|

시장보고서

상품코드

2043876

북미의 ADAS : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America ADAS - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

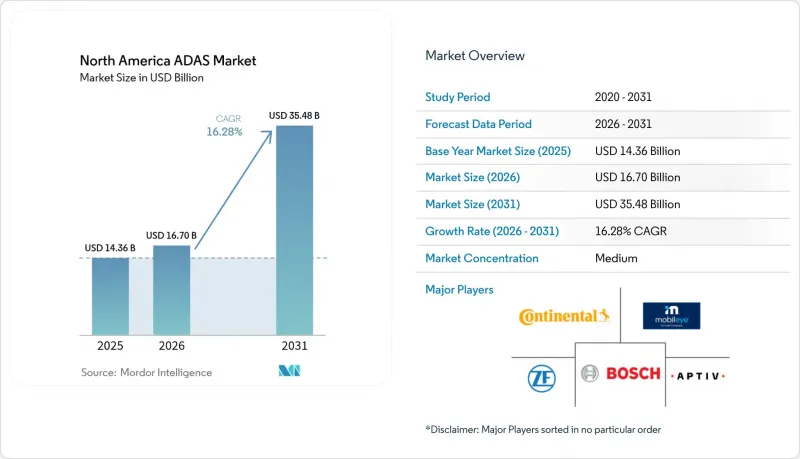

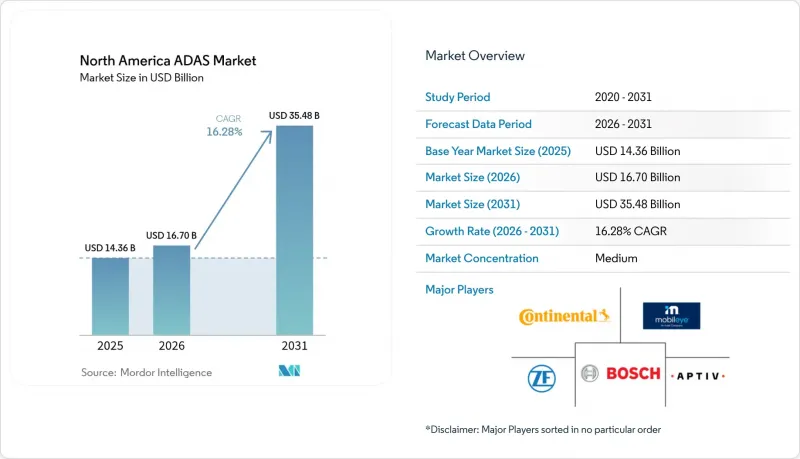

북미의 ADAS 시장 규모는 2025년에 143억 6,000만 달러로 평가되었습니다. 2026년 167억 달러에서 2031년까지 354억 8,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 16.28%를 나타낼 전망입니다.

이는 승용차 및 상용차에서 첨단 안전 및 자동화 기능으로 빠르게 전환되고 있음을 보여줍니다. 특히 미국 도로교통안전국(NHTSA)이 2029년 9월까지 모든 경차에 자동긴급제동장치(AEB) 장착을 의무화하는 등 연방정부의 안전규제 강화가 단기적인 수요 증가의 가장 큰 요인으로 작용하고 있습니다.

북미의 ADAS 시장 동향 및 인사이트

정부의 AEB 및 FCW 기준 의무화 추진

연방 정부의 규정에 따라 자동차 제조업체는 고속 주행 시에도 작동하고 저조도 환경에서 보행자를 감지할 수 있는 자동 긴급 제동 장치(AEB)를 장착해야 합니다. 이로 인해 대당 센서 수가 크게 증가하여 플랫폼의 리뉴얼 주기가 빨라지고 있습니다. Tier 1 공급업체들은 카메라, 레이더, 그리고 보급형 LiDAR를 하나의 연산장치에 통합한 융합 스택을 개발하여 목표 가격대를 초과하는 부품 비용을 증가시키지 않으면서 새로운 테스트 프로토콜을 충족하고 있습니다. 미국은 유연성을 제공하는 반면, 캐나다 교통부의 결과 중심적인 태도는 지역 전체의 조화를 저해하고 있는 것과는 대조적입니다. 컴플라이언스 대응으로 소프트웨어에 대한 지출이 앞당겨지고, 검증 주행거리가 증가하며, 2029년 기한까지 제품 출시 일정이 압축되고 있습니다.

레이더/카메라 센서 가격 하락

대량 생산과 웨이퍼 레벨 패키징으로 인해 2022-2024년 사이 77GHz 레이더 모듈의 비용은 30% 이상 절감되었으며, 엔트리급 모델에서 안전 기능 패키지의 채택 범위가 확대될 것입니다. 카메라의 평균판매가격(ASP)도 비슷한 추세를 보이고 있으며, 이는 픽셀 밀도 향상과 제조 수율 개선에 기인합니다. 솔리드 스테이트 설계의 채택으로 기존에는 1,000달러가 넘었던 LiDAR를 500달러 미만으로 구매할 수 있게 되었습니다. Hesai는 2024년 50만 1,000대 이상을 출하하여 전년 대비 134.2% 성장했습니다. 이는 비용의 하락이 급격한 보급을 촉진하고 있음을 보여줍니다. 가격 하락으로 인해 소형 세단, SUV, 심지어 이륜차까지 멀티센서 퓨전 표준화가 가속화되고 있습니다.

LiDAR 및 센서 제품군의 높은 비용

가격이 크게 하락했음에도 불구하고, 소형차를 위한 풀 프론트뷰 3센서 스택은 여전히 800달러를 초과하는 경우가 있어, OEM 업체들이 비용 경쟁이 치열한 부문에서 광범위한 도입을 주저하는 요인으로 작용하고 있습니다. 승용차용 LiDAR의 총 탑재 대수는 레이더-카메라 융합 시스템에 미치지 못하며, 레벨3 기능은 고급차 브랜드에 국한되어 있습니다. 공급업체들은 500달러 미만의 솔루션을 시장에 출시하기 위해 칩 온보드형 포토닉스 기술과 스캔 미러를 제거하기 위한 개발을 진행하고 있지만, 생산 수율은 여전히 불안정한 상황입니다.

부문 분석

교통 표지판 인식은 인프라에서 차량으로의 데이터 스트림을 통해 차량 내 분류 정확도가 향상됨에 따라 2031년까지 연평균 복합 성장률(CAGR) 25.26%로 급성장할 것으로 예측됩니다. 이 기능은 실시간 속도 제한 및 경고 정보를 궤도 계획 엔진에 공급하여 보다 높은 수준의 자율주행을 지원합니다. 2025년 매출의 30.77%로 가장 큰 비중을 차지한 적응형 크루즈 컨트롤(ACC)은 장거리 레이더 기술의 성숙과 보험사의 지지를 바탕으로 성장하고 있습니다. 적응형 크루즈 컨트롤로 인한 북미의 ADAS 시장 규모는 2029년 연방정부의 자동 긴급제동 의무화에 발맞추어 확대될 것으로 예상되며, 그 기반 역할이 더욱 강화될 것으로 전망됩니다. 비용 절감된 카메라 모듈과 표준화된 ECU 실적로 통합이 간소화됨에 따라 자동 긴급 제동, 차선 유지 지원 및 운전자 모니터링 시스템의 도입이 확대되고 있습니다.

소프트웨어 정의 차량(SDV) 전략에 따라 OEM 업체들은 판매 후 추가 기능을 번들로 제공하도록 유도하고 있으며, 운전자는 구독을 통해 사각지대 감지 및 자동 주차 기능을 이용할 수 있습니다. 북미의 ADAS 시장에서는 구매자가 인식하는 위험 프로파일에 따라 지출을 조정할 수 있기 때문에 모듈식 기능 패키지가 계속 선호되고 있습니다. 나이트 비전과 어댑티브 프론트 라이팅은 여전히 프리미엄 기능이지만, 적외선 센서의 가격 하락으로 인해 이러한 기능들이 대중화될 것으로 예측됩니다. 전반적으로, 시스템 유형 계층 구조는 기능 간 시너지 효과를 통해 소비자의 가격 책정 유연성을 유지하면서 핵심 컴퓨팅 투자 회수를 가속화할 수 있는 메커니즘을 보여줍니다.

레이더는 악천후에 대한 견고성과 중급 차량에 듀얼 및 트리플 레이더 프론트엔드를 장착할 수 있는 상품 가격으로 인해 2025년에도 33.22%의 점유율을 유지했습니다. 그럼에도 불구하고 LiDAR의 예상 CAGR 22.56%는 솔리드 스테이트 모델이 엔비디아 드라이브 오린(NVIDIA DRIVE Orin)과 통합되어 자동 비상 조향 및 250미터 전방의 강력한 물체 분류를 지원하게 되면서 전환점을 맞이할 것으로 보입니다. 메르세데스 벤츠와 볼보가 차세대 EV 플랫폼에 완전한 기능을 갖춘 스택을 도입하기로 결정함에 따라, LiDAR로 인한 북미의 ADAS 시장 규모는 빠르게 성장하고 있습니다.

차선 레벨의 시맨틱과 신호등 감지에 있어 카메라 기술은 여전히 필수적이며, 800만 화소 해상도의 채택과 함께 대량 출하가 이루어지고 있습니다. 초음파 센서는 주차 지원을 위한 5m 미만의 사각지대를 커버하고, V2X 모듈은 커넥티드 코리도(Connected Corridor)가 구축된 주에서 빠르게 보급되어 시야 범위를 넘어선 상황인식을 가능하게 하고 있습니다. 센서 융합 알고리즘은 중복성을 제공하고, 마그나(Magna)의 'Collective Perception'은 네트워크화된 환경 트윈을 구축하여 각 모달리티 간의 원활한 인계인수를 실현합니다. 공급업체 간 경쟁은 칩셋 로드맵과 인식 소프트웨어를 중심으로 전개되고 있으며, 개별 하드웨어 성능 지표의 중요성은 점점 줄어들고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측(금액(달러) 및 수량(대수))

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The North America ADAS Market size was valued at USD 14.36 billion in 2025 and estimated to grow from USD 16.7 billion in 2026 to reach USD 35.48 billion by 2031, at a CAGR of 16.28% during the forecast period (2026-2031).

Underscoring a swift shift toward advanced safety and automation features across passenger and commercial vehicles. Intensifying federal safety rules, notably the National Highway Traffic Safety Administration's requirement that all light vehicles incorporate automatic emergency braking by September 2029, is the largest catalyst for near-term demand growth..

North America ADAS Market Trends and Insights

Government-mandated AEB & FCW standards

Federal rulemaking compels OEMs to integrate automatic emergency braking that functions at highway speeds and detects pedestrians in low-light situations, driving material increases in sensor count per vehicle, and accelerating platform refresh cycles. Tier 1 suppliers are bundling camera, radar, and growing LiDAR modalities into single-calculator fusion stacks that meet the new test protocol without inflating the bill-of-materials beyond target price points. U.S. prescriptions contrast with Transport Canada's outcome-based stance that offers flexibility but stalls region-wide harmonization. Compliance work pulls forward software spending, boosts validation mileage, and compresses launch timelines into the 2029 deadline window.

Declining radar / camera sensor prices

Volume production and wafer-level packaging have cut 77 GHz radar module costs by more than 30% between 2022 and 2024, widening eligibility for safety suites on entry trims. Camera ASPs follow a similar curve because pixel density has risen while manufacturing yields improve. Due to solid-state designs, LiDAR, historically priced above USD 1,000, is now available below USD 500; Hesai shipped over 501,000 units in 2024, a 134.2% jump year on year, reflecting how cost deflation fuels exponential uptake. The affordability shift accelerates the standardization of multi-sensor fusion across compact sedans, SUVs, and even two-wheelers.

High LiDAR & sensor-suite costs

Even with sharp declines, a full forward-looking tri-sensing stack can still exceed USD 800 on compact vehicles, discouraging OEMs from broad deployment in cost-competitive segments. Passenger-car LiDAR trails radar-camera fusion in total installations, leaving Level 3 functions confined to premium nameplates. Suppliers are developing chip-on-board photonics and scanning-mirror eliminations to bring sub-USD 500 solutions to market, yet production yields remain volatile.

Other drivers and restraints analyzed in the detailed report include:

- OEM software-defined platform upgrades

- Insurance premium discounts for ADAS-equipped vehicles

- Regulatory patchwork across the NAFTA region

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Traffic sign recognition surged 25.26% CAGR through 2031 as infrastructure-to-vehicle data streams enhance on-board classification accuracy. The feature underpins higher-level automation by feeding real-time speed-limit and warning information into trajectory planning engines. Adaptive cruise control, which commanded the largest 30.77% revenue block in 2025, benefits from long-range radar maturity and insurer endorsement. The North American ADAS market size attributed to adaptive cruise control is projected to scale in lockstep with the 2029 federal AEB cut-in, reinforcing its foundational role. Autonomous emergency braking, Lane Keep Assist, and driver monitoring system installations expand as cost-down camera modules and standardized ECU footprints simplify integration.

Software-defined vehicle strategies encourage OEMs to bundle incremental functions after sale, letting drivers unlock blind-spot detection or automated parking over a subscription. The North American ADAS market continues to favor modular feature packaging because buyers can tailor spend against perceived risk profiles. Night-vision and adaptive front-lighting remain premium, yet falling infrared sensor costs foreshadow trickle-down migration. Overall, the system-type hierarchy demonstrates how cross-feature synergies accelerate payback on core compute investment while maintaining consumer pricing flexibility.

Radar retained a 33.22% share in 2025, due to resilience in adverse weather and commodity pricing that enables dual and tri-radar front ends on mid-tier cars. Still, LiDAR's expected 22.56% CAGR signals an inflection as solid-state models integrate with NVIDIA DRIVE Orin to support automated emergency steering and robust object classification out to 250 meters. The North American ADAS market size attributed to LiDAR is on a steep trajectory as Mercedes-Benz and Volvo commit to feature-complete stacks on next-generation EV platforms.

Camera technology remains indispensable for lane-level semantics and traffic light detection, with volume shipments aligning with 8-megapixel resolution adoption. Ultrasonic sensors cover sub-5-meter blind spots for park assist, while V2X modules multiply in connected corridor states to extend situational awareness beyond line of sight. Sensor fusion algorithms deliver redundancy, and Magna's Collective Perception constructs networked environmental twins to smooth handoffs between modalities. Supplier competition increasingly revolves around chipset roadmaps and perception software, overshadowing discrete hardware performance metrics.

The North American ADAS Market Report is Segmented by System Type (Adaptive Cruise Control System, Adaptive Front-Lighting, and More), Sensor Technology (Radar, Li-Dar, Camera, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Level of Autonomy (Level 1, Level 2, and More), Sales Channel (OEM and After-Market), and Country. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- Robert Bosch GmbH

- Continental AG

- ZF Friedrichshafen AG

- Mobileye (Intel)

- Aptiv PLC

- DENSO Corporation

- Magna International

- Hyundai Mobis

- Autoliv Inc.

- NVIDIA Automotive

- Aisin Corp.

- Valeo SA

- Hitachi Astemo

- Velodyne Lidar

- Waymo LLC

- Tesla Inc.

- Luminar Technologies

- Gentex Corp.

- Texas Instruments

- ON Semiconductor

- Analog Devices

- Renesas Electronics

- BlackBerry QNX

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government-mandated AEB & FCW standards

- 4.2.2 Declining radar / camera sensor prices

- 4.2.3 OEM software-defined platform upgrades

- 4.2.4 HD-mapped highway & V2X corridors expansion

- 4.2.5 Insurance premium discounts for ADAS-equipped vehicles

- 4.2.6 After-market retrofit kits for commercial fleets

- 4.3 Market Restraints

- 4.3.1 High LiDAR & sensor-suite costs

- 4.3.2 Regulatory patchwork across NAFTA region

- 4.3.3 Shortage of certified calibration technicians

- 4.3.4 Cyber-security risks in OTA ADAS updates

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By System Type

- 5.1.1 Adaptive Cruise Control

- 5.1.2 Autonomous Emergency Braking

- 5.1.3 Lane Keeping Assist

- 5.1.4 Lane Departure Warning

- 5.1.5 Blind-Spot Detection

- 5.1.6 Driver Monitoring / Drowsiness Alert

- 5.1.7 Night Vision

- 5.1.8 Adaptive Front-lighting

- 5.1.9 Traffic Sign Recognition

- 5.2 By Sensor Technology

- 5.2.1 Radar

- 5.2.2 Camera

- 5.2.3 LiDAR

- 5.2.4 Ultrasonic

- 5.2.5 Infra-red

- 5.2.6 V2X Modules

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Medium and Heavy Commercial Vehicles

- 5.3.4 Two-Wheelers (Motorcycles)

- 5.4 By Level of Autonomy (SAE)

- 5.4.1 Level 1

- 5.4.2 Level 2

- 5.4.3 Level 3

- 5.4.4 Level 4

- 5.4.5 Level 5

- 5.5 By Sales Channel

- 5.5.1 OEM-fitted

- 5.5.2 After-market Retrofit

- 5.6 By Country

- 5.6.1 United States

- 5.6.2 Canada

- 5.6.3 Rest of North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Continental AG

- 6.4.3 ZF Friedrichshafen AG

- 6.4.4 Mobileye (Intel)

- 6.4.5 Aptiv PLC

- 6.4.6 DENSO Corporation

- 6.4.7 Magna International

- 6.4.8 Hyundai Mobis

- 6.4.9 Autoliv Inc.

- 6.4.10 NVIDIA Automotive

- 6.4.11 Aisin Corp.

- 6.4.12 Valeo SA

- 6.4.13 Hitachi Astemo

- 6.4.14 Velodyne Lidar

- 6.4.15 Waymo LLC

- 6.4.16 Tesla Inc.

- 6.4.17 Luminar Technologies

- 6.4.18 Gentex Corp.

- 6.4.19 Texas Instruments

- 6.4.20 ON Semiconductor

- 6.4.21 Analog Devices

- 6.4.22 Renesas Electronics

- 6.4.23 BlackBerry QNX

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment