|

시장보고서

상품코드

2061578

POC(Point Of Care) 진단 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Point Of Care Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

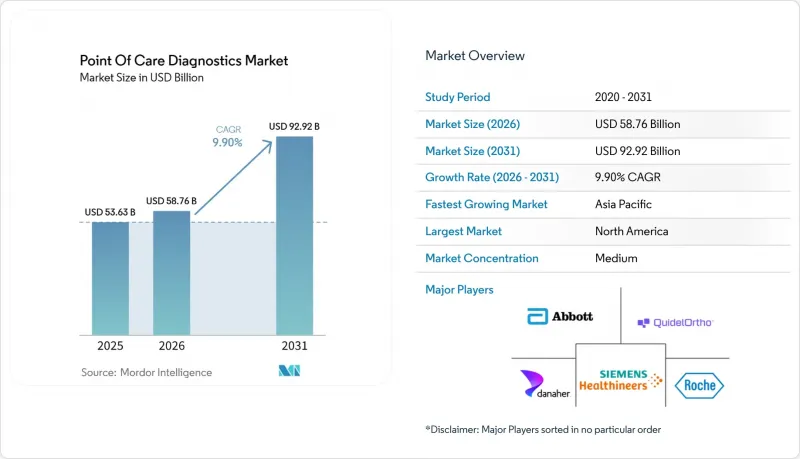

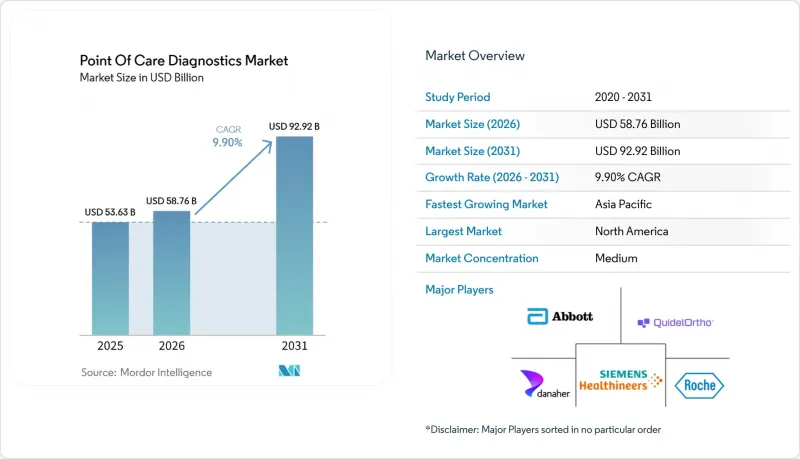

Mordor Intelligence에 의하면, POC(Point of Care) 진단 시장 규모는 2025년 536억 3,000만 달러로 평가되었습니다. 2026년 587억 6,000만 달러에서 2031년까지 929억 2,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 9.90%를 나타낼 것으로 예측됩니다.

본 보고서는 제품(혈당 모니터링 키트, 감염증 검사 키트 등), 플랫폼(측류 분석법, 마이크로플루이딕스 기반 플랫폼 등), 검체 유형(혈액, 소변 등), 구매 형태(일반의약품(OTC) 및 처방약), 최종 사용자(병원 및 진료소 등), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 POC(Point Of Care) 진단 시장 동향 및 인사이트

만성 질환 및 감염증 유병률 증가

2024년 전 세계적으로 5억 3,700만 명의 성인이 당뇨병을 앓았으며, 국제당뇨병연맹(IDF)은 2030년까지 이 수치가 6억 4,300만 명에 달할 것으로 전망하고 있습니다. 이는 혈당 측정 키트에 대한 지속적인 수요를 뒷받침하는 것입니다. 동남아시아의 뎅기열과 중앙아프리카의 MPOX(원숭이두창) 등 여러 지역에서 동시에 유행하는 상황을 감안하여, 각국 정부는 신속 진단 키트 비축을 추진하고 있습니다. 세계보건기구(WHO)는 2025년에 12종의 새로운 말라리아 신속 검사 키트를 사전 승인하여, 조달 기관들이 저기생충혈증 검출에 관한 엄격한 민감도 기준을 충족하는 검사 키트를 확보할 수 있도록 했습니다. 애보트사는 같은 해 인도 국가보건미션에 1,500만 개의 말라리아 검사 키트를 공급하여, 1차 의료 센터의 40%에서 여전히 현미경 검사를 이용할 수 없는 지역을 지원했습니다. 세페이드(Sefied)사의 ‘GeneXpert MTB/RIF Ultra’ 검사 키트는 남아프리카공화국의 진료소에서 결핵 치료 시작까지 걸리는 시간을 14일에서 2시간 미만으로 단축함으로써, 신속한 분자 검사의 임상적 우위를 입증했습니다. 만성 질환 관리와 감염병 유행에 대한 대응이라는 이 두 가지 과제는 소득 수준에 관계없이 POC(Point Of Care) 진단 시장을 견인하는 구조적인 호재가 되고 있습니다.

기술의 발전과 가정용 POC의 보급

메디케어는 2025년 의사 보수 일정에 CPT 99454를 도입하여, 월 16일 이상 생리학적 데이터를 전송하는 기기에 대해 환자 1인당 월 64달러를 지급하기로 했습니다. 로슈사의 CoaguChek 시스템은 이 규정에 따라 가상 INR 상담 대상이 되었습니다. 한편, 애보트사의 블루투스 지원 FreeStyle Libre 3 Plus는 1분마다 혈당 수치를 실시간으로 전송하여 원격으로 인슐린 조절이 가능하게 합니다. 2024년 6월에 승인된 데컴(Decom)사의 시판용 스텔로(Stelo) 센서는 그동안 보험 적용 대상이 아니었던 미국의 2형 당뇨병 환자 3,000만 명에게 연속 혈당 모니터링 서비스를 이용할 수 있는 기회를 제공했습니다. 많은 신흥 시장에서 스마트폰 보급률이 70%를 넘어서면서, 클라우드 연동형 진단 기기의 도입 장벽이 더욱 낮아지고 있습니다. 센서의 소형화와 보험 급여 제도의 개혁이 맞물리면서, 병원 중심의 검사 모델은 POC(Point of Care) 진단 시장을 확대하는 분산형 환자 주도 워크플로로 전환되고 있습니다.

엄격한 규제와 상환 격차

2024년에 발표된 FDA 지침에 따라, POC 분자 검사의 분석적 타당성 기준이 상향 조정되어, 3개의 서로 다른 임상 기관에서 양성 일치율 95% 이상, 음성 일치율 98% 이상을 충족해야 하게 되었습니다. 그 후, CMS는 2025년 요금표에서 CLIA 면제 코드 중 일부를 8-12% 삭감하여 소규모 진료소의 경영에 부담을 주고 있습니다. 앤섬(Anthem) 등 민간 보험사들은 고위험 환자에게만 호흡기 병원체 패널 검사를 허용하는 사전 승인 규정을 도입했습니다. 유럽에서는 2025년 5월 체외진단용 의료기기 규정(IVDR)의 시행 기한으로 인해, 제조업체들이 인증 기관의 감사를 확보하지 못하면서 기존 POC 기기의 약 30%가 시장에서 철수할 수밖에 없었습니다. 이러한 정책 전환은 규정 준수 비용을 증가시켜 단기적인 도입을 억제하고, POC(Point Of Care) 진단 시장의 성장을 둔화시키고 있습니다.

부문별 분석

혈당 모니터링 키트는 모세혈관 혈당 측정기의 보급과 CGM 센서의 급속한 확산에 힘입어, 2025년 POC(Point Of Care) 진단 시장 점유율 37.94%를 유지했습니다. 한편, 감염병 검사 키트는 전 세계 보건 당국이 말라리아, 결핵, 성병에 대한 새로운 신속 검사법을 사전 승인함에 따라 2031년까지 연평균 성장률(CAGR) 10.27%를 나타낼 것으로 전망됩니다. 고감도 트로포닌 및 BNP 마커를 핵심으로 하는 심장 대사 패널은 심근경색의 신속한 감별 진단에 있어 미국 응급실의 85%에서 표준적으로 채택되고 있습니다. 로슈사의 ‘CoaguChek’을 비롯한 응고 검사 키트는 환자가 직접 INR을 측정하는 것에 대한 메디케어의 보험 급여 제도의 혜택을 받고 있습니다. 임신·불임 검사 키트는 소매 채널에서 높은 판매량을 유지하고 있는 반면, 디지털 배란 모니터는 프리미엄 하위 시장을 개척하고 있습니다. 혈액가스 및 전해질 카트리지는 중환자실에서 여전히 필수적이며, Sight Diagnostics사의 ‘OLO’와 같은 AI 기반 혈액 검사 장치는 응급 진료 클리닉에 도입하는 데 따르는 장벽을 낮추고 있습니다.

폐쇄형 루프 인슐린 투여 시스템이 CGM과 자동 펌프를 결합함에 따라 제품 구성은 재조정될 전망이지만, 새로운 감염증 패널은 상대적으로 빠른 성장이 기대됩니다. 범용 제품 라인에 무선 연결 및 클라우드 분석 기능을 통합하는 제조업체는 사용자 1인당 평생 수익을 확대하고, POC(Point Of Care) 진단 시장에서의 입지를 강화할 수 있을 것입니다.

라테럴 플로우 분석법은 이미 정착된 임신 검사 및 항원 검사의 검사 건수에 힘입어, 2025년에는 매출 점유율의 34.12%를 차지했습니다. 한편, 분자진단 플랫폼은 고도의 실험실 인증이 필요하지 않고, 검체 채취부터 결과 판정까지 30분 이내에 완료되는 PCR 카트리지를 기반으로 연평균 성장률(CAGR) 10.51%를 기록하며 성장하고 있습니다. 딥스틱과 테스트 스트립은 여전히 가장 많이 판매되는 소모품이지만, 스마트폰 카메라가 전용 광학 리더기를 대체함에 따라 상품화 위기에 직면해 있습니다.

애보트의 i-STAT과 같은 마이크로플루이딕스 카트리지는 여러 가지 화학 시약, 전해질, 혈액가스, 심장 마커를 손바닥 크기의 일회용 칩에 담아 10분 이내에 결과를 제공합니다. 이 면역 분석 장비는 중규모 처리 능력을 갖춘 병원 검사실을 위해 제공되며, 병상 검사(bedside testing)와 중앙 자동화 시스템 간의 격차를 해소하고 있습니다. PCR이 더욱 간편하고 저렴해짐에 따라, 분자진단 시스템은 진료소, 재택 간호 및 소규모 클리닉에서 래터럴 플로우 검사 시장 점유율을 잠식할 것이며, POC(Point Of Care) 진단(Point-of-Care) 분야의 고감도 진단 시장이 더욱 확대될 것으로 전망됩니다.

지역별 분석

북미는 2025년에도 매출 점유율 45.67%를 유지했습니다. 이는 CLIA 인증을 받은 진료소 검사실의 긴밀한 네트워크와, 분자진단 기기 및 원격 모니터링 기기 모두에 대한 메디케어의 종합적인 보장 범위에 힘입은 결과입니다. FDA는 2024년, 신속화된 510(k) 절차를 통해 47개의 POC 기기를 승인함으로써 신속한 상용화 주기를 촉진했습니다. 세페이드사는 응급 치료 센터와 응급실에 1만 2,000대의 GeneXpert를 설치했으며, 2024년 3분기에는 카트리지 판매량이 전년 동기 대비 35% 증가했습니다. 그러나 특정 면제 검사에 대한 보상금 삭감이나 민간 보험사의 사전 승인 기준 강화가 향후 확대를 저해할 가능성이 있습니다.

아시아태평양은 가장 빠르게 성장하는 지역으로, 중국과 인도가 농촌 지역 의료 정책을 추진함에 따라 2031년까지 연평균 성장률(CAGR) 10.74%를 나타낼 것으로 전망됩니다. 중국 국가약품감독관리국(NMPA)은 2024년 로슈사의 cobas Liat 시스템을 승인하여, 6억 명의 주민에게 서비스를 제공하는 3만 6,000개의 마을 진료소 네트워크에서 이 시스템을 이용할 수 있도록 했습니다. 인도의 ‘국가 보건 미션’은 2025년, 1차 의료시설의 40%에서 현미경 검사를 이용할 수 없는 지역에 애보트사의 말라리아 신속 검사 키트 1,500만 개를 배포했습니다. 일본, 한국, 호주 역시 CGM(연속 혈당 모니터링) 및 AI 탑재 진단 기기의 적용 범위를 확대하고 있어, 아시아 선진국들의 POC(Point Of Care) 진단 시장을 성장시키고 있습니다.

유럽에서는 2025년 5월까지 기존 POC 기기의 약 30%를 시장에서 퇴출시키는 엄격한 IVDR 규제에 대한 대응이 진행되었습니다. 독일은 환자 스스로 실시하는 INR 검사에 대한 보험 적용을 확대한 반면, 영국의 국민보건서비스(NHS)는 부적절한 항생제 처방을 억제하기 위해 200개 일반 진료소에 로슈사의 cobas Liat를 도입했습니다. 남유럽 국가들은 지방 지역의 검사실 인력 부족을 인식하고, 2025년 독감 시즌을 앞두고 호흡기 신속 검사 키트를 확보했습니다. 아프리카 일부 지역과 태평양의 외딴 섬에서는 콜드체인의 제약으로 인해 분자진단 카트리지의 도입이 여전히 제한되고 있지만, 기부금으로 운영되는 프로그램이 이러한 격차를 메우고 있습니다. 전반적으로, 지역별 정책과 인프라 투자가 POC 진단 시장의 성장 궤도를 함께 강화하는 다양한 기회의 모자이크를 형성하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the point of care diagnostics market size is projected to expand from USD 53.63 billion in 2025 and USD 58.76 billion in 2026 to USD 92.92 billion by 2031, registering a CAGR of 9.90% between 2026 to 2031.

This report is Segmented by Product (Glucose Monitoring Kits, Infectious Disease Testing Kits, and More), Platform (Lateral Flow Assays, Microfluidics-Based Platforms, and More), Sample Type (Blood, Urine, and More), Mode of Purchase (Over-The-Counter (OTC) and Prescription-Based), End User (Hospitals & Clinics, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Global Point Of Care Diagnostics Market Trends and Insights

Rising Prevalence of Chronic and Infectious Diseases

Globally, 537 million adults lived with diabetes in 2024, and the International Diabetes Federation projects 643 million by 2030, underscoring sustained demand for glucose monitoring kits.Parallel outbreaks, such as dengue in Southeast Asia and mpox in Central Africa, have prompted governments to stockpile rapid diagnostic tests. WHO prequalified 12 new malaria rapid tests in 2025, allowing procurement agencies to source assays that meet stringent sensitivity thresholds for low-parasitemia detection. Abbott supplied 15 million malaria tests to India's National Health Mission the same year, covering districts where laboratory microscopy remains unavailable in 40% of primary health centers. Cepheid's GeneXpert MTB/RIF Ultra assay shortened tuberculosis time-to-treatment in South African clinics from 14 days to under 2 hours, demonstrating the clinical advantage of rapid molecular testing. This dual burden of chronic management and outbreak response creates a structural tailwind that lifts the point-of-care diagnostics market across income settings.

Technological Advances and Home-Based POC Uptake

Medicare introduced CPT 99454 in the 2025 Physician Fee Schedule, reimbursing USD 64 per patient per month for devices transmitting physiological data at least 16 days a month. Roche's CoaguChek systems now qualify for virtual INR consultations under this code, while Abbott's Bluetooth-enabled FreeStyle Libre 3 Plus streams glucose readings every minute for remote insulin titration. Dexcom's over-the-counter Stelo sensor, approved in June 2024, opened continuous glucose monitoring to 30 million U.S. Type 2 diabetics previously outside insurance coverage. Smartphone penetration above 70% in many emerging markets further lowers barriers for cloud-linked diagnostic devices. As sensor miniaturization converges with reimbursement reform, the hospital-centric testing model is giving way to decentralized, patient-directed workflows that expand the point-of-care diagnostics market.

Stringent Regulations and Reimbursement Gaps

FDA guidance issued in 2024 raised analytical validation thresholds for POC molecular tests to at least 95% positive and 98% negative percent agreement across three diverse clinical sites. CMS then cut payment for several CLIA-waived codes by 8-12% in the 2025 fee schedule, squeezing the economics for smaller practices. Private insurers, such as Anthem, introduced prior-authorization rules that limit respiratory pathogen panels to high-risk patients. In Europe, the In Vitro Diagnostic Regulation deadline of May 2025 forced roughly 30% of legacy POC devices off the market because manufacturers could not secure notified-body audits. These policy shifts raise compliance costs and curb near-term adoption, tempering growth in the point-of-care diagnostics market.

Other drivers and restraints analyzed in the detailed report include:

- Surge in CLIA-Waived Molecular Respiratory Tests

- Increasing Regulatory Approvals for Novel Assays

- Product Recalls and Accuracy Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Glucose monitoring kits maintained 37.94% of the point-of-care diagnostics market share in 2025, supported by the ubiquity of capillary blood glucose meters and the rapid uptake of CGM sensors. Infectious disease kits, however, are forecast to grow at a 10.27% CAGR through 2031 as global health agencies prequalify new rapid assays for malaria, tuberculosis, and sexually transmitted infections. Cardiometabolic panels built around high-sensitivity troponin and BNP markers are standard in 85% of U.S. emergency departments for rapid myocardial infarction rule-outs. Coagulation kits, led by Roche's CoaguChek, benefit from Medicare reimbursement for patient self-testing of INR. Pregnancy and fertility kits retain high volume in retail channels, while digital ovulation monitors are carving premium subsegments. Blood gas and electrolyte cartridges remain mission-critical in critical care units, and AI-enabled hematology analyzers such as Sight Diagnostics' OLO are lowering the entry threshold for urgent care clinics.

The product mix is likely to rebalance as closed-loop insulin delivery systems pair CGMs with automated pumps, yet novel infectious disease panels promise faster relative growth. Manufacturers that integrate wireless connectivity and cloud analytics into commodity product lines stand to extend lifetime revenue per user, fortifying their positions within the point of care diagnostics market.

Lateral flow assays captured 34.12% of revenue share in 2025, driven by entrenched pregnancy and antigen test volumes. Molecular diagnostics platforms, however, are scaling at a 10.51% CAGR, supported by PCR cartridges that deliver sample-to-answer results in under 30 minutes without high-complexity lab certification. Dipsticks and test strips remain the highest-volume consumables but face commoditization as smartphone cameras replace dedicated optical readers.

Microfluidic cartridges, such as Abbott's i-STAT, house multiple chemistries, electrolytes, blood gases, and cardiac markers in a palm-sized single-use chip that returns results in under 10 minutes. Immunoassay analyzers serve mid-throughput hospital labs, bridging the gap between bedside testing and central automation. As PCR becomes simpler and cheaper, molecular systems are expected to erode lateral flow's share in physician offices, home care, and retail clinics, further expanding the market for high-sensitivity diagnostics at the point of care.

Geography Analysis

North America retained 45.67% revenue share in 2025, supported by a dense network of CLIA-certified physician office laboratories and generous Medicare coverage for both molecular and remote monitoring devices. The FDA cleared 47 POC devices in 2024 under its accelerated 510(k) process, fostering rapid commercialization cycles. Cepheid maintains an installed base of 12,000 GeneXpert units across urgent care centers and emergency departments, driving cartridge growth of 35% year over year in Q3 2024. However, reimbursement cuts for certain waived tests and private-payer prior authorization hurdles may temper future expansion.

Asia-Pacific is the fastest-growing region, projected to log a 10.74% CAGR through 2031 as China and India roll out rural health initiatives. China's NMPA cleared Roche's cobas Liat system in 2024, unlocking access to a network of 36,000 township clinics serving 600 million residents. India's National Health Mission distributed 15 million Abbott malaria rapid tests in 2025 to areas where microscopy is unavailable in 40% of primary centers. Japan, South Korea, and Australia are also expanding coverage for CGM and AI-enabled diagnostics, expanding the point-of-care diagnostics market in developed Asia.

Europe is navigating the stringent IVDR regime that removed roughly 30% of legacy POC devices from the market by May 2025. Germany expanded reimbursement for patient-managed INR testing, while the UK's National Health Service deployed Roche cobas Liat units in 200 general practices to curb inappropriate antibiotic prescribing. Southern European nations procured rapid respiratory assays ahead of the 2025 flu season, acknowledging laboratory staffing gaps in rural areas. Cold-chain limitations continue to constrain molecular cartridge deployment in parts of Africa and remote Pacific islands, yet donor-funded programs are bridging those gaps. Overall, regional policies and infrastructure investments shape a mosaic of opportunities that together reinforce the growth trajectory of the point of care diagnostics market.

- Abbott Laboratories

- Accubiotech Co. Ltd.

- Beckton Dickinson

- bioMerieux

- Bio-Rad Laboratories

- Chembio Diagnostics Inc.

- Danaher Corporation (Cepheid & Beckman Coulter)

- EKF Diagnostics

- Roche

- HemoCue AB

- Johnson & Johnson

- LumiraDx

- Nova Biomedical

- Orasure Technologies

- PTS Diagnostics

- QuidelOrtho

- Radiometer Medical ApS

- Sekisui Diagnostics

- Siemens Healthineers

- Trinity Biotech plc

- Werfen (Instrumentation Laboratory)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Chronic & Infectious Diseases

- 4.2.2 Technological Advances & Home-Based POC Uptake

- 4.2.3 Surge In CLIA-Waived Molecular Respiratory Tests

- 4.2.4 Increasing Regulatory Approvals for Novel Assays

- 4.2.5 AI-Enabled Smartphone Lateral-Flow Analytics

- 4.2.6 Microfluidic Paper-Chips in Philanthropic Screenings

- 4.3 Market Restraints

- 4.3.1 Stringent Regulations & Reimbursement Gaps

- 4.3.2 Product Recalls & Accuracy Concerns

- 4.3.3 QC Non-Compliance Penalties in US Pols

- 4.3.4 Cold-Chain Gaps for Molecular Cartridges in Africa

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Glucose Monitoring Kits

- 5.1.2 Infectious Disease Testing Kits

- 5.1.3 Cardiometabolic Testing Kits

- 5.1.4 Coagulation Monitoring Kits

- 5.1.5 Pregnancy & Fertility Testing Kits

- 5.1.6 Blood Gas / Electrolyte & Metabolite Kits

- 5.1.7 Hematology Testing Kits

- 5.1.8 Tumor / Cancer Marker Testing Kits

- 5.1.9 Urinalysis Testing Kits

- 5.1.10 Cholesterol Test Strips

- 5.2 By Platform

- 5.2.1 Lateral Flow Assays

- 5.2.2 Dipsticks & Test Strips

- 5.2.3 Microfluidics-Based Platforms

- 5.2.4 Immunoassays (CLIA & FIA)

- 5.2.5 Molecular Diagnostics (PCR, INAAT)

- 5.3 By Sample Type

- 5.3.1 Blood

- 5.3.2 Urine

- 5.3.3 Saliva

- 5.3.4 Nasal / Throat Swab

- 5.3.5 Other Specimens (Sweat, Tear, CSF)

- 5.4 By Mode of Purchase

- 5.4.1 Over-the-Counter (OTC)

- 5.4.2 Prescription-Based

- 5.5 By End User

- 5.5.1 Hospitals & Clinics

- 5.5.2 Home-Care Settings

- 5.5.3 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Abbott Laboratories

- 6.3.2 Accubiotech Co. Ltd.

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 bioMerieux SA

- 6.3.5 Bio-Rad Laboratories Inc.

- 6.3.6 Chembio Diagnostics Inc.

- 6.3.7 Danaher Corporation (Cepheid & Beckman Coulter)

- 6.3.8 EKF Diagnostics

- 6.3.9 F. Hoffmann-La Roche Ltd.

- 6.3.10 HemoCue AB

- 6.3.11 Johnson & Johnson (LifeScan)

- 6.3.12 LumiraDx

- 6.3.13 Nova Biomedical Corporation

- 6.3.14 OraSure Technologies Inc.

- 6.3.15 PTS Diagnostics

- 6.3.16 QuidelOrtho Corporation

- 6.3.17 Radiometer Medical ApS

- 6.3.18 Sekisui Diagnostics

- 6.3.19 Siemens Healthineers AG

- 6.3.20 Trinity Biotech plc

- 6.3.21 Werfen (Instrumentation Laboratory)

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment