|

시장보고서

상품코드

2061581

당뇨병 관리 기기 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Diabetes Care Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

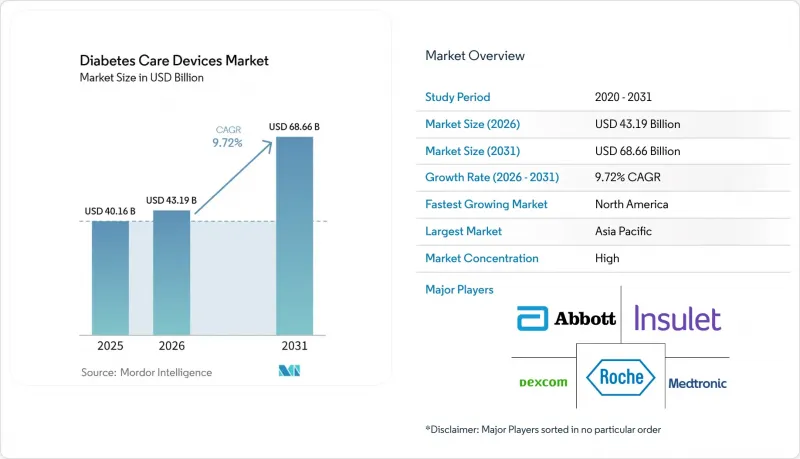

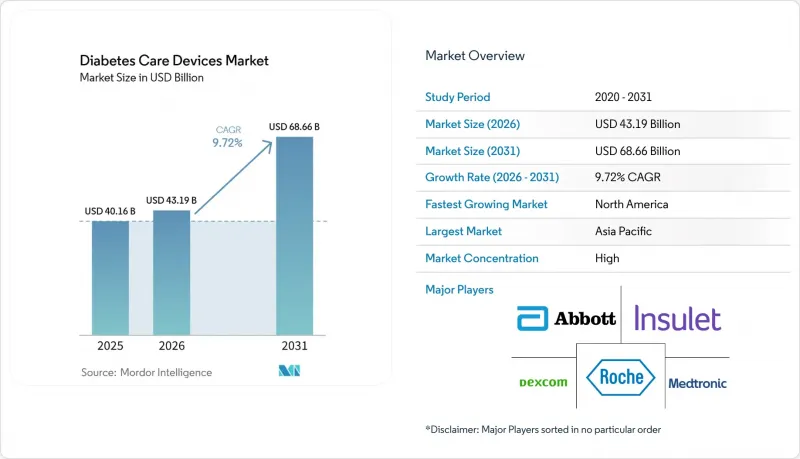

Mordor Intelligence에 의하면, 당뇨병 관리 기기 시장 규모는 2025년 401억 6,000만 달러로 평가되었습니다. 2026년 431억 9,000만 달러로 확대되어 2031년까지 686억 6,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR은 9.72%를 나타낼 전망입니다.

본 보고서는 관리 기기(인슐린 펌프, 인슐린 주사기 등), 모니터링 기기(자가 혈당 측정 및 연속 혈당 모니터링), 환자 유형(1형 당뇨병, 2형 당뇨병 등), 최종 사용자(병원 및 클리닉, 재택 간호 환경 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 당뇨병 관리 기기 시장 동향 및 인사이트

전 세계 CGM에 대한 보험 적용 확대

연속 혈당 모니터링(CGM) 시스템의 보험 적용 범위 확대는 시장 역학을 근본적으로 변화시키고 있으며, 전체 연평균 성장률(CAGR) 전망에 1.7%를 기여하고 있습니다. 중요한 진전으로, 뉴질랜드는 2024년 10월부터 CGM에 대한 자금 지원과 인슐린 펌프 이용 기회 확대를 발표했으며, 첫해에는 1만 2,000명 이상이 자금 지원을 받아 CGM을 이용했습니다. 마찬가지로, 캐나다에서는 2024년 2월 법안 C-64가 도입되어 당뇨병 치료제의 전액 공적 급여를 실현하는 한편, 당뇨병용 의료기기 및 소모품을 위한 전용 기금을 신설하여 약 370만 명의 당뇨병 환자가 안고 있는 경제적 부담을 경감하는 것을 목표로 하고 있습니다(캐나다 보건부). 보험 급여 체계는 고위험 환자만을 대상으로 하던 것에서 보다 광범위한 계층으로 확대되고 있으며, 민간 보험사들도 정부의 조치에 발맞추어 급여 기준을 확대되고 있습니다. 이를 통해 도입 확대, 치료 성과 향상, 그리고 보험 급여의 추가 확대라는 선순환이 이루어지고 있습니다.

전 세계 당뇨병 유병률 및 관련 위험 요인 증가

당뇨병 유병률의 놀라운 증가세가 시장 성장을 견인하고 있으며, 전체 연평균 성장률(CAGR) 전망치에 1.4%를 기여하고 있습니다. BMJ의 연구에 따르면, 1990년부터 2019년 사이 전 세계 연령 조정 1형 당뇨병 유병률은 인구 10만 명당 400명에서 514명으로 증가한 반면, 사망률은 10만 명당 4.74명에서 3.54명으로 감소했으며, 지속적인 관리가 필요한 당뇨병 환자의 수명이 연장되고 있음을 보여줍니다. 이러한 역학적 변화로 인해 모든 부문에서 당뇨병용 의료기기에 대한 지속적인 수요가 발생하고 있습니다. '웨스턴 시드니 당뇨병 이니셔티브'의 보고서에 따르면, 해당 지역 성인의 당뇨병 유병률은 13%를 초과하며, 연간 18억 달러의 경제적 부담이 발생하고 있어 효과적인 관리 솔루션에 대한 재정적 필요성이 부각되고 있습니다. 고령화, 비만율의 상승, 앉아 있는 시간이 많은 생활 습관이 복합적으로 작용하여 전 세계적으로 당뇨병 발병률이 가속화되고 있으며, 특히 식습관의 변화와 도시화가 주요 요인으로 작용하는 신흥 경제국에서는 그 증가세가 급속히 진행되고 있습니다.

의료기기의 높은 비용

보험 적용 전 주요 브랜드의 프리미엄 CGM 연간 비용은 3,800달러 전후로 유지되고 있는 반면, 저가형 플래시식 혈당 측정기는 2,300달러 가까이 듭니다. 공개된 기업 카탈로그 가격을 바탕으로 한 이러한 수치들은 상환 상황이 도입 여부를 좌우하는 양극화된 시장을 만들어내고 있습니다. 경영진은 저소득 지역에서는 연간 500달러의 본인 부담금이라도 도입률을 떨어뜨릴 가능성이 있음을 인식해야 하며, 현지 생산이나 구독형 자금 조달 모델이 효과적일 수 있습니다. 전략 팀에게 중요한 점은 가격 탄력성이 1인당 소득뿐만 아니라 예방 의료에 대한 문화적 인식에 따라서도 달라진다는 것입니다. 예를 들어, 일부 신흥 시장에서는 원격 의료 지원이 패키지에 포함되어 있는 경우, 만성 질환용 기기에 대한 고액의 지출을 기꺼이 감수하는 경향이 있습니다.

부문별 분석

『Journal of Diabetes Science and Technology』에 게재된 연구에 따르면, CGM 사용은 HbA1c 수치 감소 및 치료 성과 개선과 관련이 있는 것으로 나타났으나, 인종 및 사회경제적 지위에 따른 이용 격차는 여전히 존재하고 있습니다(Liebertpub). 인슐린 펌프, 펜, 주사기를 포함한 관리 기기 부문은 자동 인슐린 투여 시스템 및 스마트 인슐린 펜의 혁신에 힘입어 성장이 예상됩니다.

기술의 융합이 경쟁 구도를 재편하고 있으며, 모니터링 기기와 관리 기기의 통합을 통해 종합적인 당뇨병 관리 생태계가 형성되고 있습니다. CGM 데이터와 자동 인슐린 투여를 결합한 하이브리드 폐쇄 루프 시스템의 등장은 큰 진전이며, 연구 결과 목표 범위 내 체류 시간(Time-in-Range) 지표와 사용자의 삶의 질 향상이 입증되었습니다. 2형 당뇨병 성인 환자를 대상으로 한 Omnipod 5 자동 인슐린 투여 시스템의 임상시험에서 13주 후 헤모글로빈 A1c 수치가 8.2%에서 7.4%로 유의미하게 감소하여 혈당 조절이 개선된 것으로 나타났습니다(JAMA Network Open). 광학식 및 전자기식 센서를 포함한 비침습적 혈당 모니터링 기술의 개발은 기존의 모니터링 방법으로 인해 환자가 느끼던 불편함을 해소함으로써 시장을 한층 더 혁신할 것으로 기대되고 있습니다.

지역별 분석

북미는 2025년에도 41.94%의 시장 점유율을 유지했으며, 이는 메디케어의 환급 제도와 기기 조작 훈련을 받은 내분비 전문의의 밀도가 높은 점 등이 한 요인으로 작용했습니다. 같은 해, 미국 질병통제예방센터(CDC)는 미국 내 당뇨병 확진자 수를 2,970만 명, 미진단자 수를 870만 명으로 집계했습니다(CDC 인용). 이처럼 방대한 미진단 환자층은 잠재적인 시장 확대의 원천이며, 의료기기 제조업체는 소매 약국과 협력하여 실시하는 선별 검사 조치를 통해 이 환자층을 타겟으로 삼을 수 있습니다. 그러나 의료비 절감을 요구하는 고용주와 공적 보험사의 압박이 거세지고 있는 만큼, 향후 프리미엄 플랫폼의 가격 압박이 심화되면서 제조업체들은 가치 기반 의료(Value-Based Care) 계약으로 전환하게 될 것입니다.

아시아태평양은 도시화와 세계 최대 규모의 당뇨병 환자 수에 힘입어, 2031년까지 연평균 성장률(CAGR) 12.31%를 기록하며 가장 빠른 성장세를 보이고 있습니다. 국제당뇨병연맹(IDF)의 추산에 따르면, 이 지역의 당뇨병 환자 수는 전 세계 당뇨병 환자 수의 60% 이상을 차지하고 있습니다. 제조 기업의 경영진은 아시아태평양이 전 세계에서 디지털화가 가장 많이 진행된 인구를 보유하고 있다는 사실을 간과하기 쉬운데, 그로 인해 스마트폰과 연동되는 CGM 모델은 기존의 블루투스 전용 모델을 뛰어넘어 널리 보급될 가능성이 있습니다. 그 결과, 앱에 현지 언어로 된 AI 코칭 기능을 탑재한 공급업체는 타사를 압도할 정도로 높은 시장 점유율을 확보할 것으로 전망됩니다.

유럽은 국민건강보험 제도와 고령화 인구 덕분에 안정적인 입지를 유지하고 있습니다. 유럽의약품청(EMA)이 주도하는 해당 지역의 규제 환경은 기존에 FDA보다 더 긴 기간의 임상시험 추적 조사를 요구해 왔으며, 이는 상품화를 지연시키는 요인이 될 수 있습니다. 최근 애보트와 덱스콤 간의 특허 분쟁이 화해에 이르면서, 그동안 조달 일정에 불확실성을 초래했던 법적 우려가 해소됨에 따라 병원 구매 담당자들은 수년에 걸친 공급 계약에 대해 보다 명확한 전망을 세울 수 있게 되었습니다. 상황을 예리하게 분석해 보면, 유럽의 구매 담당자들은 앞으로 법적 제약이 없는 두 공급업체가 존재한다는 점을 활용하여 일괄 구매 할인을 협상함으로써, 평균 판매 가격을 낮추는 동시에 판매 수량을 늘릴 가능성이 있다고 볼 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the diabetes care devices market size is expected to increase from USD 40.16 billion in 2025 to USD 43.19 billion in 2026 and reach USD 68.66 billion by 2031, growing at a CAGR of 9.72% over 2026-2031.

This report is Segmented by Management Devices (Insulin Pumps, Insulin Syringes, and More), Monitoring Devices (Self-Monitoring Blood Glucose and Continuous Glucose Monitoring), by Patient Type (Type-1 Diabetes, Type-2 Diabetes and More), by End User (Hospitals & Clinics, Home-Care Settings and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Diabetes Care Devices Market Trends and Insights

Rapid Reimbursement Expansion for CGM Worldwide

The expansion of insurance coverage for continuous glucose monitoring (CGM) systems is fundamentally reshaping market dynamics, with a 1.7% contribution to the overall CAGR forecast. In a significant development, New Zealand announced funding for CGMs and expanded access to insulin pumps effective October 2024, with expectations of over 12,000 people accessing funded CGMs in the first year . Similarly, Canada's introduction of Bill C-64 in February 2024 aims to provide universal coverage for diabetes medications and create a dedicated fund for diabetes devices and supplies, addressing the financial burden for approximately 3.7 million Canadians with diabetes Health Canada . The reimbursement landscape is shifting from covering only high-risk patients to broader populations, with private insurers following government initiatives to expand coverage criteria, creating a virtuous cycle of increased adoption, improved outcomes, and further reimbursement expansion

Increasing Global Prevalence of Diabetes and Associated Risk Factors

The alarming rise in diabetes prevalence is driving market growth with a 1.4% contribution to the overall CAGR forecast. According to a BMJ study, the global age-standardized prevalence of type 1 diabetes increased from 400 to 514 per 100,000 population between 1990 and 2019, while mortality decreased from 4.74 to 3.54 per 100,000, indicating longer lifespans for diabetic patients requiring continuous management. This epidemiological shift is creating sustained demand for diabetes devices across all segments. The Western Sydney Diabetes initiative reported diabetes rates exceeding 13% among adults in the region, with an economic burden of USD 1.8 billion annually, highlighting the financial imperative for effective management solutions. The convergence of aging populations, increasing obesity rates, and sedentary lifestyles is accelerating diabetes incidence worldwide, with particularly rapid growth in emerging economies where changing dietary patterns and urbanization are contributing factors.

High Cost of Devices

Premium CGM annualized costs hover near USD 3,800 for flagship brands before insurance, while lower-priced flash glucose monitors cost closer to USD 2,300. These figures, drawn from publicly available company catalog pricing, create a bifurcated market in which reimbursement status largely dictates adoption. Executives should recognize that in low-income regions even a USD 500 annual out-of-pocket burden can depress uptake, so localized manufacturing or subscription-based financing may prove effective. The takeaway for strategy teams is that pricing elasticity varies not only by per-capita income but also by cultural perceptions of preventive care; for instance, some emerging markets accept higher spending on chronic-disease devices if bundled telehealth support is included.

Other drivers and restraints analyzed in the detailed report include:

- Advancements in Technology

- Increased Government and Private Investments

- Less Awareness About Device Usage in Remote and Underdeveloped Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The monitoring devices segment commands a dominant 65.15% market share in 2025 and is expected to grow with a 10.15% CAGR from 2026-2031, reflecting its critical role in diabetes management across all patient populations. Continuous glucose monitoring (CGM) systems are revolutionizing diabetes care through real-time data provision and integration with automated insulin delivery systems, fundamentally changing treatment paradigms. A study published in the Journal of Diabetes Science and Technology demonstrated that CGM use is associated with lower HbA1c levels and improved outcomes, though disparities in access persist based on race and socioeconomic status Liebertpub. The management devices segment, encompassing insulin pumps, pens, and syringes, is projected to grow, driven by innovations in automated insulin delivery systems and smart insulin pens.

Technological convergence is reshaping the competitive landscape, with integration between monitoring and management devices creating comprehensive diabetes management ecosystems. The emergence of hybrid closed-loop systems that combine CGM data with automated insulin delivery represents a significant advancement, with studies showing improvements in time-in-range metrics and quality of life for users. A clinical trial of the Omnipod 5 automated insulin delivery system in adults with type 2 diabetes demonstrated a significant reduction in hemoglobin A1c levels from 8.2% to 7.4% after 13 weeks, indicating improved glycemic control JAMA Network Open. The development of non-invasive glucose monitoring technologies, including optical and electromagnetic sensors, promises to further transform the market by addressing patient discomfort associated with traditional monitoring methods.

Geography Analysis

North America maintains a 41.94% share in 2025, partially owing to Medicare reimbursement and a high density of device-trained endocrinologists. In that same year, the CDC recorded 29.7 million diagnosed and 8.7 million undiagnosed cases of diabetes in the United States (same CDC citation). This sizable undiagnosed cohort provides a latent expansion pool that device makers can target via screening initiatives tied to retail pharmacies. Yet mounting pressure from employers and government payers to reduce healthcare spending suggests future price compression for premium platforms, nudging manufacturers toward value-based-care contracts.

Asia-Pacific posts the fastest growth at 12.31% CAGR through 2031, driven by urbanization and the world's highest absolute number of diabetes cases. International Diabetes Federation estimates place the region's share above 60% of global prevalence. Manufacturing executives often overlook that Asia-Pacific also boasts some of the world's most digitally engaged populations, so smartphone-tethered CGM models may leapfrog earlier Bluetooth-only variants. Consequently, suppliers that embed local language AI coaching into their apps stand to win disproportionately high market share.

Europe sustains a stable presence thanks to universal health systems and aging demographics. The region's regulatory environment, guided by the European Medicines Agency, traditionally demands longer trial follow-ups than the FDA, which can delay commercialization. The recent Abbott-Dexcom patent truce removes a legal overhang that previously cast uncertainty on procurement timelines, giving hospital buyers clearer visibility into multi-year supply contracts. An astute reading of the situation suggests that European buyers will now leverage the presence of two legally unencumbered suppliers to negotiate bulk-purchase discounts, compressing average selling prices but potentially boosting unit volumes.

- A. Menarini Diagnostics srl

- Abbott Laboratories

- Arkray

- Ascensia Diabetes Care Holdings AG (PHC Holdings Corporation)

- Bionime

- Dexcom

- Embecta Corp.

- Roche

- Insulet

- LifeScan Enterprises LLC

- Medtronic

- Nipro

- Novo Nordisk

- Rossmax

- Sanofi

- Senseonics

- Tandem Diabetes Care

- Terumo

- Trividia Health, Inc.

- Ypsomed

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid reimbursement expansion for CGM Worldwide

- 4.2.2 Increasing Global prevalence of diabetes and associated risk factors

- 4.2.3 advancements in technology

- 4.2.4 Increased Government and Private Investments

- 4.2.5 European paediatric guidelines accelerating hybrid closed-loop pump uptake

- 4.2.6 Off-label GLP-1 surge fuelling home glucose testing demand in North America

- 4.3 Market Restraints

- 4.3.1 High Cost of Devices

- 4.3.2 Less Awareness about Device usage in remote and underdeveloped region

- 4.3.3 EU-MDR re-certification backlog for legacy lancets

- 4.3.4 Patch-pump recalls dampening uptake in Oceania

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Device Type

- 5.1.1 Monitoring Devices

- 5.1.1.1 Self-Monitoring

- 5.1.1.1.1 Glucometer Devices

- 5.1.1.1.2 Test Strips

- 5.1.1.1.3 Lancets

- 5.1.1.2 Continuous Glucose Monitoring

- 5.1.1.2.1 Sensors

- 5.1.1.2.2 Durables

- 5.1.1.1 Self-Monitoring

- 5.1.2 Management Devices

- 5.1.2.1 Insulin Pumps

- 5.1.2.1.1 Insulin Pump Device

- 5.1.2.1.2 Insulin Pump Reservoir

- 5.1.2.1.3 Infusion Set

- 5.1.2.2 Insulin Syringes

- 5.1.2.3 Insulin Pens

- 5.1.2.4 Jet Injectors

- 5.1.2.1 Insulin Pumps

- 5.1.1 Monitoring Devices

- 5.2 By Patient Type

- 5.2.1 Type-1 Diabetes

- 5.2.2 Type-2 Diabetes

- 5.2.3 Gestational & Others

- 5.3 By End-user

- 5.3.1 Hospitals & Clinics

- 5.3.2 Home-care Settings

- 5.3.3 Ambulatory Surgical Centres

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 France

- 5.4.2.3 Italy

- 5.4.2.4 Spain

- 5.4.2.5 United Kingdom

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 Japan

- 5.4.3.2 South Korea

- 5.4.3.3 China

- 5.4.3.4 India

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Mexico

- 5.4.4.2 Brazil

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 GCC

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 A. Menarini Diagnostics srl

- 6.3.2 Abbott Laboratories

- 6.3.3 ARKRAY, Inc.

- 6.3.4 Ascensia Diabetes Care Holdings AG (PHC Holdings Corporation)

- 6.3.5 Bionime Corporation

- 6.3.6 Dexcom, Inc.

- 6.3.7 Embecta Corp.

- 6.3.8 F. Hoffmann-La Roche Ltd.

- 6.3.9 Insulet Corporation

- 6.3.10 LifeScan Enterprises LLC

- 6.3.11 Medtronic PLC

- 6.3.12 Nipro Corporation

- 6.3.13 Novo Nordisk A/S

- 6.3.14 Rossmax International Ltd.

- 6.3.15 Sanofi

- 6.3.16 Senseonics Holdings Inc.

- 6.3.17 Tandem Diabetes Care, Inc.

- 6.3.18 Terumo Corporation

- 6.3.19 Trividia Health, Inc.

- 6.3.20 Ypsomed AG