|

시장보고서

상품코드

2044104

아시아태평양의 데이터센터 냉각 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Asia-Pacific Data Center Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

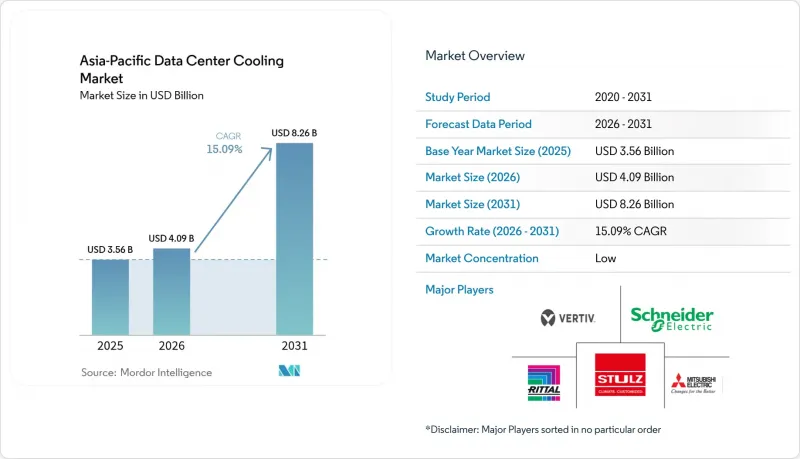

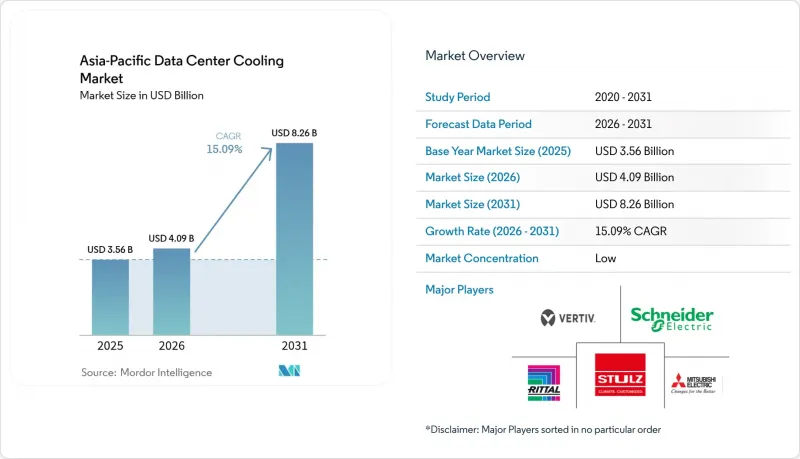

아시아태평양의 데이터센터 냉각 시장 규모는 2025년 35억 6,000만 달러로 평가되었습니다. 2026년 40억 9,000만 달러로 확대되어 2031년까지 82억 6,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR 15.09%를 나타낼 전망입니다.

생성형 AI 서버의 도입 가속화, 중국의 PUE 1.3 이하 규정, 싱가포르의 SS 715 : 2025 표준과 같은 효율성 관련 규제 의무화, 마이크로소프트, 구글, 알리바바, 텐센트의 하이퍼스케일 시설 확장으로 고성능 열관리 시스템에 대한 수요 증가 하고 있습니다. 랙당 30kW를 넘어서면 공냉식 냉각은 경제적, 기술적 한계가 발생하기 때문에 액체 냉각 아키텍처가 주목받고 있지만, 기존 시설이나 30kW 미만의 도입 환경에서는 여전히 공냉식 솔루션이 주류를 이루고 있습니다. 사업자들이 건설 일정을 18개월에서 6개월로 단축하는 가운데, 하드웨어, 소프트웨어, 신속한 조립식 공사를 결합한 벤더들이 수주를 따내고 있습니다. 2024년 철강 및 반도체 공급 부족으로 공급망 리스크는 완화되고 있지만, 동남아시아의 HVAC(공조, 환기, 냉방) 숙련된 인력 부족은 여전히 단기적인 병목현상으로 남아있습니다.

아시아태평양의 데이터센터 냉각 시장 동향 및 인사이트

AI/생성형 AI를 통한 랙 전력 밀도 향상으로 액체 냉각으로의 전환 촉진

생성형 AI 클러스터로 인해 랙 밀도는 8-12kW에서 40-60kW로 상승하고 있으며, 이 영역에서 공랭식 시스템은 비용과 열적 여유 측면에서 한계에 도달하고 있습니다. 2025년 NTT 도쿄 캠퍼스에 도입된 레노버의 'Neptune' 직접 투 칩 플랫폼은 50kW 랙을 지원하면서 40%의 에너지 절감을 실현했습니다. 또한, 중국의 2024년판 표준은 캐비닛 당 8kW를 초과하는 경우 액체 냉각을 의무화하고 있습니다. 싱가포르의 개정된 SS 715 표준은 고밀도 홀에 대해 PUE 1.2 미만을 요구하고 있습니다. 30kW 이상의 밀도에서는 침수 냉각 설계로 냉각기가 필요하지 않아 총 소유 비용을 최대 30%까지 절감할 수 있지만, OEM의 보증 조건과 절연 유체 안전에 정통한 기술자 부족으로 인해 도입이 더디게 진행되고 있습니다. 따라서 아시아태평양의 데이터센터 냉각 시장에서는 액체 루프를 지원하는 펌프, 플레이트, 열교환기 모듈에 대한 투자가 확대되고 있습니다.

클라우드 대기업의 하이퍼스케일 확장으로 수요 기반 마련

마이크로소프트의 175억 달러 규모의 인도 계획과 구글의 150억 달러 규모의 안드라 프라데시 주 캠퍼스는 각각 200-300MW의 IT 부하를 필요로 하며, 2027년까지 이 지역 냉각기 생산량의 15-20%를 흡수할 것으로 예측됩니다. Oracle의 여러 국가에 걸친 지역 계획은 모듈식 기계 블록의 6개월 납기를 지정하고 있으며, 이는 Vertiv와 슈나이더 일렉트릭에 대한 수주를 가속화하고 있습니다. 중국의 거대 기업인 알리바바와 텐센트는 재생에너지 50% 조달을 조건으로 한 광동성과 장쑤성의 토지 보조금에 매료되어 2025년에 180MW를 추가했습니다. 이러한 하이퍼스케일의 물결은 벤더 시장을 양극화시켜 유동성이 높은 지적재산권과 벤더 파이낸싱이 가능한 재무구조를 갖춘 공급업체에게 유리하게 작용하고 있습니다.

전력 및 토지 비용 상승으로 수익률 압박

싱가포르의 전기 요금은 2025년 0.35 싱가포르 달러/kWh(0.26달러/kWh)까지 상승했으며, 2030년까지 추가 할당 가능한 IT 부하는 300MW에 불과하고, 1,000평방피트(695평방피트) 이상 부지의 가격이 급등하고 있습니다. 도쿄 도심의 경우 평방미터당 1만 5,000달러를 넘어섰고, 대기시간의 악영향에도 불구하고 오사카로의 용량 이동을 유발하고 있습니다. 시드니와 홍콩에서도 비슷한 압력으로 인해 건설이 교외와 광동성으로 이동하고 있지만, 전력망과 광섬유의 부족으로 인해 급속한 확장을 방해하고 있습니다. 공냉은 시설 전력비의 40%를 차지하는 반면, 수냉은 15%를 차지하기 때문에 비용 상승으로 인해 기존 사업자들도 브라운필드 자산이라도 직접 투 칩 루프로의 전환을 추진하고 있습니다.

부문 분석

2025년, 공랭식 시스템이 구축된 운영 노하우와 방대한 도입 실적에 힘입어 공랭식 시스템이 매출의 59.96%를 차지했습니다. 그러나 AI 생성 랙의 전력 소비가 40kW를 넘어서면서 후면 도어 열교환기 및 침수 탱크가 팬 구동식 CRAC 유닛보다 밀도가 높아짐에 따라, 아시아태평양의 데이터센터 냉각 시장에서 액체 냉각 아키텍처 시장 규모는 CAGR 16.13%로 확대될 것으로 전망됩니다. 확대될 것으로 예측됩니다. 케펠 데이터센터 액침냉각 도입 시 PUE 1.03을 달성하고 냉각기를 완전히 제거함으로써 공랭식 기준 대비 설비투자(Capex) 25%, 운영비용(OpEx) 40%를 절감한 것으로 입증됐습니다. CoolIT의 직접 투 칩 루프를 통해 일본과 호주의 데이터센터 홀에서 50kW의 리트로핏이 가능해져 자산 수명을 7년 연장할 수 있게 되었습니다.

액체냉각의 모멘텀에도 불구하고, 30kW 미만의 환경, 프리쿨링 적용 기간이 긴 기후 및 인도네시아, 베트남 등 절연유체 기술이 부족한 시장에서는 공냉이 여전히 전술적 우위를 유지하고 있습니다. 다이킨의 자기 베어링식 냉각기는 도쿄에서 톤당 0.45kW를 달성하여, 물 사용 제한으로 냉각탑을 설치할 수 없는 곳에서도 공냉식 냉각 방식의 유용성을 유지하고 있습니다. 아시아태평양의 데이터센터 냉각 시장에서는 저밀도 영역에는 팬 코일을, AI 영역에는 펌프식 액체 루프를 결합한 하이브리드 구성이 계속 선호되고 있으며, 신중한 사업자에게는 전환의 장벽이 낮아지고 있습니다.

컴퓨터실용 에어핸들러는 2025년 기준 41.55%의 점유율을 유지했지만, 액체 루프를 제어하는 펌프, 밸브, 판형 열교환기 등으로 수요가 이동하고 있습니다. 그룬트포스와 자이람은 35-60℃의 수온에 대응하는 가변속 펌프를 출시하고, 인도에서 마이크로소프트와 구글과 계약을 체결했습니다. 알파라발의 컴파 블록 플레이트는 침지 쉘 내에서 95%의 열전달 효율을 달성하여 싱가포르와 도쿄에서 수 메가와트 규모의 수주를 주도하고 있습니다.

냉각기는 공조 홀용 고효율 마그네틱 베어링 유닛과 액체 순환 구역용 소형 스키드형 열교환기로 구분됩니다. 모니터링 소프트웨어 시장 성장률은 현재 CAGR 약 17%로 가장 빠르게 성장하고 있으며, 슈나이더일렉트릭의 'EcoStruxure IT'와 버티브의 'Trellis'는 머신러닝을 통한 설정값 제어를 통해 에너지 소비를 10-15% 절감하고 있습니다. 수냉식 기술의 보급이 확대됨에 따라 아시아태평양의 데이터센터 냉각 시장에서는 대용량 송풍기보다 정밀한 유량 제어 하드웨어가 점점 더 중요해질 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 아시아태평양 현재 데이터센터 규모에 관한 분석

제6장 시장 규모와 성장 예측

제7장 경쟁 구도

제8장 시장 기회와 향후 전망

KTHThe Asia-Pacific data center cooling market size is expected to increase from USD 3.56 billion in 2025 to USD 4.09 billion in 2026 and reach USD 8.26 billion by 2031, growing at a CAGR of 15.09% over 2026-2031.

Accelerating adoption of generative-AI servers, mandatory efficiency codes such as China's PUE <= 1.3 rule and Singapore's SS 715:2025 standard, and hyperscale build-outs by Microsoft, Google, Alibaba, and Tencent are expanding demand for high-performance thermal systems. Liquid architectures are gaining traction because air-based cooling reaches economic and technical limits above 30 kW per rack, yet air solutions still dominate legacy estates and sub-30 kW deployments. Vendors that combine hardware, software, and rapid prefabrication are winning contracts as operators compress build schedules from 18 months to six. Supply-chain risk is easing after 2024 steel and semiconductor shortages, but HVAC-skilled labor gaps in Southeast Asia remain a near-term bottleneck.

Asia-Pacific Data Center Cooling Market Trends and Insights

AI/Gen-AI Rack Power Densification Drives Liquid Pivot

Generative-AI clusters are lifting rack densities from 8-12 kW toward 40-60 kW, where air systems lose both cost and thermal headroom. Lenovo's Neptune direct-to-chip platform installed at NTT's Tokyo campus in 2025 saved 40% energy while supporting 50 kW racks, and China's 2024 code now obliges liquid cooling above 8 kW per cabinet. Singapore's updated SS 715 demands PUE < 1.2 for high-density halls.At densities beyond 30 kW, immersion designs eliminate chillers and cut total cost of ownership by up to 30%, although uptake is moderated by OEM warranty terms and a shortage of technicians versed in dielectric-fluid safety. The Asia-Pacific data center cooling market is therefore shifting capital toward pumps, plates, and heat-exchanger modules that underpin liquid loops.

Hyperscale Build-Outs by Cloud Majors Anchor Demand

Microsoft's USD 17.5 billion India program and Google's USD 15 billion Andhra Pradesh campus each require 200-300 MW of IT load, absorbing 15-20% of regional chiller output through 2027. Oracle's multi-country region specified six-month delivery of modular mechanical blocks, accelerating orders for Vertiv and Schneider Electric. Chinese giants Alibaba and Tencent added 180 MW in 2025, drawn by land subsidies in Guangdong and Jiangsu that are conditional on 50% renewable sourcing. The hyperscale wave bifurcates the vendor field, rewarding suppliers with liquid IP and balance-sheet strength capable of vendor financing.

Rising Electricity and Land Costs Compress Margins

Singapore's tariff climbed to SGD 0.35/kWh in 2025 (USD 0.26/kWh) and the city's land scarcity allocates only 300 MW of extra IT load through 2030, inflating plots above SGD 1,000 ft2 (USD 695 ft2). Tokyo inner districts exceed USD 15,000 m2, triggering capacity shifts to Osaka despite latency penalties. Similar pressures in Sydney and Hong Kong redirect builds toward outer suburbs or Guangdong, but grid and fiber gaps undermine quick scaling. Because air cooling can represent 40% of a facility's power bill versus 15% for liquid, cost inflation is nudging incumbents to retrofit direct-to-chip loops even on brownfield assets.

Other drivers and restraints analyzed in the detailed report include:

- Edge Data Centers at 5G Micro-Regions Need Compact Cooling

- Corporate Net-Zero and RE100 Pledges Elevate Efficiency

- Water-Use Restrictions Squeeze Evaporative Architectures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air-based systems delivered 59.96% revenue in 2025, supported by entrenched operational know-how and a vast installed base. Yet the Asia-Pacific data center cooling market size for liquid architectures is forecast to expand at a 16.13% CAGR as generative-AI racks exceed 40 kW, a density where rear-door exchangers and immersion tanks outrun fan-driven CRAC units. Immersion deployments at Keppel Data Centres achieved PUE 1.03 and removed chillers entirely, proving a 25% capex and 40% opex cut over air baselines. Direct-to-chip loops from CoolIT allowed 50 kW retrofits in Japanese and Australian halls, adding seven years to asset life.

Despite liquid's momentum, air cooling preserves tactical advantages below 30 kW, in climates with extended free-cooling windows, and in markets short on dielectric-fluid skills such as Indonesia and Vietnam. Daikin's magnetic-bearing chillers reached 0.45 kW per ton in Tokyo, sustaining air's relevance where water limits prohibit towers. The Asia-Pacific data center cooling market continues to reward hybrid estates that blend fan coils for low-density rows with pumped liquid loops for AI zones, easing migration paths for cautious operators.

Computer-room air handlers maintained 41.55% share in 2025, but demand is tilting toward pumps, valves, and plate heat exchangers that orchestrate liquid loops. Grundfos and Xylem introduced variable-speed pumps tailored to 35-60 °C water, securing Microsoft and Google contracts in India. Alfa Laval's Compabloc plates hit 95% heat-transfer efficiency inside immersion shells, driving multi-megawatt orders from Singapore and Tokyo.

Chillers bifurcate between high-efficiency magnetic-bearing units for air halls and compact skid exchangers for liquid districts. Monitoring software now grows fastest at roughly 17% CAGR, with Schneider Electric EcoStruxure IT and Vertiv Trellis trimming energy 10-15% via machine-learning set-point control. As liquid penetration deepens, the Asia-Pacific data center cooling market will progressively prize precision flow hardware over bulk air movers.

The Asia Pacific Data Center Cooling Market Report is Segmented by Cooling Technology (Air-Based, and Liquid-Based), Cooling Component (CRAH/CRAC, Chillers and Heat Exchangers, Cooling Towers and Dry Coolers, and More), Tier Type (Tier 1 and 2, and Tier 4), Data Center Size (Small, Medium, Large, and Hyperscale), Data Center Type (Colocation, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Vertiv Group Corp.

- Schneider Electric SE

- STULZ GmbH

- Huawei Digital Power Technologies Co., Ltd.

- Johnson Controls International plc

- Rittal GmbH & Co. KG

- Daikin Applied (Daikin Industries, Ltd.)

- Fujitsu General Limited

- Mitsubishi Electric Corporation

- Hitachi Cooling and Heating (Johnson Controls-Hitachi Air Conditioning)

- Baltimore Aircoil Company

- Nortek Air Solutions LLC

- Delta Electronics, Inc.

- Grundfos Holding A/S

- CoolIT Systems, Inc.

- Submer Technologies, S.L.

- Iceotope Technologies Ltd.

- Alfa Laval AB

- Trane Technologies plc

- NTT Facilities, Inc.

- Xylem Inc.

- Refrion S.r.l.

- Green Revolution Cooling, Inc.

- Munters AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI/Gen-AI Rack Power Densification

- 4.2.2 Hyperscale Build-Outs by US and Chinese Cloud Majors

- 4.2.3 Edge Data Centers at 5G Micro-Regions

- 4.2.4 Corporate Net-Zero and RE100 Pledges

- 4.2.5 Modular Prefabricated Cooling Blocks

- 4.2.6 District-Cooling Integration Pilots (Singapore-Style)

- 4.3 Market Restraints

- 4.3.1 Rising Electricity and Land Costs in Tier-1 APAC Cities

- 4.3.2 Scarcity of HVAC-Certified Labor in Emerging Southeast Asia

- 4.3.3 Water-Use Restrictions in Drought-Prone India and Australia

- 4.3.4 Lengthy Environmental Permitting and Community Pushback

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 ANALYSIS OF THE CURRENT DATA CENTER FOOTPRINT IN ASIA-PACIFIC

- 5.1 Analysis of IT Load Capacity (MW) and Area footprint (Sq. Ft.) of Data Centers (for the Period of 2019-2031)

- 5.2 Analysis of Major Data Center Hotspots in Asia-Pacific

- 5.3 Analysis of Major Upcoming Hyperscale Facilities in Asia-Pacific

6 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 6.1 By Cooling Technology

- 6.1.1 Air-Based Cooling

- 6.1.1.1 CRAH

- 6.1.1.2 Chiller and Economizer

- 6.1.1.3 Cooling Tower (Direct, Indirect, Two-Stage)

- 6.1.1.4 Others

- 6.1.2 Liquid-Based Cooling

- 6.1.2.1 Immersion Cooling

- 6.1.2.2 Direct-to-Chip Cooling

- 6.1.2.3 Rear-Door Heat Exchanger

- 6.1.1 Air-Based Cooling

- 6.2 By Cooling Component

- 6.2.1 Computer-Room Air Handlers (CRAH/CRAC)

- 6.2.2 Chillers and Heat-Exchanger Units

- 6.2.3 Cooling Towers and Dry Coolers

- 6.2.4 Pumps and Valves

- 6.2.5 Control and Monitoring Software

- 6.3 By Tier Type

- 6.3.1 Tier 1 and 2

- 6.3.2 Tier 3

- 6.3.3 Tier 4

- 6.4 By Data Center Size

- 6.4.1 Small Data Center

- 6.4.2 Medium Data Center

- 6.4.3 Large Data Center

- 6.4.4 Hyperscale Data Center

- 6.5 By Data Center Type

- 6.5.1 Colocation Data Center

- 6.5.2 Hyperscalers Data Center/CSPs

- 6.5.3 Enterprise and Edge Data Center

- 6.6 By Country

- 6.6.1 China

- 6.6.2 Japan

- 6.6.3 India

- 6.6.4 South-Korea

- 6.6.5 Australia and New Zealand

- 6.6.6 Rest of Asia-Pacific

7 COMPETITIVE LANDSCAPE

- 7.1 Market Share Analysis

- 7.2 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 7.2.1 Vertiv Group Corp.

- 7.2.2 Schneider Electric SE

- 7.2.3 STULZ GmbH

- 7.2.4 Huawei Digital Power Technologies Co., Ltd.

- 7.2.5 Johnson Controls International plc

- 7.2.6 Rittal GmbH & Co. KG

- 7.2.7 Daikin Applied (Daikin Industries, Ltd.)

- 7.2.8 Fujitsu General Limited

- 7.2.9 Mitsubishi Electric Corporation

- 7.2.10 Hitachi Cooling and Heating (Johnson Controls-Hitachi Air Conditioning)

- 7.2.11 Baltimore Aircoil Company

- 7.2.12 Nortek Air Solutions LLC

- 7.2.13 Delta Electronics, Inc.

- 7.2.14 Grundfos Holding A/S

- 7.2.15 CoolIT Systems, Inc.

- 7.2.16 Submer Technologies, S.L.

- 7.2.17 Iceotope Technologies Ltd.

- 7.2.18 Alfa Laval AB

- 7.2.19 Trane Technologies plc

- 7.2.20 NTT Facilities, Inc.

- 7.2.21 Xylem Inc.

- 7.2.22 Refrion S.r.l.

- 7.2.23 Green Revolution Cooling, Inc.

- 7.2.24 Munters AB

8 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 8.1 White-Space and Unmet-Need Assessment