|

시장보고서

상품코드

2062074

파워 커터 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Power Cutter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

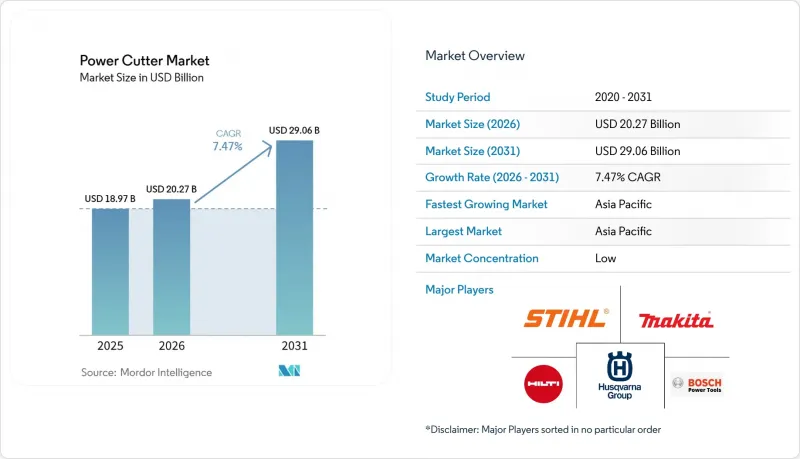

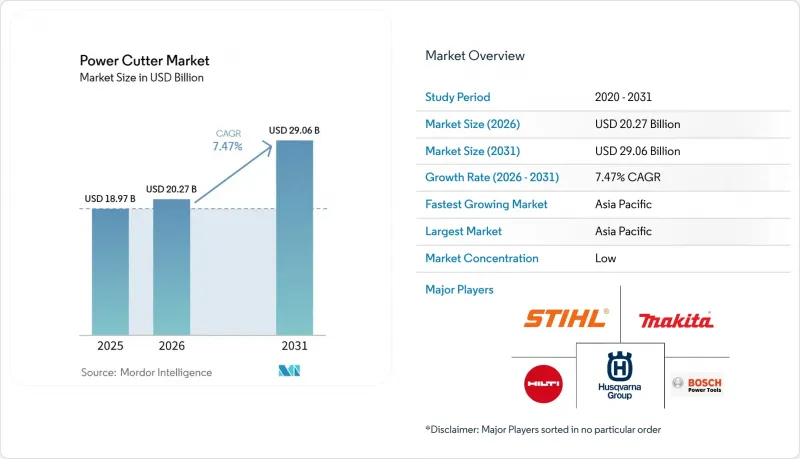

Mordor Intelligence에 의하면, 파워 커터 시장 규모는 2025년에 189억 7,000만 달러, 2026년에 202억 7,000만 달러가 되어, 2031년까지 290억 6,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 7.47%로 성장할 전망입니다.

본 보고서는 동력원별(가솔린식, 전기식-유선식 등), 제품 유형(핸드헬드 커터 톱, 워크 비하인드 커터 등), 블레이드 유형(연마 블레이드, 다이아몬드 블레이드 등), 최종 사용자 산업(건설·해체, 자동차 등), 지역(북미, 아시아태평양 등)에 따라 분류되어 있습니다. 시장 전망은 10억 달러 단위로 제시되어 있습니다.

세계 파워 커터 시장 동향과 인사이트

긴급 구조 및 재난 대응 활동에서의 도입 확대

현대 차량에 복합재료와 고장력 강판이 널리 사용됨에 따라, 긴급 구조 기관들은 절단 기능을 갖춘 파워 커터를 표준 장비 키트에 포함시키고 있습니다. Weber Rescue Systems사의 SMART-FORCE와 같은 플랫폼에서 제공하는 실시간 배터리 진단, 사용 기록, 위치 추적 기능은 여러 거점에 분산된 차량 전체의 준비 상태를 확인하고 자산 관리를 개선합니다. 컴팩트한 디자인과 전용 어태치먼트는 대중교통 수단이나 다중 차량 사고 현장에서의 신속한 전력 차단 등, 협소한 공간에서의 작업을 지원합니다. 이러한 기능 덕분에 현장에서 공구가 가동 중단될 위험이 줄어들며, 관할 구역을 넘어 전개된 후 상호 지원을 통한 복구 작업이 효율화됩니다. 제로 에미션 차량의 보급에 따라 구조대원들은 신뢰성 높은 제동 기능과 분진 억제 기능을 갖춘, 불꽃이 발생하지 않는 다이아몬드 블레이드 솔루션을 필요로 하고 있으며, 이는 파워 커터 시장에서 고품질 무선 플랫폼의 도입을 촉진하고 있습니다. 또한, 연결성 및 배터리 관리 기능은 각 부서가 수명 주기에 기반한 교체 계획이나 훈련을 수립하는 데에도 도움이 되며, 이를 통해 조달 계획과 운영상의 요구 사항 간의 일관성이 강화됩니다.

끊임없이 늘어나는 리모델링 및 개보수 활동

주택 리노베이션과 소규모 상업시설의 리모델링이 지속적으로 이루어지고 있어, 도자기, 타일, 석재, 경금속 가공이 가능한 휴대용 커터에 대한 수요는 여전히 높은 수준을 유지하고 있습니다. 주택 소유주와 소규모 시공업체들은 타일을 깔끔하게 절단하기 위한 연속 림 다이아몬드 블레이드와 콘크리트 작업을 신속하게 수행하기 위한 부문 블레이드를 함께 사용하고 있으며, 이를 통해 다양한 자재를 다루는 프로젝트에서 블레이드 교체 시간이 단축되고 있습니다. 규정 준수 및 인근 주민에 대한 배려가 요구되는 실내 작업에서는 물 분사 기능이나 방진 커버 등의 액세서리가 표준적인 선택 사항으로 자리 잡고 있습니다. 렌탈 프로그램을 통해, 구매 시 비용 대비 효과가 떨어지는 주말 프로젝트에서도 고성능 커터를 이용할 수 있게 되었습니다. 이와 함께, 시공사는 사람이 거주하는 현장에서 발생하는 분진이나 파편을 관리하기 위해 집진기나 물 세척 키트와 쉽게 연동할 수 있는 커터를 표준으로 장착하고 있습니다. 자금 조달 조건이 까다로운 상황에서 부동산 소유주들이 신축보다 개보수를 우선시함에 따라, 이러한 추세가 파워 커터 시장의 폭넓은 사용자 기반을 뒷받침하고 있습니다.

안전상의 위험 및 작업자의 부상 위험

회전식 절삭 공구에는 반동, 절삭날의 끼임, 파편 비산과 같은 고유한 위험이 있으며, 작업 현장에서는 이러한 위험을 가중시키는 변동이 심한 조건에서 작업이 이루어지는 경우가 많습니다. 이에 대응하여 제조업체는 강화된 블레이드 가드, 전자 브레이크, 그리고 날이 끼일 경우 출력을 차단하는 지능형 모터 제어 기능 등을 도입했습니다. 실내나 밀폐된 공간에서의 절단 작업이 늘어남에 따라, 실리카 노출을 관리하기 위해 물 분사 시스템과 방진 커버도 점차 표준화되고 있습니다. 무선 휴대용 장치는 혼잡한 작업 현장에서 걸려 넘어지는 사고의 위험을 줄이고, 설치 효율을 높여줍니다. 규제 및 법적 책임에 대한 압박으로 인해, 파워 커터 시장의 구매자들은 제동 시간부터 분진 대책에 이르기까지 통합된 안전 기능 전반을 바탕으로 공구를 평가하는 경향이 강해지고 있습니다. 센서를 다수 탑재하고 제동 기능을 갖춘 모델의 보급이 확대된다면, 전문 작업팀의 사고 심각도와 가동 중단 시간을 줄일 수 있을 것입니다.

부문별 분석

2025년 기준으로, 유선 전동 모델은 47.1%의 시장 점유율을 차지하고 있으며, 이는 배터리 교체 주기로 인해 작업 흐름이 방해받을 수 있는 수 시간에 걸친 작업 중단 상황에서 지속적인 토크 공급의 가치가 반영된 결과입니다. 이 점유율은 슬래브 절단, 고층 데크의 철근 절단, 그리고 중단 없는 가동 주기가 필수적인 고정식 가공 스테이션에서의 사용 현황과 일치합니다. 배터리 구동형 휴대용 모델은 플랫폼 규모 확대, 냉각 기능 및 충전 기술의 발전으로 인해 유선 모델과의 성능 격차가 줄어들고 있어, 2031년까지 연평균 성장률(CAGR) 8.8%로 가장 빠른 성장세를 보이고 있습니다. 각 브랜드는 단일 생태계를 통한 커버리지를 중시하고 있으며, 하나의 충전기와 몇 개의 배터리 팩만으로 여러 카테고리를 지원할 수 있어 활용도가 높아지고 장비 관리의 복잡성이 줄어듭니다. 전자 브레이크 및 과부하 보호 기능 덕분에, 무선 기기는 과거에 고정식 설비가 선호되던 안전성 요건을 충족하게 되었습니다. 도급업체들이 호환 가능한 수백 가지 유형의 공구에 대한 배터리 투자를 확대함에 따라, 플랫폼에 대한 종속성은 파워 커터 시장에서 전략적 요인으로 부상하고 있습니다. 또한, 조달 과정에서 도시 지역이나 폐쇄적인 환경에서는 엔진 배기 시스템이 없는 설계가 실행하기 쉬운 경우가 많으며, 분진 억제 및 진동 저감 요건도 반영되어 있습니다.

유선식 유닛은 초기 배터리 비용을 절감하고, 내장형 에너지 저장 장치에 비해 무게를 줄여줍니다. 이는 좁은 공간이나 반복적인 절단 작업에서 유용합니다. 가솔린식 절단기는 특히 고출력으로 연속 운전할 때 충전보다 급유가 더 신속하기 때문에 여전히 외딴 지역이나 재난 대응에서 중요한 역할을 하고 있지만, 인구 밀집 도시의 배기가스 규제로 인해 그 사용이 제한되고 있습니다. 유압 시스템은 토크 밀도가 최우선으로 요구되는 해체 작업이나 지하 매설물 작업 분야에서 여전히 특수한 틈새 시장을 차지하고 있지만, 호스와 보조 팩이 기동성을 제한하고 있습니다. 무선 제품의 등장으로 인해 압축기 설비나 공기 배관의 유지보수가 필요 없어짐에 따라, 공압식 솔루션은 점차 사라져 가고 있습니다. 무선 생태계가 성숙해짐에 따라, 파워 커터 업계 관계자들은 먼지 커버, 급수 시스템, 집진기와의 통합이 진전되어 종합적인 규정 준수가 실현되기를 기대하고 있습니다. 구매자들은 도구 자체의 가격뿐만 아니라 시스템 전체의 비용을 비교 검토하고 있으며, 생산성 향상이나 안전 기능이 초기 투자 비용을 상회할 경우 파워 커터 시장에서 고품질 무선 솔루션의 보급이 촉진될 것입니다.

지역별 분석

아시아태평양은 2025년 매출의 38.4%를 차지하며, 데이터센터 건설, 국가 인프라 계획, 대규모 교통 회랑을 견인력으로 삼아 2031년까지 연평균 성장률(CAGR) 8.5%로 성장할 것으로 전망됩니다. 2021년 중국의 건설기계 판매 대수와 굴삭기 출하 대수는 콘크리트, 철근, 아스팔트 등 각 사용 분야에서 커터에 대한 지속적인 수요가 있음을 시사합니다. 인도의 국가 인프라 계획 총액은 100조 루피(1조 2,000억 달러)에 달하며, 이는 고속도로 및 교통 허브의 단말 장비에 대한 향후 수년간 수요를 뒷받침하고 있습니다(1조 2,000억 달러). 사라이 칼레 칸에서 샤 자한푸르 베홀에 이르는 지역 고속 교통 시스템(RRT) 구간의 공사는 2026년 8월에 착공하여 2031년 11월까지 완료될 예정입니다. 이에 따라 해당 기간 동안 조인트 절단, 트렌치 절단 및 역 구내 절단에 대한 수요가 지속될 것으로 예측됩니다. 도쿄, 서울, 싱가포르, 홍콩 등 도시 지역의 배기가스 및 소음 규제로 인해, 실내 작업이나 야간 작업용 전기 구동 옵션에 대한 수요가 증가하고 있습니다. 한국에 영향을 미치는 생산 능력 확대를 포함한 현지 OEM 투자를 통해 공급망의 회복탄력성과 리드 타임이 개선될 것입니다.

북미와 유럽을 합치면 전 세계 매출의 약 절반을 차지하며, 프리미엄 가격, 체계적인 교육, 그리고 철저한 규정 준수 체제가 갖춰져 있습니다. 미국의 인프라 자금 조달 전망이 밝아짐에 따라, 가동 시간과 지원을 최우선으로 여기는 계약업체들의 공구 예산이 안정화되고 있습니다. 배출 가스, 실리카 분진, 손목 진동에 관한 유럽의 규제로 인해 기본 사양은 지속적으로 강화되고 있으며, 커터, 집진기, 물 세척 키트를 결합한 통합 시스템이 선호되고 있습니다. CE 마크 및 EN 규격은 성능이 문서화되고 재료의 추적성이 확보된 제품에 대한 조달 선호를 뒷받침하고 있습니다. 독일 등지 시장에서 보행식 톱 작업자를 위한 교육 자격증은 공구의 선정과 사용을 더욱 공식화하고 있습니다. 무선 플랫폼의 성능이 향상됨에 따라, 실내나 밀폐된 공간에서의 작업은 전용 환기 설비 없이도 현지 규정을 충족할 수 있어, 가솔린식 장비에서 점차 전환되고 있습니다.

남미, 중동 및 아프리카가 수요 균형에 기여하고 있습니다. 브라질, 칠레, 페루의 광업 및 채석업은 코어 트리밍 및 암석 가공에 사용되는 고성능 커터의 수주를 뒷받침하고 있습니다. 걸프협력회의(GCC) 시장의 대규모 건설 사업은 메가 프로젝트의 단계에 따라 일시적인 수요 급증을 초래하고 있습니다. 아프리카에서는 특정 경제권에서 산업화가 진행됨에 따라 도로망 정비와 항만 확장이 점진적인 성장을 가져오고 있습니다. 환율 변동과 기준 적용 상황의 차이는 판매 채널 전략에 영향을 미치고 있으며, 국제적인 건설사들은 안전성과 품질의 일관성을 확보하기 위해 고급 브랜드를 지정하는 경우가 많습니다. 이 지역 전체에서 건설업체들이 프로젝트 일정과 현금 흐름 계획에 맞추어 공구 사용을 조정하기 때문에 임대 서비스가 중요한 역할을 하고 있습니다. 파워 커터 시장은 이러한 유연성의 혜택을 누리고 있으며, 구매를 미루는 경우에도 고급 기종을 접할 기회가 늘어나고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the power cutter market size is projected to be USD 18.97 billion in 2025, USD 20.27 billion in 2026, and reach USD 29.06 billion by 2031, growing at a CAGR of 7.47% from 2026 to 2031.

This report is Segmented by Power Source (Gas-Powered, Electric - Corded, and More), by Product Type (Handheld Cut-Off Saws, Walk-Behind Cutters, and More), by Blade Type (Abrasive Blades, Diamond Blades, and More), by End-User Industry (Construction & Demolition, Automotive, and More), and by Geography (North America, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value in USD Billion.

Global Power Cutter Market Trends and Insights

Rising Adoption in Emergency Rescue and Disaster Response Operations

Emergency services are integrating connected power cutters into their standard operating kits due to the rise of composite materials and high-strength steels in modern vehicles. Real-time battery diagnostics, usage logs, and location tracking in platforms like Weber Rescue Systems' SMART-FORCE improve readiness verification and asset control across multi-station fleets. Compact form factors and specialty attachments support confined-space operations, including rapid access cuts in mass transit and multi-vehicle incidents. These capabilities reduce the risk of on-scene tool downtime and streamline mutual-aid recoveries after cross-jurisdictional deployments. As zero-emissions vehicles proliferate, responders need non-sparking diamond-blade solutions with reliable braking and dust control, which strengthens the case for premium cordless platforms in the power cutter market. Connectivity and battery management also help departments plan life-cycle replacement and training, which tightens procurement alignment with operational demands.

Growing Renovation and Remodeling Activities

Sustained home renovation and light commercial remodeling keep demand high for portable cutters that can handle porcelain, tile, masonry, and light metal tasks. Homeowners and small contractors combine continuous-rim diamond blades for clean tile cuts with segmented blades for faster concrete work, which reduces changeover time on multi-material projects. Water-suppression and dust-shroud accessories have become standard choices for indoor tasks where compliance and neighbor comfort matter. Rental programs extend access to higher-end cutters for weekend projects where purchase does not pencil out. In parallel, contractors standardize on cutters that integrate easily with vacuums and water kits to manage dust and debris on occupied sites. This activity sustains a broad base of users in the power cutter market as property owners prioritize upgrades over new builds when financing conditions are tight.

Safety Hazards and Operator Injury Risks

Rotating-blade tools present inherent risks that include kickback, binding, and debris ejection, and job sites often operate under variable conditions that can amplify these hazards. Manufacturers have responded with enhanced blade guards, electronic brakes, and intelligent motor controls that cut power during binding events. As more cutting shifts are being performed indoors or into enclosed spaces, water-suppression systems and dust shrouds are also being standardized to manage silica exposure. Portable units without cords reduce trip hazards around crowded work areas and improve setup discipline. Buyers in the power cutter market increasingly assess tools by their integrated safety stack, from braking times to dust mitigation, due to regulatory and liability pressures. Wider adoption of sensor-rich and brake-equipped models can reduce incident severity and downtime on professional crews.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Road Construction and Maintenance Programs

- Growth in DIY and Professional Landscaping Services

- Frequent Blade Replacement and Consumable Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electric corded models held 47.1% share in 2025, reflecting value in continuous torque delivery on multi-hour cutting tasks where battery-swap cycles could disrupt workflow. This position aligns with use on slab cuts, rebar sections on high-rise decks, and stationary fabrication stations where uninterrupted duty cycles are critical. Battery-powered handhelds show the fastest expansion at 8.8% CAGR through 2031 as platform-scale, cooling, and charging improvements narrow performance gaps with corded baselines. Brands emphasize single-ecosystem coverage so one charger and a few packs sustain multiple categories, which increases utilization and lowers fleet complexity. Electronic braking and overload protection features help cordless units meet safety expectations that once favored fixed installations. Platform lock-in has become a strategic factor in the power cutter market as contractors extend battery investments across hundreds of compatible tools. Procurement also reflects dust-control and vibration demands that are often easier to implement on designs without engine emissions systems in urban or enclosed environments.

Corded units eliminate upfront battery costs and reduce weight relative to onboard energy storage, which helps in tight spaces and repetitive cutting sequences. Gas-powered cutters still serve remote and disaster-response roles where refueling remains faster than charging, especially on sustained high-output cycles, although emissions policies in dense cities limit their use. Hydraulic systems continue to occupy a specialized niche for demolition and subsurface utility work where torque density is paramount, though hoses and auxiliary packs limit mobility. Pneumatic solutions are retreating as cordless options remove compressor infrastructure and airline maintenance. As cordless ecosystems mature, owners in the power cutter industry expect better integration with dust shrouds, water systems, and vacuums to deliver holistic compliance. Buyers weigh all-in system costs, not just tool-only price, which supports broader adoption of premium cordless solutions in the power cutter market when productivity gains and safety features offset initial investment.

Geography Analysis

Asia-Pacific accounted for 38.4% of 2025 revenue and is projected to grow at 8.5% CAGR through 2031, anchored by data-center construction, national infrastructure programs, and large transit corridors. China's 2021 construction-equipment sales and excavator volumes signal sustained complementary demand for cutters across concrete, rebar, and asphalt use cases. India's National Infrastructure Pipeline totals INR 100 trillion (USD 1.2 trillion), reinforcing multi-year demand for cutting equipment across highways and transit centers (USD 1.2 trillion). The Regional Rapid Transport System segment from Sarai Kale Khan to Shahjahanpur-Behror kicks off in August 2026 and is expected to be completed by November 2031, which implies sustained needs for joint, trench, and station cuts over the timeline. Urban emissions and noise policies in Tokyo, Seoul, Singapore, and Hong Kong steer buyers toward electric options for indoor and nighttime work. Localized OEM investments, including capacity decisions affecting South Korea, improve supply resilience and lead times.

North America and Europe together hold roughly the remaining half of global revenue, with premium pricing, codified training, and advanced compliance ecosystems. Funding visibility for United States infrastructure contributes to stable tool budgets among contractors that prioritize uptime and support. European regulations on emissions, silica dust, and hand-arm vibration continue to lift baseline specifications, which support integrated systems that combine cutters, vacuums, and water kits. CE marking and EN standards reinforce procurement preferences for documented performance and traceable materials. Training credentials for walk-behind saw operators in markets like Germany further formalize tool selection and usage. As cordless platforms improve, indoor and enclosed-space tasks shift away from gas equipment to meet local rules without specialized ventilation.

South America and the Middle East & Africa contribute to the balance of demand. Mining and quarrying across Brazil, Chile, and Peru sustain orders for heavy-duty cutters used in core trimming and rock processing. Large-scale construction in Gulf Cooperation Council markets produces episodic surges tied to mega-project phases. In Africa, road connectivity and port expansions add incremental growth as industrialization advances in select economies. Currency volatility and uneven enforcement of standards influence channel strategies, with international contractors often specifying premium brands for safety and quality consistency. Across these regions, rental plays an important role as contractors align tool access with project schedules and cash-flow planning. The power cutter market benefits from this flexibility, which expands access to premium platforms where outright purchase is deferred.

- Husqvarna Group

- Stihl Holding AG & Co. KG

- Makita Corporation

- Hilti Corporation

- Bosch Power Tools (Robert Bosch GmbH)

- Milwaukee Tool (Techtronic Industries)

- DeWalt (Stanley Black & Decker)

- HiKoki (Koki Holdings)

- Norton Clipper (Saint-Gobain Abrasives)

- ICS Diamond Tools (Blount International)

- Evolution Power Tools

- Wacker Neuson SE

- Metabo HPT

- Festool (TTS Tooltechnic Systems)

- Chicago Pneumatic

- Einhell Germany AG

- Ryobi Tools (TTI)

- Positec Group (Worx)

- Tyrolit Group

- ECHO Incorporated

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption in Emergency Rescue and Disaster Response Operations

- 4.2.2 Growing Renovation and Remodeling Activities

- 4.2.3 Expansion of Road Construction and Maintenance Programs

- 4.2.4 Growth in DIY and Professional Landscaping Services

- 4.2.5 Increasing Preference for Cordless and Battery-Powered Models

- 4.2.6 Mining and Quarrying Industry Expansion

- 4.3 Market Restraints

- 4.3.1 Safety Hazards and Operator Injury Risks

- 4.3.2 Frequent Blade Replacement and Consumable Costs

- 4.3.3 Seasonal Demand Fluctuations in Construction Activity

- 4.3.4 Physical Strain and Ergonomic Challenges

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Blade Technology and Compatibility Ecosystem

- 4.9 Professional vs. Consumer Grade Market Bifurcation

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Power Source

- 5.1.1 Gas-powered

- 5.1.2 Electric - Corded

- 5.1.3 Pneumatic

- 5.1.4 Hydraulic

- 5.1.5 Battery-powered (hand-held)

- 5.2 By Product Type

- 5.2.1 Handheld Cut-off Saws

- 5.2.2 Walk-behind Cutters

- 5.2.3 Stationary Cut-off Machines

- 5.3 By Blade Type

- 5.3.1 Abrasive Blades

- 5.3.2 Diamond Blades

- 5.3.3 Carbide & Multi-material Blades

- 5.4 By End-user Industry

- 5.4.1 Construction & Demolition

- 5.4.2 General Manufacturing, Metalworking & Fabrication

- 5.4.3 Automotive

- 5.4.4 Aerospace

- 5.4.5 Others (Consumer, DIY, Landscaping, Municipal, etc.)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Peru

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 Kuwait

- 5.5.5.5 Turkey

- 5.5.5.6 Egypt

- 5.5.5.7 South Africa

- 5.5.5.8 Nigeria

- 5.5.5.9 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Husqvarna Group

- 6.4.2 Stihl Holding AG & Co. KG

- 6.4.3 Makita Corporation

- 6.4.4 Hilti Corporation

- 6.4.5 Bosch Power Tools (Robert Bosch GmbH)

- 6.4.6 Milwaukee Tool (Techtronic Industries)

- 6.4.7 DeWalt (Stanley Black & Decker)

- 6.4.8 HiKoki (Koki Holdings)

- 6.4.9 Norton Clipper (Saint-Gobain Abrasives)

- 6.4.10 ICS Diamond Tools (Blount International)

- 6.4.11 Evolution Power Tools

- 6.4.12 Wacker Neuson SE

- 6.4.13 Metabo HPT

- 6.4.14 Festool (TTS Tooltechnic Systems)

- 6.4.15 Chicago Pneumatic

- 6.4.16 Einhell Germany AG

- 6.4.17 Ryobi Tools (TTI)

- 6.4.18 Positec Group (Worx)

- 6.4.19 Tyrolit Group

- 6.4.20 ECHO Incorporated

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment