|

시장보고서

상품코드

2044105

북미의 데이터센터 냉각 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America Data Center Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

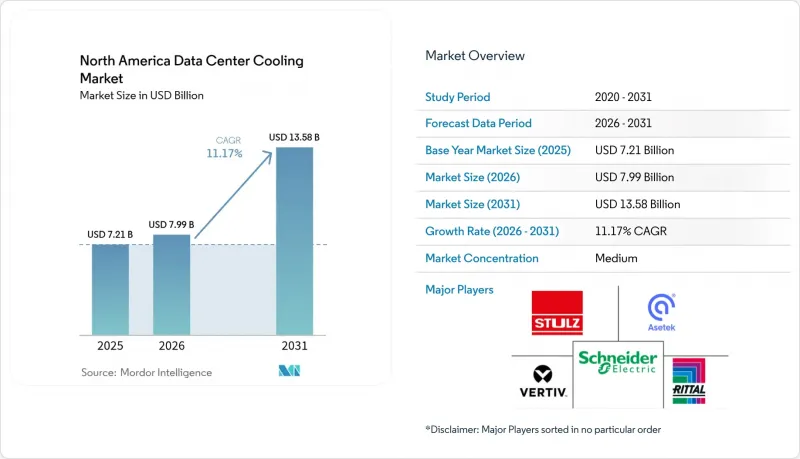

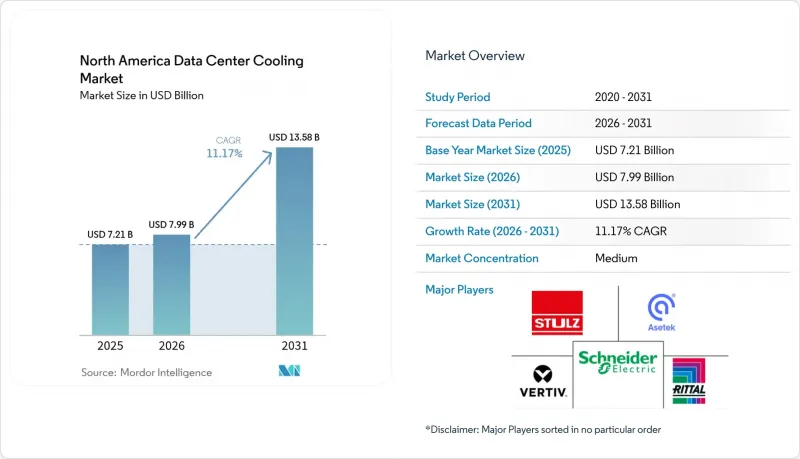

북미의 데이터센터 냉각 시장 규모는 2025년에 72억 1,000만 달러로 평가되었습니다. 2026년 79억 9,000만 달러에서 2031년까지 135억 8,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 11.17%를 나타낼 전망입니다.

40kW 이상의 랙 밀도가 증가함에 따라, 사업자들은 기존의 공랭식 시스템에서 프로세서에서 직접 열을 제거하는 액체 냉각 아키텍처로 전환해야 합니다. 이러한 전환은 임대 계약 갱신을 전력 사용 효율(PUE) 벤치마크와 연계하는 연방 정부의 규제에 의해 촉진되고 있습니다. 대상 설비 비용의 최대 30%를 공제해주는 '인플레이션 감소법'의 세액공제로 인해 지구온난화지수(GWP)가 높은 냉각기의 폐기가 가속화되고 있으며, 사막지역 시장의 주정부 물 사용량 제한으로 인해 폐루프식 드라이쿨러에 대한 수요가 증가하고 있습니다. HVAC 대기업들이 냉각기 제품군 개편을 추진하는 가운데, 액체냉각 전문업체들이 칩온도 25℃ 이하를 보장하는 설계 수주를 따내면서 경쟁은 더욱 치열해지고 있습니다. 또한, 개발업체들은 부지 선정과 총소유비용에 영향을 미치는 북버지니아의 전력망 제약과 가뭄 관련 보험 할증료에 대응하기 위해 노력하고 있습니다.

북미의 데이터센터 냉각 시장 동향 및 인사이트

미국 정부의 지속가능성 관련 대통령령에 따른 엄격한 PUE 목표 설정

연방 정부 기관은 2027년까지 신축 시설의 경우 PUE 비율이 1.4 미만, 기존 시설의 경우 1.5 미만임을 증명해야 하며, 이에 따라 주변부 에어핸들러에 의존하는 기존의 레이즈드 플로어 설계는 사실상 채택 대상에서 제외됩니다. 개정된 임대차 규정에 따르면, 집주인은 서브 미터를 통한 냉각 에너지 데이터를 공유해야 하며, 효율에 관한 계약 조건이 충족되지 않으면 세입자는 계약을 해지할 권리가 있습니다. 계약업체들은 PUE를 최대 0.20포인트까지 절감할 수 있는 가변속 압축기를 갖춘 모듈식 냉각기 플랜트로 전환하고 있습니다. 과거 에어갭 방식의 보안을 선호했던 국방 관련 워크로드에서도 중앙 플랜트 부하를 줄이기 위해 리어 도어형 열교환기를 채택하고 있습니다. 상업용 테넌트도 연방정부의 기대에 부응하여 멀티테넌트 제공업체에 유사한 효율성 기준을 보장할 것을 요구하고 있습니다.

하이퍼스케일 시설의 랙 밀도가 급증하고 있습니다.

최첨단 AI 모델을 학습하는 클러스터의 경우, 랙당 40kW를 초과하는 것이 일반화되어 있으며, 고대역폭 메모리와 멀티 다이 패키지로 인한 발열 집중으로 인해 일부 GPU 구성의 경우 80kW에 육박하는 경우도 있습니다. 이러한 부하 하에서 에너지 소비가 큰 팬을 과도하게 배치하지 않으면 공기 시스템에서 흡기 온도를 27°C 이하로 유지하기가 어렵습니다. 하이퍼스케일러 업체들은 프로세서의 열이 실내 공기로 유입되기 전에 70%-90%를 차단하는 '직접 투 칩(Direct to Chip)' 방식의 콜드 플레이트로 전환하고 있으며, 이를 통해 공조장치에 대한 부하를 줄이고 있습니다. 또한, 이러한 고밀도화는 입지 선정 기준도 바꾸고 있으며, 사업자들은 전력비용이 낮고 프리쿨링이 가능한 시간이 긴 기후 지역으로 진출하고 있습니다. 기존의 공조 인프라는 저밀도 스토리지 컬럼에 재사용되어 침몰된 투자를 최대한 활용하고, 액체 냉각 시스템이 컴퓨팅 코어를 보호하는 형태로 재사용됩니다.

전력망 제약으로 인해 버지니아주 북부의 신규 건설이 지연되고 있습니다.

도미니언 에너지의 송전 대기자 명단에는 2026년 1월 7GW가 넘는 계통연계 신청이 등록되어 있으며, 신규 변전소를 필요로 하는 프로젝트의 평균 대기 시간은 36개월에 달할 전망입니다. 500kV 송전선로에 대한 투자 부족과 새로운 송전 회랑에 대한 지역 주민의 반대로 인해 용량 확대가 정체되어 개발업체들은 예비 발전 설비를 검토하거나 오하이오 주나 노스캐롤라이나 주로의 이전을 고려해야 하는 상황에 처해 있습니다. 수소연료전지와 같은 잠정적인 해결책은 막대한 설비투자가 필요하고, 추가적인 대기오염 허가 심사를 받아야 합니다. 일부 사업자들은 기존 피더의 여유 용량에 맞추기 위해 시설 규모를 축소하고 있으며, 과거 메가사이트 위주였던 투자 계획이 세분화되고 있습니다. 또한, 혼잡 리스크로 인해 대출기관이 지연분을 필요수익률에 반영하기 때문에 자금조달 비용도 상승하고 있습니다.

부문 분석

액체 냉각 방식은 2031년까지 연평균 복합 성장률(CAGR) 12.54%로 성장하여 2025년에도 여전히 59.64%의 점유율을 차지하며 공랭식 냉각 방식을 크게 상회했습니다. 북미의 데이터센터 냉각 시장에서 액체 냉각 솔루션의 규모가 확대되고 있습니다. 이는 하이퍼스케일러 업체들이 현재 랙당 40-80kW를 소비하는 GPU를 수용하는 컴퓨팅 로우를 개조하고 있기 때문입니다. 엣지 노드의 침수 냉각 탱크는 공간과 소음의 제약을 해결하고, 대규모 트레이닝 클러스터에서는 DTC(Direct-to-Chip) 플레이트가 주류를 이루고 있습니다. 리어 도어형 열교환기는 공랭식 홀의 수명을 연장하고 설비투자 부담을 줄여주는 가교역할을 합니다. HVAC 업체들은 액체 냉각 스키드 주문이 수백 퍼센트 증가했다고 밝혔으며, 이는 틈새 실험이 아니라 장기적인 전환을 암시합니다. 저 GWP 냉매를 요구하는 규제 움직임은 사업자가 냉각기를 완전히 생략하고 건식 냉각기를 통해 열을 배출하는 온수 루프에 의존하는 것을 더욱 부추기고 있습니다.

이러한 하이브리드화 추세는 두 기술이 공존하는 것을 의미합니다. 운영자는 워크로드에 따라 홀을 구분하고, AI는 액체 냉각 구역을 할당하고, 스토리지 및 네트워크 장비는 공랭식으로 유지합니다. 이러한 유연한 접근 방식은 과거 투자를 보호하면서 시설 직원이 단계적으로 기술을 습득할 수 있도록 도와줍니다. 공급업체들은 현재 두 체제를 조정하는 제어 소프트웨어를 번들로 제공하고 있으며, 가장 유리한 열적 여유가 있는 랙으로 워크로드를 이동시키고 있습니다. 액체 냉각의 보급이 확대됨에 따라 센서, 피팅, 퀵 디스커넥트 커플링에 대한 애프터마켓 수요가 발생하여 부수적인 수익원이 개척되고 있습니다. 북미의 데이터센터 냉각 시장에서는 2상 냉매 루프를 평가하는 파일럿 프로젝트가 계속 진행되고 있지만, 상용화 시기는 현재의 예측 기간을 넘어설 가능성이 있습니다.

2025년에는 컴퓨터실용 에어핸들러가 40.72%의 점유율을 차지했으며, 이는 이 지역 전체에서 고층 홀의 역사적 기반을 반영합니다. 그러나 펌프 및 밸브는 액체 기술의 급격한 증가를 반영하여 CAGR 12.66%를 나타낼 것으로 예측됩니다. 최신 루프에는 정밀한 유량 제어가 필요합니다. 약간의 불균형만 있어도 칩 온도가 급상승하여 성능이 저하될 수 있습니다. 각 제조업체들은 유량 센서를 내장한 가변속 펌프나 회로의 밸런스를 실시간으로 자동 조절하는 스마트 밸브로 이에 대응하고 있습니다. 냉각기는 여전히 자본 프로젝트에서 가장 큰 단일 품목이지만, 그 역할은 모듈화로 전환되고 있으며, 단계적인 IT 도입에 맞추어 500kW 단위의 블록으로 현장에 반입되고 있습니다.

제어 소프트웨어는 제품의 차별화 요소로, AI 기반 플랫폼이 부하 패턴을 학습하고 추론 처리의 급격한 증가에 앞서 루프를 예냉합니다. 운영자는 이러한 시스템을 워크로드 스케줄러와 통합하여 연산 처리와 냉각이 통합된 효율화 엔진으로 활용할 수 있습니다. 하이브리드 드라이쿨러는 취수량을 60-70% 절감하여 취수 제한 지역에서의 규제 준수를 지원합니다. 하이퍼스케일러가 공급의 연속성을 보장하기 위해 다년 계약을 체결함에 따라, 업스트림 벤더들은 파급효과로 인한 매출 증가를 누리고 있습니다. 북미의 데이터센터 냉각 시장에서 기존 공랭식 냉각 부품의 점유율은 줄어들 것으로 예상되지만, 리노베이션 수요로 인해 교체용 필터, 벨트, 이코노마이저 키트에 대한 수요는 장기적으로 지속될 것으로 보입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 북미 현재 데이터센터 설치 상황에 관한 분석

제6장 시장 규모와 성장 예측

제7장 경쟁 구도

제8장 시장 기회와 향후 전망

KTHThe North America data center cooling market size is projected to be USD 7.21 billion in 2025, USD 7.99 billion in 2026, and reach USD 13.58 billion by 2031, growing at a CAGR of 11.17% from 2026 to 2031.

Rising rack densities above 40 kilowatts are pressuring operators to swap legacy air systems for liquid architectures that draw heat directly from processors, a shift reinforced by federal mandates that link lease renewals to power-usage-effectiveness benchmarks. Inflation Reduction Act tax credits covering up to 30% of eligible equipment costs accelerate the retirement of high-GWP chillers, while state water-use caps in desert markets push demand for closed-loop dry coolers. Competitive intensity remains elevated as HVAC majors retrofit chiller portfolios and liquid-cooling specialists secure design wins by guaranteeing sub-25 °C chip temperatures. Developers are also navigating power-grid constraints in Northern Virginia and drought-related insurance surcharges that influence site selection and total cost of ownership.

North America Data Center Cooling Market Trends and Insights

Stringent PUE Targets Under U.S. Executive Order on Federal Sustainability

Federal agencies must now prove PUE ratios below 1.4 for new builds and below 1.5 for existing sites by fiscal 2027, effectively disqualifying legacy raised-floor designs that rely on perimeter air handlers. Updated leasing rules require landlords to share sub-metered cooling energy data, giving tenants the right to terminate contracts if efficiency covenants are missed. Contractors are pivoting to modular chiller plants with variable-speed compressors that trim PUE by up to 0.20 points. Defense workloads that once favored air-gapped security are adopting rear-door heat exchangers to cut the load seen by central plants. Commercial tenants are mirroring federal expectations, forcing multi-tenant providers to guarantee similar efficiency thresholds.

Escalating Rack Densities in Hyperscale Facilities

Training clusters for frontier AI models routinely exceed 40 kW per rack, with some GPU configurations nearing 80 kW as high-bandwidth memory and multi-die packages condense heat output. Air systems struggle to keep inlet temperatures under 27 °C at these loads without energy-intensive fan over-provisioning. Hyperscalers are moving to direct-to-chip cold plates that intercept 70%-90% of processor heat before it enters room air, easing demand on air handlers. This density also reshapes site selection, pushing operators toward regions with affordable electricity and climates that permit more free-cooling hours. Legacy air infrastructure is being repurposed for lower-density storage rows, maximizing sunk investments while liquid systems protect the compute core.

Power-Grid Constraints Delaying New Builds in Northern Virginia

Dominion Energy's transmission queue listed more than 7 GW of interconnection requests in January 2026, with average waits of 36 months for projects needing new substations. Underinvestment in 500 kV lines and local opposition to new corridors stall capacity expansions and force developers to explore backup generation or relocate to Ohio and North Carolina. Interim solutions such as hydrogen fuel cells add significant capital expense and trigger additional air-permit reviews. Some operators downsize footprints to fit within existing feeder headroom, fragmenting once-megasite-oriented investment plans. The congestion risk also elevates financing costs, as lenders price delays into required returns.

Other drivers and restraints analyzed in the detailed report include:

- Growing Adoption of Liquid Cooling for AI and ML Workloads

- Inflation Reduction Act Tax Credits for Low-GWP Chillers

- Volatility in Refrigerant Prices Amid HFC Phase-Down

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Liquid-based approaches will grow at a 12.54% CAGR through 2031, far ahead of air methods that still dominated with 59.64% share in 2025. The North America data center cooling market size for liquid solutions is expanding as hyperscalers retrofit compute rows that now host GPUs drawing 40-80 kW per rack. Immersion baths in edge nodes solve space and acoustic limits, while direct-to-chip plates dominate large training clusters. Rear-door heat exchangers act as a bridge, extending the life of air-cooled halls and reducing capex burdens. HVAC vendors disclose multi-hundred-percent order growth for liquid skids, signaling a secular pivot rather than a niche experiment. Regulatory pushes for low-GWP refrigerants further encourage operators to bypass chillers altogether, relying on warm-water loops that reject heat through dry coolers.

The hybridization trend means both technologies will coexist. Operators segment halls by workload, dedicating liquid zones to AI while leaving storage and network gear on air cooling. This flexible approach protects prior investments and allows gradual skill-set development among facilities staff. Suppliers now bundle control software that orchestrates both regimes, shifting workloads to racks with the most favorable thermal headroom. As liquid penetration rises, aftermarket demand emerges for sensors, fittings, and quick-disconnect couplings, opening ancillary revenue pools. The North America data center cooling market continues to witness pilots that evaluate two-phase refrigerant loops, though commercial readiness may postdate the current forecast period.

Computer room air handlers held 40.72% share in 2025, reflecting the historical base of raised-floor halls across the region. Yet pumps and valves are projected to rise at a 12.66% CAGR, mirroring the liquid-technology surge. Modern loops require precision flow control; even slight imbalances can spike chip temperatures and throttle performance. Manufacturers respond with variable-speed pumps featuring embedded flow sensors and smart valves that auto-balance circuits in real time. Chillers remain the single largest line-item in capital projects, but their role shifts toward modularity, arriving on site in 500 kW blocks that match staged IT deployments.

Control software differentiates offerings as AI-driven platforms learn load patterns and pre-cool loops before inference bursts. Operators integrate these systems with workload schedulers so compute and cooling act as a unified efficiency engine. Hybrid dry-coolers cut water draw by 60-70%, aiding compliance in jurisdictions with withdrawal caps. Upstream component vendors enjoy pull-through sales as hyperscalers lock in multi-year contracts to guarantee supply continuity. The North America data center cooling market share for traditional air components will erode, but retrofit demand ensures an extended tail for replacement filters, belts, and economizer kits.

The North America Data Center Cooling Market Report is Segmented by Cooling Technology (Air-Based, and Liquid-Based), Cooling Component (CRAH/CRAC, Chillers and Heat Exchangers, Cooling Towers and Dry Coolers, and More), Tier Type (Tier 1 and 2, and Tier 4), Data Center Size (Small, Medium, Large, and Hyperscale), Data Center Type (Colocation, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Vertiv Group Corp.

- Stulz GmbH

- Schneider Electric SE

- Rittal GmbH and Co. KG

- Asetek A/S

- Alfa Laval AB

- Iceotope Technologies Ltd.

- Green Revolution Cooling Inc.

- Chilldyne Inc.

- Airedale International Air-Conditioning Ltd.

- Nortek Air Solutions LLC

- Mitsubishi Electric Corporation

- Johnson Controls International plc

- Munters Group AB

- Delta Electronics Inc.

- Hewlett Packard Enterprise Company

- IBM Corporation

- Cisco Systems Inc.

- LiquidStack Inc.

- Submer Technologies, S.L.

- CoolIT Systems Inc.

- Trane Technologies plc

- Super Micro Computer Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent PUE Targets Under U.S. Executive Order on Federal Sustainability

- 4.2.2 Escalating Rack Densities in Hyperscale Facilities

- 4.2.3 Growing Adoption of Liquid Cooling for AI/ML Workloads

- 4.2.4 Heat-To-District Energy Purchase Agreements in Canadian Provinces

- 4.2.5 Inflation Reduction Act Tax Credits for Low-GWP Refrigerant Chillers

- 4.2.6 State-Level Water Withdrawal Caps Accelerating Closed-Loop Retrofits

- 4.3 Market Restraints

- 4.3.1 Volatility in Refrigerant Prices Amid HFC Phase-Down

- 4.3.2 Power-Grid Constraints Delaying New Builds in Northern Virginia

- 4.3.3 Limited Skills for Immersion-Cooling Maintenance

- 4.3.4 Insurance-Premium Surcharges for Water-Based Systems in Drought Zones

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 ANALYSIS OF THE CURRENT DATA CENTER FOOTPRINT IN NORTH AMERICA

- 5.1 Analysis of IT Load Capacity (MW) and Area footprint (Sq. Ft.) of Data Centers (for the Period of 2019-2031)

- 5.2 Analysis of Major Data Center Hotspots in North America

- 5.3 Analysis of Major Upcoming Hyperscale Facilities in North America

6 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 6.1 By Cooling Technology

- 6.1.1 Air-Based Cooling

- 6.1.1.1 CRAH

- 6.1.1.2 Chiller and Economizer

- 6.1.1.3 Cooling Tower (Direct, Indirect, Two-Stage)

- 6.1.1.4 Others

- 6.1.2 Liquid-Based Cooling

- 6.1.2.1 Immersion Cooling

- 6.1.2.2 Direct-to-Chip Cooling

- 6.1.2.3 Rear-Door Heat Exchanger

- 6.1.1 Air-Based Cooling

- 6.2 By Cooling Component

- 6.2.1 Computer-Room Air Handlers (CRAH/CRAC)

- 6.2.2 Chillers and Heat-Exchanger Units

- 6.2.3 Cooling Towers and Dry Coolers

- 6.2.4 Pumps and Valves

- 6.2.5 Control and Monitoring Software

- 6.3 By Tier Type

- 6.3.1 Tier 1 and 2

- 6.3.2 Tier 3

- 6.3.3 Tier 4

- 6.4 By Data Center Size

- 6.4.1 Small Data Center

- 6.4.2 Medium Data Center

- 6.4.3 Large Data Center

- 6.4.4 Hyperscale Data Center

- 6.5 By Data Center Type

- 6.5.1 Colocation Data Center

- 6.5.2 Hyperscalers Data Center/CSPs

- 6.5.3 Enterprise and Edge Data Center

- 6.6 By Country

- 6.6.1 United States

- 6.6.2 Canada

- 6.6.3 Mexico

7 COMPETITIVE LANDSCAPE

- 7.1 Market Share Analysis

- 7.2 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 7.2.1 Vertiv Group Corp.

- 7.2.2 Stulz GmbH

- 7.2.3 Schneider Electric SE

- 7.2.4 Rittal GmbH and Co. KG

- 7.2.5 Asetek A/S

- 7.2.6 Alfa Laval AB

- 7.2.7 Iceotope Technologies Ltd.

- 7.2.8 Green Revolution Cooling Inc.

- 7.2.9 Chilldyne Inc.

- 7.2.10 Airedale International Air-Conditioning Ltd.

- 7.2.11 Nortek Air Solutions LLC

- 7.2.12 Mitsubishi Electric Corporation

- 7.2.13 Johnson Controls International plc

- 7.2.14 Munters Group AB

- 7.2.15 Delta Electronics Inc.

- 7.2.16 Hewlett Packard Enterprise Company

- 7.2.17 IBM Corporation

- 7.2.18 Cisco Systems Inc.

- 7.2.19 LiquidStack Inc.

- 7.2.20 Submer Technologies, S.L.

- 7.2.21 CoolIT Systems Inc.

- 7.2.22 Trane Technologies plc

- 7.2.23 Super Micro Computer Inc.

8 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 8.1 White-Space and Unmet-Need Assessment