|

시장보고서

상품코드

2063432

기업 에이전트 인프라 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Enterprise Agent Infrastructure - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

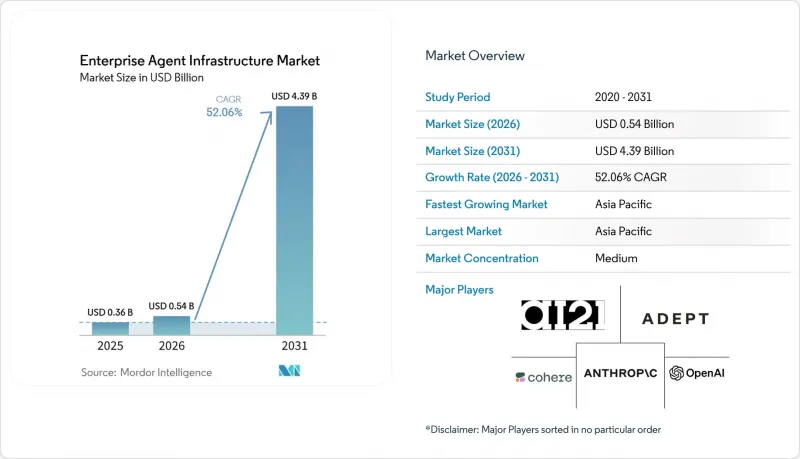

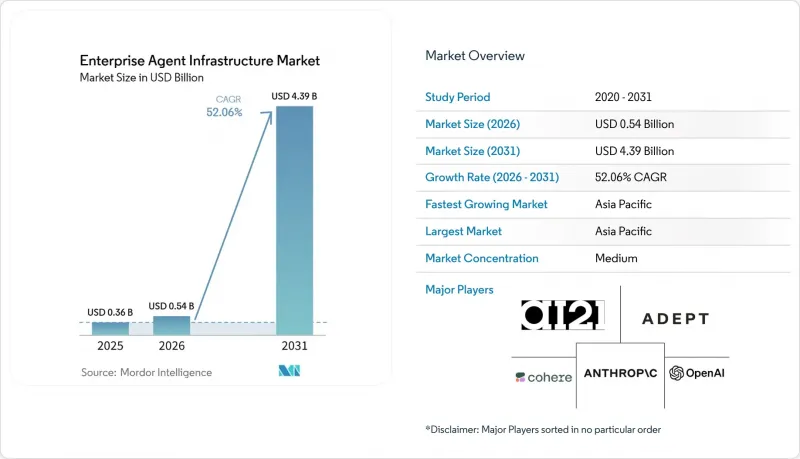

Mordor Intelligence에 의하면, 기업 에이전트 인프라 시장 규모는 2025년에 3억 6,000만 달러로 평가되었고, 2026년에 5억 4,000만 달러로 추정되고, 2031년까지 43억 9,000만 달러에 이를 것으로 예측됩니다. 2026-2031년 CAGR 52.06%로 성장할 전망입니다.

본 보고서는 도입 모델별(클라우드, 온프레미스, 하이브리드), 구성 요소별(소프트웨어 및 서비스), 기업 규모별(대기업, 중소기업), 업종별(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 헬스케어 및 생명과학, 소매 및 전자상거래, 제조, 기타) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 기업 에이전트 인프라 시장 동향 및 인사이트

클라우드 네이티브 AI 인프라의 급속한 확산

기업들은 에이전트의 워크로드를 탄력적인 클라우드 환경으로 이전하고 있으며, 도입 주기를 수 분기에서 수 주일로 단축하고 있습니다. Databricks는 2025년에 연간 매출 40억 달러를 돌파했으며, 이 중 10억 달러 이상은 오케스트레이션, 벡터 스토리지, 거버넌스를 단일 플랫폼에 통합한 AI 제품에서 발생할 것으로 예측됩니다. 현재 퍼블릭 클라우드 제공업체들은 GPU 접근, 관리형 벡터 데이터베이스, 모니터링 대시보드를 제공하고 있으며, 이로 인해 전환 비용이 발생하고 벤더 종속성이 심화되고 있습니다. 퍼블릭 클라우드에만 의존할 수 없는 규제 산업에서는 하이브리드 스택이 채택되고 있으며, 이는 산업별 인프라 전략의 양극화를 반영하고 있습니다. 마이크로서비스 아키텍처 덕분에 단계적인 배포가 가능해졌으며, IT 팀은 확장 전에 투자 대비 효과를 검증할 수 있어 도입이 가속화되고 있습니다.

대화형 AI 도입 급증

대화형 에이전트는 기본적인 챗봇에서 트랜잭션 실행 및 백엔드 시스템 오케스트레이션이 가능한 컨텍스트 인식형 어시스턴트로 진화했습니다. Anthropic사의 'Claude Code'는 2026년 2월 연간 매출 25억 달러를 돌파했으며, 기업용 구독자 수는 2개월도 채 되지 않아 4배로 증가했습니다. 유럽 기업들은 데이터 주권 관련 규제 요건을 충족하기 위해 Mistral사의 Magistral 모델 등, 지역에 기반을 둔 대안 솔루션을 모색하고 있습니다. 플러그인을 지원하는 'Claude Cowork'의 등장은 투자자들이 자율형 대화 에이전트가 기존의 SaaS 수익원을 잠식할 가능성이 있음을 인식하게 만들었고, 이로 인해 레거시 소프트웨어 주식에 대한 광범위한 매도세가 촉발되었습니다. 현재 조직은 추론 품질, 컨텍스트 윈도우 길이, 지연 시간, 그리고 100만 토큰당 비용을 기준으로 에이전트 플랫폼을 평가했습니다.

높은 계산 비용과 에너지 소비

상시 가동되는 에이전트는 일회성 모델 훈련보다 추론 비용이 더 많이 드는 경향이 있어 IT 예산을 압박하고 있습니다. 기업들이 상시 가동형 에이전트를 운영함에 따라, 일본의 데이터센터는 국내 전력 수요를 최대 20%까지 끌어올릴 것으로 예측됩니다. 모델 공급업체들은 Mistral의 경우 토큰 100만 개당 2달러(GPT-4o의 5달러 대비)라는 공격적인 가격 인하로 대응하고 있어, 멀티 모델 라우팅이 매력적인 선택지로 떠오르고 있습니다. 일부 조직에서는 일상적인 추론 작업에는 Mistral을, 복잡한 작업에는 프리미엄 모델을 조합하여 65%의 비용 절감을 달성했다고 보고되고 있습니다. 그러나 GPU 부족과 에너지 가격 급등이 여전히 확장성을 제약하고 있습니다. 또한, 일본의 도시 지역에서 토지 부족과 냉각 용량 부족으로 인해 하이퍼스케일 시설이 최종 사용자와 멀리 떨어진 곳에 설치될 수밖에 없게 되어, 지연 시간의 문제가 발생하고 특정 이용 사례가 제한될 가능성이 있습니다.

부문별 분석

2026년에는 하이브리드 아키텍처가 기업 에이전트 인프라 시장에서 점유율을 확대할 것으로 예상되며, 2031년까지 연평균 성장률(CAGR) 27.64%로 성장할 것으로 전망됩니다. 2025년 시점에서도 클라우드는 여전히 기업 에이전트 인프라 시장 점유율의 64.49%를 차지하고 있으며, 이는 Pinecone의 서버리스 추론 서비스와 Databricks의 통합 스택의 매력이 반영된 결과입니다. 방위 및 생명과학 등 규제 대상 분야에서는 기밀 데이터 관리를 위해 온프레미스 환경에서의 통제가 필요하지만, 한편으로는 훈련 및 추론을 위한 버스트 용량도 필요로 합니다.

하이브리드 모델을 통해 기업은 기밀성이 높은 워크로드를 사내 데이터센터에 유지하면서, 연산 부하가 높은 작업은 퍼블릭 클라우드의 GPU로 오프로드할 수 있어 비용과 규정 준수를 모두 최적화할 수 있습니다. Cohere가 Oracle이나 Dell과 같은 고객을 대상으로 펼치는 '온프레미스 우선' 전략과 5억 달러 규모의 자금 조달 성공은 주권을 고려한 도입이 앞으로도 매우 중요하다는 투자자들의 확신을 보여줍니다. 후지쯔와 NVIDIA의 CPU-GPU 스택 관련 제휴는 On-Premise 환경의 거버넌스와 클라우드 기반의 버스트 탄력성을 결합하려는 노력을 강조하는 것입니다.

서비스 시장은 연평균 성장률(CAGR) 26.23%로 확대될 것으로 예상되며, 이는 업종을 불문하고 통합, 미세 조정 및 가시성 솔루션에 대한 수요가 증가하고 있음을 반영합니다. 이러한 성장은 고도의 서비스를 제공함으로써 업무 효율을 높이고 업무 흐름을 합리화하려는 기업들에 의해 주도되고 있습니다. 한편, 소프트웨어는 2025년 기업 에이전트 인프라 시장 규모의 44.39%를 차지했으며, 원활한 운영과 데이터 관리를 실현하는 데 필수적인 오케스트레이션 프레임워크, 벡터 데이터베이스, API 액세스 등의 핵심 도구를 제공합니다.

2만 5,000명의 인력을 보유한 액센츄어의 Databricks 비즈니스 그룹은 시스템 통합사업자들이 소프트웨어 라이선스에 거버넌스, 교육, 지속적인 최적화 등의 추가 서비스를 묶어 제공하는 추세를 강조하고 있습니다. 이러한 접근 방식을 통해 기업은 복잡한 도입 요건을 충족하면서도 소프트웨어 투자의 가치를 극대화할 수 있습니다. 예를 들어, Databricks의 AppKit은 반복적인 코드를 줄여 개발을 간소화하지만, 규제 대상 시스템을 도입할 때는 규정 준수 및 효율성을 확보하기 위해 여전히 전문 서비스가 필요합니다. 기업들은 원활한 업그레이드, 안전한 데이터 파이프라인, 그리고 검색 매개변수 최적화를 가능하게 하는 관리형 서비스를 선택하는 경향이 점점 더 강해지고 있습니다. 이러한 서비스를 통해 사내 팀은 플랫폼 인프라의 복잡한 관리에 시간을 할애하지 않고 자사의 전문 지식 활용에 집중할 수 있게 되어, 궁극적으로 더 나은 성과와 혁신을 촉진합니다.

지역별 분석

2025년 북미는 기업 에이전트 인프라 시장의 25.82%를 차지했습니다. 이는 GPU의 풍부한 공급, 연방 정부의 조달 인센티브, 그리고 벤처 캐피털의 집중 투자로 인한 혜택을 받은 결과입니다. 기업들은 클라우드의 경제성을 활용하고 있지만, 전력 비용 상승에 직면해 있으며, 이로 인해 하이퍼스케일러들은 대륙 내 저비용 지역에 데이터센터를 구축하고 있습니다. 주 차원의 개인정보 보호법 등 규제 당국의 감독으로 인해, 조직들은 세밀한 데이터 거처 관리를 실시할 수밖에 없게 되었습니다. 이는 복잡성을 가중시킬 뿐만 아니라, 궁극적으로는 규정 준수 요건을 충족하는 에이전트 프레임워크에 대한 수요를 촉진하게 될 것입니다.

아시아태평양은 일본, 중국, 인도, 한국의 견인에 힘입어 2031년까지 연평균 성장률(CAGR) 24.26%로 성장할 것으로 전망됩니다. 2026년 3월 조사에 따르면, 매출액 1조 엔(약 67억 달러)을 넘는 일본 기업의 80%가 생성형 AI를 도입하고 있으며, 이는 자동화에 대한 상향식 지시를 시사합니다. 일본의 데이터센터 용량은 2030년까지 2배, 2040년까지 9배로 확대되어야 하지만, 전력 인프라 확충이 지연될 경우 인프라 병목 현상이 성장의 걸림돌이 될 수 있습니다. 인도 및 동남아시아 국가들에서는 미국과 중동의 투자자들이 주도하는 대규모 투자에 힘입어, 다양한 언어 시장에 대응하기 위해 다국어 모델이 도입되고 있습니다.

유럽의 전망은 감사 증거와 투명성 요건을 부과하는 'AI법'에 의해 형성되고 있습니다. 규정 준수에 따른 부담이 조기 도입을 지연시키는 반면, 명확한 지침은 궁극적으로 대기업의 조달 리스크를 경감시킵니다. Mistral이나 Aleph Alpha와 같은 벤더들은 데이터 소재지 및 설명 가능성을 차별화 요인으로 내세우며, 지역 규제를 준수하는 대안으로 자리매김하고 있습니다. 중동 및 아프리카에서는 아랍어권 시장에 대응하기 위해, 특히 OpenAI와 G42의 제휴를 비롯한 소버린 클라우드 파트너십을 적극 활용하고 있습니다. 한편, 남미에서의 활동은 브라질과 아르헨티나에 집중되어 있으며, 이들 국가에서는 대화형 에이전트가 포르투갈어와 스페인어로 제공되는 고객 지원을 자동화하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the enterprise agent infrastructure market size is projected to be USD 0.36 billion in 2025, USD 0.54 billion in 2026, and reach USD 4.39 billion by 2031, growing at a CAGR of 52.06% from 2026 to 2031.

This report is Segmented by Deployment Model (Cloud, On-Premise, and Hybrid), Component (Software and Services), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (IT and Telecom, BFSI, Healthcare and Life Sciences, Retail and ECommerce, Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Enterprise Agent Infrastructure Market Trends and Insights

Rapid Adoption of Cloud-Native AI Infrastructure

Enterprises are lifting and shifting agent workloads into elastic cloud environments, reducing deployment cycles from quarters to weeks. Databricks surpassed USD 4 billion annualized revenue in 2025, with more than USD 1 billion coming from AI products that bundle orchestration, vector storage, and governance on a unified platform. Public cloud providers now offer GPU access, managed vector databases, and monitoring dashboards, creating switching costs that deepen vendor lock-in. Regulated sectors that cannot rely solely on public clouds are embracing hybrid stacks, reflecting a bifurcation of infrastructure strategies by industry. Microservice architectures enable incremental rollouts, allowing IT teams to validate return on investment before scaling and thereby accelerating adoption.

Surge in Conversational AI Deployments

Conversational agents have evolved from basic chatbots into context-aware assistants capable of executing transactions and orchestrating back-end systems. Anthropic's Claude Code passed a USD 2.5 billion run rate in February 2026, with enterprise subscriptions quadrupling in less than two months. European firms are pursuing regional alternatives, such as Mistral's Magistral models, to meet data-sovereignty mandates. The debut of Claude Cowork with plug-ins triggered a broad sell-off in legacy software stocks as investors recognized that autonomous conversational agents could cannibalize traditional SaaS revenue streams. Organizations now benchmark agent platforms on reasoning quality, context-window length, latency, and cost per million tokens.

High Compute Costs and Energy Consumption

Continuous-running agents often incur higher inference expenses than one-time model training, tightening IT budgets. Japanese data centers will lift national electricity demand by up to 20% as enterprises run always-on agents. Model vendors are responding through aggressive price cuts, such as Mistral's USD 2 per million tokens versus GPT-4o's USD 5, making multi-model routing attractive. Organizations report 65% cost savings by combining Mistral for routine inference with premium models for complex tasks, yet GPU scarcity and rising energy prices still constrain scalability. Japan's shortage of urban land and cooling capacity is pushing hyperscale facilities far from end users, creating latency trade-offs that could limit certain use cases.

Other drivers and restraints analyzed in the detailed report include:

- Increased Investment in Autonomous IT Agents

- Emergence of Vector Database Interoperability Standards

- Data Privacy Regulations Limiting Orchestration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid architectures accounted for a growing slice of the Enterprise Agent Infrastructure market in 2026 and are forecast to expand at a 27.64% CAGR through 2031. Cloud still represented 64.49% of the Enterprise Agent Infrastructure market share in 2025, reflecting the appeal of serverless inference services from Pinecone and unified stacks from Databricks. Regulated sectors such as defense and life sciences require on-premise control for sensitive data, yet they also need burst capacity for training and inference.

Hybrid models let enterprises keep confidential workloads in private data centers while offloading compute-intensive tasks to public-cloud GPUs, optimizing both cost and compliance. Cohere's on-premises-first strategy with customers Oracle and Dell, and its USD 500 million raise, signal investor conviction that sovereignty-friendly deployments will remain pivotal. Fujitsu's partnership with NVIDIA on CPU-GPU stacks underscores efforts to blend on-premise governance with cloud-burst elasticity.

Services are projected to expand at a 26.23% CAGR, reflecting the growing need for integration, fine-tuning, and observability solutions across industries. This growth is driven by enterprises seeking to enhance operational efficiency and streamline workflows through advanced service offerings. Software, on the other hand, accounted for 44.39% of the Enterprise Agent Infrastructure market size in 2025, providing essential tools such as orchestration frameworks, vector databases, and API access, which are critical for enabling seamless operations and data management.

Accenture's 25,000-person Databricks business group highlights the trend of system integrators bundling software licenses with additional services like governance, training, and continuous optimization. This approach ensures that enterprises can maximize the value of their software investments while addressing complex deployment requirements. For instance, Databricks' AppKit simplifies development by reducing boilerplate code; however, regulated deployments still necessitate professional services to ensure compliance and efficiency. Enterprises are increasingly opting for managed services that facilitate smooth upgrades, secure data pipelines, and optimize retrieval parameters. These services allow internal teams to concentrate on leveraging their domain expertise rather than managing the intricacies of platform infrastructure, ultimately driving better outcomes and innovation.

Geography Analysis

North America commanded 25.82% of the Enterprise Agent Infrastructure market in 2025, benefiting from dense GPU availability, federal procurement incentives, and venture capital concentration. Enterprises leverage favorable cloud economics but face rising electricity costs, prompting hyperscalers to locate data centers in lower-cost regions within the continent. Regulatory scrutiny, such as state-level privacy statutes, forces organizations to implement granular data-residency controls that add complexity yet ultimately stimulate demand for compliance-ready agent frameworks.

Asia-Pacific is forecast to expand at a 24.26% CAGR through 2031, propelled by Japan, China, India, and South Korea. A March 2026 survey reported that 80% of Japanese firms with revenue above JPY 1 trillion (USD 6.7 billion approximately) had deployed generative AI, signaling top-down mandates for automation. Japan's data-center capacity must double by 2030 and increase ninefold by 2040, exposing infrastructure bottlenecks that could moderate growth if power upgrades lag. India and Southeast Asian economies adopt multilingual models to serve diverse linguistic markets, supported by hyperscale investments from U.S. and Middle Eastern investors.

Europe's outlook is shaped by the AI Act, which imposes audit-trail and transparency requirements. While compliance overhead slows early adoption, clear guardrails ultimately de-risk procurement for large enterprises. Vendors such as Mistral and Aleph Alpha position themselves as regionally compliant options, differentiating on data residency and explainability. The Middle East and Africa region leverages sovereign cloud partnerships, most notably the OpenAI-G42 alliance, to serve Arabic-language markets, while South America's activity centers on Brazil and Argentina, where conversational agents automate Portuguese and Spanish customer support.

- OpenAI OpCo, LLC

- Anthropic PBC

- Cohere Inc.

- AI21 Labs Ltd.

- Adept AI Labs, Inc.

- Reka AI, Inc.

- LangChain Inc.

- Pinecone Systems, Inc.

- Weaviate BV

- Hugging Face SAS

- Mistral AI SAS

- Aleph Alpha GmbH

- Stability AI Ltd.

- Scale AI, Inc.

- Anyscale, Inc.

- Replit, Inc.

- LlamaIndex LLC

- Contextual AI, Inc.

- Runway AI, Inc.

- Databricks, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of Cloud-Native AI Infrastructure

- 4.2.2 Surge in Conversational AI Deployments

- 4.2.3 Increased Investment in Autonomous IT Agents

- 4.2.4 Emergence of Vector Database Interoperability Standards

- 4.2.5 Rise of Compliance-Ready Agent Frameworks for Regulated Industries

- 4.2.6 On-Device AI Accelerators Enabling Edge Agents

- 4.3 Market Restraints

- 4.3.1 High Compute Costs and Energy Consumption

- 4.3.2 Data Privacy Regulations Limiting Orchestration

- 4.3.3 Fragmentation of Agent Protocol Standards

- 4.3.4 Scarcity of Talent for Multi-Agent Alignment and Safety

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Component

- 5.2.1 Software

- 5.2.2 Services

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Industry Vertical

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Retail and eCommerce

- 5.4.5 Manufacturing

- 5.4.6 Energy and Utilities

- 5.4.7 Government and Public Sector

- 5.4.8 Other Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 OpenAI OpCo, LLC

- 6.4.2 Anthropic PBC

- 6.4.3 Cohere Inc.

- 6.4.4 AI21 Labs Ltd.

- 6.4.5 Adept AI Labs, Inc.

- 6.4.6 Reka AI, Inc.

- 6.4.7 LangChain Inc.

- 6.4.8 Pinecone Systems, Inc.

- 6.4.9 Weaviate BV

- 6.4.10 Hugging Face SAS

- 6.4.11 Mistral AI SAS

- 6.4.12 Aleph Alpha GmbH

- 6.4.13 Stability AI Ltd.

- 6.4.14 Scale AI, Inc.

- 6.4.15 Anyscale, Inc.

- 6.4.16 Replit, Inc.

- 6.4.17 LlamaIndex LLC

- 6.4.18 Contextual AI, Inc.

- 6.4.19 Runway AI, Inc.

- 6.4.20 Databricks, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment