|

시장보고서

상품코드

2063759

필리핀의 골판지 포장 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Philippines Corrugated Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

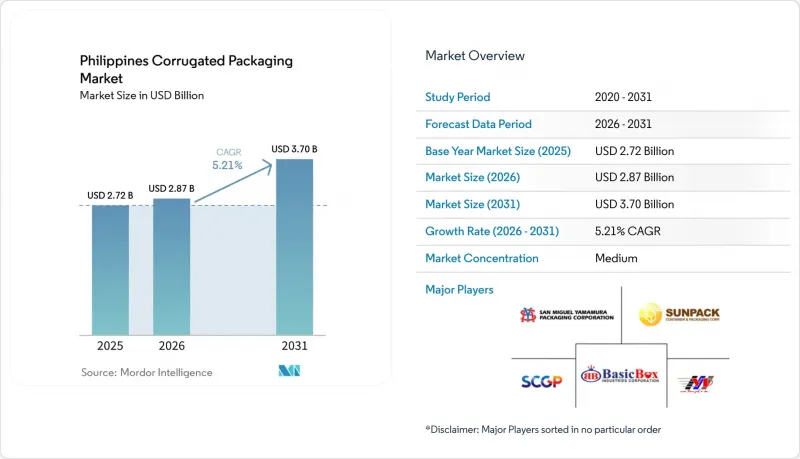

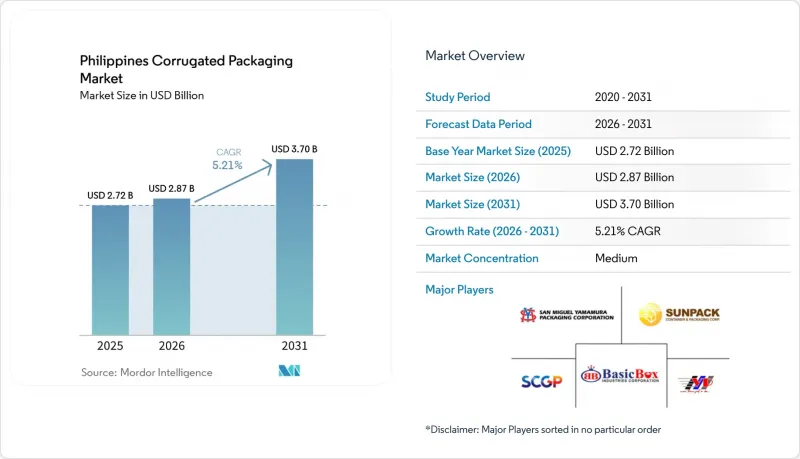

Mordor Intelligence에 의하면, 필리핀 골판지 포장 시장 규모는 2025년 27억 2,000만 달러, 2026년 28억 7,000만 달러에서 2031년까지 37억 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 5.21%를 나타낼 것으로 예측됩니다.

본 보고서는 원료(버진 크라프트 라이너보드, 재생 라이너보드 등), 플루트 유형(A 플루트 등), 포장 유형(레귤러 슬롯 컨테이너 등), 벽 구조(싱글월, 더블월 등), 인쇄 기술(플렉소 인쇄 등), 최종 사용자 산업(가공식품 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

필리핀 골판지 포장 시장 동향과 인사이트

전자상거래의 성장이 소포 처리량 증가를 가속화

당일 및 익일 배송 약속은 유통 양상을 일변시켜, 팔레트 단위로 매장에 물품을 보충하던 방식에서 수백만 건에 달하는 단품 배송으로 전환시켰습니다. 11월 11일이나 12월 12일과 같은 플래시 세일로 인한 수요 급증으로 인해, 골판지 제조업체들은 계절 한정으로 공백 제품을 재고로 확보하고, 모서리 압축 강도를 유지하면서 화물 중량을 제한할 수 있는 골판지 조합을 조정해야만 합니다. 육상, 해상, 항공을 아우르는 복합 운송은 습기에 노출되는 정도를 증가시켜, 적층 시험을 통과하면서도 경량인 재생 섬유 라이너로의 전환을 사업자들에게 촉진하고 있습니다. 풀필먼트 센터에서는 자동 분류기가 최소한의 인력으로 소포 스캔, 라벨 부착, 매니페스트 작성을 수행할 수 있도록 상자 크기를 표준화하고 있습니다. 이러한 변화들이 복합적으로 작용하여 필리핀의 골판지 포장 시장 취급량이 증가하고 있으며, 특히 메트로 마닐라의 소포 허브에서 그 추세가 두드러집니다.

일회용 플라스틱에 대한 정부의 규제가 종이 기반 대체품의 확산을 촉진하고 있습니다.

‘확대 생산자 책임법’에 따르면, 브랜드 소유자는 2024년까지 플라스틱 포장 사용량의 40%, 2028년까지 80%를 회수해야 할 의무가 있으며, 이를 위반할 경우 최대 500만 달러의 벌금이 부과됩니다. 이와 동시에, 재무성은 일회용 비닐봉지에 대해 1Kg당 100달러의 물품세를 도입하는 방안을 추진하고 있으며, 이로 인해 소매 가격이 94% 상승할 것으로 예측됩니다. 가송시의 행정 복합 시설 내 일회용 플라스틱 제품 금지령부터 전국적인 소포장(사셰)의 단계적 폐지에 이르기까지, 각지의 조례가 압박을 강화하고 있습니다. 각 브랜드 소유 기업들은 현재 재활용 가능성 심사에서 높은 평가를 받을 수 있는 골판지 재질의 2차 포장재와 섬유 기반 테이크아웃 용기를 지정하고 있습니다. 이러한 규제로 인해 조달 담당자들은 골판지 추가 조달을 확보하도록 독려받고 있으며, 이는 필리핀 골판지 포장 시장의 성장세를 더욱 공고히 하고 있습니다.

국내 및 수입 폐지 가격의 변동

2024년, 미국 및 EU의 회수율이 하락하고 인도네시아의 검사 수수료가 상승함에 따라, 수입 폐지(OCC) 시세는 유럽산 95/5가 톤당 160달러에서 미국산 DS-OCC가 톤당 230달러로 변동했습니다. 현지 가공업체들은 이중의 위험에 직면해 있습니다. 수입 등급의 입고 비용 상승에 더해, 비공식 부문의 회수업자들이 공급을 줄였을 때 시장 가격이 급등락하는 상황이 발생하고 있습니다. 기능적인 자원 회수 시설을 가동하고 있는 바랑가이(행정구)는 고작 44%에 불과하며, 메트로 마닐라의 서비스 적용률은 20%에 그치고 있어 제지 공장은 화물 도착 지연이나 섬유 품질 저하에 취약한 상태입니다. 이러한 충격은 매출총이익률을 압박하고 있으며, 필리핀 골판지 포장 시장에서 단기적인 투자 의욕을 위축시키고 있습니다.

부문별 분석

2025년, 필리핀의 골판지 포장 시장에서 재생 라이너보드는 56.12%의 점유율을 차지하며, 국내 폐지(OCC) 공급원에 대한 구조적인 의존도를 반영하고 있습니다. 필리핀의 재생 섬유용 골판지 포장 시장은 원지 펄프 부족을 보완하기 위해 제지 업체들이 현지에서 포장된 골판지와 수입된 A급 폐지(OCC)를 혼합하여 사용하고 있기 때문에 계속해서 성장하고 있습니다. 연평균 성장률(CAGR) 7.13%가 예상되는 세미케미컬·플루팅은 동등한 적재 강도를 갖추면서도 경량인 제품을 찾는 섬 간 운송업체들로부터 지지를 얻고 있으며, 이러한 추세는 유류할증료의 상승으로 인해 더욱 강화되고 있습니다. 버진 크래프트 라이너 보드는 습기 저항성이 중요한 농산물 및 의약품 수출용이라는 틈새 시장을 꾸준히 유지하고 있으며, 인쇄 시의 광택과 습윤 강도에 대한 평가가 그 높은 가격을 정당화하고 있습니다.

골판지 심지 시장은 United Pulp and Paper사가 새로 가동한 일일 생산량 870톤 규모의 OCC 생산 라인의 혜택을 받고 있습니다. 이 라인에서는 PrimeRotor 스크린을 사용하여 불순물을 제거하고, 용지 폭의 안정성을 확보하고 있습니다. 또한, 농림부가 99곳의 하이브리드 에너지 방식 냉장 창고에 30억 페소(5,280만 달러)를 투자함에 따라 고성능 코팅재에 대한 수요가 점차 증가하고 있습니다. 왁스 또는 바이오 코팅이 적용된 라이너를 갖춘 3층 구조의 블랭크는 장거리 냉장 운송 시 결로로 인한 손상을 방지하며, 필리핀 골판지 포장 시장 전체에서 수익성이 높은 틈새 시장을 형성하고 있습니다. 수입 OCC 가격의 변동으로 인해 제지 업체들은 예측 가능한 비용으로 원료를 확보할 수 있는 자사 회수 센터에 대한 의존도를 높이고 있으며, 전기 요금이 상승하는 상황에서도 이익률을 높이고 있습니다.

B 플루트는 내압성, 인쇄 적합성, 자동 케이스 포장기와의 호환성 면에서 균형이 뛰어나, 2025년에는 41.37%의 시장 점유율을 차지했습니다. 이 가공 업체는 상당한 가동 중단 시간 없이 B 플루트에서 C 플루트, E 플루트로 전환할 수 있는 연속 나이프 방식을 채택하여, 계절 한정 음료 트레이나 전자기기용 수축 포장 대체품에 신속하게 대응할 수 있도록 하고 있습니다. B 플루트 두께의 3분의 1에 해당하는 F 플루트는 화장품 및 스마트 워치 판매업체들이 택배용 파우치에 들어갈 수 있고, 부피 중량 할증 요금을 절감할 수 있는 얇은 포장재를 선호함에 따라 연평균 성장률(CAGR) 6.89%를 나타낼 것으로 전망됩니다.

필리핀의 F 플루트 골판지 포장 시장 규모는 현재로서는 여전히 소규모이지만, 멀티패스 디지털 그래픽 기술을 통해 단위당 이익률은 높은 임베디드니다. C-플루트는 무거운 통조림 제품의 포장에서 여전히 확고한 입지를 유지하고 있지만, 브랜드 소유주들은 얇은 두께를 통해 업스트림 공정에서 비용을 절감하는 데 주목하고 있습니다. E-플루트는 피자나 의류 우편 배송용 포장재로서, 접이식 골판지 상자를 대체할 수 있는 견고한 대안으로도 활용됩니다. 한편, A 플루트의 사용은 뛰어난 완충성이 필요한 대량의 농산물 수출로 한정되어 있습니다. 슬림형 설계의 도입은 항해 시간을 단축하고 습기 유입 위험을 줄이며, 사업자가 더 가벼운 구조로 전환할 수 있도록 하는 항만 현대화 추세와 발을 맞추고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the philippines corrugated packaging market size is projected to expand from USD 2.72 billion in 2025 and USD 2.87 billion in 2026 to USD 3.7 billion by 2031, registering a CAGR of 5.21% between 2026 to 2031.

This report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, and More), Flute Type (A Flute, and More), Packaging Type (Regular Slotted Containers, and More), Wall Type (Single-Wall, Double-Wall, and More), Printing Technology (Flexographic Printing, and More), End-User Industry (Processed Foods, and More). The Market Forecasts are Provided in Terms of Value (USD).

Philippines Corrugated Packaging Market Trends and Insights

E-Commerce Growth Accelerating Parcel Volumes

Same-day and next-day delivery commitments have transformed the distribution landscape, swapping palletized store replenishment for millions of single-item drop-offs. Flash-sale peaks on 11-11 and 12-12 force corrugators to stock seasonal blanks and adjust flute combinations that limit freight weight while preserving edge-crush strength. Multi-modal legs across road, sea, and air magnify humidity exposure, steering merchants toward lighter recycled-fiber liners that still pass stacking tests. Fulfillment centers are standardizing box footprints so automated sorters can scan, label, and manifest parcels with minimal human touch. These shifts collectively raise volumes for the Philippines' corrugated packaging market, especially in Metro Manila's parcel hubs.

Government Restrictions on Single-Use Plastics Favoring Paper-Based Alternatives

The Extended Producer Responsibility Act requires brand owners to recover 40% of their plastic packaging footprint in 2024, climbing to 80% by 2028, with fines up to USD 5 million for non-compliance. Simultaneously, the Department of Finance is pressing for a USD 100-per-kilogram excise tax on disposable plastic bags, potentially pushing retail bag prices up 94%. Local ordinances from Quezon City's civic complex ban on plastic disposables to nationwide sachet phase-outs compound the pressure. Brand owners now specify corrugated secondary packs and fiber-based takeout containers that score favorably on recyclability audits. These mandates are nudging procurement managers to lock in extra corrugated volumes, fortifying the growth arc of the Philippines corrugated packaging market.

Volatility in Domestic and Imported Recovered Paper Prices

Import OCC quotes swung from USD 160 per tonne for European 95/5 to USD 230 per tonne for U.S. DS-OCC in 2024 as U.S. and EU collection rates dipped and Indonesian inspection fees rose. Local converters suffer double exposure: higher landed costs on imported grades and erratic street-price jumps when informal-sector collectors thin out supply. Only 44% of barangays operate functional materials-recovery facilities, with Metro Manila's coverage at 20%, leaving mills vulnerable to cargo arrival lags and fiber quality downgrades. These shocks crimp gross margins and temper near-term investment appetite in the Philippines corrugated packaging market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Shift Toward Sustainable and Recycled Fiber Packaging

- Expansion of Processed Food and Beverage Manufacturing Hubs

- Port Congestion and Shipping Delays Inflating Lead Times and Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled linerboard captured 56.12% of the Philippines corrugated packaging market in 2025, reflecting structural dependence on domestic OCC streams. The Philippines' corrugated packaging market for recycled fiber continues to grow as mills blend locally baled cartons with imported Class A OCC to offset the scarcity of virgin pulp. Semi-chemical fluting, forecast to grow at a 7.13% CAGR, is gaining favor among inter-island shippers seeking lighter grammages with similar stacking strength, a shift amplified by rising fuel surcharges. Virgin Kraft linerboard remains a niche for moisture-critical produce and pharmaceutical exports, where print gloss and wet-strength ratings justify the premium.

The corrugating medium benefits from United Pulp and Paper's new 870-TPD OCC line, which filters contaminants using PrimeRotor screens to stabilize runnability. Demand for performance coatings is inching up as the Department of Agriculture spends PHP 3 billion (USD 52.8 million) on 99 hybrid-energy cold storages. Triple-wall blanks with wax or bio-coated liners prevent condensation damage on long reefers, creating a profitable specialty pocket within the broader Philippines corrugated packaging market share landscape. Imported OCC volatility continues to push mills toward captive collection centers that lock in fiber at predictable costs, strengthening margins even as power tariffs rise.

B flute secured 41.37% market share in 2025 thanks to its balance of crush resistance, print surface, and compatibility with automatic case packers. Converters run continuous-knife setups that switch from B to C to E flute without major downtime, allowing rapid response to seasonal beverage trays or electronics shrink-wrap replacements. F flute, one-third the caliper of B, is projected for 6.89% CAGR as cosmetics and smart-watch sellers opt for slimmer parcels that fit courier pouches and reduce dimensional weight surcharges.

The Philippines corrugated packaging market size for F flute remains modest today yet offers higher unit margins because of multi-pass digital graphics. C flute maintains a foothold in heavy canned-goods packs, but brand owners eye upstream savings from thinner profiles. E flute doubles as a rigid alternative to folding cartons for pizza and apparel mailers, while A flute's usage is confined to bulk agro-exports requiring superior cushioning. Thin-profile adoption aligns with port modernization that reduces voyage time, easing moisture-ingress risks and enabling merchants to shift toward lighter makeup.

List of Companies Covered in this Report:

- SCG Packaging Public Company Limited

- San Miguel Yamamura Packaging Corp.

- Liberty Corrugated Boxes Mfg. Corp.

- Valenzuela Packaging Container Corp.

- Quality Corrugated Box Manufacturing Corp.

- Sunpack Container and Packaging Corp.

- Prime Worldwide Paper Packaging Corp.

- Steniel Graham Packaging Philippines Corp.

- Malinta Corrugated Boxes Manufacturing Corp.

- Basic Box Industries Corp.

- Papercon Philippines Inc.

- Central Corrugated Box Corp.

- Duraboard Packaging Corp.

- Three Dimensional Packaging Corp.

- Boxworld Co Inc.

- Basic Box Industries Corp.

- RM Box Center

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce Growth Accelerating Parcel Volumes

- 4.2.2 Rapid Shift Toward Sustainable and Recycled Fiber Packaging

- 4.2.3 Expansion of Processed Food and Beverage Manufacturing Hubs

- 4.2.4 Government Restrictions on Single-Use Plastics Favoring Paper-Based Alternatives

- 4.2.5 Modernization of Inter-Island Logistics Networks Demanding Durable Lightweight Boxes

- 4.2.6 Adoption of Digital Printing Enabling Short-Run Customization for SMEs

- 4.3 Market Restraints

- 4.3.1 Volatility in Domestic and Imported Recovered Paper Prices

- 4.3.2 Substitution Threat From Flexible Plastics and Reusable Plastic Crates

- 4.3.3 Port Congestion and Shipping Delays Inflating Lead Times and Costs

- 4.3.4 Escalating Electricity Tariffs Increasing Corrugator Operating Expenses

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Virgin Kraft Linerboard

- 5.1.2 Recycled Linerboard

- 5.1.3 Corrugating Medium

- 5.1.4 Semi-Chemical Fluting

- 5.1.5 Other Materials

- 5.2 By Flute Type

- 5.2.1 A Flute

- 5.2.2 B Flute

- 5.2.3 C Flute

- 5.2.4 E Flute

- 5.2.5 F Flute

- 5.3 By Packaging Type

- 5.3.1 Regular Slotted Containers

- 5.3.2 Die-Cut Custom Boxes

- 5.3.3 Folding Cartons

- 5.3.4 Point-of-Purchase Displays

- 5.3.5 Pallet Boxes

- 5.3.6 Other Packaging Types

- 5.4 By Wall Type

- 5.4.1 Single-Wall

- 5.4.2 Double-Wall

- 5.4.3 Triple-Wall

- 5.4.4 Single Face

- 5.5 By Printing Technology

- 5.5.1 Flexographic Printing

- 5.5.2 Digital Inkjet Printing

- 5.5.3 Litho-Lamination

- 5.5.4 Screen Printing

- 5.5.5 Other Printing Technologies

- 5.6 By End-User Industry

- 5.6.1 Processed Foods

- 5.6.2 Fresh Food and Produce

- 5.6.3 Beverages

- 5.6.4 Electrical Products

- 5.6.5 Personal Care and Cosmetics

- 5.6.6 E-commerce Fulfillment Centers

- 5.6.7 Pharmaceuticals

- 5.6.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SCG Packaging Public Company Limited

- 6.4.2 San Miguel Yamamura Packaging Corp.

- 6.4.3 Liberty Corrugated Boxes Mfg. Corp.

- 6.4.4 Valenzuela Packaging Container Corp.

- 6.4.5 Quality Corrugated Box Manufacturing Corp.

- 6.4.6 Sunpack Container and Packaging Corp.

- 6.4.7 Prime Worldwide Paper Packaging Corp.

- 6.4.8 Steniel Graham Packaging Philippines Corp.

- 6.4.9 Malinta Corrugated Boxes Manufacturing Corp.

- 6.4.10 Basic Box Industries Corp.

- 6.4.11 Papercon Philippines Inc.

- 6.4.12 Central Corrugated Box Corp.

- 6.4.13 Duraboard Packaging Corp.

- 6.4.14 Three Dimensional Packaging Corp.

- 6.4.15 Boxworld Co Inc.

- 6.4.16 Basic Box Industries Corp.

- 6.4.17 RM Box Center

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment