|

시장보고서

상품코드

2062053

인도 창고 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)India Warehouse - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

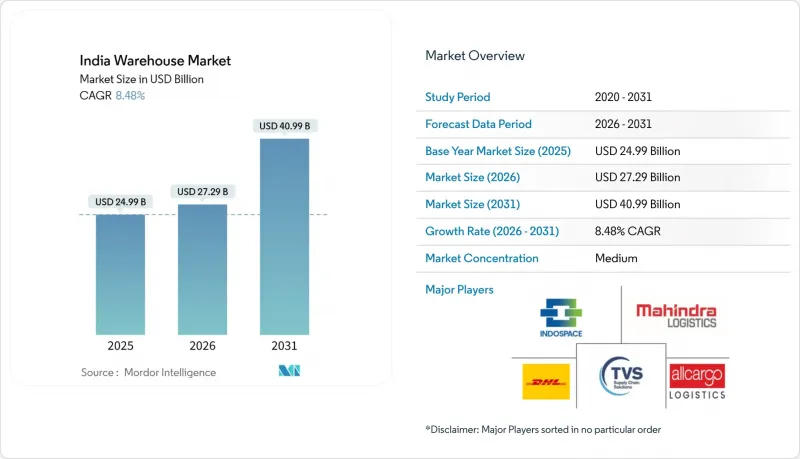

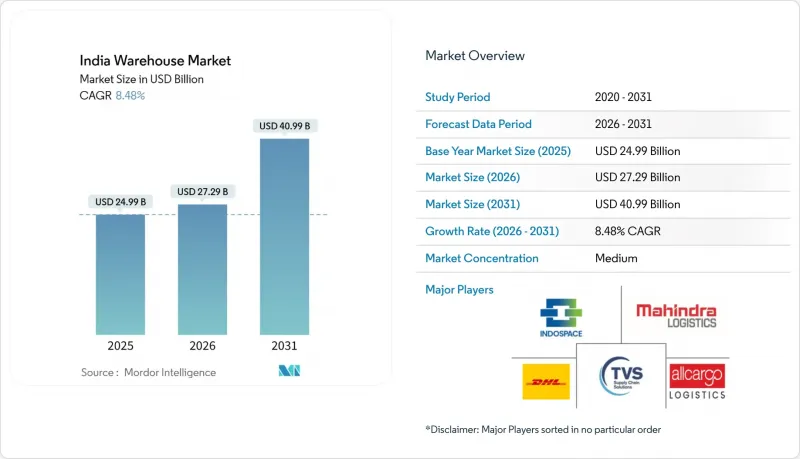

Mordor Intelligence에 의하면, 인도 창고 시장 규모는 2025년 249억 9,000만 달러로 평가되었고, 2026년에는 272억 9,000만 달러로 추정되고, 2026-2031년 CAGR 8.48%로 성장을 지속할 전망이며, 2031년까지 409억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 창고 유형별(일반 창고 및 보관, 냉장 창고 및 보관), 등급별(등급 A, 등급 B, 등급 C, 비등급), 최종 사용자 산업별(전자상거래 및 소매, 식품 및 음료, 제약 및 헬스케어, 기타), 지역별(북인도, 남인도, 서인도, 동인도, 중부 인도)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

인도의 창고 시장 동향 및 인사이트

국가물류정책(NLP-2022)의 시행

이 정책은 2030년까지 물류 비용을 GDP의 8% 이하로 줄이는 것을 목표로 하고 있으며, 이에 따라 조직형 창고에 대한 투자가 촉진되고 있습니다. 주 차원의 CLAP(주 물류 행동 계획)에서는 특히 마하라슈트라주, 구자라트주, 타밀나두주에서 승인 절차를 단축하는 원스톱 통관 제도가 도입되었습니다. ULIP를 통한 36개 중앙 및 주 차원의 시스템 통합으로 화물 및 용량의 실시간 가시화가 실현되어, 3PL 사업자를 위한 동적인 공간 배분이 가능해집니다. 4,600억 루피의 자금을 바탕으로 의무적으로 조성된 35개의 복합물류단지는 창고, 세관, 운송 거점을 갖추고 있어, 내륙 지역의 이용 가능한 입지 범위를 확대되고 있습니다. 임차인은 철도 및 도로 연결 지점까지의 접근성을 개선하여 전체 체류 시간을 단축하고 재고 회전율을 높일 수 있습니다.

전용 화물 회랑 및 복합 물류 단지의 가동

2025년까지 서부 및 동부 회랑의 완공률은 96.4%에 달했으며, 시속 100km로 주행하는 화물열차가 하루 352편 운행될 수 있게 되어 델리-뭄바이 구간과 루디아나-콜카타 구간의 운송 시간이 최대 40% 단축되었습니다. 현재 임차인들은 회랑의 교차점으로부터 30km 반경 내의 입지를 선호하고 있으며, 루하리와 비완디에서 수요가 꾸준히 유지되고 있는 것이 그 증거입니다. IndoSpace가 추진하는 170만 평방피트 규모의 비완디 파크나 Welspun One이 추진하는 120만 평방피트 규모의 탈레가온 프로젝트와 같은 개발사들의 발표에서는 DFC 인터체인지 및 계획 중인 MMLP와의 근접성이 특히 강조되고 있습니다.

환경영향 평가 및 소방안전 인가의 장기화

2만 제곱미터를 초과하는 시설은 환경·산림·기후 변화부(MoEFCC)의 지침에 따라 환경영향 평가(EIA) 승인이 필요하며, 이로 인해 프로젝트 착수 기간이 최대 12개월 연장됩니다. 또한, 고층 창고 구조물의 경우 NBC-2016(2016년 국가건축기준)에 따라 스프링클러 및 소화전에 관한 엄격한 기준을 충족해야 합니다. 개발사는 지연을 줄이기 위해 EIA 적용 기준에 미달하는 규모로 프로젝트를 단계적으로 진행하는 경우가 있으며, 이 경우 규모의 경제성을 희생하게 됩니다. 2024년 WDRA 핸드북은 기술 기준의 통일을 목표로 하고 있으나, 그 채택 여부는 주마다 다릅니다.

부문별 분석

2025년 기준, 인도 창고 시장 점유율의 60.01%를 일반 창고 및 보관 서비스가 차지하고 있으며, 이 분야는 전자상거래, FMCG, 엔지니어링 제품을 다루고 있습니다. 냉장 창고 시장은 백신 유통, QSR(퀵서비스 레스토랑)의 확대, 신선식품 수출을 배경으로 연평균 성장률(CAGR) 12.94%를 기록하며 성장할 것으로 전망됩니다. 스노우맨 로지스틱스는 2026년 3월까지 22개 도시에서 팔레트 수용 능력을 15만 4,330개에서 16만 230개로 확대하고, 푸네와 파트나에 새로운 거점을 추가했습니다. 냉장 시설은 상온 창고에 비해 최대 60% 높은 임대료 프리미엄이 책정되어 있으며, 엄격한 규정 준수 요건으로 인해 85-90%의 입주율을 달성하고 있습니다. 따라서 인도 창고 시장에서 콜드체인 하위 부문의 규모는 2031년까지 상온 창고의 신규 공급량을 상회할 것으로 전망됩니다.

제약 기업 임차인들은 WHO-GDP 인증을 받은 환경과 지속적인 모니터링을 요구하며, 이를 통해 장기 임대 계약이 유지되어 전문 사업자에게 더 높은 수익률을 가져다주고 있습니다. 일반 창고 역시 여전히 중요하지만, 상품화 및 미시적 시장공급 과잉으로 인해 임대료 상승이 억제되고 있으며, 이로 인해 소유주들은 자동화 및 ESG 기능 도입을 서둘러야 하는 상황에 놓여 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the india warehouse market size is expected to grow from USD 24.99 billion in 2025 to USD 27.29 billion in 2026 and is forecast to reach USD 40.99 billion by 2031 at 8.48% CAGR over 2026-2031.

This report is Segmented by Warehouse Type (General Warehousing and Storage, Refrigerated Warehousing and Storage), by Grade (Grade-A, Grade-B, Grade-C and Unorganized), by End-User Industry (E-Commerce and Retail, Food and Beverage, Pharma and Healthcare, and More), and by Geography (North India, South India, West India, East India, Central India). The Market Forecasts are Provided in Terms of Value (USD).

India Warehouse Market Trends and Insights

Implementation of National Logistics Policy (NLP-2022)

The policy targets a logistics-cost reduction to below 8% of GDP by 2030, spurring organized warehousing investment. State-level CLAPs have introduced single-window clearances that shorten approval cycles, especially in Maharashtra, Gujarat, and Tamil Nadu. ULIP's integration of 36 central and state systems offers real-time visibility of cargo and capacity, enabling dynamic space allocation for 3PLs. The mandated 35 multi-modal logistics parks, backed by INR 46,000 crore, embed warehousing, customs, and transport nodes, widening the radius of feasible hinterland sites. Tenants gain faster access to rail-road interfaces, cutting overall dwell time and improving inventory turns.

Commissioning of Dedicated Freight Corridors & Multi-Modal Logistics Parks

By 2025, the Western and Eastern corridors reached 96.4% completion, enabling 352 daily freight trains running at 100 km/h and slicing Delhi-Mumbai and Ludhiana-Kolkata transit times by up to 40%. Occupiers now favor sites within 30 km of corridor nodes, evidenced by robust absorption in Luhari and Bhiwandi. Developer announcements, such as IndoSpace's 1.7 million sq ft Bhiwandi park and Welspun One's 1.2 million sq ft Talegaon project, specifically cite proximity to DFC interchanges and planned MMLPs.

Lengthy Environmental-Impact & Fire-Safety Clearance Timelines

Facilities exceeding 20,000 sq m require EIA approval under MoEFCC guidelines, extending project gestation by up to 12 months. High-rack structures also face strict sprinkler and hydrant compliance under NBC-2016. Developers sometimes phase projects below the EIA threshold to mitigate delays, sacrificing economies of scale. The 2024 WDRA handbook aims to harmonize technical norms, yet adoption varies across states.

Other drivers and restraints analyzed in the detailed report include:

- Production-Linked Incentive Schemes Boosting Manufacturing Inventory

- Omni-Channel Retail's Push for Decentralized Micro-Fulfilment Centers

- Intermittent Grid Power Jeopardizing Automation Uptime

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

General warehousing and storage controlled 60.01% of India warehouse market share in 2025, serving e-commerce, FMCG, and engineering goods. Refrigerated warehousing is forecast to grow at 12.94% CAGR on the back of vaccine distribution, QSR expansion, and perishable exports. Snowman Logistics augmented capacity from 154,330 to 160,230 pallets across 22 cities by March 2026, adding new Pune and Patna sites. Refrigerated facilities command rent premiums of up to 60% over ambient warehouses and achieve 85-90% occupancy due to stringent compliance gaps. The India warehouse market size for the cold chain sub-segment is thus projected to outpace ambient space additions through 2031.

Pharmaceutical occupiers demand WHO-GDP-validated environments with continuous monitoring, sustaining long-duration leases and higher yields for specialized operators. General warehousing remains vital, but commoditization and micro-market oversupply temper rent growth, pushing landlords to retrofit automation and ESG features.

List of Companies Covered in this Report:

- Mahindra Logistics

- Snowman Logistics

- IndoSpace

- DHL Group

- VRL Logistics Limited

- TVS Supply Chain Solutions

- Allcargo Logistics

- TCI Supply Chain Solutions

- Delhivery

- Safexpress

- LOGOS India

- Godamwale Logistic

- Warehouzez

- Ascendas Firstspace

- StarAgri Warehousing

- Blue Dart Express

- ColdEx Logistics

- Kintetsu World Express (India) Pvt. Ltd.

- XpressBees

- Apollo LogiSolutions*

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Implementation of National Logistics Policy (NLP-2022)

- 4.2.2 Commissioning of Dedicated Freight Corridors and Multi-Modal Logistics Parks

- 4.2.3 Production-Linked Incentive (PLI) Schemes Boosting Domestic Manufacturing Inventory Needs

- 4.2.4 Omni-Channel Retail's Push for Decentralized Micro-Fulfilment Centers

- 4.2.5 Surge in ESG-Compliant 'Green Warehouse' Certifications Attracting Premium Tenants

- 4.2.6 Reverse-Logistics & Returns-Processing Space Demand from Rising E-Commerce Returns

- 4.3 Market Restraints

- 4.3.1 Lengthy Environmental-Impact & Fire-Safety Clearance Timelines

- 4.3.2 Intermittent Grid Power Jeopardizing Automation Uptime, Raising Backup CAPEX

- 4.3.3 Shortage of Skilled Warehouse Automation Technicians

- 4.3.4 Insurance Premiums Escalating Due to Warehouse Fire-Load & Climate Risk

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 Segmentation by Warehouse Type (Value)

- 5.1.1 General Warehousing and Storage

- 5.1.2 Refrigerated Warehousing and Storage

- 5.2 Segmentation by Grade (Value)

- 5.2.1 Grade-A

- 5.2.2 Grade-B

- 5.2.3 Grade-C & Unorganised

- 5.3 Segmentation by End-User Industry (Value)

- 5.3.1 E-commerce and Retail

- 5.3.2 Food and Beverage

- 5.3.3 Pharma and Healthcare

- 5.3.4 Automotive

- 5.3.5 Manufacturing and Engineering Goods

- 5.3.6 Others

- 5.4 Segmentation by Region (Value)

- 5.4.1 North India

- 5.4.1.1 Delhi-NCR

- 5.4.1.2 Punjab

- 5.4.1.3 Haryana

- 5.4.1.4 Others

- 5.4.2 South India

- 5.4.2.1 Karnataka

- 5.4.2.2 Tamil Nadu

- 5.4.2.3 Telangana

- 5.4.2.4 Others

- 5.4.3 West India

- 5.4.3.1 Maharashtra

- 5.4.3.2 Gujarat

- 5.4.3.3 Others

- 5.4.4 East India

- 5.4.4.1 West Bengal

- 5.4.4.2 Odisha

- 5.4.4.3 Others

- 5.4.5 Central India

- 5.4.5.1 Madhya Pradesh

- 5.4.5.2 Chhattisgarh

- 5.4.1 North India

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Mahindra Logistics

- 6.4.2 Snowman Logistics

- 6.4.3 IndoSpace

- 6.4.4 DHL Group

- 6.4.5 VRL Logistics Limited

- 6.4.6 TVS Supply Chain Solutions

- 6.4.7 Allcargo Logistics

- 6.4.8 TCI Supply Chain Solutions

- 6.4.9 Delhivery

- 6.4.10 Safexpress

- 6.4.11 LOGOS India

- 6.4.12 Godamwale Logistic

- 6.4.13 Warehouzez

- 6.4.14 Ascendas Firstspace

- 6.4.15 StarAgri Warehousing

- 6.4.16 Blue Dart Express

- 6.4.17 ColdEx Logistics

- 6.4.18 Kintetsu World Express (India) Pvt. Ltd.

- 6.4.19 XpressBees

- 6.4.20 Apollo LogiSolutions*