|

시장보고서

상품코드

2062049

미국의 화학제품 창고 및 보관 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Chemical Warehousing And Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

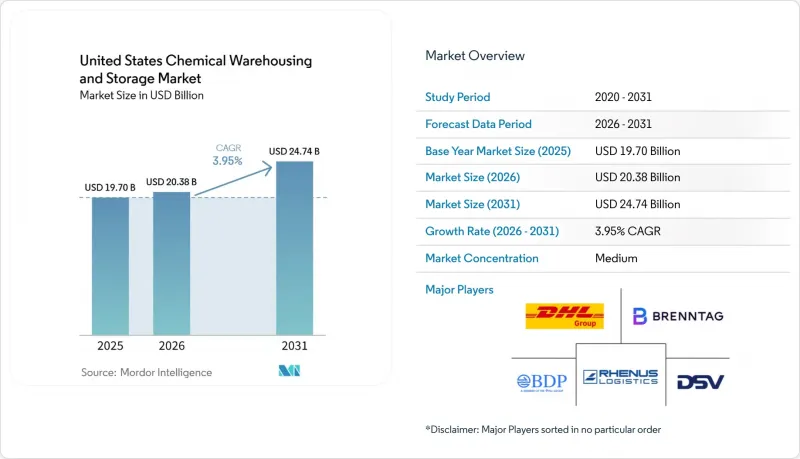

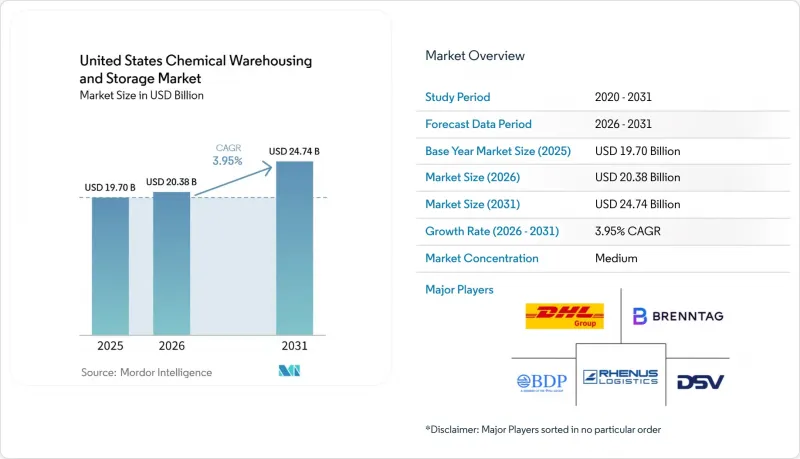

Mordor Intelligence에 의하면, 미국의 화학제품 창고 및 보관 시장 규모는 2025년 197억 달러로 평가되었고, 2026년에는 203억 8,000만 달러로 추정되고, 2031년까지 247억 4,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 3.95%로 성장할 전망입니다.

본 보고서는 창고 유형별(일반 창고, 특수 화학제품 창고 등), 화학 물질 유형별(인화성 액체, 부식성 물질 등), 최종 사용자 산업별(기초 화학제품 제조, 특수 화학제품 제조 등) 및 지역별(북동부, 중서부 등)로 분류되어 있습니다. 시장 전망은 금액 기준으로 제시되어 있습니다.

미국의 화학제품 창고 및 보관 시장 동향과 인사이트

셰일가스 붐과 석유화학 산업의 부흥

신규 및 계획 중인 멕시코만 연안 크래커 시설은 생산 거점 및 수출 회랑 인근의 위험물 대응 보관 시설에 대한 수년간 수요를 뒷받침하고 있습니다. 이바빌 패리시에 건설 중인 Shintech사의 34억 달러 규모 에틸렌 염소알칼리 복합 단지는 2030년 완공을 목표로 하고 있으며, 루이지애나주의 원료 공급을 바탕으로 한 지속적인 생산 능력 확대를 시사하고 있습니다. 엑슨모빌은 코퍼스크리스티 인근에 에탄 크래커 및 폴리에틸렌 공장을 건설하는 방안을 검토 중이며, 이에 필요한 자본 투자 규모는 최대 86억 달러에 달할 전망입니다. 이 안건이 승인되면, 폴리머 및 중간 제품의 생산 설비 확충에 따른 일시적 보관 수요가 확대되어, 추가적인 수요를 견인하는 요인이 될 것입니다. 벤처 월드(Venture World)는 캐머런 패리시(Cameron Parish)에서 진행될 86억 달러 규모의 CP2 프로젝트를 승인했으며, 한편 셰니에르(Cheniere)는 코퍼스 크리스티(Corpus Christi)에 4개의 생산 라인을 추가하는 신청을 제출하여, 이로 인해 최대 생산 능력이 연간 2,400만 톤 증가하게 됩니다. 이러한 에너지 메가 프로젝트에서는 냉매, 부식 방지제, 특수 공정용 화학 약품을 엄격한 분리 관리 하에 인접한 장소에 보관하고, 실시간으로 재고를 추적해야 합니다. 수출 물류가 이러한 사이클을 뒷받침하고 있으며, 에너지 트랜스퍼(Energy Transfer)의 플렉스포트(Flexport)와 엔터프라이즈 프로덕츠 파트너스(Enterprise Products Partners)의 확장 계획이 네덜란드 및 휴스턴 선박 운하 주변의 가동률과 적기 재고 전략을 형성하고 있습니다.

화학제품의 니어쇼어링과 리쇼어링

의약품 및 특수 화학제품에 대한 투자로 인해, 미국 생산 라인과 가까운 곳에 위치한 온도 조절 보관 시설과 검증된 품질 시스템에 대한 수요가 증가하고 있습니다. 대형 제약사가 발표한 사업 계획에서는 유효 성분(API) 및 주사제의 생산 능력 확대가 강조되고 있으며, 이를 위해서는 GDP(의약품 유통 관리 기준)에 부합하는 창고 보관 및 21 CFR Part 11을 준수하는 모니터링이 필수적입니다. 유통업체들의 투자도 이러한 변화를 반영하고 있으며, Cencora사는 2030년까지 전미의 허브 거점에 10억 달러를 투자하겠다고 약속했습니다. 여기에는 서부 해안 지역의 사업 확장 및 앨라배마주 도슨의 콜드체인 시설 확충이 포함되며, 섭씨 2-8도에서 보관해야 하는 제품 증가에 대응하기 위한 조치입니다. 네트워크 통합은 리쇼어링을 촉진하고 있으며, DSV는 2025년에 DB 쉔커 인수를 완료하여 지역 간 물류망의 확장과 표준화를 강화했습니다. 지역 사업자들은 액체 벌크 자산의 처리 시간을 단축하기 위해 항만에서의 트레일러 세척 및 유지보수 등 부가가치 서비스를 추가하고 있으며, 니어쇼어링이 확대되는 가운데 미국의 화학제품 창고 및 보관 시장을 강화하고 있습니다.

위험물 처리 시설에 대한 막대한 설비 투자

위험물 전용 창고의 개보수나 신축에는 120분 내화 구조, 격리된 누출 방지 구역, 거품 소화 시스템 및 증기 제어 시스템 등 막대한 자본 투자가 필요합니다. 또한, 사업자들은 2026년 1월까지 물질에 대한 규정 준수, 2027년 7월까지 혼합물에 대한 규정 준수를 의무화하는 OSHA의 2024년 최종 규정에 부합하기 위해, 유해물질 정보 전달 및 안전 데이터 시트(SDS)를 업데이트하고 있습니다. 경제적 영향 평가에 따르면, 일부 표시 변경으로 인해 지속적인 규정 준수 부담은 줄어들겠지만, 문서 및 라벨 수정과 교육에는 일시적인 비용이 발생합니다. e-매니페스트의 활용 및 기록 보관을 포함한 주 및 연방 차원의 프로세스 변경으로 인해 시스템과 워크플로우에 새로운 업무 프로세스가 추가되었으며, 많은 사업장에서는 이를 품질 관리 및 창고 관리 시스템(WMS) 용도과 통합하고 있습니다. 저장 실무는 EPA의 2차 봉쇄 요건을 충족해야 하며, 누출이나 빗물에 대응할 수 있는 충분한 용량과 적합한 재질이 요구됩니다. 이로 인해 시설의 배치나 설비 투자 계획에 영향을 미치게 됩니다. 이러한 의무 사항들은 미국 화학물질 창고 및 보관 시장에서 규정 준수를 철저히 이행하는 시설에 대해 프리미엄 가격 책정을 촉진하고 있습니다. 이 시장에서는 보험 가입 및 고객 감사를 위해 문서화된 안전 기록과 검사 로그가 필수적입니다.

부문별 분석

2025년에는 특수 화학제품 창고가 34.12%로 1위를 차지했습니다. 이는 내화벽, 분리된 누출 방지 구역, 본질 안전형 설비를 갖춘 전용 시설을 반영한 것으로, 이를 통해 규정 준수를 유지하면서 가연성 물질, 부식성 물질, 산화제를 단일 현장에서 관리할 수 있게 됩니다. 온도 관리형 창고는 생명과학 분야 제품 출시 시 검증된 냉각 장치, 이중화 전원 공급 장치 및 21 CFR Part 11을 준수하는 데이터 로거가 요구되기 때문에 2031년까지 연평균 성장률(CAGR) 4.8%로 가장 높은 성장이 예상됩니다. DHL이 앰빌에 건설한 100만 평방피트 규모의 헬스케어 허브는 GDP 및 GMP 기준을 준수하는 관리 체계를 갖추고 있으며, 자유무역지역(FTZ) 지위를 보유하고 있어, 시간적 제약이 있는 의약품 물류에 맞추어 통관 및 관세 절차를 최적화할 수 있도록 설계되었습니다. 안전성, 품질, 콜드체인의 신뢰성을 모두 갖춘 시설은 미국 화학제품 창고 및 보관 시장에서 일반 산업용 수준을 상회하는 임대료 프리미엄을 유지하고 있습니다.

전체 사업장 내 위험물 창고에서는 강화된 환기 및 누출 방지 대책, 2차 봉쇄 계획에 더해, 호환성을 고려한 보관 및 정기적인 훈련이 병행되고 있습니다. 공유 시설에서의 일반적인 화학물질 보관은 여전히 비위험물 제품 및 완제품의 보관을 담당하고 있지만, 가장 빠른 성장세를 보이고 있는 분야는 자동화와 감사 대응이 가능한 문서화를 결합한 온도 관리 환경입니다. 최근 프로젝트로는 AI 탑재 로봇과 새로운 WMS를 활용하여 정시 배송 실적을 유지하면서 냉장 용량을 확대한 EVERSANA사의 멤피스 물류 센터 등을 들 수 있습니다. 이러한 추세로 인해 미국의 화학제품 창고 및 보관 업계에서는 위험물 관리 및 품질 시스템을 대규모로 표준화할 수 있는 멀티 클라이언트 거점에 대한 수요가 집중되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the united states chemical warehousing and storage market size is expected to increase from USD 19.70 billion in 2025 to USD 20.38 billion in 2026 and reach USD 24.74 billion by 2031, growing at a CAGR of 3.95% over 2026-2031.

This report is Segmented by Warehouse Type (General Warehousing, Speciality Chemical Warehouse, and More), by Chemical Type (Flammable Liquids, Corrosives, and More), by End-User Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, and More), and by Regions (Northeast, Midwest, and More). The Market Forecasts are Provided in Terms of Value (USD Billion).

United States Chemical Warehousing And Storage Market Trends and Insights

Shale Gas Boom and Petrochemical Renaissance

New and proposed Gulf Coast crackers anchor multi-year demand for hazmat-compliant storage near production centers and export corridors. Shintech's USD 3.4 billion ethylene and chlor-alkali complex in Iberville Parish targets 2030 completion, and signals sustained feedstock-backed capacity growth in Louisiana. ExxonMobil is evaluating an ethane cracker and polyethylene plant near Corpus Christi with a potential USD 8.6 billion capital plan, which, if approved, would expand staging needs for polymers and intermediates buildouts add further pull. Venture Global approved the USD 8.6 billion CP2 project in Cameron Parish, while Cheniere filed to add four Corpus Christi trains that would lift peak capacity by 24 mtpa. These energy megaprojects require adjacent storage of refrigerants, corrosion inhibitors, and specialty process chemicals under strict segregation with real-time inventory tracking. Export logistics reinforce the cycle, as Energy Transfer's Flexport and Enterprise Products Partners' expansions shape occupancy and just-in-time inventory strategies near Nederland and the Houston Ship Channel.

Nearshoring and Reshoring of Chemical Manufacturing

Pharmaceutical and specialty chemical investments increase demand for temperature-controlled storage and validated quality systems close to the United States manufacturing lines. Corporate plans disclosed by leading pharma manufacturers highlight expanded active pharmaceutical ingredients and injectable therapy capacity that will rely on GDP-compliant warehousing and 21 CFR Part 11-validated monitoring. Distributor investments mirror this shift, as Cencora committed USD 1 billion through 2030 across national hubs, including a West Coast expansion and a cold-chain scale-up at Dothan, Alabama, to meet the rise in products that need 2-to-8 degree Celsius storage. Network consolidation also supports reshoring, with DSV completing the DB Schenker acquisition in 2025, enhancing cross-regional warehousing reach and standardization. Regional operators add value-added services such as trailer wash and maintenance at ports to reduce cycle times for liquid-bulk assets, reinforcing the United States chemical warehousing and storage market as nearshoring advances.

High Capital Investment for Hazmat-Compliant Facilities

Upgrading or building hazmat-ready warehouses requires significant capital for 120-minute fire-rated construction, segregated bunded zones, and foam-deluge and vapor-control systems. Operators are also updating hazard communication and safety data sheets to align with OSHA's 2024 final rule, which sets substance compliance by January 2026 and mixture compliance by July 2027. Economic impact assessments indicate one-time costs for file and label revisions and training, even as certain labeling changes reduce recurring compliance burdens. State and federal process changes, including e-Manifest use and record retention, add system and workflow workstreams that many sites integrate with quality management and WMS applications. Storage practices must meet EPA secondary-containment expectations, with adequate capacity and compatible materials for spills and stormwater, which drives site layout and capex plans. These obligations reinforce premium pricing for compliant sites in the United States chemical warehousing and storage market, where documented safety and inspection logs are essential for insurability and customer audits.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Gulf Coast Petrochemical Export Terminals

- Rising Specialty Chemicals Production Volumes

- Acute Shortage of Trained Hazardous Material Handlers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Specialty chemical warehouses led with 34.12% in 2025, reflecting purpose-built facilities with rated fire walls, segregated bunded zones, and intrinsically safe handling that allow flammables, corrosives, and oxidizers to be managed in a single site while maintaining compliance. Temperature-controlled warehouses post the fastest growth at a projected 4.8% CAGR to 2031 as life sciences launches require validated chillers, redundant power, and 21 CFR Part 11-validated data loggers. DHL's million-square-foot healthcare hub in Annville is designed with GDP and GMP controls and Foreign Trade Zone status to align customs and tariff processes with time-sensitive pharma flows. Facilities that can blend safety, quality, and cold-chain reliability sustain rent premiums that exceed general industrial levels in the United States chemical warehousing and storage market.

Across the base, hazardous material warehouses combine enhanced ventilation, spill containment, and secondary containment plans with compatibility-controlled storage and routine drills. General chemical storage in shared sites continues to serve non-hazmat products and finished goods, but the fastest growth sits in temperature-controlled settings that pair automation with audit-ready documentation. Recent projects include EVERSANA's Memphis distribution center using AI-enabled robotics and a new WMS to expand cold capacity while sustaining on-time delivery metrics. These patterns consolidate demand around multi-client nodes that can standardize hazard controls and quality systems at scale for the United States chemical warehousing and storage industry.

List of Companies Covered in this Report:

- DHL Group

- Brenntag North America

- Rhenus Logistics

- BDP International

- DSV

- C.H. Robinson

- XPO Logistics

- HOYER Group

- ADLI Logistics

- CEVA Logistics

- Quantix Supply Chain

- R&S Logistics

- Talke Logistics

- Hellmann Worldwide Logistics

- Yusen Logistics (part of NYK Line)

- Bertschi AG

- Kuehne + Nagel

- Den Hartogh Logistics

- Weber Hazmat Logistics

- Odyssey Logistics & Technology Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shale Gas Boom and Petrochemical Renaissance

- 4.2.2 Nearshoring and Reshoring of Chemical Manufacturing

- 4.2.3 Expansion of Gulf Coast Petrochemical Export Terminals

- 4.2.4 Rising Specialty Chemicals Production Volumes

- 4.2.5 Outsourcing Trend Among Chemical Manufacturers

- 4.2.6 Growing Cross-Border Chemical Trade with Mexico and Canada

- 4.3 Market Restraints

- 4.3.1 High Capital Investment for Hazmat-Compliant Facilities

- 4.3.2 Acute Shortage of Trained Hazardous Material Handlers

- 4.3.3 Escalating Insurance and Liability Premiums

- 4.3.4 Land Scarcity Near Major Port and Rail Terminals

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Automation Integration in Chemical Inventory Management

- 4.9 Shift Toward Multi-Client Shared Chemical Storage Models

5 Market Size & Growth Forecasts (Value, USD Billion)

- 5.1 By Warehouse Type

- 5.1.1 General Warehousing

- 5.1.2 Speciality Chemical Warehouse

- 5.1.3 Hazardous Materials (HAZMAT) Warehouses

- 5.1.4 Temperature-Controlled Chemical Warehouses

- 5.2 By Chemical Type

- 5.2.1 Flammable Liquids

- 5.2.2 Corrosives

- 5.2.3 Toxic Substances

- 5.2.4 Oxidizers

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Basic Chemicals Manufacturing

- 5.3.2 Specialty Chemicals Manufacturing

- 5.3.3 Pharmaceuticals & Life Sciences

- 5.3.4 Agrochemicals

- 5.3.5 Paints, Coatings & Adhesives

- 5.3.6 Food & Feed Additives

- 5.3.7 Oil & Gas / Petrochemicals

- 5.3.8 Others

- 5.4 By Region - United States

- 5.4.1 Northeast

- 5.4.2 Midwest

- 5.4.3 Southeast

- 5.4.4 Southwest

- 5.4.5 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 Brenntag North America

- 6.4.3 Rhenus Logistics

- 6.4.4 BDP International

- 6.4.5 DSV

- 6.4.6 C.H. Robinson

- 6.4.7 XPO Logistics

- 6.4.8 HOYER Group

- 6.4.9 ADLI Logistics

- 6.4.10 CEVA Logistics

- 6.4.11 Quantix Supply Chain

- 6.4.12 R&S Logistics

- 6.4.13 Talke Logistics

- 6.4.14 Hellmann Worldwide Logistics

- 6.4.15 Yusen Logistics (part of NYK Line)

- 6.4.16 Bertschi AG

- 6.4.17 Kuehne + Nagel

- 6.4.18 Den Hartogh Logistics

- 6.4.19 Weber Hazmat Logistics

- 6.4.20 Odyssey Logistics & Technology Corporation