|

시장보고서

상품코드

2061749

중국의 골판지 포장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)China Corrugated Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

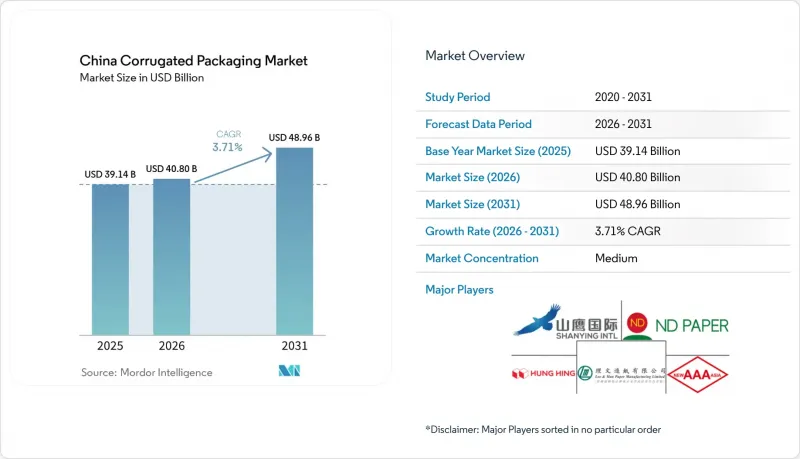

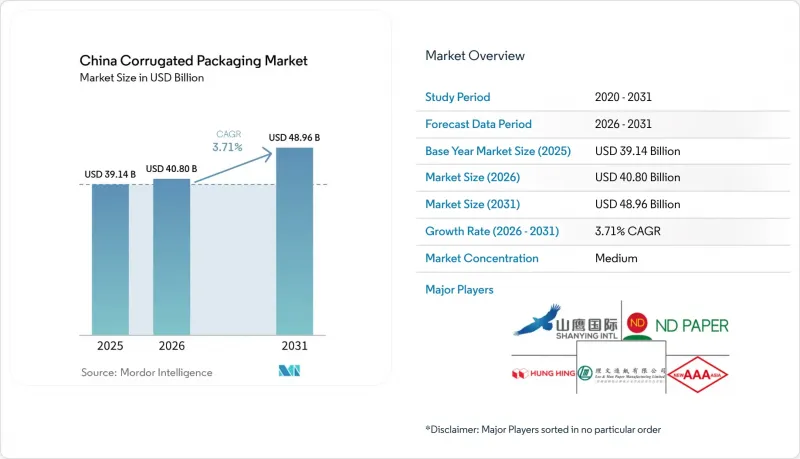

Mordor Intelligence에 의하면, 중국의 골판지 포장 시장 규모는 2025년에 391억 4,000만 달러로 평가되었습니다. 2026년에 408억 달러에 달하고, 2031년까지 489억 6,000만 달러에 이를 것으로 예측됩니다. 2026년부터 2031년에 걸쳐 CAGR은 3.71%를 나타낼 전망입니다.

본 보고서는 원료(버진 크라프트 라이너보드, 재생 라이너보드, 골판지 심재 등), 플루트 유형(A 플루트 등), 포장 유형(레귤러 슬롯 컨테이너 등), 벽 구조(싱글, 더블 등), 인쇄 기술(플렉소 인쇄 등), 최종 사용자 산업(가공 식품 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중국의 골판지 포장 시장 동향과 인사이트

확대되는 전자상거래 물류 수요

2024년, 중국에서는 1750억 개의 소포가 처리되었으며, 그중 약 68%를 골판지 상자가 차지했습니다. 이를 통해 해당 채널은 중국의 골판지 포장 시장에서 최대 단일 수요처로서의 입지를 확고히 다졌습니다. 풀필먼트 센터에서는 기존의 슬롯이 있는 컨테이너에서 빈 공간을 채우는 재료를 줄일 수 있는 적정 크기의 다이컷 상자로 전환하고 있으며, 이를 통해 자동 라인에서 30초 미만으로 포장 주기를 완료할 수 있게 되었습니다. JD 로지스틱스는 2024년에 10억 개 이상의 2차 포장 상자를 줄였으며, 이로 인해 제조업체들은 생산량이 아닌 리드타임, 디지털 맞춤화, 설계 정밀도 측면에서 경쟁할 수밖에 없게 되었습니다. 하이난 자유무역항 및 광둥·홍콩·마카오 대만구의 국경 간 전자상거래 판매업체들은 국제항공운송협회(IATA)의 부피 중량 규정에 부합하는 마이크로 플루트 형식을 요구하고 있으며, 평균 판 두께가 감소하고 있음에도 불구하고 단위당 수요는 계속 증가하고 있습니다. 2025년에 총 상품 가치 4조 9,000억 위안(6,800억 달러)을 창출한 라이브 커머스는 포장을 화면상의 광고로 탈바꿈시켰으며, 각 브랜드가 오프셋 인쇄가 가능하고 카메라에 잘 나오는 배송용 상자에 대해 40-60%의 추가 비용을 지불하도록 유도하고 있습니다.

재활용 가능한 포장을 장려하는 환경 규제 강화

생태환경부는 새로운 골판지 상자의 재생 재료 함유율 기준을 기존 70%에서 2027년까지 85%로 상향 조정했습니다. 이로 인해 2025년 재생 라이너보드 시장 점유율은 63.21%로 안정되었습니다. 2025년에 폐지 수입 할당량을 420만 톤으로 축소하는 조치로 인해 국내 폐지 시장이 공급 부족에 직면하면서, 가격은 전년 대비 12% 상승했습니다. 각 성에서 시행되고 있는 확대 생산자 책임(EPR) 시범 사업으로 인해 회수 비용이 브랜드 소유주에게 전가되면서, 저장성과 장쑤성에서는 경량화 및 대체 섬유의 시범 도입이 가속화되고 있습니다. 의약품 분야에서는 새로운 T/CNPPA 3029-2025 규격이 낮은 수증기 투과성을 규정하고 있어, 콜드체인용 골판지 상자에서 버진 크라프트 등급이 규제 측면에서 우위를 점하고 있습니다. 대형 제지 업체들은 규모의 경제를 활용해 폐수 처리 및 VOC(휘발성 유기 화합물) 대책에 대한 설비 투자를 감당하고 있지만, 지방의 가공업체들은 제14차 5개년 계획 하에서 8%-12%의 이익률 하락에 직면해 있습니다.

폐지 수입 정책의 변동

2025년에는 불순물 함유율 0.3%라는 상한 규제로 인해 수입량이 420만 톤으로 감소했습니다. 이로 인해 제지 업체들은 현물 시장의 가격 급등에 직면하게 되었으며, 통관 기간도 7일에서 18일로 늘어났습니다. 국내 폐지(OCC) 가격이 12% 상승하면서 자체 제지 설비를 갖추지 않은 가공업체들이 어려움을 겪고 있습니다. 또한 재활용성 측면에서 타협점이 있음에도 불구하고, 일부 구매자들은 플렉서블 파우치로 전환하고 있습니다. 그동안 미국산 장섬유 스크랩을 주로 사용해 온 연안 지역 제지 업체들은 현재 버진 펄프로의 자본 재분배를 추진하고 있습니다. 그 예로, 나인 드래곤스가 48억 달러를 투자해 건설한, 연간 110만 톤의 화학 펄프를 생산하는 북해 복합 시설을 들 수 있습니다. 도시 지역의 골판지 폐기물 수거 체계는 여전히 분산되어 있으며, 도시 지역 골판지 폐기물의 35%가 혼합 폐기물로 수거되고 있어 탈색 비용이 증가하고, 소규모 제지 업체의 경쟁력이 약화되고 있습니다.

부문별 분석

2025년, 재생 라이너보드는 중국의 골판지 포장 시장의 63.21%를 차지했으며, 이는 2027년까지 택배용 골판지에 85%의 재생 소재 사용을 의무화하는 정책을 반영한 것입니다. 통합형 제지 제조업체는 전국적인 폐지 수거 네트워크를 통해 원료 조달 면에서 우위를 확보하고, 비용 경쟁력의 기반을 다지고 있습니다. 버진 크래프트 라이너 보드는 연평균 성장률(CAGR) 4.77%를 나타낼 것으로 예측되며, 신선식품 수출업체와 고급 이커머스 브랜드들이 더 높은 링 크러시 강도, 인열 저항성 및 더 매끄러운 인쇄면을 요구함에 따라 전체 시장 성장률을 상회할 전망입니다. 나인 드래곤즈의 북해 공장과 리 앤 만의 특수 크라프트지 생산 라인 확충은 이 프리미엄 시장을 겨냥한 것입니다. 골판지 원지 제조업체들은 침엽수 원료의 위험을 분산하기 위해 대나무나 짚을 원료로 하는 반화학 펄프를 시험하고 있지만, 습기에 민감한 특성 때문에 이러한 등급의 제품은 여전히 습도가 낮은 물류 경로로만 한정되어 있습니다.

왁스를 사용하지 않고 재활용성을 확보하기 위해 바이오 배리어 코팅 및 전분계 접착제의 시범 생산이 확대되고 있으며, 이는 중국의 골판지 포장 시장이 대량 생산되는 재생재 함유 제품과 규모는 작지만 높은 수익률을 보이는 신재(virgin material) 틈새 시장으로 양극화될 것임을 시사합니다. 이와 동시에, T/CNPPA 3029-2025에 근거한 식품 접촉 및 의약품 관련 규제로 인해, 엄격한 온도 관리가 필요한 용도는 버진 펄프로 전환되고 있으며, 이를 통해 원자재 비용 상승을 상쇄할 수 있는 가격 안정성이 보장되고 있습니다. 따라서 컨버터의 전략은 범용 제품 제조업체가 재생 라이너보드의 효율성을 추구하는 한편, 부가가치형 전문 제조업체가 프리미엄 크라프트지나 기능성 코팅을 활용해 브랜드 소유주를 유치하는 방식으로 양극화가 진행되고 있습니다.

B 플루트는 일반 상품의 완충성과 비용 간의 균형을 고려할 때, 2025년 중국의 골판지 포장 시장에서 34.15%의 점유율을 차지했습니다. 그러나 국경 간 판매 업체들이 부피와 중량의 최적화를 꾀하고, 화장품 브랜드들이 오프셋 인쇄 수준의 그래픽을 요구하는 가운데, F-플루트는 2031년까지 연평균 성장률(CAGR) 4.15%로 성장하고 있습니다. 이 플루트의 두께(0.75-1.0 mm) 덕분에 직접 오프셋 인쇄가 가능해져 오프셋 라미네이션 공정이 필요 없을 뿐만 아니라, 재고 부피를 줄일 수 있습니다. 이는 높이 제한이 있는 자동 창고에서 매우 중요합니다.

E 플루트는 소매점용 진열대로서, 적정한 원자재 비용으로 강성을 확보할 수 있는 타협안으로서의 입지를 유지하고 있습니다. A 플루트는 두께가 5mm라는 특성 때문에 깨지기 쉬운 도자기나 무거운 산업용 부품에 여전히 사용되고 있지만, 경량화에 대한 요구로 인해 그 시장 점유율은 감소하는 추세입니다. 현재 골판지 제조기 OEM 제조업체들은 공장에서 15분 이내에 플루트 프로파일을 교체할 수 있는 퀵 체인지 카세트 시스템을 공급하고 있으며, 이를 통해 중소기업도 마이크로 플루트를 쉽게 도입할 수 있게 되어 도입 추세가 가속화되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 역학

제6장 시장 규모 및 성장 예측

제7장 경쟁 구도

제8장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the china corrugated packaging market size is projected to be USD 39.14 billion in 2025, USD 40.80 billion in 2026, and reach USD 48.96 billion by 2031, growing at a CAGR of 3.71% from 2026 to 2031.

This report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, and More), Flute Type (A Flute, and More), Packaging Type (Regular Slotted Containers, and More), Wall Type (Single, Double, and More), Printing Technology (Flexographic, and More), and End-User Industry (Processed Foods, and More). The Market Forecasts are Provided in Terms of Value (USD).

China Corrugated Packaging Market Trends and Insights

Expanding E-Commerce Fulfillment Demand

China processed 175 billion parcels in 2024, and corrugated boxes accounted for roughly 68% of that volume, cementing the channel as the single largest off-taker in the China corrugated packaging market. Fulfillment centers are shifting from regular slotted containers to right-sized, die-cut boxes that reduce void fill, enabling automated lines to complete a pack cycle in under 30 seconds. JD Logistics eliminated more than 1 billion secondary cartons in 2024, forcing converters to compete on lead time, digital customization, and design precision rather than tonnage. Cross-border sellers in the Hainan Free Trade Port and the Greater Bay Area demand micro flute formats that comply with International Air Transport Association dimensional-weight rules, sustaining unit growth even as average board weight declines. Livestream shopping, a channel that generated CNY 4.9 trillion (USD 0.68 trillion) in gross merchandise value during 2025, has turned packaging into on-screen advertising, prompting brands to pay 40%-60% premiums for litho-laminated, camera-ready shippers.

Rising Environmental Regulations Favoring Recyclable Packaging

The Ministry of Ecology and Environment raised the recycled-content threshold for new corrugated boxes to 85% by 2027, up from a 70% baseline, anchoring recycled linerboard's 63.21% share in 2025. Import quotas that cut recovered-paper inflows to 4.2 million tonnes in 2025 tightened domestic scrap markets, lifting prices 12% year on year. Provincial extended-producer-responsibility pilots shift collection costs to brand owners, accelerating lightweighting and alternative-fiber trials in Zhejiang and Jiangsu. In pharmaceuticals, the new T/CNPPA 3029-2025 standard specifies low moisture-vapor transmission, carving a regulatory moat for virgin kraft grades in cold-chain cartons. Large mills capitalize on scale to absorb wastewater and VOC-control capex, while regional converters face margin erosion of 8%-12% under the 14th Five-Year Plan.

Volatility in Recovered Paper Import Policies

Imports slid to 4.2 million tonnes in 2025 under a 0.3% contamination cap, exposing mills to spot-market spikes and lengthening customs clearance from 7 to 18 days. Domestic OCC prices rose 12%, squeezing converters without captive pulping and prompting some buyers to shift to flexible pouches despite recyclability trade-offs. Coastal mills that historically favored long-fiber American scrap are reallocating capital to virgin pulp, illustrated by Nine Dragons' USD 4.8 billion Beihai complex with 1.1 million tonnes of chemical pulp. Municipal collection remains fragmented, with 35% of urban corrugated waste still co-mingled, adding de-inking costs and weakening small-mill competitiveness.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Fresh Produce and Food Delivery Services

- Urbanization Driving Consumer Goods Consumption

- Competition from Flexible Plastic Packaging

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled linerboard accounted for 63.21% of the China corrugated packaging market in 2025, reflecting the mandated 85% recycled content requirement for express parcels by 2027. Integrated mills capture feedstock advantages through nationwide OCC collection networks, anchoring their cost leadership. Virgin Kraft linerboard is forecast to expand at 4.77% CAGR, outperforming overall growth as fresh-produce exporters and luxury e-commerce brands demand higher ring-crush strength, tear resistance, and cleaner print surfaces. Nine Dragons' Beihai mill and Lee and Man's specialty-kraft upgrades target this premium. Corrugating medium producers are testing semi-chemical pulps from bamboo and straw to hedge softwood risks, though moisture sensitivity still confines such grades to low-humidity logistics corridors.

Bio-based barrier coatings and starch adhesives are scaling up in pilot runs to achieve recyclability without wax, signaling that the China corrugated packaging market will bifurcate into high-volume recycled-content and smaller, high-margin virgin niches. In parallel, food-contact and pharmaceutical mandates under T/CNPPA 3029-2025 steer critical temperature-controlled applications toward virgin fiber, guaranteeing a price umbrella that offsets higher raw-material costs. The converter strategy, therefore, splits commodity players chase recycled linerboard efficiency, while value-added specialists court brand owners with premium kraft and functional coatings.

B flute held 34.15% of the China corrugated packaging market share in 2025 because of its cushioning-to-cost balance in general merchandise. However, the F flute is accelerating at 4.15% CAGR through 2031 as cross-border sellers optimize for dimensional weight and cosmetics brands seek offset-level graphics. The flute's 0.75-1.0 mm caliper allows direct lithographic printing, eliminating litho-lamination steps and lowering inventory bulk, which is vital in automated warehouses with height constraints.

E flute remains the compromise format for retail-ready displays, offering rigidity with acceptable board economy. A flute persists for fragile ceramics and heavy industrial parts owing to its 5 mm thickness, though its share erodes under lightweighting mandates. Corrugator OEMs now ship quick-change cassette systems that let factories swap flute profiles in under 15 minutes, democratizing micro flute access for small and medium enterprises and enhancing adoption momentum.

List of Companies Covered in this Report:

- Shanying International Holdings Co. Ltd.

- Nine Dragons Paper (Holdings) Limited

- Lee & Man Paper Manufacturing Ltd.

- Hung Hing Printing Group Limited

- New Asia Packaging Co. Ltd.

- HengFeng Packaging Materials Co. Ltd.

- Shanghai DE Printed Box

- Belpax

- Baoding Yueyang Packaging

- ZZ Group International Holdings Limited

- Jingxing Paper

- Minfeng Special Paper Co. Ltd.

- Yutian Hs Packaging Co. Ltd.

- Dongguan Jianxin

- Rizhao Forest Packaging

- Sinopack Industries Ltd.

- International Paper (China) Co. Ltd.

- Smurfit Westrock plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Overview of the Global Corrugated Packaging Market

- 4.6 Investment Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Expanding E-Commerce Fulfillment Demand

- 5.1.2 Rising Environmental Regulations Favoring Recyclable Packaging

- 5.1.3 Growth in Fresh Produce and Food Delivery Services

- 5.1.4 Urbanization Driving Consumer Goods Consumption

- 5.1.5 Provincial Incentives for Lightweight Packaging Innovation

- 5.1.6 Adoption of Digital Print-On-Demand Corrugated Boxes by SMEs

- 5.2 Market Restraints

- 5.2.1 Volatility in Recovered Paper Import Policies

- 5.2.2 Competition from Flexible Plastic Packaging

- 5.2.3 Bottlenecks in Last-Mile Logistics Pallet Standardization

- 5.2.4 Emerging Bioplastic Corrugated Alternatives from Startups

6 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 6.1 By Material

- 6.1.1 Virgin Kraft Linerboard

- 6.1.2 Recycled Linerboard

- 6.1.3 Corrugating Medium

- 6.1.4 Semi-Chemical Fluting

- 6.1.5 Other Materials

- 6.2 By Flute Type

- 6.2.1 A Flute

- 6.2.2 B Flute

- 6.2.3 C Flute

- 6.2.4 E Flute

- 6.2.5 F Flute

- 6.3 By Packaging Type

- 6.3.1 Regular Slotted Containers

- 6.3.2 Die-Cut Custom Boxes

- 6.3.3 Folding Cartons

- 6.3.4 Point-of-Purchase Displays

- 6.3.5 Pallet Boxes

- 6.3.6 Other Packaging Types

- 6.4 By Wall Type

- 6.4.1 Single-Wall

- 6.4.2 Double-Wall

- 6.4.3 Triple-Wall

- 6.4.4 Single Face

- 6.5 By Printing Technology

- 6.5.1 Flexographic Printing

- 6.5.2 Digital Inkjet Printing

- 6.5.3 Litho-Lamination

- 6.5.4 Screen Printing

- 6.5.5 Other Printing Technologies

- 6.6 By End-User Industry

- 6.6.1 Processed Foods

- 6.6.2 Fresh Food and Produce

- 6.6.3 Beverages

- 6.6.4 Paper Products

- 6.6.5 Electrical Products

- 6.6.6 Personal Care and Cosmetics

- 6.6.7 E-commerce Fulfillment Centers

- 6.6.8 Pharmaceuticals

- 6.6.9 Other End-User Industries

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles

- 7.4.1 Shanying International Holdings Co. Ltd.

- 7.4.2 Nine Dragons Paper (Holdings) Limited

- 7.4.3 Lee & Man Paper Manufacturing Ltd.

- 7.4.4 Hung Hing Printing Group Limited

- 7.4.5 New Asia Packaging Co. Ltd.

- 7.4.6 HengFeng Packaging Materials Co. Ltd.

- 7.4.7 Shanghai DE Printed Box

- 7.4.8 Belpax

- 7.4.9 Baoding Yueyang Packaging

- 7.4.10 ZZ Group International Holdings Limited

- 7.4.11 Jingxing Paper

- 7.4.12 Minfeng Special Paper Co. Ltd.

- 7.4.13 Yutian Hs Packaging Co. Ltd.

- 7.4.14 Dongguan Jianxin

- 7.4.15 Rizhao Forest Packaging

- 7.4.16 Sinopack Industries Ltd.

- 7.4.17 International Paper (China) Co. Ltd.

- 7.4.18 Smurfit Westrock plc

8 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 8.1 White-Space and Unmet-Need Assessment