|

시장보고서

상품코드

2061509

바이오시밀러 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Biosimilars - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

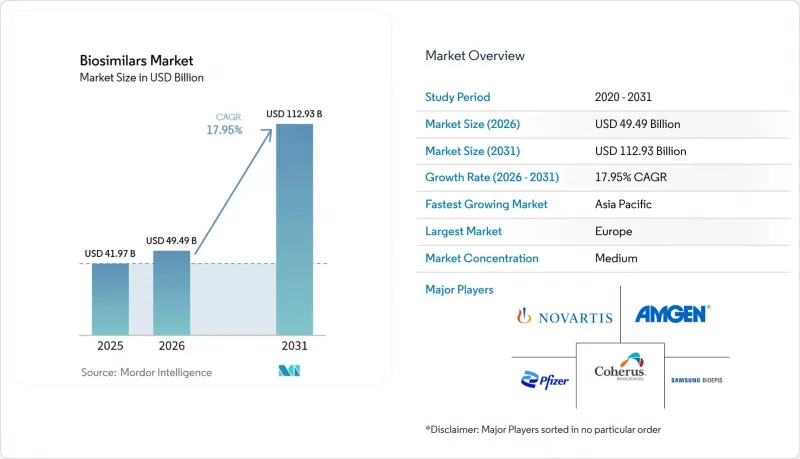

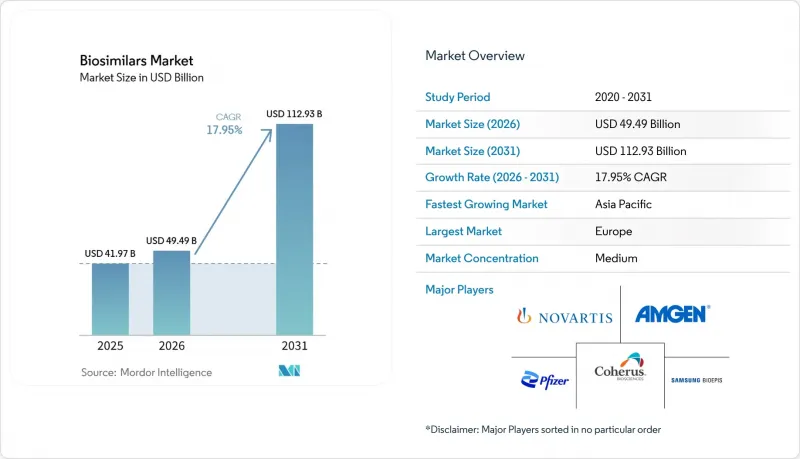

Mordor Intelligence에 의하면, 바이오시밀러 시장 규모는 2025년 419억 7,000만 달러로 평가되었습니다. 2026년 494억 9,000만 달러로 확대되어 2031년까지 1,129억 3,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR은 17.95%를 나타낼 전망입니다.

본 보고서에서는 업계를 제품 분류(단일클론 항체, 재조합 호르몬 등), 적응증(혈액 질환, 자가면역 질환·만성 염증성 질환 등), 최종 사용자(병원 등), 제조 형태(자체 제조 등), 투여 경로(정맥 내, 피하), 지역(북미, 유럽, 아시아태평양, 중동, 남미)별로 분류하고 있습니다.

세계의 바이오시밀러 시장 동향과 인사이트

여러 블록버스터 생물학적 제제의 특허 만료가 임박하고 있습니다.

시장 규모 확대는 2029년부터 2034년 사이에 약 4,000억 달러 규모의 참조 제품 매출을 창출할 것으로 예상되며, 이는 전례 없는 특허 만료의 물결에 힘입은 것입니다. 2025년 한 해에만 25개의 고부가가치 바이오의약품이 독점권을 상실했으므로, 각 개발사들은 개발권과 제조권을 동시에 확보하기 위해 서두르고 있습니다. 여기서 도출되는 결론은 개발 파이프라인이 현재 매우 혼잡하기 때문에 자금이 아니라 분석 시험 능력이 일부 프로그램의 병목 요인으로 대두되고 있다는 점입니다. 샌즈(Sands) 등의 기업들은 이미 28종의 분자로 구성된 파이프라인을 공개했으며, 이는 이 기회의 규모를 보여줍니다. 암 치료에 특화된 단일클론 항체가 가장 큰 영향을 받을 것으로 보이며, 이는 예측 기간 내 블록버스터급 항암제의 평균 판매 가격이 하락할 것임을 의미합니다. 이러한 변화는 치료비 절감과 접근성 향상을 가져오는 한편, 그동안 2-3개 업체밖에 없던 치료 분야에서 경쟁이 심화되는 결과를 초래할 것입니다.

만성 질환 및 자가면역 질환의 유병률 급증

만성 질환 및 자가면역 질환은 전 세계적으로 급증하고 있으며, 미국 내 처방약 지출의 절반 이상을 이미 전문의약품이 차지하고 있습니다. 그 결과, 이러한 질환을 대상으로 하는 바이오시밀러는 가장 빠르게 성장하고 있는 적응증군으로, 2025년부터 2030년에 걸쳐 연평균 성장률(CAGR) 23%를 나타낼 것으로 전망됩니다. 발병률 상승 데이터를 통해 추측할 수 있는 것은 설령 바이오시밀러가 두 자릿수 시장 점유율 확대를 달성한다 하더라도, 환자 수가 동시에 증가하고 있기 때문에 지불 주체의 예산은 점점 더逼迫하게 될 것이라는 점입니다. 현재 종양학 분야가 최대의 수익원이지만, 진단율이 상승함에 따라 자가면역질환 처방전이 그 격차를 좁혀가고 있습니다. 브라질에서 진행된 프로그램을 통해 수집된 실제 데이터에 따르면, 병세가 안정된 환자로 전환함으로써 50%가 넘는 비용 절감 효과가 확인되었으며, 다른 신흥 시장에서도 유사한 성과를 거둘 가능성이 시사되고 있습니다. 환자들이 장기 유지 요법으로 꾸준히 전환함에 따라, 만성 질환용 바이오시밀러의 상업적 매력이 높아지고 있으며, 피하 투여 제제에 대한 투자가 촉진되고 있습니다.

제조 및 분석의 본질적인 복잡성

바이오시밀러 개발에는 여전히 1억-3억 달러의 비용이 소요되며, 7-8년이라는 기간이 걸립니다. 이는 각 분자가 40개 이상의 상호 독립적인 분석 시험을 거쳐야 하기 때문입니다. 이러한 수치를 통해 추측할 수 있는 것은 자금 제약으로 인해 중소 개발 기업들은 폭넓은 포트폴리오보다는 좁지만 고부가가치가 높은 틈새 시장으로 진출하게 될 것이라는 점입니다. 포유류 세포 배양, 특히 중국 햄스터 난소(CHO) 세포주는 인간과 유사한 당사슬 프로파일을 가지고 있어 여전히 생산의 주축을 이루고 있습니다. 개발 기업이 항체-약물 복합체(ADC)나 융합 단백질을 표적으로 삼을 경우, 복잡성은 더욱 커집니다. 이들 모두 파이프라인 공개 과정에서 등장하기 시작했습니다. 당사슬 프로파일링이나 전하 변이체 분석과 같은 분석 과제를 수행하려면 고가의 장비가 필요하기 때문에 많은 기업이 전문 CDMO에 외주를 맡길 수밖에 없는 실정입니다. 후기 단계의 바이오시밀러 프로그램에서 약 50% 전후로 나타나는 높은 실패율은 성공 확률을 좌우하는 요소가 자본력뿐만 아니라 전문 지식이기도 함을 시사합니다.

부문별 분석

단일클론 항체(mAb) 바이오시밀러 시장 규모는 2025년에 총 매출의 47.35%를 차지했습니다. 그 연평균 성장률(CAGR)은 10%대 중반으로 둔화되지만, 절대적인 매출액은 계속해서 증가하고 있습니다. 이러한 점에서 볼 때, 현재 수십 가지에 달하는 mAb 표적들이 제약사들의 관심을 분산시키고 있기 때문에 시장 점유율 1위라는 사실이 근본적인 세분화를 가리고 있다는 추측이 성립됩니다. 저분자량 헤파린 시장은 연평균 성장률(CAGR) 20.25%를 기록하며 성장하고 있으며, 이는 항응고제 분야가 향후 치열한 경쟁이 예상되는 시장이 될 가능성을 시사하고 있습니다. 2024년에 5종의 우스테키누맙 바이오시밀러가 FDA 승인을 받은 것은 출시 시기가 집중됨에 따라 가격대가 압박을 받게 되어 후속 출시 제품마다 제품 수명 주기가 단축될 가능성이 있음을 여실히 보여주고 있습니다. 각 개발사는 렙티시맙이나 베바시주맙 등의 단일클론항체(mAb)를 우선적으로 개발하고 있습니다. 이는 임상 평가 지표가 확립되어 있어, 비교 시험의 범위가 좁아지기 때문입니다. 그러나 새롭게 등장한 이중 특이성 항체가 향후 동등성 평가를 복잡하게 만들 가능성이 있어, 규제 당국은 지침을 더욱 세밀하게 다듬어야할 것입니다.

2025년에는 종양학 분야가 바이오시밀러 시장 점유율의 54.30%를 차지하며, 보험 급여 예산에서 가장 큰 비중을 차지했습니다. 이로부터 즉시 도출되는 결론은 종양학 분야의 지불 주체가 전환을 강제할 수 있는 가장 큰 영향력을 가지고 있으며, 그로 인해 시장 침투가 가속화된다는 점입니다. 자가면역 질환 및 염증성 질환은 22.10%의 예측 연평균 성장률(CAGR)을 보이고 있으며, 이는 2031년까지 이 두 적응증 간의 매출 격차가 크게 좁혀질 가능성이 있음을 시사합니다. 야보이와 같은 체크포인트 억제제를 표적으로 하는 향후 바이오시밀러의 출시는 2차적인 효과를 시사하고 있습니다. 즉, 고가의 면역종양학 치료제가 바이오시밀러로 인해 시장 점유율을 빼앗길 경우, 그로 인해 절감된 비용이 정밀 의학의 보다 광범위한 활용에 쓰일 가능성이 있다는 것입니다. 그 결과, 이러한 움직임이 혁신가들을 더욱 복잡한 생물학적 제제의 개발로 이끌고, 혁신의 순환을 다시 활성화시킬지도 모릅니다.

지역별 분석

유럽은 2006년의 선구적인 규제 체계와 조율된 조달 정책을 반영하여, 36.65%의 바이오시밀러 시장 점유율로 계속해서 주도적인 위치를 차지하고 있습니다. 많은 EU 회원국에서는 절감된 비용을 병원 예산에 환원하는 이익 공유 제도를 도입하고 있으며, 이를 통해 처방 의사의 참여가 촉진되고 있습니다. 이러한 점에서 볼 때, 유럽의 성숙한 인프라는 현재 공급업체의 다양성을 유지하는 다중 업체 선정 방식 등 선진적인 계약 모델의 시험장으로 기능하고 있는 것으로 추정됩니다. 인플릭시맙에 대한 사례 연구에 따르면, 바이오시밀러의 등장으로 인해 원개발품의 가격이 급락하고 있으며, 전문 치료제 분야에서도 경쟁이 효과적으로 작용하고 있음이 입증되었습니다. 해당 지역에서는 독점권 상실 사례가 3회 연속으로 발생할 것으로 예상되며, 이는 바이오시밀러 시장 침투를 가속화하는 한편, 중소 제약사들에게는 감당하기 어려운 수준의 가격 하락을 초래할 우려도 있습니다.

아시아태평양은 한국의 대기업인 삼성바이오에피스 및 셀트리온, 그리고 중국의 규제 개혁에 힘입어 연평균 성장률(CAGR) 23.10%를 나타낼 것으로 예측되는 가장 빠르게 성장하는 지역입니다. 생산 능력 수치를 통해 추측할 수 있는 것은 아시아가 수탁 제조 거점에서 설계·개발 거점으로 진화하고 있다는 점이며, 이는 임상시험 인프라의 현지화를 통해 뒷받침되고 있습니다. 인도는 제네릭 의약품의 전통을 바탕으로 바이오시밀러 승인 절차를 신속하게 진행하고 있습니다. 한편, 호주와 일본은 공급망의 회복탄력성을 높이기 위해 국내 바이오의약품 생산에 투자하고 있습니다. 팬데믹으로 인해 바이오의약품 자급자족을 위한 정부의 인센티브가 가속화됨에 따라, 전 세계 승인 건수에서 아시아가 차지하는 비중은 전 세계 수요 증가만 고려했을 때 예상되는 것보다 더 빠른 속도로 상승할 것으로 보입니다.

미국이 주도하는 북미는 보급률 면에서는 유럽에 뒤처져 있지만, 2024년 7월 기준 FDA 승인 56건, 출시 41건이라는 실적을 바탕으로 절대적인 수익 잠재력 면에서는 최대 규모를 자랑하고 있습니다. 주목할 점은 ‘인플레이션 억제법(IRA)’에 포함된 메디케어 지급 제도 개혁을 통해, 공적 의료 프로그램에서 바이오시밀러로의 신속한 전환을 유도하는 인센티브가 재구축될 가능성이 있다는 것입니다. 5년 동안 1,810억 달러의 비용 절감이 예상된다는 예측은 그 경제적 중요성을 여실히 보여주고 있습니다. 캐나다 각 주의 처방약 목록에서도 의학적 근거가 없는 약품 변경이 의무화되어 있으며, 이러한 정책적 선택은 북미 대륙 전체에 걸쳐 통일적으로 도입될 가능성이 있습니다. 이러한 요인들을 종합해 보면, 현재의 성장 격차가 지속될 경우 2030년대 초반까지 북미가 시장 규모 면에서 유럽을 추월할 것으로 예측됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the biosimilars market size is expected to increase from USD 41.97 billion in 2025 to USD 49.49 billion in 2026 and reach USD 112.93 billion by 2031, growing at a CAGR of 17.95% over 2026-2031.

This report Segments the Industry Into by Product Class (Monoclonal Antibodies, Recombinant Hormones, and More), Indication (Blood Disorders, Autoimmune & Chronic Inflammatory, and More), End User (Hospitals, and More), Manufacturing Type (In-House, and More), Route of Administration (Intravenous, and Sub-Cutaneous), and Geography (North America, Europe, Asia-Pacific, Middle East, and South America).

Global Biosimilars Market Trends and Insights

Imminent Patent Expiry of Multiple Blockbuster Biologics

Market size expansion is being propelled by an unprecedented wave of patent expirations that will unlock an estimated USD 400 billion in reference product sales between 2029 and 2034. Because 25 high-value biologics lose exclusivity in 2025 alone, developers are rushing to secure development slots and manufacturing slots simultaneously. The inference drawn here is that development pipelines are now so crowded that analytical testing capacity, not funding, is emerging as the gating factor for some programs. Companies such as Sandoz have already disclosed pipelines of 28 molecules, demonstrating the scale of the opportunity . Oncology-focused monoclonal antibodies are most exposed, implying lower average selling prices for blockbuster cancer drugs within the forecast period. This disruption will lower treatment costs and widen access, but it also raises competitive intensity in therapeutic areas that previously featured only two or three suppliers.

Escalating Prevalence of Chronic and Autoimmune Diseases

Chronic and autoimmune diseases are surging worldwide, and specialty medicines already account for over half of U.S. prescription expenditure. Consequently, biosimilars targeting these conditions represent the fastest-growing indication cohort, clocking a 23% CAGR from 2025-2030. The inference from rising prevalence data is that payer budgets will come under mounting strain even if biosimilars achieve double-digit market share gains, because absolute patient numbers are rising in parallel. Oncology remains the largest revenue pool today, but autoimmune prescriptions are narrowing that gap as diagnosis rates climb. Real-world evidence from programs in Brazil shows cost savings exceeding 50% when stable patients are switched, suggesting that similar outcomes could surface in other emerging markets. Steady patient migration toward long-term maintenance therapies heightens the commercial attractiveness of chronic-disease biosimilars and incentivizes investment in subcutaneous formulations.

Intrinsic Manufacturing and Analytical Complexity

Developing a biosimilar still costs USD 100-300 million and takes as long as seven to eight years because each molecule must undergo more than 40 orthogonal analytical tests. An inference from these numbers is that capital rationing will steer smaller developers toward narrow, high-value niches rather than broad portfolios. Mammalian cell culture, particularly Chinese Hamster Ovary (CHO) lines, remains the production workhorse because of its human-like glycosylation profile. Complexity rises further when developers target antibody-drug conjugates or fusion proteins, both of which are beginning to surface in pipeline disclosures. Analytical challenges, including glycan profiling and charge variant analysis, require expensive instrumentation, pushing many firms to outsource to specialized CDMOs. High failure rates-hovering around 50 % for late-stage biosimilar programs-signal that expertise, rather than capital alone, determines success probabilities.

Other drivers and restraints analyzed in the detailed report include:

- Growing Clinician and Patient Confidence Driven by Real-World Evidence

- Rising Capital Investment, Strategic Alliances, and CMO/CDMO Capacity Expansions

- Ongoing Interchangeability and Substitution Skepticism in Certain Healthcare Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The biosimilar market size for monoclonal antibodies stands at 47.35 % of total revenue in 2025, and while their aggregate CAGR moderates to the mid-teens, absolute sales continue to rise. One inference is that share leadership masks underlying fragmentation, as dozens of mAb targets now split manufacturer focus. Low-molecular-weight heparins are growing at 20.25% CAGR, signaling that anticoagulation may become the next competitive battleground. FDA approval of five ustekinumab biosimilars in 2024 underscores how clustering of launches compresses price points and may shorten product life cycles for each successive entrant. Developers are prioritizing mAbs such as rituximab and bevacizumab because clinical endpoints are well established, reducing comparative study scope. Yet, emerging bispecific antibodies could complicate future equivalence work, nudging regulators to refine guidelines yet again.

The oncology segment accounts for 54.30% biosimilar market share in 2025, commanding the largest slice of reimbursement budgets. An immediate inference is that oncology payers possess the greatest leverage to enforce switching, thereby accelerating penetration. Autoimmune and inflammatory diseases post a 22.10% forecast CAGR, which implies that by 2031 the revenue gap between the two indications could narrow considerably. Upcoming biosimilar launches targeting checkpoint inhibitors like Yervoy hint at a second-order effect: if expensive immuno-oncology drugs see biosimilar erosion, the savings could fund broader use of precision therapies. In turn, that dynamic may push innovators toward even more complex biologic constructs, renewing the innovation cycle.

Geography Analysis

Europe continues to lead with 36.65 % biosimilar market share, reflecting its pioneering 2006 regulatory path and coordinated procurement policies. Many EU member states have instituted gain-sharing schemes, channeling savings back to hospital budgets, which encourages prescriber engagement. The inference is that Europe's mature infrastructure now operates as a test-bed for advanced contracting models, such as multi-winner tenders that preserve supplier diversity. Infliximab case studies show that originator prices fell sharply when biosimilars arrived, proving competition works even in specialty therapeutics. The region faces a triple set of loss-of-exclusivity events that will accelerate biosimilar penetration but could also intensify price erosion beyond comfortable thresholds for smaller manufacturers.

Asia-Pacific is the fastest-growing territory at a projected 23.10 % CAGR, catalyzed by South Korean giants Samsung Bioepis and Celltrion and by China's regulatory reforms. An inference from capacity figures is that Asia is evolving from a contract-manufacturing hub into a design-and-development powerhouse, as evidenced by the localization of clinical trial infrastructure. India leverages its generics heritage to fast-track biosimilar filings, while Australia and Japan are investing in domestic bioproduction for supply-chain resilience. The pandemic accelerated government incentives for biologics self-sufficiency, suggesting that Asia's share of global approvals will rise faster than global demand growth alone would indicate.

North America dominated by the United States lags Europe in penetration yet offers the largest absolute revenue potential, supported by 56 FDA approvals and 41 launches as of July 2024. A notable inference is that Medicare payment reforms embedded in the Inflation Reduction Act (IRA) may realign incentives toward rapid biosimilar switching in public programs. Projected U.S. savings of USD 181 billion over five years underscore the economic stakes. Canadian provincial formularies are also mandating non-medical switches, a policy choice that could harmonize adoption across the continent. Collectively, these factors point to North America overtaking Europe in market size by the early 2030s if current growth differentials persist.

- Pfizer

- Sandoz Group

- Amgen

- Viatris

- Samsung Group

- Celltrion Healthcare

- Eli Lilly and Company

- Biocon Ltd

- Teva Pharmaceutical Industries

- Stada Arzneimittel

- Dr Reddy's Laboratories

- Coherus Biosciences

- LG Chem (LG Life Sciences)

- Intas Pharmaceutical

- Fresenius

- Alvotech

- Bio-Thera Solutions

- Shanghai Henlius Biotech

- Lupin

- Hikma Pharmaceuticals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Imminent Patent Expiry Of Multiple Blockbuster Biologics

- 4.2.2 Escalating Prevalence Of Chronic And Autoimmune Diseases

- 4.2.3 Global Cost-Containment Mandates And Tender-Based Procurement Models

- 4.2.4 Growing Clinician And Patient Confidence Driven By Real-World Evidence

- 4.2.5 Rising Capital Investment, Strategic Alliances, And Cmo/Cdmo Capacity Expansions

- 4.2.6 Increasing Demand Due To Cost-Effectiveness

- 4.3 Market Restraints

- 4.3.1 Intrinsic Manufacturing And Analytical Complexity

- 4.3.2 Ongoing Interchangeability And Substitution Skepticism In Certain Healthcare Systems

- 4.3.3 Originator Defensive Tactics-Patent Litigation, Rebate Walls, And Brand-Loyalty Programs

- 4.3.4 Severe Price Erosion And Narrow Margins

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Class

- 5.1.1 Monoclonal Antibodies

- 5.1.2 Recombinant Hormones (EPO, G-CSF)

- 5.1.3 Insulins

- 5.1.4 Low-Molecular-Weight Heparins

- 5.1.5 Fusion Proteins & Others

- 5.2 By Indication

- 5.2.1 Oncology

- 5.2.2 Autoimmune & Chronic Inflammatory

- 5.2.3 Metabolic Disorders

- 5.2.4 Blood & Coagulation Disorders

- 5.2.5 Others

- 5.3 By End-user

- 5.3.1 Hospitals

- 5.3.2 Specialty Clinics

- 5.3.3 Retail & Mail-Order Pharmacies

- 5.4 By Manufacturing Type

- 5.4.1 In-house

- 5.4.2 Contract/Outsourced (CMO/CDMO)

- 5.5 By Route of Administration

- 5.5.1 Intravenous

- 5.5.2 Sub-cutaneous

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Pfizer Inc.

- 6.4.2 Sandoz

- 6.4.3 Amgen Inc.

- 6.4.4 Viatris Inc.

- 6.4.5 Samsung Bioepis Co. Ltd

- 6.4.6 Celltrion Healthcare

- 6.4.7 Eli Lilly and Company

- 6.4.8 Biocon Ltd

- 6.4.9 Teva Pharmaceutical Industries Ltd

- 6.4.10 Stada Arzneimittel AG

- 6.4.11 Dr Reddy's Laboratories

- 6.4.12 Coherus Biosciences Inc.

- 6.4.13 LG Chem (LG Life Sciences)

- 6.4.14 Intas Pharmaceuticals Ltd

- 6.4.15 Fresenius Kabi

- 6.4.16 Alvotech

- 6.4.17 Bio-Thera Solutions

- 6.4.18 Shanghai Henlius Biotech

- 6.4.19 Lupin Ltd

- 6.4.20 Hikma Pharmaceuticals PLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment