|

시장보고서

상품코드

2061752

아시아태평양의 IT 디바이스 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Asia-Pacific IT Device - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

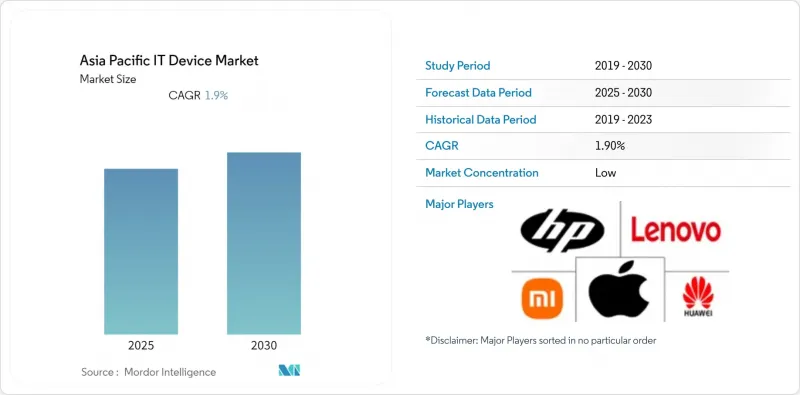

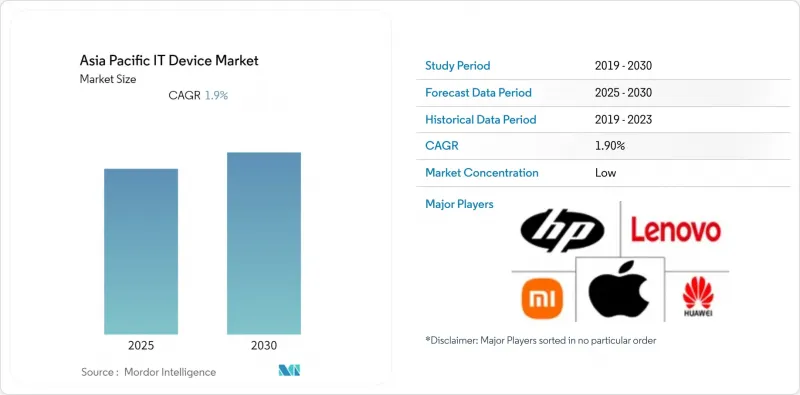

Mordor Intelligence에 의하면, 아시아태평양의 IT 디바이스 시장 규모는 2025년 7,200억 달러로 평가되었고, 2026년에는 7,900억 달러로 추정되고, 2026-2031년 CAGR 8.73%로 성장을 지속할 전망이며, 2031년까지 1조 2,100억 달러에 이를 것으로 예측됩니다.

본 보고서는 디바이스 유형별(스마트폰, 태블릿, 노트북, 데스크톱 및 워크스테이션, 웨어러블, PC 모니터 및 주변기기), 최종 사용자 산업별(소비자, 기타), 연결 기술별(5G 지원, 4G/LTE, Wi-Fi 전용, 유선), 유통 채널별(오프라인 소매, 온라인 소매, 기타) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

아시아태평양의 IT 디바이스 시장 동향 및 인사이트

5G 인프라의 급속한 확산이 기기 교체 주기를 앞당기고 있습니다.

2025년 12월까지 말레이시아 인구의 80% 이상이 독립형 5G 통신 서비스 범위에 포함될 예정이며, 이에 따라 물류 및 제조 기업들은 실시간 경로 설정과 창고 자동화를 가능하게 하는 5G 태블릿으로 4G 휴대용 단말기를 교체하고 있습니다. 인도의 주요 통신사는 독립형 5G 서비스를 300개 도시로 확대하고 네트워크 지연 시간을 10밀리초 미만으로 단축함으로써, 중급형 스마트폰에서도 클라우드 게임과 산업용 IoT를 이용할 수 있게 되었습니다. 태국과 필리핀의 통신사들은 현재 5G 요금제에 단말기 할부 요금제를 묶어 판매하고 있으며, 이로 인해 단말기 교체 주기가 단축되고 있습니다. IMT-2020 규격에서는 하위 호환성이 유지되고 있지만, 기업 측에서는 4G 칩셋으로는 네트워크 슬라이싱 정책에 따른 패킷 검사 오버헤드를 감당할 수 없어, 2023년에 막 구입한 단말기조차 조기에 구식이 되어버린다는 사실이 밝혀졌습니다. 가장 큰 혜택을 보고 있는 분야는 미션 크리티컬한 워크로드에 대해 서비스 품질을 보장해야 하는 의료 및 제조업 분야입니다.

소비자용 전자기기에서의 새로운 온디바이스 AI 활용 사례

인도, 인도네시아, 베트남의 데이터 현지화 법은 생체 인식 데이터 및 금융 데이터의 국경 간 전송을 금지하고 있어, 각 OEM 기업들은 추론 워크로드를 엣지 측으로 이전할 수밖에 없는 상황입니다. 2026년에 출시될 플래그십 스마트폰은 70억 파라미터 규모의 언어 모델을 로컬에서 실행하여, 클라우드를 호출하지 않고도 실시간 번역, 회의 녹취, 개인정보 보호형 음성 비서 기능을 구현합니다. 삼성은 2026년 중 8억 대의 기기에 갤럭시 AI를 사전 설치할 전망이며, 생산성 향상용 애드온을 위한 프리미엄 구독 서비스를 통해 수익 창출을 확대할 계획입니다. 자동차 제조업체들은 인포테인먼트용으로 맞춤형 AI 칩셋을 채택하고 있으며, 이는 기기 내 지능이 기존의 컴퓨팅 형태를 뛰어넘을 것임을 시사합니다. 전용 신경망 엔진은 저가형 모델에서 CPU에 의존하는 추론 방식에 비해 낮은 지연 시간과 뛰어난 배터리 수명을 실현하기 때문에 프리미엄급 제품군에서는 30-40%의 가격 인상이 예상됩니다.

반도체 공급망의 변동

2026년 초, 고대역폭 메모리가 AI 가속기용으로 전용된 결과, DRAM 현물 가격은 전 분기 대비 90-95% 급등했고, NAND 가격은 55-60% 상승했습니다. 현재 소비자용 노트북이나 보급형 태블릿의 경우, LPDDR5 모듈의 리드타임이 16-20주에 달하고 있어, 제품 출시가 지연되거나 배터리 사용 시간을 희생해야 하는 구형 메모리를 사용한 부품 목록을 재설계할 수밖에 없는 상황입니다. 각 PC OEM 업체들은 2차 공급업체로부터의 조달을 검토하고 있지만, 이로 인해 성능 검증 및 지정학적 우려가 커지고 있습니다. Realme와 Honor를 비롯한 중견 스마트폰 브랜드들은 장기적인 공급을 확보할 만한 구매력이 부족하여, 300달러 미만 가격대에서 이미 낮은 이익률을 더욱 압박하고 있습니다. 메모리 시장은 역사적으로 주기적인 변동을 거듭해 왔으며, 2027년까지 공급 과잉으로 전환될 가능성이 있기 때문에 파운드리 각사는 생산 능력 확충에 신중한 태도를 유지하고 있습니다.

부문별 분석

웨어러블 기기는 2031년까지 연평균 성장률(CAGR) 9.93%를 나타낼 것으로 예측되지만, 2025년 기준 아시아태평양의 IT 디바이스 시장 점유율 중 스마트폰이 48.43%를 차지했습니다. 이 부문의 성장은 심전도(ECG), 혈중 산소 포화도, 연속 혈당 모니터링 등의 건강 모니터링 기능에 힘입어 이루어지고 있으며, 일본, 한국, 싱가포르에서는 이러한 기능을 이용하면 보험료를 10-15% 할인해 주는 제도가 도입되어 있습니다. 또한, 바코드 스캐너와 열화상 카메라를 탑재한 내환경형 웨어러블 단말기는 물류 업무에서 기존의 핸드헬드 단말기를 점차 대체하고 있으며, 기업 사용자들 수요 증가를 주도하고 있습니다. 태블릿은 인도와 인도네시아가 교육 프로그램을 위해 단말기를 배포함에 따라 2025년에 두 자릿수의 출하 성장률을 기록했으나, 그 수량은 여전히 재정 주기의 영향을 받기 쉬운 상황입니다. 노트북 시장은 2025년 10월 Windows 10 지원 종료에 앞서 기업용 업그레이드 수요가 급증한 반면, 메모리 가격 급등으로 인해 대당 50-80달러의 비용 증가가 발생하면서 소비자 수요는 주춤하는 등 복잡한 양상을 보였습니다. 데스크톱 PC와 워크스테이션은 CAD 설계나 알고리즘 트레이딩와 같은 틈새 용도로 사용되고 있으며, 사용자들은 멀티코어 CPU나 디스크리트 GPU에 대해 상대적으로 높은 가격을 지불하고 있습니다.

현재 스마트폰의 차별화는 소프트웨어 중심으로 이루어지고 있으며, 생성형 AI 어시스턴트와 연방 학습 플랫폼이 개인정보를 침해하지 않으면서 사용자 경험을 향상시키고 있습니다. 레노버의 크로스 디바이스 어시스턴트는 노트북, 태블릿, 스마트폰 간에 작업을 동기화하여 폼 팩터를 초월한 융합을 입증하고 있습니다. 스마트폰의 매출총이익률이 20-25%인 반면, 40-50%의 매출총이익률을 자랑하는 히어러블 및 스마트 링은 웨어러블 제품군을 확대하고 수익원을 다각화하고 있습니다. 물류 분야의 내환경형 핸드헬드 단말기 아시아태평양 IT 디바이스 시장은 현재 규모는 작지만, 5G 연결과 엣지 AI로 인해 기존 Windows CE 단말기에 대한 의존도가 낮아짐에 따라 급속히 확대되고 있습니다.

기업 구매자 시장은 연평균 성장률(CAGR) 9.53%로 확대될 것으로 예상되며, 소비자와의 격차는 줄어들 것으로 보입니다. 소비자는 2025년 매출의 67.14%를 차지했으나, 현재는 업그레이드 빈도가 줄어들고 있습니다. 하이브리드 근무 모델에서는 제로 트러스트 보안 기준을 충족하기 위해 하드웨어 루트 오브 트러스트(HRT) 기능을 갖춘 노트북이 필요하며, 금융, 의료, 기술 등 각 업계에서 기기 교체 작업이 진행되고 있습니다. Device-as-a-Service(DaaS) 서비스는 하드웨어, 소프트웨어, 지원을 운영 비용(OPEX) 부담이 적은 구독 형식으로 제공하여, 대량 구매를 통한 할인 혜택을 받을 만한 규모가 없는 중소기업의 관심을 끌고 있습니다. 교육 분야의 조달 규모는 2025년 인도네시아 교육부가 150만 대의 태블릿을 도입하면서 급증했으나, 2027년 예산은 불투명합니다.

정부 기관은 에너지 효율 및 재활용 가능성에 관한 지표를 조달 요건에 명시하고 있으며, 이에 따라 규정 준수 체계가 잘 갖춰진 대형 OEM 업체에 유리한 조달 기준이 마련되어 있습니다. 일부 아세안 시장에서는 중소기업들이 여전히 기술 도입에 뒤처져 있지만, 2025년 조사 결과 75%가 새로운 디지털 결제 수단을 도입한 것으로 나타나, 하드웨어 수요를 견인하는 광범위한 디지털화가 진행되고 있음을 시사합니다. Windows 11의 하드웨어 사양과 AI 코프로세서가 표준화됨에 따라, 아시아태평양의 기업용 노트북 시장은 꾸준히 확대될 것으로 예측됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the asia-Pacific iT device market size is expected to grow from USD 0.72 trillion in 2025 to USD 0.79 trillion in 2026 and is forecast to reach USD 1.21 trillion by 2031 at an 8.73% CAGR over 2026-2031.

This report is Segmented by Device Type (Smartphones, Tablets, Laptops and Notebooks, Desktops and Workstations, Wearables, and PC Monitors and Peripherals), End-User Industry (Consumer, and More), Connectivity Technology (5G Enabled, 4G/LTE, Wi-Fi Only, and Wired), Distribution Channel (Offline Retail, Online Retail, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific IT Device Market Trends and Insights

Rapid 5G Infrastructure Roll-out Accelerating Device Refresh Cycles

Standalone 5G coverage surpassed 80% of Malaysia's population by December 2025, prompting logistics and manufacturing firms to replace 4G handhelds with 5G tablets that enable real-time routing and warehouse automation. India's leading operator extended standalone 5G to 300 cities, cutting network latency below 10 milliseconds, making cloud gaming and industrial IoT viable on mid-tier smartphones. Operators in Thailand and the Philippines now bundle 5G plans with device-financing offers, shortening replacement intervals. Although IMT-2020 rules retain backward compatibility, enterprises find that 4G chipsets cannot sustain the packet inspection overhead of network slicing policies, leading to the accelerated obsolescence of devices bought as recently as 2023. The largest gains are occurring in healthcare and manufacturing verticals that require guaranteed quality of service for mission-critical workloads.

Emerging AI-On-Device Use-Cases in Consumer Electronics

Data-localization laws in India, Indonesia, and Vietnam bar cross-border transfer of biometric and financial data, driving OEMs to shift inference workloads to the edge. Flagship smartphones launched in 2026 are running 7-billion-parameter language models locally, enabling real-time translation, meeting transcription, and privacy-preserving voice assistance without cloud calls. Samsung expects to preload Galaxy AI on 800 million devices during 2026, expanding monetization through premium subscriptions for productivity add-ons. Automotive OEMs are adopting custom AI chipsets for infotainment, signaling that on-device intelligence will transcend traditional computing form factors. The premium tier commands a 30-40% price uplift, as dedicated neural engines deliver lower latency and better battery life compared to CPU-bound inference on budget models.

Semiconductor Supply Chain Volatility

DRAM spot prices jumped 90-95% quarter-on-quarter in early 2026, and NAND prices rose 55-60%, as high-bandwidth memory was diverted to AI accelerators. Consumer laptops and entry-level tablets now face 16-20-week lead times for LPDDR5 modules, delaying product launches or forcing bill-of-materials redesigns around older memory that compromises battery life. PC OEMs have explored sourcing from second-tier suppliers, raising performance-validation and geopolitical concerns. Realme, Honor, and other mid-tier smartphone brands lack the purchasing clout to lock in long-term supply, squeezing already-thin margins in the sub-USD 300 bracket. Foundries remain cautious about adding capacity because the memory market is historically cyclical and could swing to oversupply by 2027.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Local Electronics Manufacturing

- Growing BYOD Adoption in Small and Medium Enterprises

- Intensifying Regulatory Scrutiny on E-waste Management

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wearables are projected to post a 9.93% CAGR through 2031, while smartphones retained 48.43% of the Asia-Pacific IT device market share in 2025. The segment's rise is driven by health-monitoring functions such as ECG, blood-oxygen saturation, and continuous glucose monitoring that qualify users for 10-15% insurance premium discounts in Japan, South Korea, and Singapore. Ruggedized wearables equipped with barcode scanners and thermal cameras are also replacing legacy handhelds in logistics operations, capturing incremental demand from enterprise buyers. Tablets recorded double-digit shipment growth in 2025 as India and Indonesia distributed devices for education programs, yet volumes remain susceptible to fiscal cycles. Laptops experienced mixed dynamics, such as corporate upgrades surged ahead of Windows 10's end-of-support in October 2025, but consumer demand slowed due to memory price inflation, which added USD 50-80 per unit. Desktops and workstations serve niche applications such as CAD design and algorithmic trading, where users pay premiums for multi-core CPUs and discrete GPUs.

Smartphone differentiation is now software-led, with generative AI assistants and federated learning platforms augmenting the user experience without compromising privacy. Lenovo's cross-device assistant synchronizes tasks between laptops, tablets, and phones, demonstrating convergence across form factors. Hearables and smart rings, which carry 40-50% gross margins versus 20-25% for smartphones, extend the wearables family and diversify revenue streams. The Asia-Pacific IT device market for rugged handhelds in logistics is small today but expanding rapidly as 5G connectivity and edge AI reduce reliance on legacy Windows CE terminals.

Enterprise buyers are forecast to expand at a 9.53% CAGR, narrowing the gap with consumers, who generated 67.14% of 2025 revenue but now upgrade less frequently. Hybrid work models require laptops with hardware root-of-trust (HRT) features to meet zero-trust security standards, prompting fleet renewals across finance, healthcare, and technology verticals. Device-as-a-service offerings bundle hardware, software, and support into opex-friendly subscriptions, attracting SMEs that lack scale for volume discounts. Education procurements spiked in 2025 when Indonesia's Ministry of Education deployed 1.5 million tablets, though funding for 2027 is uncertain.

Government agencies specify energy-efficiency and recyclability metrics, adding procurement hurdles that favor established OEMs with mature compliance processes. SMEs remain technology laggards in some ASEAN markets, yet a 2025 survey showed 75% adopting new digital-payment tools, signaling broader digitization that will lift hardware demand. The Asia-Pacific IT device market for enterprise laptops is expected to expand steadily as Windows 11 hardware baselines and AI co-processors become standard.

List of Companies Covered in this Report:

- Samsung Electronics Co., Ltd.

- Apple Inc.

- Huawei Technologies Co., Ltd.

- Xiaomi Corporation

- Lenovo Group Limited

- OPPO Guangdong Mobile Telecommunications Corp., Ltd.

- Vivo Mobile Communication Co., Ltd.

- ASUSTeK Computer Inc.

- Acer Inc.

- Dell Technologies Inc.

- HP Inc.

- Sony Group Corporation

- Panasonic Holdings Corporation

- LG Electronics Inc.

- Toshiba Corporation

- Fujitsu Limited

- NEC Corporation

- Transsion Holdings

- Realme Chongqing Mobile Telecommunications Corp. Ltd.

- HONOR Device Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid 5G Infrastructure Roll-out Accelerating Device Refresh Cycles

- 4.2.2 Growing BYOD Adoption in Small and Medium Enterprises

- 4.2.3 Expanding E-commerce Penetration for Electronics in Tier-2 and Tier-3 Cities

- 4.2.4 Government Incentives for Local Electronics Manufacturing

- 4.2.5 Emerging AI-On-Device Use-Cases in Consumer Electronics

- 4.2.6 Gamification and Esports Fueling Demand for High-Performance Devices

- 4.3 Market Restraints

- 4.3.1 Semiconductor Supply Chain Volatility

- 4.3.2 Intensifying Regulatory Scrutiny on E-waste Management

- 4.3.3 Currency Fluctuations Impacting Import-Dependent OEMs

- 4.3.4 Saturation of Premium Smartphone Segment in Urban Hubs

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Type

- 5.1.1 Smartphones

- 5.1.2 Tablets

- 5.1.3 Laptops and Notebooks

- 5.1.4 Desktops and Workstations

- 5.1.5 Wearables

- 5.1.6 PC Monitors and Peripherals

- 5.2 By End-User Industry

- 5.2.1 Consumer

- 5.2.2 Enterprise

- 5.2.3 Government and Public Sector

- 5.2.4 Education

- 5.3 By Connectivity Technology

- 5.3.1 5G Enabled

- 5.3.2 4G/LTE

- 5.3.3 Wi-Fi Only

- 5.3.4 Wired

- 5.4 By Distribution Channel

- 5.4.1 Offline Retail

- 5.4.2 Online Retail

- 5.4.3 Enterprise Direct Sales

- 5.4.4 Value-Added Resellers

- 5.5 By Geography

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 India

- 5.5.4 South Korea

- 5.5.5 Australia and New Zealand

- 5.5.6 Rest of Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Samsung Electronics Co., Ltd.

- 6.4.2 Apple Inc.

- 6.4.3 Huawei Technologies Co., Ltd.

- 6.4.4 Xiaomi Corporation

- 6.4.5 Lenovo Group Limited

- 6.4.6 OPPO Guangdong Mobile Telecommunications Corp., Ltd.

- 6.4.7 Vivo Mobile Communication Co., Ltd.

- 6.4.8 ASUSTeK Computer Inc.

- 6.4.9 Acer Inc.

- 6.4.10 Dell Technologies Inc.

- 6.4.11 HP Inc.

- 6.4.12 Sony Group Corporation

- 6.4.13 Panasonic Holdings Corporation

- 6.4.14 LG Electronics Inc.

- 6.4.15 Toshiba Corporation

- 6.4.16 Fujitsu Limited

- 6.4.17 NEC Corporation

- 6.4.18 Transsion Holdings

- 6.4.19 Realme Chongqing Mobile Telecommunications Corp. Ltd.

- 6.4.20 HONOR Device Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment