|

시장보고서

상품코드

2061750

미국의 골판지 포장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Corrugated Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

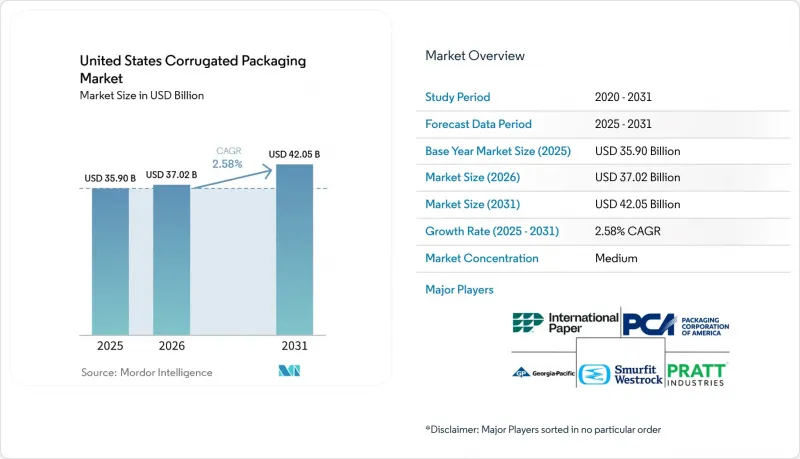

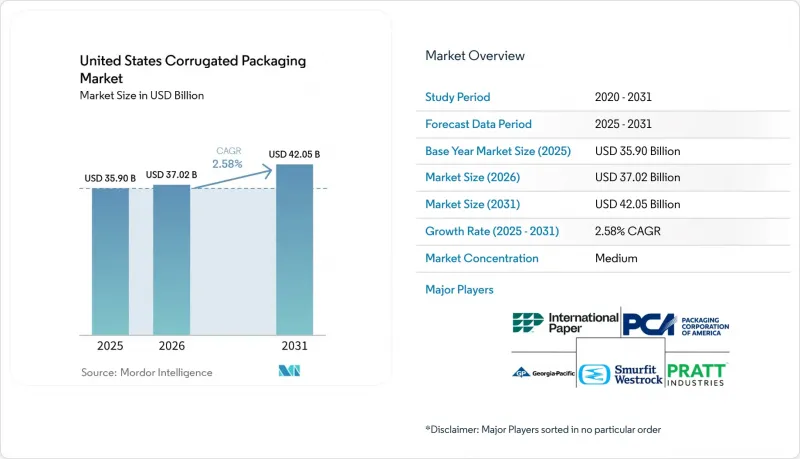

Mordor Intelligence에 의하면, 미국의 골판지 포장 시장 규모는 2025년에 359억 달러로 평가되었습니다. 2026년 370억 2,000만 달러에서 2031년까지 420억 5,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 2.58%를 나타낼 전망입니다.

본 보고서는 원재료(버진 크래프트 라이너보드, 재생 라이너보드 등), 플루트 유형(A 플루트 등), 포장 유형(일반 슬롯 컨테이너 등), 벽 구조(싱글, 더블 등), 인쇄 기술(플렉소 인쇄 등) 및 최종 사용자 산업(가공 식품 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 골판지 포장 시장 동향과 인사이트

전자상거래 주문 처리 수요의 급증

미국의 골판지 포장 시장은 가장 빠르게 성장하고 있으며, 소포 배송망을 통해 당일 배송이 보장되고 있습니다. 아마존, 월마트 및 제3자 물류 기업들은 2025년까지 5,000만 제곱피트 이상의 물류 공간을 증설했으며, 각 시설에서는 정확한 두께 공차를 충족하는 자동화 대응 상자가 필요합니다. 택배 업체의 부피 중량 요금 적용으로 인해 화주들은 적절한 크기의 포장을 요구하게 되었으며, 이에 따라 맞춤형 다이컷 포장에 대한 수요가 증가하고 있습니다. 스마핏 웨스트록의 ‘Track Vision’ 플랫폼은 2025년에 130만 개 이상의 화물을 추적하며, 디지털 트윈이 빈 차 운행을 어떻게 줄이는지 보여주었습니다. 이에 대해 인터내셔널 페이퍼사는 미국 남동부 주요 대도시권에서 1일 이내 배송이 가능한 범위를 유지하기 위해 미시시피주에 2억 2,500만 달러를 투자해 신규 공장을 건설하기로 결정했습니다. 해당 공장은 2027년 말에 가동을 시작할 예정입니다. 그 결과, 물류 처리의 집적화가 진행되면서 미국의 골판지 포장 시장에서 지역별 생산 능력이 통합되고, 리드타임이 단축되고 있습니다.

플라스틱 대체로의 전환과 순환형 경제의 의무화

캘리포니아주, 콜로라도주, 메인주, 메릴랜드주, 미네소타주, 오리건주, 버몬트주의 확대 생산자 책임(EPR) 규제는 브랜드 소유자에게 회수 및 선별 시스템에 대한 자금 조달을 의무화하고 있으며, 이는 섬유 기반 소재에 있어 정책적인 호재로 작용하고 있습니다. 캘리포니아주 상원 법안 제54호만 보더라도, 2032년까지 일회용 포장재의 재활용률을 65%로 의무화하고 있으며, 이미 71-76%의 회수율을 자랑하는 골판지 등급 소재의 선택을 뒷받침하고 있습니다. 플랫 인더스트리즈는 이러한 규제로 인한 수요를 흡수하기 위해 2025년 조지아주 워너 로빈스에 1억 2,000만 달러를 투자해 재생재 혼합 공장을 설립했습니다. 연방 의회에서 STEWARD 법안이 심의됨에 따라 전국적인 규제 통합이 진전되어, 규정 준수 비용 절감이 이루어질 가능성이 있습니다. 정책 추진력이 가속화되는 가운데, 미국의 골판지 포장 시장은 폐쇄형 섬유 인프라의 혜택을 누리고 있습니다.

크래프트 펄프 공급망의 지속적인 변동

2026년 중국의 단섬유 펄프 기준 가격은 톤당 약 570달러로 상승한 반면, 2026년 1월 미국 북부산 표백 침엽수 크라프트 펄프는 톤당 730달러 전후로 거래되었습니다. 2026년 1월, 돔타(Domtar)사가 연간 생산량 38만 톤 규모의 크로프턴 공장을 폐쇄함에 따라 조정용 생산 능력이 상실되었고, 미국의 라이너보드 공장은 더 높은 비용이 드는 스칸디나비아산 펄프를 조달할 수밖에 없게 되었습니다. 2026년 초, 북유럽에서 미국 걸프 연안 지역으로의 해상 운임은 40피트 컨테이너당 3,200달러를 넘어섰으며, 이로 인해 도착 비용이 상승했습니다. 이러한 동향은 미국의 골판지 포장 시장에서 비통합형 가공업체의 이익률을 위협하고 있으며, 수직 통합이나 장기 공급 계약 체결을 촉진하고 있습니다.

부문별 분석

2025년, 재생 라이너보드는 61.57%의 시장 점유율을 유지하며 비용 면에서의 우위를 확립했으나, 버진 크래프트 라이너보드는 연평균 성장률(CAGR) 3.03%를 기록하며 소재 시장의 성장을 주도할 것으로 전망됩니다. 화장품 및 전자기기 분야에서 인쇄 품질에 대한 요구가 높아지는 가운데, 버진 섬유가 제공하는 매끄러운 표면에 대한 수요가 증가하고 있습니다. 돔타르사의 공장 폐쇄로 인해 버진 펄프 공급이 부족해지면서 현물 가격이 톤당 730달러까지 치솟았습니다. 이 수준에서는 기존 재활용 소재와의 가격 차이가 줄어듭니다. 현재 많은 브랜드가 산림관리협의회(FSC) 인증을 요구하고 있기 때문에 재활용 섬유와 원료 섬유의 균형을 맞추고 있는 제지 업체가 계약을 따낼 가능성이 있습니다. 그 결과, 고품질 그래픽 용도가 미국의 골판지 포장 시장에 새로운 가치의 원천을 제공합니다.

순환형 경제에 관한 규제 강화는 재생 펄프 함유율이 높은 제품을 뒷받침하고 있으며, 이는 플랫 인더스트리즈가 주로 사업을 전개하고 있는 분야입니다. 그러나 화이트 탑 라이너 보드와 같은 혼합 소재도 매장 진열대에서 인기를 얻고 있습니다. 인터내셔널 페이퍼사는 이미 연간 700만 톤의 사용 후 골판지 용기를 처리하고 있으며, 이를 통해 수입 펄프에 대한 의존도를 낮추고 사내 섬유 순환 체계를 강화하고 있습니다. 그 결과 탄생한 2층 구조의 소재 생태계 덕분에, 미국의 골판지 포장 시장 전반에서 가격뿐만 아니라 성능 및 브랜딩 요건도 섬유 선정에 영향을 미치게 되었습니다.

2025년 출하량에서 C-플루트가 39.10%를 차지했으나, 가전제품 및 화장품 업계가 보호 성능을 유지하면서도 경량 포장을 요구하는 가운데, E-플루트는 2031년까지 연평균 성장률(CAGR) 4.13%를 기록하며 다른 모든 유형을 앞지를 것으로 예측됩니다. 얇은 두께는 부피 중량을 줄여주며, 로봇 포장 라인에 적합하기 때문에 E-플루트는 기능 면에서 우위를 차지합니다. 또한, 디지털 잉크젯 인쇄기는 마이크로 플루트에 더욱 선명하게 인쇄할 수 있어, 맞춤형 포장 트렌드에도 부합합니다. 깨지기 쉬운 유리 제품이나 도자기의 경우, A 플루트가 여전히 최고의 완충 성능을 제공하지만, 컨버터가 보드의 사양을 과도하게 높이는 대신 인서트를 재설계하게 되면서 그 시장 점유율은 감소하고 있습니다. 이러한 구조의 변화로 인해, 미국의 골판지 포장 시장 내에서는 혁신에 대한 압박이 계속해서 커지고 있습니다.

로봇 처리용 상자의 경우 두께를 엄격하게 관리해야 하므로, 이는 첨단 공정 모니터링 시스템을 가동하는 대규모 통합 시설에 유리하게 작용합니다. 스마핏 웨스트록(Smarfit Westlock)과 BHS 콜루게이트(BHS Corrugated)는 마이크로플루트용 골판지 제조 기계와 인쇄 라인을 최적화하여, 주요 기업들이 시장 점유율을 유지하는 데 기여하고 있습니다. 소형 시트 피더는 틈새 시장 생산에 대응할 수 있지만, 플루트 형상을 전환할 때는 더 높은 폐기 위험을 감수해야 합니다. 따라서, 얇은 골판지의 단위당 경제성을 둘러싼 경쟁이 미국의 골판지 포장 시장의 설비 투자 주기를 좌우하게 될 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the united states corrugated packaging market size was valued at USD 35.90 billion in 2025 and estimated to grow from USD 37.02 billion in 2026 to reach USD 42.05 billion by 2031, at a CAGR of 2.58% during the forecast period (2026-2031).

This report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, and More), Flute Type (A Flute, and More), Packaging Type (Regular Slotted Containers, and More), Wall Type (Single, Double, and More), Printing Technology (Flexographic, and More), and End-User Industry (Processed Foods, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Corrugated Packaging Market Trends and Insights

E-Commerce Fulfilment Demand Surge

The United States corrugated packaging market is expanding fastest, where parcel networks promise same-day delivery. Amazon, Walmart, and third-party logistics firms added more than 50 million square feet of fulfillment space in 2025, each facility requiring automation-compatible boxes that hold precise caliper tolerances. Dimensional-weight fees from parcel carriers push shippers toward right-sized packaging, which lifts demand for custom die-cut formats. Smurfit Westrock's Track Vision platform traced over 1.3 million packages in 2025 and illustrated how digital twins reduce empty-mile trucking. International Paper responded by committing USD 225 million to a greenfield plant in Mississippi, scheduled for late 2027, to stay within a one-day delivery radius of major southeastern metros. Fulfillment density is therefore reinforcing regional capacity clusters and shortening lead times across the United States corrugated packaging market.

Shift Toward Plastic Substitution And Circular Economy Mandates

Extended producer responsibility rules in California, Colorado, Maine, Maryland, Minnesota, Oregon, and Vermont require brand owners to finance collection and sorting systems, creating a policy tailwind for fiber substrates. California Senate Bill 54 alone mandates a 65% recycling rate for single-use packaging by 2032, tilting material selection toward corrugated grades, which already have a 71-76% recovery rate. Pratt Industries opened a USD 120 million recycled-content plant in Warner Robins, Georgia, in 2025 to capture demand from these mandates. Federal STEWARD Act deliberations in Congress could harmonize rules nationwide and compress compliance costs. As policy momentum accelerates, the United States corrugated packaging market benefits from its closed-loop fibre infrastructure.

Ongoing Kraft Pulp Supply Chain Volatility

China's short-fiber pulp benchmark for 2026 rose to roughly USD 570 per ton, while domestic northern bleached softwood kraft held near USD 730 per ton in January 2026. Domtar's January 2026 closure of its 380,000-ton Crofton mill removed swing capacity and forced U.S. linerboard mills to source higher-cost Scandinavian pulp. Ocean freight from Northern Europe to the Gulf Coast exceeded USD 3,200 per forty-foot container early in 2026, pushing landed costs higher. These dynamics threaten margins for non-integrated converters inside the United States corrugated packaging market and encourage vertical integration or long-term supply contracts.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Same-Day Grocery Delivery Networks

- Technological Integration Of RFID-Embedded Smart Corrugated Boxes

- Rising Energy Costs Impacting Boxboard Production Economics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled linerboard maintained 61.57% share in 2025, anchoring cost leadership, yet virgin kraft linerboard is forecast to pace material growth at a 3.03% CAGR. Print-quality requirements in cosmetics and electronics are pulling demand toward the smoother surface that virgin fiber delivers. Domtar's mill closure tightened virgin supply, nudging spot pulp toward USD 730 per ton, a level that narrows traditional recycled discounts. Many brands now specify Forest Stewardship Council certificates, so mills balancing recycled and virgin fiber can win contracts. Consequently, premium graphics applications are injecting fresh value pools into the United States corrugated packaging market.

Rising circular-economy mandates favor high recycled content, a space where Pratt Industries operates exclusively. Yet blended options such as white-top linerboard are gaining traction in point-of-purchase displays. International Paper already processes 7 million tons of old corrugated containers annually, reducing exposure to imported pulp and reinforcing internal fiber loops. The resulting two-tier material ecosystem ensures that performance and branding demands, rather than price alone, govern fiber choice across the United States corrugated packaging market.

C flute commanded 39.10% of 2025 shipments, but E flute is projected to outpace all others at a 4.13% CAGR through 2031 as consumer electronics and cosmetics seek lighter packs that remain protective. Thinner calipers cut dimensional weight and suit robotic packing lines, giving E flute a functional edge. Digital inkjet presses also print more cleanly on micro flutes, aligning with the trend toward personalized packaging. For fragile glassware and ceramics, A flute still offers the highest cushioning, yet its share is declining as converters redesign inserts rather than over-specify board. These mix shifts keep innovation pressure high within the United States corrugated packaging market.

Robot-friendly boxes need tight caliper control, which favors large integrated facilities running advanced process monitors. Smurfit Westrock and BHS Corrugated have tailored corrugators and press lines for micro flutes, helping big players defend their share. Smaller sheet feeders fill niche runs but must absorb higher scrap risk when shifting between flute profiles. The battle for unit economics at thin calipers will therefore shape equipment investment cycles across the United States corrugated packaging market.

List of Companies Covered in this Report:

- International Paper Company

- Smurfit Westrock plc

- Packaging Corporation of America

- Georgia-Pacific LLC

- Pratt Industries Inc.

- Sonoco Products Company

- Cascades Inc.

- The BoxMaker Inc.

- Mondi Group

- Jamestown Container Companies

- Graphic Packaging Holding Company

- R&R Corrugated Packaging Group

- Great Little Box Company Ltd.

- Liberty Corrugated LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce Fulfillment Demand Surge

- 4.2.2 Shift Toward Plastic Substitution and Circular Economy Mandates

- 4.2.3 Expansion of Same-Day Grocery Delivery Networks

- 4.2.4 Technological Integration of RFID-Embedded Smart Corrugated Boxes

- 4.2.5 Growth of Direct-to-Consumer Subscription Services

- 4.2.6 Accelerating Nearshoring of Manufacturing to the United States

- 4.3 Market Restraints

- 4.3.1 Ongoing Kraft Pulp Supply Chain Volatility

- 4.3.2 Rising Energy Costs Impacting Boxboard Production Economics

- 4.3.3 Increasing Adoption of Reusable Plastic Containers in Produce Supply Chains

- 4.3.4 Regulatory Pressure on Forest Stewardship Certifications

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Kraft Linerboard

- 5.1.2 Recycled Linerboard

- 5.1.3 Corrugating Medium

- 5.1.4 Semi-Chemical Fluting

- 5.1.5 Other Materials

- 5.2 By Flute Type

- 5.2.1 A Flute

- 5.2.2 B Flute

- 5.2.3 C Flute

- 5.2.4 E Flute

- 5.2.5 F Flute

- 5.3 By Packaging Type

- 5.3.1 Regular Slotted Containers

- 5.3.2 Die-Cut Custom Boxes

- 5.3.3 Folding Cartons

- 5.3.4 Point-of-Purchase Displays

- 5.3.5 Pallet Boxes

- 5.3.6 Other Packaging Types

- 5.4 By Wall Type

- 5.4.1 Single-Wall

- 5.4.2 Double-Wall

- 5.4.3 Triple-Wall

- 5.4.4 Single Face

- 5.5 By Printing Technology

- 5.5.1 Flexographic Printing

- 5.5.2 Digital Inkjet Printing

- 5.5.3 Litho-Lamination

- 5.5.4 Screen Printing

- 5.5.5 Other Printing Technologies

- 5.6 By End-User Industry

- 5.6.1 Processed Foods

- 5.6.2 Fresh Food and Produce

- 5.6.3 Beverages

- 5.6.4 Paper Products

- 5.6.5 Electrical Products

- 5.6.6 Personal Care and Cosmetics

- 5.6.7 E-commerce Fulfillment Centers

- 5.6.8 Pharmaceuticals

- 5.6.9 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 International Paper Company

- 6.4.2 Smurfit Westrock plc

- 6.4.3 Packaging Corporation of America

- 6.4.4 Georgia-Pacific LLC

- 6.4.5 Pratt Industries Inc.

- 6.4.6 Sonoco Products Company

- 6.4.7 Cascades Inc.

- 6.4.8 The BoxMaker Inc.

- 6.4.9 Mondi Group

- 6.4.10 Jamestown Container Companies

- 6.4.11 Graphic Packaging Holding Company

- 6.4.12 R&R Corrugated Packaging Group

- 6.4.13 Great Little Box Company Ltd.

- 6.4.14 Liberty Corrugated LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment