|

시장보고서

상품코드

2062051

아시아태평양의 화학제품 창고 및 보관 시장 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Asia-Pacific Chemical Warehousing And Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

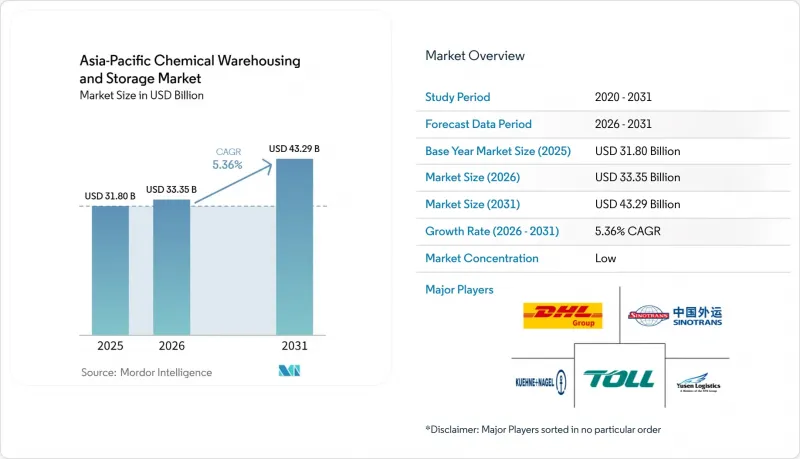

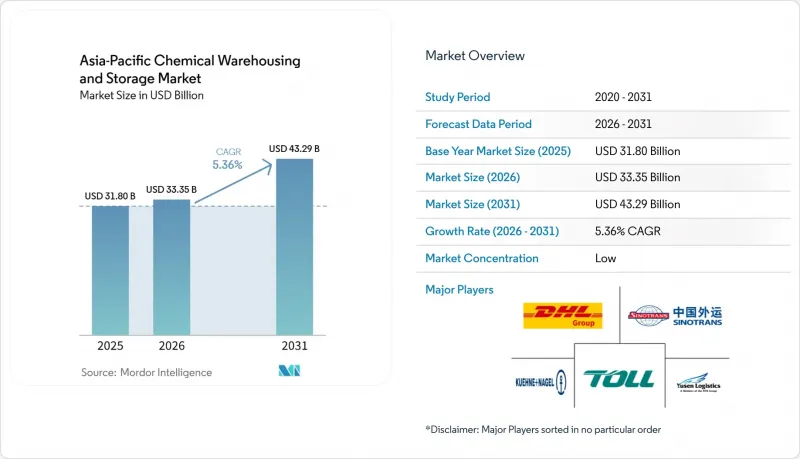

Mordor Intelligence에 의하면, 아시아태평양 화학제품 창고 및 보관 시장 규모는 2025년에 318억 달러, 2026년에 333억 5,000만 달러가 되어, 2031년까지 432억 9,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 5.36%로 성장할 것으로 전망됩니다.

본 보고서는 창고 유형(일반 창고, 특수 화학제품 창고 등), 화학제품 유형(인화성 액체, 부식성 물질 등), 최종 사용자 산업(기초 화학제품 제조, 특수 화학제품 제조 등), 그리고 국가(중국, 인도, 일본 등)별로 분류되어 있습니다. 시장 전망은 금액 기준(10억 달러)으로 제시되어 있습니다.

아시아태평양 화학제품 창고 및 보관 시장 동향과 인사이트

의약품 콜드체인 및 생명과학 제조 분야의 성장

콜드체인 물류는 바이오의약품 및 백신 유통 과정에서 엄격한 모니터링 및 경보 기능을 갖춘 다양한 온도 구역을 유지할 수 있는 시설이 필요해짐에 따라, 보관 사양을 재구축하고 있습니다. 지역 사업자들은 회전율 향상과 자본의 고정화를 억제하기 위해 임대 자산의 풀링 체계를 구축하고 있으며, 그 일례로 임상용 자재를 대상으로 아시아태평양의 여러 허브를 아우르는 편도 팔레트 운송 네트워크를 들 수 있습니다. 예측 알림 기능을 갖춘 실시간 냉동 컨테이너 원격 모니터링은 많은 입찰 프로젝트에서 표준으로 자리 잡았으며, 시간 단위 모니터링은 현재 아시아태평양의 화학제품 창고 및 보관 시장 전반에 걸쳐 조달 체크리스트에 포함되어 있습니다. 대만의 바이오의약품 보관 시설에서 볼 수 있는 것처럼, 신속한 경보 기능을 갖춘 환경 모니터링 시스템이 제안 요청서(RFP)에 명시되는 사례가 증가하고 있으며, 이는 사업자가 적정 유통 기준(GDP) 요건을 충족하는 데 도움이 되고 있습니다. 인도 및 동남아시아 지역의 네트워크 확충을 통해 항만 인근의 보관 능력과 내륙 지역의 냉장 창고가 연계되어, 시간 및 온도에 민감한 화물의 인계 및 사이클 타임 단축이 이루어지고 있습니다. 아시아태평양 전체에서 식품 및 의약품 분야의 강력한 수요를 배경으로 콜드체인 보관 면적이 지속적으로 확대되고 있으며, 이에 따라 아시아태평양의 화학제품 창고 및 보관 시장을 지탱하는 온도 관리형 거점의 요금 안정성과 가동률이 뒷받침되고 있습니다.

제3자 물류(3PL) 업체로의 아웃소싱 가속화

각 화학 제조업체는 가시성 확보, 규정 준수 대응 체계 구축, 그리고 규모에 맞는 비용 관리를 실현하기 위해 주요 물류 파트너와의 협력을 통해 창고 보관 및 운송 업무를 통합하고 있습니다. 대표적인 사례로, 항공, 해상, 육로를 아우르는 연간 수만 건의 출하를 총괄하기 위해 단일 지역 리더를 선정하고, 경로 리스크 및 운송업체 심사에 통합 플랫폼을 활용하는 경우가 있습니다. 이는 아시아태평양의 화학제품 창고 및 보관 시장에서 아웃소싱이 복잡한 네트워크의 위험을 어떻게 줄이는지를 보여줍니다. 중국에서는 위험물에 대한 전 과정 IT 추적 및 당국과의 전자적 연계를 공식화하는 규제안이 마련됨에 따라, 소규모 화주들은 이미 규정 준수 시스템을 운영하고 있는 3PL 파트너와 제휴하는 방향으로 나아가고 있습니다. 또한, 각 아웃소싱 업체들은 화학제품 전용 워크플로를 활용한 재포장 및 서류 관리와 같은 부가가치 서비스를 패키지화하고 있으며, 이를 통해 아시아태평양의 화학제품 창고 및 보관 시장에서 리드 타임 단축과 예외 처리 비용 절감을 실현하고 있습니다. 지역 사업자들이 인도와 동남아시아로 네트워크를 확장함에 따라, 항만 거점과 내륙 물류 센터 간의 연계가 강화되어 대규모 사업 전개 시에도 서비스 신뢰성이 향상되고 있습니다.

연안 공업 지대의 심각한 토지 부족

아시아의 연안 산업 지역에서는 완충 구역 및 위험 중첩 구역에 대한 규제가 강화되면서 유해 물질 보관에 적합한 토지 재고가 줄어들고 있습니다. 중국의 연안 위험 구역에 대한 동료 검토를 거친 분석에 따르면, 안전 거리 규제가 정착됨에 따라 허용된 산업용 공간이 현저히 축소되고 있으며, 이는 지가를 상승시켜 아시아태평양의 화학제품 창고 및 보관 시장 내 확장 계획을 복잡하게 만들고 있습니다. 각 사업자는 서비스 수준과 안전 기준을 유지하면서, 제한된 부지 면적을 보완하기 위해 고층 랙, 자동화 및 수직적 밀도 향상을 통해 대응하고 있습니다. 재개발은 구역 지정 및 지역 사회의 제약에 직면해 있으며, 네트워크는 내륙 지역으로 재분배되고 있습니다. 이로 인해 육상 운송비나 복합 운송 비용은 증가하지만, 건설 가능한 부지를 확보할 수 있습니다. 성숙한 대도시권의 콜드체인 시설은 가동률이 포화 상태에 이르고, 이에 따라 인증된 냉장 팔레트 보관 공간의 프리미엄이 확대되면서 상온 보관과의 가치 격차가 지속적으로 발생하고 있습니다. 장기적으로 볼 때, 아시아태평양의 화학제품 창고 및 보관 시장에서 희소한 토지가 더욱 엄격한 규제 기준을 충족하게 되면, 자동화, 안전 인증, 스마트 에너지 관리를 융합한 프로젝트가 비용 면에서 우위를 점하게 될 것입니다.

부문별 분석

2025년 기준으로 일반 창고는 아시아태평양 화학제품 창고 및 보관 시장 점유율의 30.12%를 차지하고 있으며, 이는 상온 조건에서 보관 가능한 범용 용제, 기유, 중간 화학제품에 대한 폭넓은 적합성을 반영한 것입니다. 바이오의약품, 백신 및 온도에 민감한 제제에는 매핑된 냉장 구역, 검증된 센서 및 이벤트 로그가 필요하기 때문에 온도 관리 시설 시장은 2031년까지 연평균 성장률(CAGR) 6.81%로 성장을 이어가고 있습니다. 각 운영사는 제품의 품질을 저해하지 않으면서도 다양한 제품 포트폴리오를 관리하기 위해, 동일 부지 내에 상온 보관 구역과 함께 냉장실을 계속해서 설치하고 있습니다. 25°C 미만의 보관실, 발포제식 자동 스프링클러, 창고 관리 시스템(WMS)와 연동된 피킹 기능을 갖춘 전용 물류 허브는 수요가 많은 거점에서의 고품질 인프라로의 구조적 전환을 반영하고 있습니다. 성숙한 대도시권에서는 콜드체인 시설의 이용률이 여전히 포화 상태이며, 이로 인해 상온 보관 시설과의 임대료 격차가 유지되면서 신축 물건의 경제성을 뒷받침하고 있습니다. 예측 기간 동안 아시아태평양의 화학제품 창고 및 보관 시장에서는 항만이나 공항 인근에 상온·냉장 통합형 시설의 도입이 확대되어, 화물 인수·인도 절차의 단축과 온도 관리가 필요한 화물의 예외적 위험 감소가 기대됩니다.

아시아태평양의 화학제품 창고 및 보관 시장에서 온도 관리 시설 시장 규모는 GDP, ISO 9001 및 ISO 45001 관련 인증 기준이 강화됨에 따라 확대될 것으로 예측됩니다. 물류 및 예측 알림과 관련된 실시간 원격 측정 데이터는 신규 입찰에서 표준 기능으로 자리 잡고 있으며, 이를 통해 IoT 지원 냉장실 및 보관 중인 물품에 대한 지속적인 모니터링의 사업적 타당성이 강화되고 있습니다. 유해 물질 보관에 관한 병행 기준 제정으로 인해 내화성, 환기, 내진 고정과 관련된 기본적인 구조 요건이 강화되었으며, 이에 따라 설비 투자(CAPEX) 수요가 증가하고, 기존 시설과 A급 시설 간의 성능 격차가 확대되고 있습니다. 고객들이 보관, 모니터링, 규정 준수 보고를 통합한 다년 계약을 검토함에 따라, 이러한 추세가 아시아태평양의 화학제품 창고 및 보관 업계의 양상을 변화시키고 있습니다. 온도 매핑, 구역 분리 및 제어된 기류에 대한 시설 차원의 투자를 통해, 사업자는 감사 요건을 충족하면서 평방피트당 유효 용량을 확대할 수 있게 되었습니다. 그 결과, 아시아태평양의 화학제품 창고 및 보관 시장에서 인증을 받은 냉장 환경 및 특수 용도 대응 환경으로의 비중이 꾸준히 증가하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the asia-Pacific chemical warehousing and storage market size is projected to be USD 31.80 billion in 2025, USD 33.35 billion in 2026, and reach USD 43.29 billion by 2031, growing at a CAGR of 5.36% from 2026 to 2031.

This report is Segmented by Warehouse Type (General Warehousing, Specialty Chemical Warehouse, and More), by Chemical Type (Flammable Liquids, Corrosives, and More), by End-User Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, and More), and by Country (China, India, Japan, and More). The Market Forecasts are Provided in Terms of Value (USD Billion).

Asia-Pacific Chemical Warehousing And Storage Market Trends and Insights

Pharmaceutical Cold Chain and Life Sciences Manufacturing Growth

Cold-chain logistics is reshaping storage specifications as biologics and vaccine flows demand facilities that can maintain distinct temperature zones with tight monitoring and alerting. Regional operations are deploying rental-asset pooling to accelerate turns and limit capital lock-up, illustrated by one-way pallet shipper networks now spanning multiple Asia-Pacific hubs for clinical materials. Real-time reefer telemetry with predictive alerts has become standard in many tenders, and hour-by-hour monitoring is now embedded into procurement checklists across the Asia-Pacific chemical warehousing and storage market. Environmental Monitoring Systems with rapid alarms, as seen in Taiwan biologics storage, are increasingly specified in requests for proposals and help operators meet Good Distribution Practice expectations. Network buildouts in India and Southeast Asia are aligning port-proximate capacity with inland cold rooms to reduce handovers and cycle time for time- and temperature-sensitive shipments. Cold-chain square meters across APAC continue to expand under strong food and pharma pull, which supports rate resilience and utilization for temperature-controlled nodes serving the Asia-Pacific chemical warehousing and storage market.

Accelerating Outsourcing to Third-Party Logistics (3PL) Providers

Chemical producers are consolidating warehousing and transportation with lead logistics partners to gain visibility, compliance readiness, and scale-based cost control. A prominent example is the selection of a single regional leader to orchestrate tens of thousands of annual shipments across air, ocean, and road while using integrated platforms for lane risk and carrier vetting, which demonstrates how outsourcing de-risks complex networks in the Asia-Pacific chemical warehousing and storage market. Draft regulations in China are formalizing lifecycle IT tracking and electronic connectivity with authorities for dangerous goods, which is pushing smaller shippers toward 3PL partnerships that already operate compliant systems. Outsourcers are also bundling value-added services like repackaging and documentation management using specialized chemical workflows, which shortens lead times and reduces exception costs in the Asia-Pacific chemical warehousing and storage market. Network expansion by regional operators into India and Southeast Asia is strengthening the interplay between port-based nodes and inland distribution centers that support higher service reliability at scale.

Severe Land Scarcity in Coastal Industrial Corridors

Coastal industrial belts in Asia are tightening buffer zones and risk overlays, which reduces the inventory of land parcels eligible for hazardous-materials storage. Peer-reviewed analysis of China's coastal risk zones shows a clear contraction of permitted industrial spaces as safety-distance rules take hold, which elevates land prices and complicates expansion plans for the Asia-Pacific chemical warehousing and storage market. Operators are responding with high-bay racking, automation, and vertical density to offset constrained footprints while maintaining service levels and safety envelopes. Redevelopments are facing zoning and community constraints, and networks are rebalancing inland, which adds drayage and intermodal costs but secures buildable land. Cold-chain locations in mature metros are running tight utilization, which amplifies the premium on certified refrigerated pallet positions and creates a durable value gap with ambient storage. Over the long term, projects that blend automation, safety certification, and smart energy management will carry a cost advantage when scarce land meets higher regulatory thresholds in the Asia-Pacific chemical warehousing and storage market.

Other drivers and restraints analyzed in the detailed report include:

- Strategic LNG-to-Chemicals Hub Investments

- Build-Own-Operate (BOO) and Build-Operate-Transfer (BOT) Project Models

- Chronic Shortage of Trained Hazmat Handling Personnel

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

General warehousing captured 30.12% of the Asia-Pacific chemical warehousing and storage market share in 2025, reflecting broad suitability for commodity solvents, base oils, and intermediate chemicals subject to ambient conditions. Temperature-controlled facilities are pacing growth at 6.81% CAGR through 2031 as biologics, vaccines, and sensitive formulations require mapped refrigeration zones, validated sensors, and event logging. Operators continue to deploy cold rooms alongside ambient bays in the same compound to manage mixed portfolios without compromising product integrity. Purpose-built distribution hubs with sub-25°C rooms, foam-based automated sprinklers, and WMS-integrated order picking reflect a structural pivot toward premium infrastructure in high-volume nodes. Cold-chain utilization remains tight across mature metros, which sustains rent differentials relative to dry storage and supports new-build economics. Over the forecast window, the Asia-Pacific chemical warehousing and storage market will likely see greater adoption of integrated ambient-and-cold sites near ports and airports to trim handovers and reduce exception risk for sensitive loads.

The Asia-Pacific chemical warehousing and storage market size for temperature-controlled facilities is projected to expand as certification frameworks tighten around GDP, ISO 9001, and ISO 45001. Real-time telemetry, in referring to logistics and predictive alerting are becoming a default feature in new tenders, which strengthens the business case for IoT-enabled cold rooms and continuous monitoring in storage. Parallel standard-setting for toxic-substance storage is raising baseline structural requirements for fire resistance, ventilation, and seismic anchoring, which is lifting capex needs and widening performance spreads between legacy and Grade A facilities. These preferences are reshaping the Asia-Pacific chemical warehousing and storage industry profile as customers weigh multi-year commitments that bundle storage, monitoring, and compliance reporting. Facility-level investments in temperature mapping, zone segregation, and controlled airflow are also enabling operators to stretch usable capacity per square foot while upholding audit requirements. The net effect is a steady mix shift toward certified cold and specialty-ready environments within the Asia-Pacific chemical warehousing and storage market.

List of Companies Covered in this Report:

- DHL Group

- Sinotrans

- Toll Group

- Kuehne + Nagel International AG

- Yusen Logistics Co., Ltd. (Part of NYK Line)

- HOYER Group

- C.H. Robinson

- DSV

- Suttons Group

- Nippon Express

- Broekman Logistics

- CEVA Logistics

- Rhenus Logistics

- BDP International

- Den Hartogh Logistics

- Talke Logistics

- Kerry Logistics Network Ltd.

- United Parcel Service (UPS)

- Stolt-Nielsen Ltd.

- Aegis Logistics Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Pharmaceutical Cold Chain and Life Sciences Manufacturing Growth

- 4.2.2 Accelerating Outsourcing to Third-Party Logistics (3PL) Providers

- 4.2.3 Strategic LNG-to-Chemicals Hub Investments

- 4.2.4 Build-Own-Operate (BOO) and Build-Operate-Transfer (BOT) Project Models

- 4.2.5 Growth in Specialty Chemicals and Advanced Materials Manufacturing

- 4.2.6 E-commerce and Chemical Distribution to Small-Scale Industries

- 4.3 Market Restraints

- 4.3.1 Severe Land Scarcity in Coastal Industrial Corridors

- 4.3.2 Chronic Shortage of Trained Hazmat Handling Personnel

- 4.3.3 Escalating Insurance Premiums Following Major Incidents

- 4.3.4 High Capital Intensity and Long Payback Periods

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Chemical Type Segmentation Driving Facility Design

- 4.9 Temperature-Controlled Segment Leading Premium Growth

5 Market Size & Growth Forecasts (Value, USD Billion)

- 5.1 By Warehouse Type

- 5.1.1 General Warehousing

- 5.1.2 Specialty Chemical Warehouse

- 5.1.3 Hazardous Materials (HAZMAT) Warehouses

- 5.1.4 Temperature-Controlled Chemical Warehouses

- 5.2 By Chemical Type

- 5.2.1 Flammable Liquids

- 5.2.2 Corrosives

- 5.2.3 Toxic Substances

- 5.2.4 Oxidizers

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Basic Chemicals Manufacturing

- 5.3.2 Specialty Chemicals Manufacturing

- 5.3.3 Pharmaceuticals & Life Sciences

- 5.3.4 Agrochemicals

- 5.3.5 Paints, Coatings & Adhesives

- 5.3.6 Food & Feed Additives

- 5.3.7 Oil & Gas / Petrochemicals

- 5.3.8 Others

- 5.4 By Country

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 South Korea

- 5.4.5 Indonesia

- 5.4.6 Malaysia

- 5.4.7 Thailand

- 5.4.8 Vietnam

- 5.4.9 Philippines

- 5.4.10 Singapore

- 5.4.11 Australia

- 5.4.12 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 Sinotrans

- 6.4.3 Toll Group

- 6.4.4 Kuehne + Nagel International AG

- 6.4.5 Yusen Logistics Co., Ltd. (Part of NYK Line)

- 6.4.6 HOYER Group

- 6.4.7 C.H. Robinson

- 6.4.8 DSV

- 6.4.9 Suttons Group

- 6.4.10 Nippon Express

- 6.4.11 Broekman Logistics

- 6.4.12 CEVA Logistics

- 6.4.13 Rhenus Logistics

- 6.4.14 BDP International

- 6.4.15 Den Hartogh Logistics

- 6.4.16 Talke Logistics

- 6.4.17 Kerry Logistics Network Ltd.

- 6.4.18 United Parcel Service (UPS)

- 6.4.19 Stolt-Nielsen Ltd.

- 6.4.20 Aegis Logistics Ltd