|

시장보고서

상품코드

2063462

의료 인재 관리 IT 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Medical Talent Management IT - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

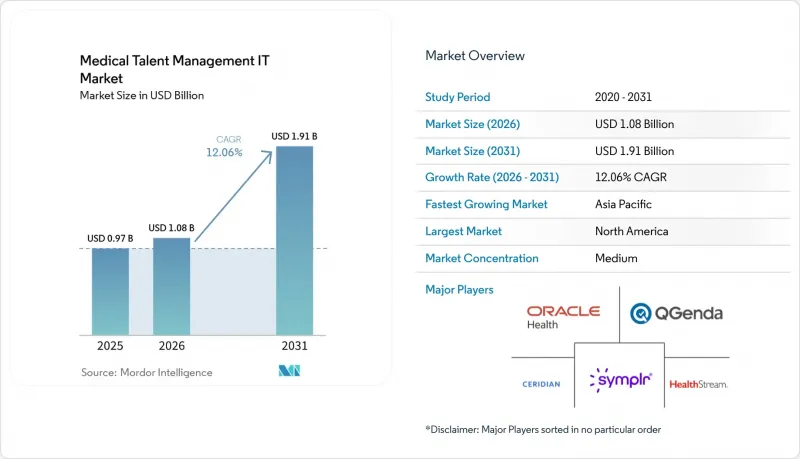

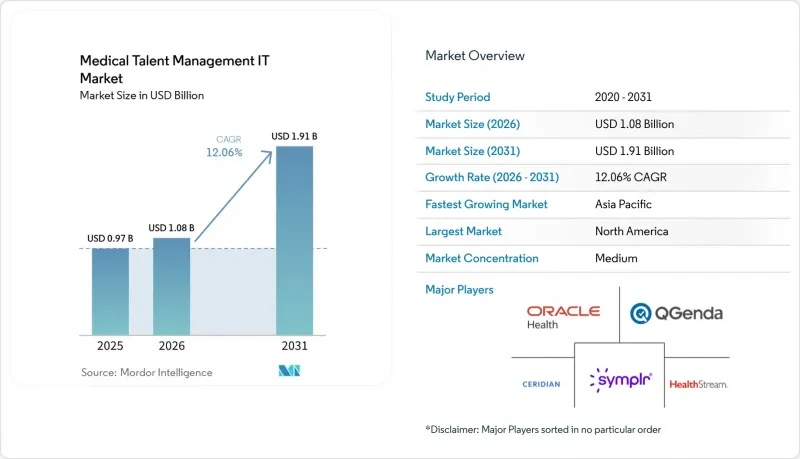

Mordor Intelligence에 의하면, 의료 인재 관리 IT 시장 규모는 2025년에 9억 7,000만 달러로 평가되었고, 2026년 10억 8,000만 달러로 추정되고, 2031년까지 19억 1,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 12.06%를 나타낼 전망입니다.

본 보고서는 구성 요소별(소프트웨어, 서비스), 도입 형태별(웹 및 클라우드, 온프레미스), 모듈별(채용 및 지원자 추적, 교육 및 규정 준수, 기타), 최종 사용자별(병원 및 의료 시스템, 기타), 조직 규모별(대기업, 중견기업, 중소기업) 및 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 예상 금액은 달러(USD)로 표시되어 있습니다.

세계의 의료 인력 관리 IT 시장 동향 및 인사이트

인력 부족과 인건비 압박으로 인해 채용, 일정 관리, 이직률 개선, 분석 도구 도입이 가속화되고 있습니다.

세계적으로 간호사 및 의료 관련 인력의 부족 현상은 계속 확대되고 있으며, 미국에서만 2038년까지 10만 8,960명의 정규 간호사가 부족할 것으로 예측됩니다. 병원은 이미 운영 예산의 절반 이상을 인건비로 지출하고 있기 때문에 CFO는 직원의 근무 시간을 직접적인 환자 치료에 할당할 수 있도록 예측 기반 이직 모델과 AI를 활용한 근무 일정 관리를 우선시하고 있습니다. 90일 전에 퇴사 가능성을 감지하는 실시간 분석을 통해 관리자는 코칭이나 근무 일정 조정을 통한 조기 개입이 가능해지며, 이에 따른 비용은 결원 보충에 드는 비용의 약 10분의 1 수준으로 절감됩니다. 이러한 도구는 인사 관리 시스템을 단순한 관리 기록의 보관 장소에서 처리 능력이나 품질 지표에 직접적인 영향을 미치는 현장 운영 대시보드로 변화시킵니다. 가치 기반 보상 제도가 확대됨에 따라 경영진은 인력 배치 최적화 프로젝트를 재입원 페널티 및 환자 경험 보너스와 연계하는 경향이 강해지고 있으며, 의료 인력 관리 IT 시장에 대한 투자에 대한 예산 지원이 확고해지고 있습니다.

클라우드 우선 전략과 AI를 활용한 인재 분석 및 스케줄링이 현대화를 가속화합니다.

2024년에 발생한 체인지 헬스케어(Change Healthcare)에 대한 사이버 공격은 급여 계산 및 자격 인증 데이터 피드가 수 주간 중단되었을 때, 단일 공급업체나 온프레미스형 아키텍처가 시스템적 위험을 초래할 수 있음을 보여주었습니다. 그 결과, 24시간 보안 감시를 수행할 자원이 부족한 중규모 병원이나 지역 병원에서는 클라우드 도입이 표준적인 조달 모델로 자리 잡았습니다. 멀티사이트 시스템에서는 클라우드 데이터베이스에 AI 알고리즘을 통합하여, 실시간 환자 수와 중증도 점수에 맞추어 인력을 배정함으로써, 가동 개시 후 6개월 만에 초과 근무 시간을 두 자릿수 비율로 줄였습니다. 각 채용 기업은 이력서 심사보다 근무 희망 일정을 예측하는 것을 더욱 중요하게 여기는 경향이 강해지고 있습니다. 이는 세심한 일정 관리의 개선이 투자 수익률(ROI)의 조기 실현으로 이어지고, 편견에 기반한 소송 위험을 피할 수 있기 때문입니다. 그 결과, 의료 인력 관리 IT 시장에서는 분기마다 클라우드 네이티브 솔루션이 출시되면서 혁신 주기가 단축되고, 구독 수익의 성장이 가속화되고 있습니다.

사이버 보안 및 개인정보 보호 위험과 HIPAA 규정 준수 비용이 도입을 지연시키고 있습니다.

2024년, 의료 업계에서는 보고 의무가 있는 정보 유출 사고가 725건 발생했으며, 건당 평균 비용은 1,093만 달러에 달했습니다. 인재 플랫폼에는 개인 식별자, 징계 기록, 사회보장번호 등 랜섬웨어 집단의 표적이 되기 쉬운 고가치 데이터가 저장되어 있습니다. 중견 벤더들은 HITRUST 및 SOC 2 인증을 유지하기 위해 연간 최대 30만 달러를 지출해야 하며, 이는 제품 개발 예산을 압박하고 의료 인력 관리 IT 시장의 새로운 틈새 분야에 진출할 수 있는 능력을 제한하고 있습니다. 따라서 일부 의료 시스템에서는 전체 솔루션으로의 전환을 미루고, 핵심인 인사 및 급여 계산 시스템을 온프레미스로 유지하면서, 명확한 투자 수익률(ROI)이 위험을 상회하는 경우에만 클라우드 모듈을 선택적으로 도입하고 있습니다.

부문별 분석

2025년 지출 중 소프트웨어가 65.12%를 차지했지만, 서비스 매출은 2031년까지 연평균 성장률(CAGR) 14.78%로 증가할 것으로 예상되며, 이는 의료 인력 관리 IT 시장 내 소프트웨어 성장률을 상회하는 수치입니다. 대규모 의료 시스템의 경우, 서로 분리된 ATS(채용 관리 시스템), LMS(학습 관리 시스템), 스케줄링 제품을 통합 제품군으로 통합함에 따라, 도입, 데이터 마이그레이션 및 변경 관리 컨설팅이 프로젝트 총 비용에서 큰 비중을 차지하게 되었습니다.

벤더가 고객을 대신해 자격 인증 및 일정 관리를 운영하는 매니지드 서비스는 가장 빠르게 성장하고 있으며, 일회성 프로젝트를 수익을 안정적으로 창출하는 지속적인 계약으로 전환하고 있습니다. Oracle의 ‘Workforce-as-a-Service’ 번들 솔루션은 인증된 전문가를 병원 팀에 배치하여 플랫폼 관리 업무를 IT 부서의 부담에서 덜어주고 있으며, 이는 성과 기반 가격 책정으로의 광범위한 전환을 시사합니다. 이러한 전환은 공급업체의 수익 모델을 재편하여, 단순한 코드 기반이 아닌 소프트웨어 지적 재산권(IP)과 심도 있는 전문 지식을 결합한 기업에 보상을 제공하게 될 것입니다.

2025년에는 웹 및 클라우드 도입이 전체 도입 건수의 59.24%를 차지했으며, 연평균 성장률(CAGR) 15.61%로 성장할 것으로 전망됩니다. 이는 의료 인력 관리 IT 시장에서 구매자들이 구독형 모델의 경제성과 벤더 관리를 통한 보안 업데이트를 선호하는 경향을 반영한 것입니다. 지역 병원들은 온프레미스형 데이터센터에서 철수하는 주된 이유로 사이버 보안 인력 확보의 어려움을 꼽고 있습니다.

그럼에도 불구하고, 특히 대학 병원, 연방 기관 및 엄격한 데이터 거주지법이 적용되는 지역에서는 여전히 상당수의 시스템이 온프레미스 방식으로 도입되고 있습니다. 예를 들어, 독일의 '클라우드 규정 준수 관리 카탈로그'에서는 인증 정보를 EU 역내에 저장해야 할 의무가 있으며, 기밀 문서는 로컬에 저장하는 한편, 익명화된 일정 데이터를 머신러닝 최적화를 위해 클라우드로 전송하는 하이브리드 아키텍처가 채택되고 있습니다. 현재 각 벤더사는 SaaS 코드 기반의 컨테이너화 버전을 제공하고 있어, 고객은 기능적인 타협 없이 호스팅 모델을 전환할 수 있게 되었습니다.

지역별 분석

2025년, 북미는 매출의 45.23%를 차지했습니다. 이는 CMS(의료보험서비스센터)의 인력 배치 요건과 HIPAA(의료보험 이동성 및 책임에 관한 법률)의 보안 규정에 따라 의료 제공업체가 일정 관리, 교육, 자격 인증 업무 프로세스를 디지털화할 수밖에 없게 되었기 때문입니다. 미국의 의료 시스템에서는 노동 시장이 인플레이션 양상을 보이는 가운데, 이익률 확대 수단으로 삼아 경영진 수준의 대시보드에 인재 분석 기능을 통합하는 움직임이 점점 더 확산되고 있습니다. 캐나다에서는 주별 분할로 인해 전국적인 확산이 지연되고 있지만, 상호 운용 가능한 의료 제공업체 등록 시스템을 위해 연방 정부가 2억 캐나다 달러를 배정함에 따라 클라우드 기반 자격 인증 플랫폼에 대한 수요가 증가하고 있습니다. 멕시코의 사립 병원들은 국경을 넘어 방문하는 의료 관광객을 수용하기 위해 이중 언어 지원 채용 포털을 도입하고 있으며, 이는 영어와 스페인어 양쪽의 규제 체계에 정통한 업체들에게 틈새 시장의 성장 기회를 제시하고 있습니다.

2025년 지출에서 유럽이 큰 비중을 차지했습니다. 독일의 43억 유로 규모 병원 디지털화 기금은 소프트웨어 비용의 대부분을 지원하여 신속한 도입을 촉진하는 한편, GDPR(EU 개인정보보호규정)의 거주지 조항을 충족하기 위해 온프레미스 호스팅을 더욱 선호하고 있습니다. 영국의 NHS 인력 데이터 이니셔티브는 130만 명의 직원 인사 기록을 일원화하여 관리하고 있으며, 각 트러스트에 근태 관리 및 역량 평가 데이터를 위한 표준화된 API 도입을 권장하고 있습니다. 남유럽 국가들은 예산 제약에 직면해 있어, 현지 통합 서비스와 결합된 오픈소스 인사 관리 제품군을 선호하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 14.13%를 나타낼 것으로 예측되며, 의료 인력 관리 IT 시장에서 전 지역 중 가장 높은 성장률을 보이고 있습니다. 중국은 2030년까지 100만 명의 신규 일반 개업의 면허 발급을 목표로 하고 있으며, 각 성의 보건국에서 대규모 자격 인증 업무의 자동화가 요구되고 있습니다. 인도의 '국가 디지털 헬스 미션'은 상호 운용성 지침을 마련해 놓았으며, 이에 따라 의료 기관들은 정부의 보상 프로그램에 참여하기 위해 클라우드 기반 신원 인증 및 일정 관리 시스템 도입을 간접적으로 요구받고 있습니다. 일본에서는 노동력의 고령화를 배경으로, 간호사의 역량과 노인 간호 중증도 점수를 대조하는 AI 기반 스케줄링 시범 사업이 진행되고 있습니다. 한편, 호주와 한국에서는 관할 구역을 넘나드는 화상 진료를 유지하기 위해 원격의료 분야의 자격 인증 검증을 우선시하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the medical talent management iT market size was valued at USD 0.97 billion in 2025 and is estimated to grow from USD 1.08 billion in 2026 to reach USD 1.91 billion by 2031, at a CAGR of 12.06% during the forecast period (2026-2031).

This report is Segmented by Component (Software, Services), Deployment (Web/Cloud, On-Premise), Module (Recruiting & Applicant Tracking, Learning & Compliance, and More), End User (Hospitals & Health Systems, and More), Organization Size (Large, Mid-Size, Small), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Forecasts in Value (USD).

Global Medical Talent Management IT Market Trends and Insights

Workforce Shortages and Labor Cost Pressure Intensify Adoption of Recruiting, Scheduling, Retention and Analytics Tools

Global nurse and allied-health shortfalls continue to widen, with the United States alone projecting a gap of 108,960 registered nurses by 2038. Hospitals already devote more than half of their operating budgets to labor, so CFOs are prioritizing predictive turnover models and AI-driven scheduling that can redeploy staff hours toward direct patient care. Real-time analytics that flag likely resignations 90 days in advance allow managers to intervene early with coaching or shift-pattern adjustments, which costs roughly one-tenth of back-filling an open role. Such tools convert talent systems from administrative record keepers into frontline operational dashboards that directly affect throughput and quality metrics. As value-based reimbursement expands, executives increasingly tie staffing optimization projects to readmission penalties and patient-experience bonuses, cementing budget support for Medical talent management IT market investments.

Cloud-First and AI-Enabled Workforce Analytics/Scheduling Accelerate Modernization

The Change Healthcare cyberattack in 2024 demonstrated that single-vendor or on-premise architectures create systemic risk when payroll and credentialing feeds are disrupted for weeks. Consequently, cloud deployment has become the default procurement model for mid-sized and community hospitals that lack the resources for round-the-clock security monitoring. Multi-site systems are layering AI algorithms on top of cloud databases to adjust staffing to live census and acuity scores, trimming overtime hours by double-digit percentages in the first six months after go-live. Increasingly, vendors emphasize shift-preference prediction rather than resume screening because granular scheduling improvements yield faster ROI and avoid bias litigation concerns. As a result, the Medical talent management IT market sees cloud-native releases arriving quarterly, shortening innovation cycles and reinforcing subscription revenue growth.

Cybersecurity/Privacy Risk and HIPAA Compliance Costs Slow Rollouts

Healthcare experienced 725 reportable breaches in 2024, with an average cost of USD 10.93 million per incident . Talent platforms store personal identifiers, disciplinary notes, and Social Security numbers, high-value data that attract ransomware gangs. Mid-size vendors must spend up to USD 300,000 annually to maintain HITRUST or SOC 2 certifications, eroding product-development budgets and limiting their ability to enter new Medical talent management IT market niches. Some health systems, therefore defer full-suite migration, keeping core HR or payroll on-premise while selectively adopting cloud modules only where clear ROI outweighs risk.

Other drivers and restraints analyzed in the detailed report include:

- Compliance-Driven Training and Competency Tracking Embed LMS Usage

- NCQA Credentialing/Delegation Tightening Catalyzes Credentialing Automation

- Integration Complexity with EHR/HR/Payroll Ecosystems Raises Implementation Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 65.12% of 2025 spending, yet services revenue is forecast to rise at a 14.78% CAGR through 2031, outpacing software growth in the Medical talent management IT market. Implementation, data migration, and change management consulting now account for a significant share of total project costs for large health systems as they consolidate disparate ATS, LMS, and scheduling products into unified suites.

Managed services, where a vendor operates credentialing or scheduling on the client's behalf, are expanding fastest, converting one-time projects into recurring contracts that smooth revenue. Oracle's workforce-as-a-service bundle embeds certified credentialing specialists within hospital teams and shifts platform administration off IT's plate, signaling a broader move toward outcome-based pricing. The transition reshapes vendor profitability models, rewarding companies that pair software IP with deep domain expertise rather than pure-play code bases.

Web and cloud implementations accounted for 59.24% of total installations in 2025 and are projected to grow at a 15.61% CAGR, reflecting buyer preference for subscription economics and vendor-managed security updates in the Medical talent management IT market. Community hospitals cite the inability to recruit cybersecurity talent as a top reason for exiting on-premises data centers.

Even so, a significant number of deployments remain on-premise, especially in academic medical centers, federal institutions, and regions with strict data-residency laws. Germany's Cloud Compliance Controls Catalogue, for instance, requires credential files to be stored within EU borders, prompting hybrid architectures that store sensitive documents locally while sending anonymized scheduling data to the cloud for machine learning optimization. Vendors now offer containerized versions of their SaaS code bases, letting customers switch between hosting models without functional trade-offs

Geography Analysis

North America generated 45.23% revenue in 2025 as CMS staffing mandates and HIPAA security rules forced providers to digitize scheduling, learning, and credentialing workflows. U.S. health systems increasingly embed workforce analytics into board-level dashboards, framing them as levers for margin expansion amid inflationary labor markets. Canada's provincial fragmentation slows national roll-outs, yet a federal CAD 200 million allocation for interoperable provider registries is boosting demand for cloud credentialing platforms. Mexico's private hospitals deploy bilingual recruiting portals to serve cross-border medical tourists, signaling a niche growth path for vendors fluent in both English and Spanish regulatory frameworks.

Europe contributed a significant share of the 2025 spending. Germany's EUR 4.3 billion hospital digitization fund reimburses the majority of software costs, spurring rapid procurement but also reinforcing on-premise hosting preferences to meet GDPR residency clauses. The United Kingdom's NHS Workforce Data Initiative centralizes staffing records for 1.3 million employees, pushing trusts to adopt standardized APIs for time-and-attendance and competency feeds. Southern European countries face budget constraints, so they favor open-source talent suites bundled with local integrator services.

Asia-Pacific is projected to grow at a 14.13% CAGR through 2031, the fastest among all regions in the Medical talent management IT market. China aims to license 1 million new general practitioners by 2030, requiring mass-scale credentialing automation across provincial health bureaus. India's National Digital Health Mission sets interoperability guidelines that indirectly compel provider organizations to adopt cloud credentialing and scheduling to participate in government reimbursement programs. Japan's aging workforce drives AI-based scheduling pilots that match nurse skills to geriatric-care acuity scores, while Australia and South Korea prioritize telemedicine credential validation to sustain cross-jurisdiction video consultations.

- ADP

- ATOSS Software

- CAQH

- Ceridian (Dayforce)

- HealthStream

- Infor

- Modio Health

- Ntracts

- Oracle Health

- PMG Credentialing

- QGenda

- Relias

- RLDatix

- SAP SuccessFactors (SAP SE)

- Smartlinx

- Strata Decision Technology

- Streamline Verify

- symplr

- Workday

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Workforce Shortages and Labor Cost Pressure Intensify Adoption of Recruiting, Scheduling, Retention and Analytics Tools

- 4.2.2 Cloud-First And AI-Enabled Workforce Analytics/Scheduling Accelerate Modernization

- 4.2.3 Compliance-Driven Training and Competency Tracking (HIPAA, TJC) Embed LMS Usage

- 4.2.4 PBJ Staffing-Data Enforcement in Long-Term Care Accelerates Time/Attendance And Scheduling Digitization

- 4.2.5 NCQA Credentialing/Delegation Tightening (Shorter Verification Windows, Continuous Monitoring) Catalyzes Credentialing Automation

- 4.3 Market Restraints

- 4.3.1 Cybersecurity/privacy risk and HIPAA compliance costs slow rollouts

- 4.3.2 Integration complexity with EHR/HR/payroll ecosystems raises implementation burden

- 4.3.3 Policy volatility around LTC staffing minimums reduces compliance-driven urgency in nursing homes

- 4.3.4 Budget constraints and competing IT priorities delay workforce platform investments

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Web/Cloud-based

- 5.2.2 On-premise

- 5.3 By Module / Function

- 5.3.1 Recruiting & Applicant Tracking (ATS)

- 5.3.2 Learning & Compliance (LMS/LXP; CE tracking)

- 5.3.3 Performance & Succession

- 5.3.4 Compensation & Benefits

- 5.3.5 Scheduling & Time & Attendance

- 5.3.6 Credentialing & Payer Enrollment

- 5.3.7 Workforce Analytics

- 5.4 By End User

- 5.4.1 Hospitals & Health Systems

- 5.4.2 Ambulatory/Clinics & Physician Groups

- 5.4.3 Long-term Care / Skilled Nursing

- 5.4.4 Behavioral Health

- 5.4.5 Home Health & Hospice

- 5.4.6 Payers / Health Plans (credentialing-focused)

- 5.5 By Organization Size

- 5.5.1 Large Enterprises

- 5.5.2 Mid-size Enterprises

- 5.5.3 Small Enterprises

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 ADP

- 6.3.2 ATOSS Software

- 6.3.3 CAQH

- 6.3.4 Ceridian (Dayforce)

- 6.3.5 HealthStream

- 6.3.6 Infor

- 6.3.7 Modio Health

- 6.3.8 Ntracts

- 6.3.9 Oracle Health

- 6.3.10 PMG Credentialing

- 6.3.11 QGenda

- 6.3.12 Relias

- 6.3.13 RLDatix

- 6.3.14 SAP SuccessFactors (SAP SE)

- 6.3.15 Smartlinx

- 6.3.16 Strata Decision Technology

- 6.3.17 Streamline Verify

- 6.3.18 symplr

- 6.3.19 Workday

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment