|

시장보고서

상품코드

2062299

미국의 애프터마켓 TPMS : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Aftermarket TPMS - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

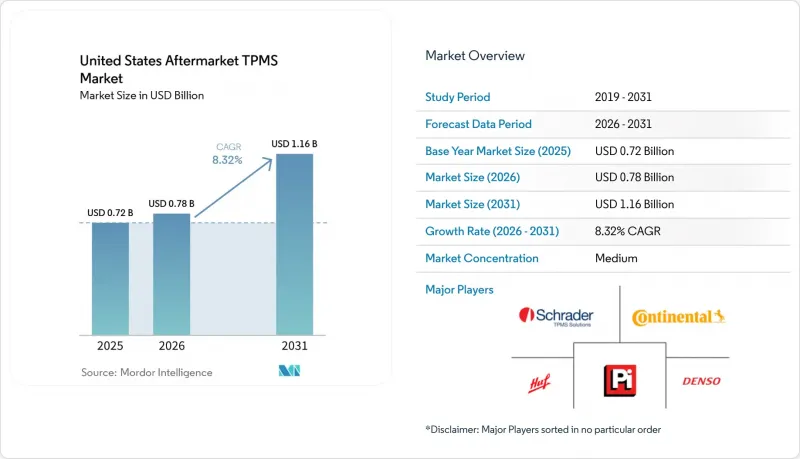

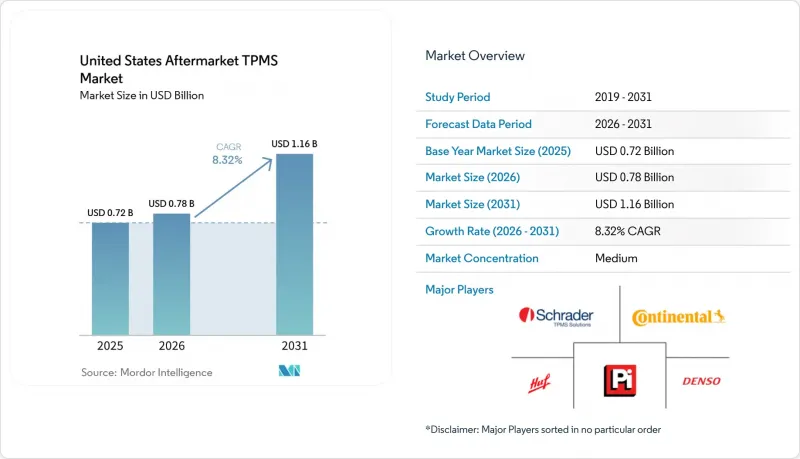

미국의 애프터마켓 TPMS 시장 규모는 2025년 7억 2,000만 달러로 평가되었습니다. 2026년 7억 8,000만 달러로 확대되어 예측 기간(2026-2031년) CAGR 8.32%를 나타내, 2031년까지 11억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 유형(직접식 TPMS 및 간접식 TPMS), 기술 통합(독립형 TPMS 장치 및 스마트/커넥티드 TPMS), 차종(승용차 및 상용차), 판매 채널(오프라인 및 온라인)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 애프터마켓 TPMS 시장 동향 및 인사이트

FMVSS 138의 시행과 센서 교체 주기

FMVSS 138은 타이어 공기압이 표시된 수치보다 현저히 낮아진 경우 바퀴별로 경고를 발령하도록 의무화하고 있으며, 이로 인해 신차에 탑재된 직접 TPMS의 우위가 확고해졌습니다. 1세대 센서는 현재 내장된 리튬 배터리의 수명이 다해가고 있어, 정기적인 타이어 정비와는 별개로 교체 수요가 발생하고 있습니다. 테슬라의 모델 3 및 Y에 영향을 미친 최근의 리콜은 규정 준수 감시가 강화되었으며, 소유주들이 신속히 센서 점검을 실시하도록 권고받고 있음을 여실히 보여주고 있습니다. 뉴욕, 펜실베이니아, 텍사스 등 일부 주에서는 차량 검사 프로그램이 제대로 작동하지 않는 TPMS를 자동으로 감지하기 때문에 규정 위반이 즉시 애프터마켓 판매로 이어지고 있습니다. 입법자들은 FAST법의 의무에 따라 변조 방지 아키텍처에 대한 검토를 진행 중이며, 향후 서비스 프로토콜을 재정의할 가능성이 있는 규정 제정을 염두에 두고 있습니다.

DIY용 TPMS 센서 및 진단 도구의 전자상거래 시장 확대

아마존 마켓플레이스에서는 리프로그래밍 도구와 GM 호환 센서의 온라인 판매가 급증하고 있어, 온라인 시장으로의 급속한 확산이 두드러지고 있습니다. Alligator사의 Sens.it RS+와 같은 범용 센서는 거의 모든 차종에 호환됩니다. 이러한 센서는 인터넷 연결 도구를 통해 펌웨어 업데이트를 수신하므로, 수리 업체는 OEM별 재고를 대폭 줄일 수 있습니다. 이러한 비용 절감은 소비자를 끌어들이지만, 데미니미스(경미) 기준에 따라 많은 소포가 연방 검사를 받지 않게 됨에 따라 위조품의 위험이 높아지고 있습니다. 이는 미국 세관 당국도 우려하고 있는 점입니다. 이러한 상황은 설치 업체에게 성장의 기회가 되는 동시에, 품질 관리 측면에서도 과제를 안겨주고 있습니다.

센서의 평균 판매 가격(ASP) 하락이 설치 업체의 이익률을 압박하고 있습니다.

애프터마켓 센서 가격은 크게 하락하고 있습니다. 예전에는 OEM 제품으로 가격이 비쌌던 것들이, 현재는 프로그래밍이 가능한 장치나 저렴한 범용 제품으로 훨씬 더 낮은 비용에 제공되고 있습니다. 업계 평균 수준의 서비스 요금을 책정하고 있는 설치 업체의 경우, 부품비와 인건비를 차감한 후의 이익을 유지하기는 어렵습니다. 이 문제는 합리적인 가격의 DIY용 리런 도구의 보급으로 인해 더욱 심각해지고 있으며, 지식이 있는 소유자가 전문가의 도움 없이도 작업을 수행할 수 있게 되었습니다. 한편, 대규모 타이어 체인점은 그 구매력을 활용해 타이어의 교차 판매를 통해 센서의 이익률 하락에 대응하고 있지만, 단독 점포는 더욱 어려운 이익률 상황에 직면해 있습니다.

부문별 분석

직접 시스템은 FMVSS 138의 휠별 정확도 요건에 따라 2025년 미국의 애프터마켓 TPMS 시장 점유율의 83.26%를 차지하며, 해당 시장에서 최대 점유율을 확보했습니다. ABS 차륜 속도 비교에 의존하는 간접 솔루션은 16.74%를 차지했으나, 비용에 민감한 소형 상용차 플릿 시장에서 2031년까지 연평균 성장률(CAGR) 8.56%를 나타낼 가능성이 있습니다.

직접 기술 분야에서는 블루투스 LE 및 원격 펌웨어 업데이트의 도입이 확대되고 있으며, 수익의 중심이 하드웨어 단말기에서 소프트웨어 구독 모델로 이동하고 있습니다. 간접적인 솔루션은 동시에 발생하는 공기압 저하나 정지 상태에서의 공기 누출을 감지할 수 없습니다는 한계로 인해, 규정 준수가 요구되는 환경에서는 직접 센서를 보조하는 역할에 그치고 있습니다.

2025년 기준으로 미국의 애프터마켓 TPMS(타이어 공기압 모니터링 시스템) 시장 점유율의 64.15%를 독립형 제품이 차지했으나, 차량 함대가 ISO 15638-23 표준을 준수하는 커넥티드 플랫폼을 도입함에 따라 현재는 점차 감소하는 추세에 있습니다. 스마트 솔루션 시장은 2031년까지 연평균 성장률(CAGR) 8.37%를 기록하며, 전체 시장 성장률을 상회할 것으로 전망됩니다.

물류 업체들은 유지보수 일정 관리에 클라우드 분석을 활용하고 있으며, 이로 인해 예기치 못한 타이어 고장이 대폭 감소했다고 보고되고 있습니다. 암호화 기술의 강화로 인해 학술 연구에서 지적되었던 개인정보 보호 문제가 해결됨에 따라, 연결형 TPMS(타이어 공기압 모니터링 시스템)는 보험 인수 부서나 기업의 컴플라이언스 팀에게 더욱 수용하기 쉬운 시스템이 되었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the united states aftermarket TPMS market size is expected to grow from USD 0.72 billion in 2025 to USD 0.78 billion in 2026 and is forecast to reach USD 1.16 billion by 2031, at a CAGR of 8.32% during the forecast period (2026-2031).

This report is Segmented by Type (Direct TPMS and Indirect TPMS), Technology Integration (Stand-Alone TPMS Units and Smart/Connected TPMS), Vehicle Type (Passenger Cars and Commercial Vehicles), and Distribution Channel (Offline and Online). The Market Forecasts are Provided in Terms of Value (USD).

United States Aftermarket TPMS Market Trends and Insights

FMVSS 138 Enforcement and Sensor Replacement Cycles

FMVSS 138 mandates a per-wheel warning when tire pressure drops significantly below placard levels, solidifying the dominance of direct TPMS in new vehicles. Sensors from the first wave are now outlasting their sealed lithium batteries, leading to a replacement demand that's independent of regular tire service events. A recent recall affecting Tesla's Model 3 and Y underscores the compliance scrutiny nudging owners to promptly service sensors. In states like New York, Pennsylvania, and Texas, inspection programs automatically flag non-functional TPMS, turning regulatory non-compliance into instant aftermarket sales. Legislators, under the FAST Act mandate, are delving into tamper-resistant architectures, eyeing potential rulemaking that could redefine future service protocols.

E-commerce Expansion for DIY TPMS Sensors and Diagnostic Tools

Amazon's marketplace highlights a surge in online sales for a relearn tool and GM-compatible sensors, underscoring rapid online penetration . Universal sensors, like Alligator's Sens.it RS+, cover nearly all vehicles. These sensors receive firmware updates through web-connected tools, allowing repair shops to significantly reduce their OEM-specific inventory. While these cost savings attract consumers, the de minimis threshold means many small parcels can skip federal inspection, heightening the risk of counterfeits, a concern noted by U.S. Customs. This dynamic presents both growth opportunities and quality-control hurdles for installers.

Declining Sensor ASPs Squeezing Installer Margins

Aftermarket sensor prices have decreased significantly. Once priced higher at OEMs, they now include programmable units and budget generics at much lower costs. Installers, with an industry-average service ticket, find it challenging to maintain profits after accounting for parts and labor. This challenge is further intensified by the availability of affordable DIY relearn tools, which enable savvy owners to bypass professional assistance. While high-volume tire chains utilize their purchasing power and cross-sell tires to counteract shrinking sensor margins, single-location shops face tighter profit margins.

Other drivers and restraints analyzed in the detailed report include:

- Fleet Telematics Retrofits Among Light Commercial Vehicle Operators

- Insurance-Linked Discounts for Connected-TPMS Adoption

- Technical Skill Gap at Independent Repair Shops

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Direct systems captured 83.26% of the United States aftermarket TPMS market share in 2025, owing to FMVSS 138's per-wheel accuracy requirements, securing the largest share of the United States aftermarket TPMS market. Indirect solutions, reliant on ABS wheel-speed comparisons, held 16.74% yet may grow 8.56% CAGR through 2031 among cost-sensitive light-commercial fleets.

Direct technology continues to adopt Bluetooth LE and remote firmware updates, shifting revenue emphasis from hardware units to software subscriptions. Indirect options remain limited by their inability to detect simultaneous pressure loss or stationary leaks, relegating them to a secondary role to direct sensors in compliance-driven environments.

Stand-alone configurations accounted for 64.15% of the United States aftermarket TPMS market share in 2025, but are now in gradual decline as fleets adopt connected platforms aligned with ISO 15638-23. Smart solutions are projected to outpace overall growth with an 8.37% CAGR through 2031.

Logistics operators harness cloud analytics for maintenance scheduling, reporting a significant drop in unplanned tire failures. Upgraded encryption addresses privacy issues highlighted in academic studies, rendering connected TPMS (Tire Pressure Monitoring Systems) more palatable for insurance underwriting and corporate compliance teams.

List of Companies Covered in this Report:

- Sensata Technologies (Schrader)

- Continental AG

- Huf Hulsbeck & Furst

- Pacific Industrial

- DENSO Corp

- Alligator Ventilfabrik

- Dill Air Controls

- Standard Motor Products

- Autel Intelligent Tech.

- Bartec USA

- ATEQ TPMS Tools

- Orange Electronic

- Steelmate

- Haltec Corporation

- Myers Tire Supply

- Cub Elecparts

- Nonda Inc.

- PressurePro

- BorgWarner (Servoflex)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandated TPMS Replacement Interval Under NHTSA Part 563 (2025)

- 4.2.2 Surging E-Commerce Volumes For DIY TPMS Sensors & Tools

- 4.2.3 Growing Fleet Telematics Retrofits Among LCV Operators

- 4.2.4 Rise in ADAS Recalibration Bundling At Tire-Service Chains

- 4.2.5 Insurance-Linked Discounts For Connected-TPMS Adoption

- 4.2.6 Lithium-Free MEMS Pressure-Sensor Breakthroughs

- 4.3 Market Restraints

- 4.3.1 Declining Sensor ASPs Squeezing Installer Margins

- 4.3.2 Increasing Competition From Low-Cost Chinese Clones

- 4.3.3 Technical Skill Gap At Independent Repair Shops

- 4.3.4 EV solid-State Tires With Embedded Self-Inflation Tech

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power - Suppliers

- 4.7.3 Bargaining Power - Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Type

- 5.1.1 Direct TPMS

- 5.1.2 Indirect TPMS

- 5.2 By Technology Integration

- 5.2.1 Stand-alone TPMS Units

- 5.2.2 Smart/Connected TPMS

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.1.1 Hatchbacks

- 5.3.1.2 Sedans

- 5.3.1.3 Sport Utility Vehicles (SUVs) & Multi-Utility Vehicles (MUVs)

- 5.3.2 Commercial Vehicles

- 5.3.2.1 Light Commercial Vehicles

- 5.3.2.2 Medium & Heavy Commercial Vehicles

- 5.3.2.3 Buses & Coaches

- 5.3.1 Passenger Cars

- 5.4 By Distribution Channel

- 5.4.1 Offline

- 5.4.2 Online

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Sensata Technologies (Schrader)

- 6.4.2 Continental AG

- 6.4.3 Huf Hulsbeck & Furst

- 6.4.4 Pacific Industrial

- 6.4.5 DENSO Corp

- 6.4.6 Alligator Ventilfabrik

- 6.4.7 Dill Air Controls

- 6.4.8 Standard Motor Products

- 6.4.9 Autel Intelligent Tech.

- 6.4.10 Bartec USA

- 6.4.11 ATEQ TPMS Tools

- 6.4.12 Orange Electronic

- 6.4.13 Steelmate

- 6.4.14 Haltec Corporation

- 6.4.15 Myers Tire Supply

- 6.4.16 Cub Elecparts

- 6.4.17 Nonda Inc.

- 6.4.18 PressurePro

- 6.4.19 BorgWarner (Servoflex)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment