|

시장보고서

상품코드

2061746

비디오 스트리밍 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Video Streaming Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

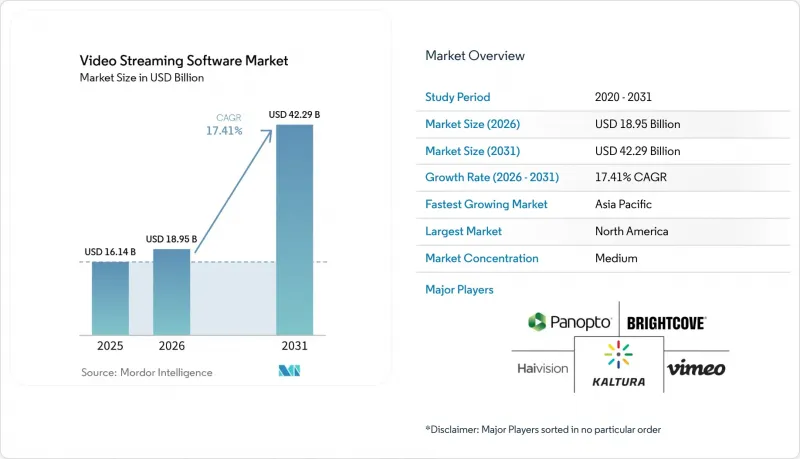

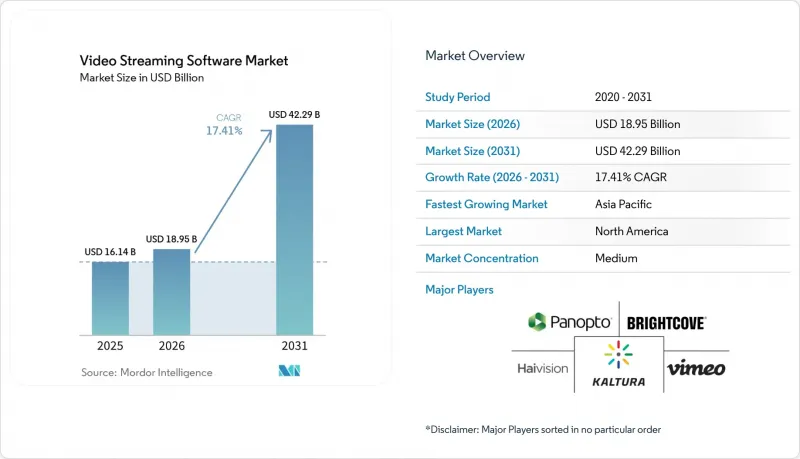

Mordor Intelligence에 의하면, 2026년 비디오 스트리밍 소프트웨어 시장 규모는 189억 5,000만 달러에 달할 것으로 추정됩니다. 2025년 161억 4,000만 달러에서 성장하여 2031년에는 422억 9,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 17.41%를 나타낼 것으로 전망됩니다.

본 보고서는 구성 요소(솔루션, 서비스), 도입 형태(클라우드, On-Premise), 스트리밍 형태(라이브, 주문형 비디오), 업종(미디어 및 엔터테인먼트, 법인·기업, 기타) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 비디오 스트리밍 소프트웨어 시장 동향 및 분석

아시아태평양 기업들의 비디오 활용 방식을 혁신하는 5G 독립형 네트워크의 급속한 확산

독립형 5G의 도입으로 초기 제조 시범 프로젝트에서 종단 간 지연 시간이 10밀리초 미만으로 단축되었습니다. 현재 공장에서는 로봇 용접 라인에서 촬영된 다각도 HD 영상을 원격지의 검사원에게 스트리밍으로 전송하여, 수작업으로 인한 지연을 해소하고 생산을 지속하고 있습니다. 불과 1초의 단축만으로도 시간당 생산 대수가 증가하기 때문에 경영진은 인라인 품질 모니터링 솔루션을 위한 비디오 스트리밍 소프트웨어 시장에 신속하게 예산을 배정하고 있습니다. 이러한 새로운 사례는 공급망 컨소시엄 내에서 급속히 확산되며, 대상 수요를 초기 스마트 팩토리 도입 기업을 넘어 확대시키고 있습니다.

북미 OTT 플랫폼에서 기능 사이클 단축을 실현하는 클라우드 네이티브 마이크로서비스

2024년, 많은 북미의 컨텐츠 제공업체들은 인코딩, 추천, 서버 측 광고 삽입을 독립적인 워크로드로 처리하는 컨테이너화된 마이크로서비스로 모놀리식 시스템을 분해했습니다. 이를 통해 사업자는 유명인의 생방송 인터뷰 중 추천 기능 등 부하가 급증하는 마이크로서비스만 확장할 수 있어, 스택의 다른 부분에 과도한 비용을 들이지 않아도 됩니다. 그 결과로 탄생하는 ‘성장에 따른 과금’이라는 경제성은 과도한 자원 확보를 줄여 연구 개발비 증액으로 이어지고, 신규 가입자를 유치하며, 비디오 스트리밍 소프트웨어 시장에 더욱 탄력을 불어넣을 것입니다.

특허 사용료의 급등이 독립 벤더들의 오픈 코덱 채택을 촉진하고 있습니다.

적응형 비트레이트와 관련된 지적 재산권 최소 지불액이 인상됨에 따라, 틈새 시장 제공업체들은 로열티가 없는 형식을 시험적으로 도입할 수밖에 없게 되었습니다. 한 학습 관리 플랫폼에서는 비트레이트 라더를 재조정함으로써, 파일 크기가 약간 증가한 것을 상쇄하고 라이선스 비용을 절감하여 매출 총이익률을 유지했습니다. 서버 측 감지 루틴은 지원되지 않는 기기를 낮은 비트레이트로 전환함으로써 로열티 인상 위험에 대한 대비책을 제공하지만, 한편으로는 특허료의 영향을 가장 크게 받는 부문에서 비디오 스트리밍 소프트웨어 시장에 하방 압력을 가하고 있습니다.

부문별 분석

솔루션은 2025년 매출의 대부분을 차지했으며, 그 비중은 89.3%에 달했습니다. 이는 모든 도입 과정에서 자산의 가져오기, 인코딩, 관리를 수행하는 플랫폼의 핵심이 여전히 필요하기 때문입니다. 이러한 핵심 인프라를 바탕으로 분석 기능, AI 썸네일, 자동 품질 관리(QC)가 동일한 코드베이스에 추가됨에 따라 비디오 스트리밍 소프트웨어 시장은 지속적으로 성장하고 있습니다. 한편, 서비스 수익은 연평균 성장률(CAGR) 20.9%로 증가할 것으로 전망됩니다. 이는 업무에 쫓기는 IT 부서가 음성-텍스트 변환 태깅, 이벤트 기반 트랜스코딩, 제로 트러스트 액세스 제어와 같은 복잡한 통합 작업을 외부에 위탁하기 위함입니다. 관리 계약을 통해 SLA 준수 현황을 모니터링하고 취약점에 대한 패치를 적용함으로써, 안정적이고 지속적인 수익원이 창출됩니다. 예측 기간 동안 플랫폼 공급업체와 전문 통합업체 간의 공동 영업 프로그램을 통해 비디오 스트리밍 소프트웨어 시장에 더 많은 비즈니스 기회가 창출될 것입니다.

서비스의 성장이 가속화되더라도, 플랫폼 아키텍처를 보유한 벤더는 가격 결정력을 유지합니다. 왜냐하면 컨텐츠 라이브러리나 비즈니스 로직이 통합되면, 고객이 플랫폼을 바꾸는 일은 거의 없기 때문입니다. 코덱의 지속적인 혁신은 정기적인 업그레이드를 촉진하여 계약 갱신으로 이어집니다. 한편, 분석 플러그인은 해지율과 버퍼링 현상을 연관 짓는 대시보드에 정보를 제공합니다. 이러한 상호작용을 통해 수익이 안정화되고, 서비스 생태계가 함께 번창하는 가운데에서도 솔루션 계층은 비디오 스트리밍 소프트웨어 시장의 중심에 계속 자리매김할 것입니다.

2025년에는 클라우드 기반 서비스가 비디오 스트리밍 소프트웨어 시장 규모의 68.40%를 차지했으며, 예측 불가능한 트래픽 급증에 대응할 수 있는 유연한 용량을 필요로 하는 사업자가 증가함에 따라 연평균 성장률(CAGR) 22.1%를 나타낼 것으로 전망됩니다. 엣지 노드는 현재 최종 사용자와 가까운 곳에서 적시 패키징 및 광고 결정 처리를 수행하여, 로딩 시간을 단축하는 동시에 오리진 서버의 부하를 줄이고 있습니다. 이 접근 방식은 2025년 음악 축제에서 그 진가를 발휘했습니다. 그곳에서는 휴대전화 통신 상태가 불안정한 상황에서도 멀티 카메라를 통한 4K 스트림의 프레임 일관성이 유지되어, 비디오 스트리밍 소프트웨어 시장에서 클라우드-엣지 아키텍처에 대한 신뢰가 더욱 공고해졌습니다.

데이터 주권이나 기존 투자 측면에서 로컬 처리가 필요한 경우, On-Premise 솔루션은 여전히 유효합니다. 은행은 기밀성이 높은 이사회를 프라이빗 센터 내에서 인코딩하고, DRM으로 보호된 스트림을 외부 CDN으로 전송하여 전 세계에서 재생할 수 있도록 하고 있습니다. On-Premise에서의 캡처, 리저널 클라우드에서의 트랜스코딩, 엣지에서의 지오블로킹과 같은 하이브리드 파이프라인을 통해 사업자는 규정 준수 및 확장성을 모두 확보할 수 있습니다. 통합 콘솔의 보급에 따라 의사결정권자들은 아키텍처의 이념보다 상업적 조건을 더 중요시하게 되었지만, 그럼에도 불구하고 더 광범위한 비디오 스트리밍 소프트웨어 시장과 부합하는 ‘클라우드 퍼스트’ 전략에 대한 기세는 여전히 이어지고 있습니다.

지역별 분석

북미는 광대역 보급, 고밀도 하이퍼스케일 용량, 그리고 비디오 우선 워크플로로 조기에 문화적 전환을 이룬 덕분에 2025년 비디오 스트리밍 소프트웨어 시장에서 37.60%의 점유율을 차지했습니다. 병원들은 규제 관련 부담을 검색 가능한 지식 기반으로 전환하는 규정 준수 아카이브에 예산을 할당하고 있는 반면, 방송사들은 고객 유지율을 높이는 예측 분석 기능을 도입하고 있습니다. 한 상장 벤더의 2024년 SEC 제출 서류는 자동화된 엔게이지먼트 엔진으로의 전략적 전환을 확인하는 내용이었으며, 투자자들은 기업 가치 상승을 통해 이러한 움직임을 긍정적으로 평가하고, 일반화된 서비스 제공보다는 차별화된 기능 세트에 대한 신뢰를 보여주었습니다.

아시아태평양은 모바일 우선 인구 동향과, 고해상도 및 저지연 경험을 지방까지 제공하는 적극적인 5G SA(Standalone) 방식의 보급에 힘입어 연평균 성장률(CAGR) 약 19.4%를 나타낼 것으로 전망됩니다. 각국 정부는 통신탑 건설 및 현지 컨텐츠 제작에 보조금을 지원하고 있으며, 언어별 자막 및 더빙은 표준 입찰 요건으로 자리 잡고 있습니다. 각 통신사는 제어 평면을 공유하면서도 워크로드를 국가별로 분리하는 멀티테넌트형 지역 클라우드를 구축하고 있으며, 이를 통해 규정 준수 요건과 규모의 경제 사이의 균형을 유지하면서 비디오 스트리밍 소프트웨어 시장의 총 잠재 시장 규모를 확대되고 있습니다.

유럽에서는 소비자의 높은 기대와 엄격한 개인정보 보호법이 공존하고 있습니다. 2024년 사법부의 판결에 따라, 각 플랫폼은 개인 식별 정보가 EU 역외로 유출되지 않도록 EU 내 데이터센터 건설을 가속화했습니다. 영국의 한 방송사가 7,000시간 이상의 기존 컨텐츠를 클라우드 네이티브 워크플로로 전환한 결과, 병렬 처리 처리량이 10배 향상되었습니다. 초기 비용은 급증했지만, 처리 시간이 단축됨에 따라 시청자들이 이제 당연하게 여기는 ‘에피소드 당일 공개’가 가능해졌습니다. 광고주가 자금을 지원하는 요금제가 보급되면서, 유럽의 측정 프레임워크에 최적화된 SSAI 모듈에 대한 수요를 견인하는 동시에, 비디오 스트리밍 소프트웨어 시장의 지역적 비즈니스 기회를 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the video streaming software market size in 2026 is estimated at USD 18.95 billion, growing from 2025 value of USD 16.14 billion with 2031 projections showing USD 42.29 billion, growing at 17.41% CAGR over 2026-2031.

This report is Segmented by Component (Solutions, Services), Deployment Type (Cloud, On-Premise), Streaming Type (Live, Video On Demand), Vertical (Media and Entertainment, Corporate and Enterprise, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Video Streaming Software Market Trends and Insights

Rapid 5G stand-alone networks transforming enterprise video in Asia-Pacific

Standalone 5G roll-outs have pushed end-to-end latency below 10 milliseconds in early manufacturing pilots. Factories now stream multi-angle HD feeds from robotic welding lines to remote inspectors, eliminating manual lag and keeping production running. When every fractional second saved translates into extra units produced per hour, management quickly assigns a budget to the video streaming software market for inline quality monitoring solutions. Emerging case studies travel fast across supply-chain consortia, expanding addressable demand beyond initial smart-factory adopters.

Cloud-native microservices shortening feature cycles for North-American OTT platforms

In 2024, many North American providers decomposed monoliths into containerised microservices that handle encoding, recommendation, and server-side ad insertion as independent workloads. Operators can now dial up only the microservice that spikes, such as recommendations during a celebrity live interview, without overspending on the rest of the stack. The resulting pay-as-you-grow economics reduce over-provisioning, fuel incremental R&D allocations, and attract new subscribers, feeding additional momentum into the video streaming software market.

Patent royalty escalation motivating open codecs among independent vendors

Rising minimum payments for adaptive-bitrate IP compel niche providers to trial royalty-free formats. One learning-management platform offset marginally larger file sizes by re-balancing bitrate ladders, saving licence fees and protecting gross margin. Server-side detection routines down-switch devices that lack support, providing a hedge against royalty hikes, yet placing downward pressure on the video streaming software market in segments most exposed to patent fees.

Other drivers and restraints analyzed in the detailed report include:

- Corporate hybrid-work townhalls fuelling live-video platforms in Europe

- Interactive livestream shopping catalysing ultra-low-latency tools in the Middle East

- GDPR data-transfer rulings reshaping EU platform architectures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions contributed the larger slice of 2025 revenue, estimated at 89.3%, because every deployment still needs a platform core to ingest, encode, and manage assets. That core foundation keeps the video streaming software market expanding as feature road-maps layer analytics, AI thumbnails, and automated QC onto the same codebase. Services revenue, however, is forecast to climb at 20.9% CAGR as overstretched IT departments outsource complex integrations such as speech-to-text tagging, event-driven transcodings, and zero-trust access controls. Managed contract, then monitor SLA compliance and patch vulnerabilities, creating sticky annuity streams. Over the forecast horizon, joint go-to-market programmes between platform suppliers and specialised integrators will channel incremental opportunities back into the video streaming software market.

Even with faster services growth, vendors that own the platform architecture preserve pricing power because customers rarely re-platform once content libraries and business logic are embedded. Continuous codec innovation triggers periodic upgrades that renew contracts, while analytics plug-ins feed dashboards correlating churn to buffer events. The interplay stabilises revenue and keeps the solutions layer at the centre of the video streaming software market even as service ecosystems flourish in parallel.

Cloud deployment captured 68.40% of the video streaming software market size in 2025 and is projected to grow at a 22.1% CAGR as operators gravitate toward elastic capacity that accommodates unpredictable traffic spikes. Edge nodes now handle just-in-time packaging and ad decisioning nearer to end-users, reducing startup time and offloading origin servers. The approach shone during a 2025 music festival where multi-camera 4K streams retained frame integrity despite fluctuating cellular conditions, reinforcing trust in cloud-edge architectures within the video streaming software market.

On-premise solutions remain viable when data sovereignty or sunk investments dictate local processing. Banks encode sensitive board meetings inside private centres, then push DRM-protected ladders to external CDNs for worldwide playback. Hybrid pipelines, capture on-premise, transcode in regional clouds, enforce geo-blocking at the edge, let operators blend compliance with elasticity. As single-pane consoles converge, decision makers weigh commercial terms rather than architectural philosophy, yet the momentum still favours cloud-first strategies that align with the broader video streaming software market.

Geography Analysis

North America held 37.60% of the video streaming software market in 2025 due to widespread broadband, dense hyperscale capacity, and an early cultural shift toward video-first workflows. Hospitals budget for compliant archives that convert regulatory burdens into searchable knowledge bases, while broadcasters embed predictive analytics that improve customer retention. A publicly listed vendor's 2024 SEC filing confirmed a strategic pivot toward automated engagement engines, and investors rewarded the move with valuation gains, signalling confidence in differentiated feature sets over commoditised delivery .

Asia-Pacific is set for roughly 19.4% CAGR thanks to mobile-first demographics and aggressive 5G stand-alone coverage that brings high-resolution, low-latency experiences into rural districts. Governments subsidise tower build-outs and local content production, turning language-specific subtitles and dubbing into standard bid requirements. Providers deploy multi-tenant regional clouds that segregate workloads by country while sharing control planes, balancing compliance with economies of scale and enlarging the total addressable slice of the video streaming software market.

Europe blends advanced consumer expectations with stringent privacy laws. After 2024 judicial rulings, platforms accelerated data-centre build-outs inside the bloc to ensure personal identifiers never exit EU borders. A UK broadcaster's migration of 7,000-plus hours of heritage content into a cloud-native workflow yielded a ten-fold uptick in parallel processing throughput . Though upfront costs spiked, turnaround times shrink, enabling same-day episodic release that viewers now expect. Advertiser-funded tiers gain traction, driving demand for SSAI modules tuned to European measurement frameworks and enlarging the regional opportunity within the video streaming software market.

- Brightcove Inc.

- Kaltura Inc.

- Amazon Web Services, Inc. (AWS Elemental)

- IBM Corporation

- Vimeo.com Inc.

- Panopto Inc.

- Haivision Systems Inc.

- Vbrick Systems Inc.

- Qumu Corporation

- Dacast

- Mux

- MediaPlatform, Inc.

- Bitmovin

- Akamai Technologies, Inc.

- Wowza Media Systems, LLC

- JW Player Inc.

- Google LLC (YouTube Live)

- Harmonic Inc.

- Telestream, LLC

- Cloudinary

- Synamedia Ltd.

- Verizon Media (Edgecast)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid rollout of 5G SA networks accelerating low-latency enterprise streaming demand in Asia-Pacific

- 4.2.2 Cloud-native micro-services adoption boosting SaaS OTT platforms in North America

- 4.2.3 Corporate spend on hybrid-work townhalls fuelling internal live-video platforms in Europe

- 4.2.4 Shoppable livestream commerce uptake driving interactive streaming tools in the Middle East

- 4.2.5 US CMS rules mandating secure tele-video archiving in healthcare

- 4.2.6 D2C sports-rights migration energising multi-CDN orchestration in South America

- 4.3 Market Restraints

- 4.3.1 Escalating adaptive-bitrate patent royalties squeezing smaller vendors

- 4.3.2 GDPR / Schrems-II hurdles limiting EU cross-border video data flows

- 4.3.3 Rural last-mile congestion in Africa undermining QoS SLAs

- 4.3.4 High creator churn on freemium platforms eroding SMB ARPU

- 4.4 Regulatory Outlook

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Investment Analysis

- 4.8 Pricing Analysis

- 4.8.1 Subscription-based

- 4.8.2 Advertising-supported

- 4.8.3 Transaction-based (Pay-per-View)

- 4.8.4 Hybrid / Freemium

5 MARKET SIZE AND GROWTH FORECASTS (VALUE USD BILLION)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 Video Management

- 5.1.1.2 Transcoding and Processing

- 5.1.1.3 Video Delivery and Post-Production

- 5.1.1.4 Video Analytics

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Managed Services

- 5.1.1 Solutions

- 5.2 By Deployment Type

- 5.2.1 Cloud

- 5.2.2 On-premise

- 5.3 By Streaming Type

- 5.3.1 Live

- 5.3.2 Video on Demand

- 5.4 By Vertical

- 5.4.1 Media and Entertainment

- 5.4.1.1 OTT Platforms

- 5.4.1.2 Broadcast and Cable TV Networks

- 5.4.1.3 Sports and Esports

- 5.4.2 Corporate and Enterprise

- 5.4.3 Education and eLearning

- 5.4.4 Healthcare and Telemedicine

- 5.4.5 Banking, Financial Services and Insurance (BFSI)

- 5.4.6 Other Verticals

- 5.4.1 Media and Entertainment

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 Latin America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Mexico

- 5.5.2.4 Rest of Latin America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 New Zealand

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Developments

- 6.2 Vendor Positioning Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.3.1 Brightcove Inc.

- 6.3.2 Kaltura Inc.

- 6.3.3 Amazon Web Services, Inc. (AWS Elemental)

- 6.3.4 IBM Corporation

- 6.3.5 Vimeo.com Inc.

- 6.3.6 Panopto Inc.

- 6.3.7 Haivision Systems Inc.

- 6.3.8 Vbrick Systems Inc.

- 6.3.9 Qumu Corporation

- 6.3.10 Dacast

- 6.3.11 Mux

- 6.3.12 MediaPlatform, Inc.

- 6.3.13 Bitmovin

- 6.3.14 Akamai Technologies, Inc.

- 6.3.15 Wowza Media Systems, LLC

- 6.3.16 JW Player Inc.

- 6.3.17 Google LLC (YouTube Live)

- 6.3.18 Harmonic Inc.

- 6.3.19 Telestream, LLC

- 6.3.20 Cloudinary

- 6.3.21 Synamedia Ltd.

- 6.3.22 Verizon Media (Edgecast)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment