|

시장보고서

상품코드

2062300

유럽의 애프터마켓 TPMS : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Aftermarket TPMS - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

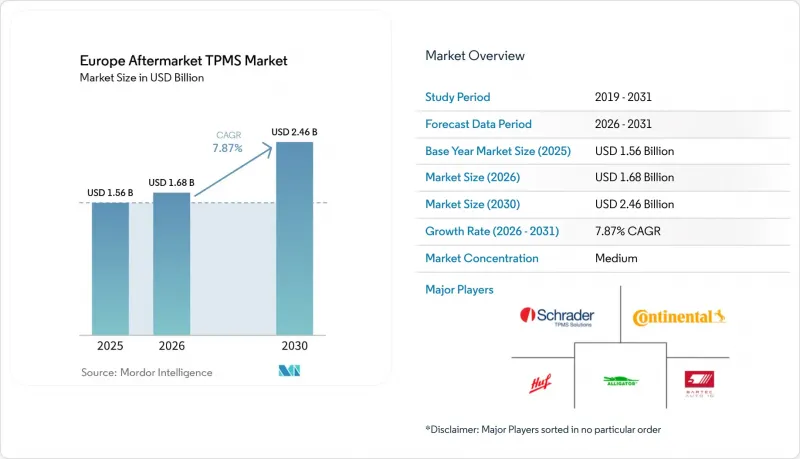

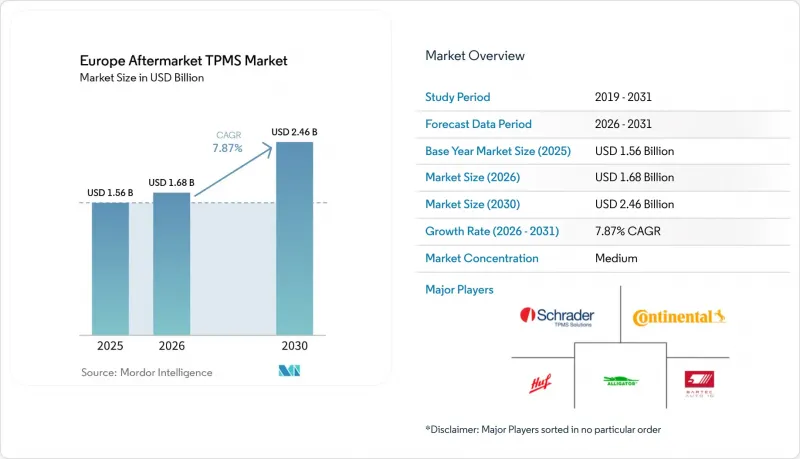

유럽의 애프터마켓 TPMS 시장 규모는 2025년 15억 6,000만 달러로 평가되었습니다. 2026년 16억 8,000만 달러로 확대되어 2031년까지 24억 6,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 7.87%를 나타낼 것으로 전망됩니다.

본 보고서는 유형(직접식 TPMS 및 간접식 TPMS), 기술 통합(독립형 TPMS 장치 및 스마트/커넥티드 TPMS), 차종(승용차 및 상용차), 유통 채널(오프라인 및 온라인), 지역(독일, 영국, 프랑스, 이탈리아, 스페인 및 기타 유럽)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽의 애프터마켓 TPMS 시장 동향 및 분석

차량의 노후화로 인해 센서 교체 수요가 장기화되고 있습니다.

유럽의 승용차 평균 연식은 증가하고 있으며, 일부 지역에서는 차량의 노후화가 심각하다고 보고되고 있습니다. 이러한 추세로 인해 많은 1세대 직접 센서의 사용 기간이 일반적인 배터리 수명을 초과하는 상황이 발생하고 있습니다. 수리 비용을 절감하기 위해, 비용 효율성을 중시하는 지역의 정비 공장에서는 범용 프로그래밍 가능 센서의 사용이 증가하고 있습니다. 이러한 접근 방식은 당분간 지속될 것으로 예상되는 지속적인 교환 수요를 뒷받침하는 것입니다.

EU 규정 ECE 661/2009에 따른 교체 주기 촉진

독일, 프랑스, 네덜란드에서는 정기 점검 시 정상적으로 작동하지 않는 TPMS가 부적합으로 간주되게 되었으며, 이러한 규제가 서비스 제공업체와 제조업체에게 확실한 수익원이 되고 있습니다. 이러한 규제의 철저한 이행으로 차량의 안전 기준 준수가 보장됨에 따라, TPMS의 유지보수 및 교체 수요가 증가하고 있습니다. UNECE R141의 적용 범위가 트럭 및 트레일러로 확대된 것은 제2의 규정 준수 물결을 의미하며, 경고 임계값을 충족할 수 있는 직접 TPMS에 이점을 가져다줍니다. 이러한 움직임에 따라, 차량 운영 업체와 OEM이 제재를 피하고 운영상의 안전성을 높이기 위해 규정 준수를 우선시하게 될 것이므로, 시장에 성장 기회가 생길 것으로 예측됩니다.

릴란/프로그래밍에 수반되는 고비용의 센서 및 인건비

폴란드에서는 계기판의 경고 표시로 문제가 나타났음에도 불구하고, 많은 고객이 수리를 미루고 있습니다. 그 주된 이유는 특히 인건비나 프로그래밍 비용을 고려할 때 센서 교체에 막대한 비용이 들기 때문입니다. 게다가 BMW나 테슬라의 시스템에 적용된 암호화 기술로 인해 정비소는 OEM 부품을 구매하거나 고가의 장비에 투자할 수밖에 없게 되었으며, 이로 인해 서비스 요금이 더욱 상승하고 있습니다.

부문별 분석

2025년, 유럽의 애프터마켓에서 직접 TPMS는 시장 점유율의 74.38%를 차지했습니다. 이는 UNECE 규정에 따라 요구되는 실시간 및 휠별 경보 기능에 따른 것입니다. 한편, 가격이 40-50% 저렴한 간접 시스템은 특히 남유럽에서 2014년 이전의 밴 운영업체들이 저비용으로 규정 준수를 추구함에 따라 연평균 성장률(CAGR) 8.14%를 기록하며 성장하고 있습니다.

예측 기간 동안 알고리즘 개선으로 오감지가 감소함에 따라, EU TPMS 애프터마켓에서 간접식 TPMS 시장이 가속화될 것으로 전망됩니다. 그러나 절대압 측정 시 정확도 문제로 인해, 도입은 비용을 중시하는 선단에 한정되어 있습니다. NXP의 AEC-Q100 인증 NTM88K 등 반도체 기술의 발전에 힘입어, 직접식 TPMS는 대형 차량 분야에서 장기적인 표준으로 자리 잡아가고 있으며, 유럽의 애프터마켓 TPMS 시장에서 직접식 솔루션의 주도적 입지를 강화하고 있습니다.

2025년, 유럽의 애프터마켓 TPMS 시장 규모 중 57.19%를 독립형 밸브가 차지했습니다. 이는 설치 업체가 텔레매틱스 게이트웨이와의 페어링이 필요 없는 보다 간단한 재학습 과정을 선호했기 때문입니다. 슈레더(Schrader)와 후프(Huf)의 범용 SKU는 재고 비용을 낮게 유지함으로써 독립 정비소의 지지를 계속 얻고 있습니다.

커넥티드 TPMS의 매출액은 ESG 중심의 데이터 보고 및 예측 유지보수 계약을 배경으로 연평균 성장률(CAGR) 8.05%를 나타낼 전망입니다. 차량 1대당 월간 구독 요금이 더 저렴해지면, 유럽의 애프터마켓 TPMS 시장에서 커넥티드 키트의 점유율이 크게 확대될 가능성이 있습니다. 센서 수명 주기 도중에 교체하는 것을 꺼리는 차량 관리자들은 배터리 수명을 대폭 개선하는 NXP의 UWB 아키텍처에 매력을 느낄 수도 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the european aftermarket market size is projected to grow from USD 1.56 billion in 2025 to USD 1.68 billion in 2026, and is forecast to reach USD 2.46 billion by 2031, growing at a CAGR of 7.87% from 2026 to 2031.

This report is Segmented by Type (Direct TPMS and Indirect TPMS), Technology Integration (Stand-Alone TPMS Units and Smart/Connected TPMS), Vehicle Type (Passenger Cars and Commercial Vehicles), Distribution Channel (Offline and Online), and Geography (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

Europe Aftermarket TPMS Market Trends and Insights

Aging Vehicle Parc Prolongs Sensor Replacement Demand

The average age of passenger cars in Europe has increased, with some regions reporting significantly older vehicles. This trend has led many first-generation direct sensors to exceed their typical battery life. To maintain affordability in repairs, workshops in cost-sensitive areas are increasingly using universal programmable sensors. This approach supports a sustained replacement trend expected to continue for the foreseeable future.

EU Regulation ECE 661/2009 Replacement-Cycle Pull

In Germany, France, and the Netherlands, periodic inspections now treat non-functional TPMS as failures, turning regulation into a reliable revenue source for service providers and manufacturers. This regulatory enforcement ensures that vehicles comply with safety standards, driving demand for TPMS maintenance and replacement. The extension of UNECE R141 to trucks and trailers signals a second compliance wave, benefiting direct TPMS that can meet the alert threshold. This development is expected to create growth opportunities in the market as fleet operators and OEMs prioritize compliance to avoid penalties and enhance operational safety.

High Sensor and Labor Cost for Relearn/Programming

In Poland, many customers delay repairs even when dashboard warnings signal issues, primarily because replacing sensors is costly, especially when labor and programming are factored in. Additionally, encryption on BMW and Tesla systems compels workshops to either purchase OEM parts or invest in advanced tools, further driving up service bills.

Other drivers and restraints analyzed in the detailed report include:

- Rising Consumer Focus on Tire Safety and Fuel Economy

- OTA-upgradeable Connected TPMS Kits

- EV-Specific High-Pressure Tires Create Compatibility Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Direct TPMS commanded 74.38% of the European aftermarket market share in 2025, owing to real-time, wheel-specific alerts demanded by UNECE rules. Indirect systems priced 40-50% lower are growing at an 8.14% CAGR as operators of pre-2014 vans seek low-cost compliance, particularly in Southern Europe.

Over the forecast period, the EU TPMS aftermarket market for indirect TPMS is projected to accelerate as algorithm refinements reduce false positives. Yet, gaps in absolute-pressure measurement limit uptake to cost-sensitive fleets. Semiconductor advances, such as NXP's AEC-Q100-qualified NTM88K, are cementing direct TPMS as the long-term default across heavy-duty vehicles, reinforcing the leadership position of direct solutions in the European aftermarket market.

Stand-alone valves held 57.19% of the European aftermarket TPMS market size in 2025 as installers favored simpler re-learn processes that do not require pairing with telematics gateways. Universal-fit SKUs from Schrader and Huf keep inventory overhead low, sustaining loyalty among independent workshops.

Connected TPMS revenue will advance at an 8.05% CAGR on the back of ESG-driven data reporting and predictive maintenance contracts. The European aftermarket TPMS market share for connected kits could grow significantly if subscription prices become more affordable per vehicle per month. Fleet managers, hesitant about mid-cycle sensor swaps, may find NXP's UWB architecture appealing, offering a notable improvement in battery life.

List of Companies Covered in this Report:

- Continental AG

- Sensata Technologies Inc.- Schrader

- Huf Hulsbeck & Furst GmbH

- Alligator Ventilfabrik GmbH

- ATEQ TPMS Tools

- Bartec Auto ID

- Autel Intelligent Technology

- Cub Elecparts Inc.

- Orange Electronic Co.

- Denso Corporation

- Pacific Industrial Co.

- ZF TRW Automotive

- Valeo SA

- Haltec Corporation

- Infitronic Technology

- Steelmate Automotive

- NXP Semiconductors

- Maxwell Products (TPMS Warehouse)

- Ridecell Fleet-TPMS

- Pricol Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Vehicle Parc Prolongs Sensor Replacement Demand

- 4.2.2 EU Regulation ECE 661/2009 Replacement-Cycle Pull

- 4.2.3 Rising Consumer Focus on Tire Safety and Fuel-Economy

- 4.2.4 Fleet-Wide ESG Reporting Needs Real-Time Pressure Data

- 4.2.5 OTA-Upgradeable Connected TPMS Kits as New Revenue Stream

- 4.2.6 E-Commerce Parts Channels Widen Access to Universal Kits

- 4.3 Market Restraints

- 4.3.1 High Sensor and Labor Cost for Relearn/Programming

- 4.3.2 EV-Specific High-Pressure Tires Create Compatibility Gaps

- 4.3.3 Accuracy Issues with Indirect TPMS Erode Confidence

- 4.3.4 Cyber-Risks in Connected Sensors Raise Recall Liability

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Type

- 5.1.1 Direct TPMS

- 5.1.2 Indirect TPMS

- 5.2 By Technology Integration

- 5.2.1 Stand-alone TPMS Units

- 5.2.2 Smart/Connected TPMS

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.1.1 Hatchbacks

- 5.3.1.2 Sedans

- 5.3.1.3 Sports Utility Vehicles (SUVs) & Multi-Utility Vehicles (MUVs)

- 5.3.2 Commercial Vehicles

- 5.3.2.1 Light Commercial Vehicles

- 5.3.2.2 Medium and Heavy Commercial Vehicles

- 5.3.2.3 Buses and Coaches

- 5.3.1 Passenger Cars

- 5.4 By Distribution Channel

- 5.4.1 Offline

- 5.4.2 Online

- 5.5 By Country

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Continental AG

- 6.4.2 Sensata Technologies Inc.- Schrader

- 6.4.3 Huf Hulsbeck & Furst GmbH

- 6.4.4 Alligator Ventilfabrik GmbH

- 6.4.5 ATEQ TPMS Tools

- 6.4.6 Bartec Auto ID

- 6.4.7 Autel Intelligent Technology

- 6.4.8 Cub Elecparts Inc.

- 6.4.9 Orange Electronic Co.

- 6.4.10 Denso Corporation

- 6.4.11 Pacific Industrial Co.

- 6.4.12 ZF TRW Automotive

- 6.4.13 Valeo SA

- 6.4.14 Haltec Corporation

- 6.4.15 Infitronic Technology

- 6.4.16 Steelmate Automotive

- 6.4.17 NXP Semiconductors

- 6.4.18 Maxwell Products (TPMS Warehouse)

- 6.4.19 Ridecell Fleet-TPMS

- 6.4.20 Pricol Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet Need Assessment