- 5.5 By Enterprise Size

- 5.5.1 Small and Medium Enterprises (SMEs)

- 5.5.2 Large Enterprises

- 5.6 By End-User Vertical

- 5.6.1 IT and Telecom

- 5.6.2 BFSI

- 5.6.3 Retail and E-commerce

- 5.6.4 Healthcare

- 5.6.5 Travel and Hospitality

- 5.6.6 Logistics and Transportation

- 5.6.7 Government and Public Sector

- 5.6.8 Education

- 5.6.9 Other End-User Verticals

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 United Kingdom

- 5.7.3.2 Germany

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 South Korea

- 5.7.4.4 India

- 5.7.4.5 Rest of Asia Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 United Arab Emirates

- 5.7.5.1.2 Saudi Arabia

- 5.7.5.1.3 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Rest of Africa

- 5.7.5.1 Middle East

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Funding, Partnerships)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Twilio Inc.

- 6.4.2 Vonage Holdings Corp.

- 6.4.3 Sinch AB

- 6.4.4 Infobip Ltd.

- 6.4.5 MessageBird B.V.

- 6.4.6 Bandwidth Inc.

- 6.4.7 Plivo Inc.

- 6.4.8 8x8 Inc.

- 6.4.9 Voximplant (Zingaya Inc.)

- 6.4.10 Voxvalley Technologies

- 6.4.11 IntelePeer Cloud Communications

- 6.4.12 Wazo Communication Inc.

- 6.4.13 Avaya Inc.

- 6.4.14 AT&T Inc.

- 6.4.15 Mitel Networks Corporation

- 6.4.16 Telestax

- 6.4.17 CM.com N.V.

- 6.4.18 Kaleyra Inc.

- 6.4.19 Route Mobile Ltd.

- 6.4.20 Telnyx LLC

- 6.4.21 RingCentral Inc.

- 6.4.22 Cisco Systems Inc.

- 6.4.23 Link Mobility Group ASA

- 6.4.24 TeleSign Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment