|

시장보고서

상품코드

2065528

의료 분야 인재 관리 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Talent Management In Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

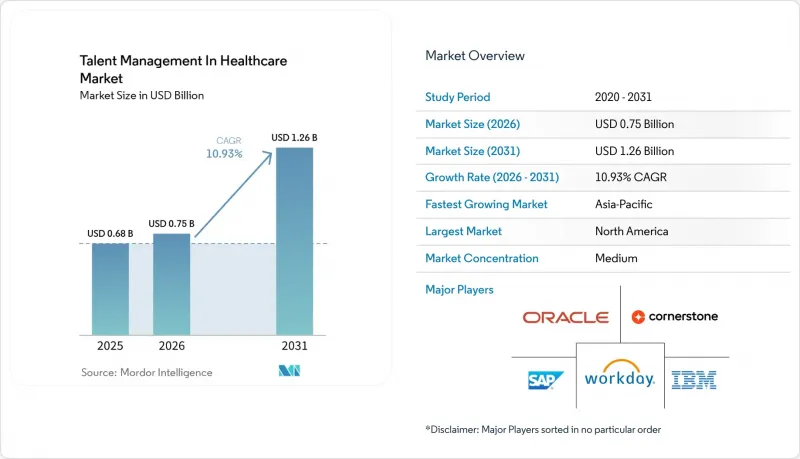

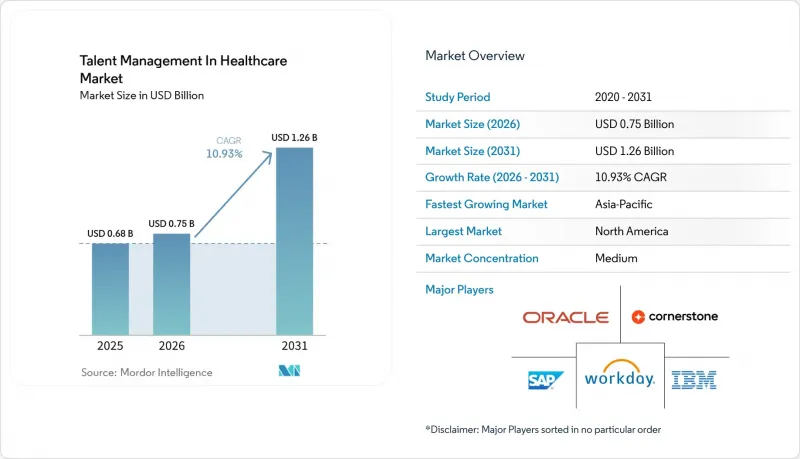

의료 분야 인재 관리 시장 규모는 2025년에 6억 8,000만 달러로 평가되었고, 2026년 7억 5,000만 달러로 추정되고, 2031년까지 12억 6,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 10.93%를 나타낼 전망입니다.

본 보고서는 구성 요소별(소프트웨어 및 서비스), 도입 형태별(클라우드, 온프레미스, 하이브리드), 용도별(성능 관리, 학습·역량 개발, 후계자 계획 등), 최종 사용자 산업 분야별(병원·의료 시스템, 외래·전문 클리닉, 재택치료 기관 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 의료 분야 인재 관리 시장 동향 및 인사이트

급성기 간호 인력의 심각한 부족으로 인해 인재 확보 경쟁이 치열해지고 있습니다.

현재 진행 중인 정규 간호사(RN) 부족으로 인해, 급성기 의료 분야에서 인재 관리 플랫폼에 대한 수요가 크게 증가하고 있습니다. 2026년 초까지 33% 이상의 병원이 간호사(RN) 결원율이 10%를 초과한다고 보고했으며, 전국적인 간호사(RN) 부족 인원은 15만 8,600명으로 추산됩니다. 병원 1곳당 평균 43명의 간호사 자리가 공석인 것으로 나타나, 이 문제의 심각성이 여실히 드러나고 있습니다. 이러한 인력 부족은 고르게 분포되어 있는 것이 아니며, 텔레메트리나 스텝다운 병동과 같은 특정 전문 분야에서는 약 4.5년마다 인력이 완전히 교체되고 있습니다. 이처럼 이직률이 높기 때문에 수작업에 의존하는 인사 관리는 비효율적일 뿐만 아니라 비용도 많이 듭니다. 그 결과, 의료기관에서는 첨단 인재 관리 솔루션의 도입이 점점 더 확대되고 있습니다. 인재 파이프라인 분석, 사내 이동 추적, 이직 예측 모델링 등의 기능을 갖춘 이러한 플랫폼은 더 이상 단순한 선택적 도구로 간주되지 않습니다. 오히려 재무 위험을 줄이고 업무의 안정성을 확보하기 위해 필수적인 요소가 되어가고 있습니다. 이러한 추세는 의료 시장의 인력 문제에 대처하기 위해 기술에 대한 의존도가 높아지고 있음을 보여주며, 인력 관리 시스템 도입을 더욱 촉진하고 있습니다.

의료 종사자의 번아웃으로 인한 이직률 문제에 대한 집중

팬데믹 정점 당시의 수치는 완화되었지만, 번아웃은 여전히 인력 비용 측면에서 심각한 문제로 남아 있습니다. 43개 주의 약 1만 8,000명의 의사를 대상으로 실시된 2024년 AMA 조사에 따르면, 43.2%가 여전히 적어도 한 가지 이상의 번아웃 증상을 보고한 반면, 직무 만족도는 76.5%로 상승하여 조직적인 개입을 통해 직원 참여도를 높일 수 있음을 보여주고 있습니다. 인재 관리 업체에게 있어 전략적 인사이트은 웰빙 프로그램의 한계 수익이 측정 가능하다는 점입니다. 2025년에 미국 ‘마그넷 인증’ 병원 50곳을 대상으로 실시된 다기관 공동 연구에 따르면, 공유 거버넌스 모델이 확립되고 업무 부담 관리 기능이 충실하며 적극적인 사내 표창 제도를 도입한 조직에서 번아웃 발생 확률이 통계적으로 낮은 것으로 나타났습니다. 의료 시스템에서는 기존의 직원 만족도 조사에 그치지 않고, 임상의에 특화된 참여도 분석, 업무 부담 정도 모니터링, 경력 정체 징후, 그리고 표창 빈도를 포함할 수 있는 기능을 인재 관리 플랫폼에 요구하고 있습니다. 2026년 Prolink가 400명 이상의 파견 의료 종사자를 대상으로 실시한 설문조사에서 2026년 의료 업계의 가장 큰 위협으로 번아웃(29%), 사기 저하(21%), 인재 이직률(20%)이 꼽혔습니다. 이는 참여도 데이터와 연동된 고객 유지율 향상 도구가 단순한 이상이 아니라, 현재 구매 시 최우선 고려 사항임을 입증하고 있습니다.

중규모 의료기관에서 파편화된 IT 인프라

2026년 CHIME가 의료 기술 리더을 대상으로 실시한 ‘Leadership Pulse Survey’에 따르면, 응답자의 76%가 도구의 난립과 분산이 업무를 어렵게 만들고 있다고 답했으며, 일부 조직에서는 100개 이상의 엔터프라이즈 도구를 관리하고 있는 반면, 85%는 기술 현대화의 주요 장애물로 재정적 제약을 꼽고 있습니다. 인적 자원 관리 업체에게 있어 가장 중대한 과제는 통합의 복잡성입니다. 설문 응답자의 74%가 새로운 플랫폼에 기존 EHR 시스템과의 원활한 연동성을 요구하고 있으며, 이는 많은 중견 인재 관리 솔루션이 막대한 전문 서비스 투자 없이는 극복하기 어려운 장애물로 작용하고 있습니다. 병상 수가 200개 미만인 의료기관에서는 이 문제가 더욱 심각해집니다. 이러한 조직에는 대개 진료 일정, 자격 인증, 급여 계산 시스템에 걸친 API 통합을 관리하는 전담 인터페이스 엔지니어링 팀이 없기 때문입니다. 연방 정부의 모니터링 데이터에 따르면, 독립형 크리티컬 액세스 병원은 의료 그룹에 소속된 동종 병원에 비해 EHR 상호운용성이 현저히 낮은 것으로 나타났으며, 이와 유사한 구조적 격차가 HR 기술 분야에서도 나타납니다. 주요 EHR 플랫폼과 사전 구축 및 인증을 완료한 통합 기능을 제공하지 못하는 벤더는 잠재 고객 수가 매우 많은 중견 시장에서 판매 주기가 장기화될 위험을 감수하게 됩니다.

부문별 분석

구성 요소별 세분화 분석에 따르면, 2025년 의료 인력 관리 시장에서 소프트웨어의 매출 점유율은 72.28%를 차지했습니다. 이는 멀티모듈형 엔터프라이즈 제품군에 투자하고 초기 라이선스 비용을 자산으로 계상하는 대규모 의료 시스템의 플랫폼 중심 구매 패턴을 반영한 것입니다. 서비스 부문은 2026-2031년 연평균 성장률(CAGR) 12.43%를 기록하며 시장 전체를 상회할 것으로 전망됩니다. 이는 규모에 관계없이 모든 제공업체가 설정, 워크플로우 재설계 및 변경 관리가 인재 플랫폼이 측정 가능한 성과를 가져올지 여부를 좌우하는 경우가 많다는 점을 인식하고 있기 때문입니다. 도입 컨설팅 및 맞춤화를 포함한 전문 서비스는 서비스 부문 내에서 가장 큰 점유율을 차지하고 있지만, 조직이 기간 한정 도입 계약에서 지속적인 플랫폼 최적화로 전환함에 따라 지원 및 유지보수 서비스에 대한 수요도 증가하고 있습니다. 이를 통해 전략적으로 볼 때, 과거에는 소프트웨어 기능 면에서 경쟁해 온 벤더들이 현재는 연간 계약액을 유지하고 고객 이탈률을 낮추기 위해 서비스 역량을 확충하거나 인수를 추진하고 있다는 점을 알 수 있습니다.

서비스 수익 성장을 뒷받침하는 틈새 시장 동향으로, 의료 분야에 특화된 설정에 관한 전문 지식에 대한 수요가 증가하고 있다는 점을 들 수 있습니다. 일반적인 HCM(인적 자본 관리) 시스템을 도입할 때에도 간호사 면허 추적, 여러 주에 걸친 면허 협정, 그리고 JCAHO(미국 의료시설 인증 합동위원회)가 요구하는 역량 증명 서류 관리를 지원하기 위해서는 광범위한 맞춤 설정이 필요합니다. HealthStream과 같은 벤더들은 이에 대응하여 AI를 활용한 설정 도구와, 2025년 1월에 출시된 ‘HealthStream Learning Experience’ 플랫폼과 같은 사전 구축된 의료용 컨텐츠 라이브러리를 구축하고 있습니다. 이러한 조치들은 고객이 가치를 실현하기까지 걸리는 시간을 단축하고, 도입 서비스 비용을 절감하는 동시에 컨텐츠 구독을 통해 지속적인 수익을 창출하고 있습니다. 경쟁 측면에서 볼 때, AI를 통해 일상적인 도입 작업이 자동화되고, 벤더들이 관리형 서비스 계층을 구독 요금에 포함시키면서, 소프트웨어 수익과 서비스 수익의 경계는 앞으로도 점점 더 모호해질 것입니다.

2025년 기준으로 의료 분야 인재 관리 시장에서 클라우드 도입은 68.31%의 점유율을 차지했으며, 동시에 2031년까지 연평균 성장률(CAGR) 13.47%를 기록하며 가장 빠르게 성장하고 있는 도입 형태이기도 합니다. 이러한 이례적인 조합은 온프레미스 및 하이브리드 환경에서의 전환에 힘입어, 이 부문이 시장을 독점하고 있을 뿐만 아니라 여전히 활발하게 성장하고 있음을 보여줍니다. 의료 시스템에서 나타나는 ‘클라우드 우선’ 경향은 모바일 인력의 움직임이 가속화됨에 따라 더욱 강화되고 있습니다. 2024년에는 미국 전체 등록 간호사의 5.3%가 여행 간호사로 근무했으며, 같은 해 약 20%가 근무처를 변경했습니다. 이로 인해 자격 증명 및 일정 관리가 분산되면서, 로컬에서 호스팅되는 인프라에서는 관리가 어려운 수준의 복잡성이 발생하고 있습니다. IHH 헬스케어가 2026년 5월 10개국 89개 병원에 Oracle Fusion Cloud HCM을 도입한 사례는 대형 다국적 의료 그룹이 클라우드 플랫폼을 활용하여 온프레미스 시스템으로는 구조적으로 실현할 수 없었던 대규모 인재 가시화를 달성했음을 보여줍니다.

온프레미스 도입은 시장 점유율이 감소하는 추세이지만, 데이터 주권에 관한 요건이 엄격한 국가의 정부 산하 병원 시스템에서는 여전히 그 중요성을 유지하고 있습니다. 특히 중국, 인도, 중동에서는 각국의 의료 데이터 규제로 인해 국경을 넘는 클라우드 전송이 제한될 가능성이 있기 때문입니다. 하이브리드 도입은 기밀성이 높은 직원 데이터를 온프레미스에서 보관하면서, 클라우드 기반의 분석 기능이나 AI 기능을 활용할 수 있는 중간적인 아키텍처로 부상하고 있습니다. 이 구성은 EHR 인프라에 막대한 투자를 하고 있으며, 플랫폼의 완전한 전환에 따른 자본적 혼란을 감당할 수 없는 시스템에서 특히 높은 평가를 받고 있습니다. 독일의 규제 준수 체계, 특히 연방노동법원이 2022년에 내린 근무 시간 기록 의무화 판결(2024년 행정법원에서 재확인됨)은 도입 모델에 관계없이 규정 준수를 중시하는 디지털 인사 도구에 대한 수요를 창출하고 있으며, 유럽 기업 고객들 사이에서 하이브리드 모델의 유효성을 유지하고 있습니다.

지역별 분석

2025년, 북미는 의료 분야 인재 관리 시장에서 39.42%의 점유율을 차지하며 시장을 주도했습니다. 이는 미국 내 급성기 의료시설의 타의 추종을 불허하는 밀도, 성숙한 SaaS 조달 인프라, 그리고 CMS(미국 의료보험서비스센터)의 가치 기반 의료 의무화 및 조인트 커미션의 인증 기준에 따른 지속적인 규제 압력에 힘입은 결과입니다. 2026년 기준으로 미국에서만 약 15만 8,600명의 정규 간호사(RN)가 부족할 것으로 추정되며, 병원에서 정규 간호사가 이직할 때 발생하는 비용은 간호사 1인당 평균 6만 90달러에 달할 전망입니다. 이는 기술 투자에 대한 강력한 경제적 유인책이 되고 있습니다. 캐나다와 멕시코는 규모는 작지만 성장세가 두드러지는 하위 시장입니다. 캐나다에서는 번아웃과 관련된 유사한 이직 추세가 나타나는 반면, 멕시코에서는 계속 확장되고 있는 민간 병원 부문이 클라우드 기반 인사 플랫폼에 대한 투자를 시작하고 있습니다. 2026년 1월에 시작된 500억 달러 규모의 이니셔티브인 CMS(미국 의료보험서비스센터)의 ‘농촌 지역 의료 혁신 프로그램’은 의료 서비스가 부족한 미국 지역사회를 위한 인재 관리 기술에 자금을 지원하고 있으며, 콜로라도주 등 일부 주에서는 원격의료와 기술 통합에 특히 2억 5,550만 달러를 배정하고 있습니다. 이 연방 프로그램을 통해, 그동안 기술 도입에 소극적이었던 지방의 의료 제공업체들이 예측 기간 동안 대상 시장에 진입할 것으로 예측됩니다.

2025년에는 유럽이 시장 수익에서 상당한 점유율을 차지했습니다. 그 선두에 선 것은 독일과 영국이었으며, 이들 국가에서는 디지털 근태 관리 의무화 규제와 국민보건서비스(NHS)의 인력 부족 위기로 인해, 기존에 종이 기반이었던 인사 프로세스가 플랫폼을 활용한 프로세스로 전환되고 있습니다. 독일 연방노동법원의 근로시간 기록 의무화에 관한 판결은 2024년 8월 함부르크 행정법원에 의해 재확인되었으며, 특히 약 43만 명의 의료 보조원(이 중 약 50%가 파트타임 근로자)을 중심으로 규정 준수를 동력으로 한 디지털화된 노무 관리에 대한 수요를 창출했습니다. 이러한 의료 보조원의 근무 일정은 복잡하여 수동 시스템으로는 정확하게 파악할 수 없습니다. 영국의 국민보건서비스(NHS)는 여전히 주요 수요처이며, NHS Management사는 UKG Rapid Hire 도입 후 채용까지 소요되는 기간이 10일 단축되었고, 연간 220만 달러의 신규 수익이 창출되었다고 보고했습니다. 프랑스, 이탈리아 및 기타 유럽 국가들은 의료 분야에서의 기업용 인사 플랫폼 도입이 아직 초기 단계에 있어, 다국어 지원 기능을 갖춘 제품을 보유한 공급업체에게는 중기적인 성장 기회가 되고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR)이 13.89%로 가장 빠른 성장이 전망되는 지역이며, 이는 의료 인프라에 대한 투자, 병원의 디지털화 추진 방침, 그리고 구조적으로 서비스가 부족한 인력 관리 소프트웨어 시장을 반영한 것입니다. 인도 정부 산하 기관인 AIIMS 네트워크는 2026년 3월 기준으로 교원 약 2,316명, 비교원 약 15,525명의 결원이 있다고 보고했으며, 이는 각각 정원의 약 36%, 26%에 해당합니다. 또한 2026년 2월, 연방 보건부 장관은 AI를 활용한 진단과 교원의 신속한 채용을 동등한 우선순위로 삼았으며, 이는 인재 관리 기술이 국가 정책 논의의 장에 진입하고 있음을 시사했습니다. 중국 국가위생건강위원회가 정한 ‘스마트 관리 단계별 평가 기준’에 따르면, 레벨 2 인증 이후 디지털 인사 모듈 도입이 의무화되어 있으며, 이는 약 35,000곳의 등록 시설로 구성된 공공 병원 시스템 전체에 영향을 미치고 있어, Yanfang Software나 Medrun과 같은 국내 벤더의 채택을 촉진하고 있습니다. 2026년 1월에 개최된 ‘Hospital Management Asia 2025’ 컨퍼런스에서 의료 리더을 대상으로 실시한 설문조사 결과, 해당 지역이 직면한 가장 일반적인 체계적 과제로는 재정적 제약이나 디지털 전환을 제치고 인재 관리가 꼽혔습니다. 사우디아라비아와 아랍에미리트(UAE)를 필두로 한 중동 및 아프리카에서는 ‘비전 2030’에 부합하는 광범위한 디지털 전환 프로그램의 일환으로, 의료 종사자 관리 기술에 대한 투자가 진행되고 있습니다. 한편, 남미, 특히 브라질에서는 대규모 민간 병원 그룹을 중심으로 초기 단계 수요가 나타나고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the talent management in healthcare market size was valued at USD 0.68 billion in 2025 and estimated to grow from USD 0.75 billion in 2026 to reach USD 1.26 billion by 2031, at a CAGR of 10.93% during the forecast period (2026-2031).

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, On-Premise, and Hybrid), Application (Performance Management, Learning and Development, Succession Planning, and More), End User Industry (Hospitals and Health Systems, Ambulatory and Specialty Clinics, Home Healthcare Agencies, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Talent Management In Healthcare Market Trends and Insights

Acute Nursing Staff Shortage Intensifying Competition For Talent

The ongoing shortage of registered nurses (RNs) is driving significant demand for talent management platforms within the acute care sector. By early 2026, more than 33% of hospitals reported RN vacancy rates exceeding 10%, with the national shortage estimated at 158,600 RNs. On average, hospitals are managing 43 unfilled RN positions, highlighting the critical nature of this issue. This shortage is not evenly distributed, as certain specialties, such as telemetry and step-down units, are experiencing complete staff turnover approximately every 4.5 years. Such high turnover rates make manual human resource tracking both inefficient and costly. As a result, healthcare organizations are increasingly adopting advanced talent management solutions. These platforms, which offer features like pipeline analytics, internal mobility tracking, and predictive attrition modeling, are no longer viewed as optional tools. Instead, they are becoming essential for mitigating financial risks and ensuring operational stability. This trend underscores the growing reliance on technology to address workforce challenges in the healthcare market, further propelling the adoption of talent management systems.

Clinician-burnout-led Retention Focus

Burnout remains a material talent cost even as peak-pandemic rates ease. A 2024 AMA survey of nearly 18,000 physicians across 43 states found that 43.2% still reported at least one burnout symptom, while job satisfaction rose to 76.5%, signaling that improvements in engagement are achievable through organizational intervention. The strategic insight for talent management vendors is that the marginal return on well-being programs is measurable: organizations with stronger shared-governance models, better workload-control features, and active internal-recognition tools showed statistically lower burnout odds in a 2025 multicenter study across 50 Magnet-status US hospitals. Health systems have begun requiring talent platforms to include clinician-specific engagement analytics, monitoring workload intensity, career stagnation signals, and recognition frequency, beyond traditional employee satisfaction surveys. A 2026 Prolink survey of over 400 travel healthcare professionals identified burnout (29%), declining morale (21%), and workforce retention (20%) as the top perceived threats to healthcare in 2026, reinforcing that retention tooling tied to engagement data is a current, not aspirational, purchasing priority.

Fragmented IT Infrastructure In Mid Tier Providers

A 2026 CHIME Leadership Pulse Survey of healthcare technology leaders found that 76% cited tool sprawl and fragmentation as making operations harder, with some organizations managing over 100 enterprise tools, while 85% identified financial limitations as the primary barrier to technology modernization. The most consequential challenge for talent management vendors is integration complexity: 74% of survey respondents require new platforms to offer seamless connectivity with existing EHR systems, a threshold many mid-tier talent management solutions cannot clear without substantial professional services investment. For providers below the 200-bed threshold, the problem compounds, as these organizations typically lack dedicated interface engineering teams to manage API integrations across clinical scheduling, credentialing, and payroll systems. Independent critical access hospitals demonstrated substantially lower EHR interoperability than system-affiliated peers in federal monitoring data, and the same structural gap applies to HR technology. Vendors that fail to offer pre-built, certified integrations with dominant EHR platforms risk a protracted sales cycle in the mid-market, which represents a significant volume of potential accounts.

Other drivers and restraints analyzed in the detailed report include:

- Competency-tracking Mandates for Clinical Staff

- Shift to Value-based Care Demanding Upskilling

- Data Privacy Concerns Around Staff Credential Records And HR Data

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Across the component segmentation, software held a 72.28% revenue share of the talent management in healthcare market in 2025, reflecting the platform-centric buying pattern of large health systems that invest in multi-module enterprise suites and capitalize the initial license outlay. The services segment is forecast to grow at 12.43% CAGR from 2026 to 2031, outpacing the overall market, as providers of all sizes recognize that configuration, workflow redesign, and change management often determine whether a talent platform delivers measurable outcomes. Professional services, which encompass implementation consulting and customization, contribute the largest share within the services segment, while support and maintenance services are gaining traction as organizations move away from time-limited deployment contracts toward continuous platform optimization. The strategic implication is that vendors who have historically competed on software features are now building out or acquiring services capabilities to defend annual contract value and reduce churn.

A niche dynamic amplifying services revenue growth is the increasing demand for healthcare-specific configuration expertise. General-purpose HCM implementations require extensive customization to handle nurse licensure tracking, multistate compact licensure and JCAHO-required competency documentation. Vendors like HealthStream have responded by building AI-assisted configuration tooling and pre-built healthcare content libraries, such as the HealthStream Learning Experience platform launched in January 2025, that accelerate time-to-value and reduce implementation services cost for clients, while still generating recurring revenue through content subscriptions. The competitive implication is that the line between software and services revenue will continue to blur as AI automates routine implementation tasks and vendors bundle managed-service tiers into subscription pricing.

Cloud deployment held 68.31% share of the talent management in healthcare market in 2025 and is simultaneously the fastest-growing mode at 13.47% CAGR through 2031, an unusual combination indicating that this segment is both dominant and still in active expansion, driven by migration from on-premise and hybrid environments. The cloud-first preference among health systems is reinforced by accelerating mobile workforce dynamics: 5.3% of all US registered nurses worked as travel nurses in 2024, and approximately 20% changed work settings in the same year, creating distributed credential and scheduling complexity that is difficult to manage on locally hosted infrastructure. IHH Healthcare's May 2026 deployment of Oracle Fusion Cloud HCM across 89 hospitals in 10 countries illustrates how major multi-national healthcare groups are leveraging cloud platforms to achieve workforce visibility at scale that on-premise systems structurally cannot deliver.

On-premise deployment, while declining in share, retains relevance for government-owned hospital systems in countries with strict data sovereignty requirements, particularly in China, India, and the Middle East, where national health data regulations can restrict cross-border cloud transfers. Hybrid deployment is emerging as an intermediate architecture that allows organizations to maintain sensitive staff data on-premises while leveraging cloud-based analytics and AI capabilities, a configuration particularly valued in systems that have made substantial EHR infrastructure investments and cannot absorb the capital disruption of a full platform migration. Regulatory compliance frameworks in Germany, including the Federal Labor Court's 2022 mandatory time-tracking ruling reaffirmed by administrative courts in 2024, are creating compliance-driven demand for digitized HR tools regardless of deployment model, keeping hybrid viable in European enterprise accounts.

Geography Analysis

North America dominated the talent management in healthcare market with a 39.42% share in 2025, driven by the United States' unmatched density of acute-care facilities, a mature SaaS procurement infrastructure, and sustained regulatory pressure from CMS value-based care mandates and Joint Commission accreditation standards. The United States alone carries an estimated 158,600 RN shortage as of 2026, with hospital RN turnover costs averaging USD 60,090 per bedside nurse, creating a powerful financial incentive for technology investment. Canada and Mexico represent smaller but growing sub-markets: Canada is experiencing similar burnout-linked attrition dynamics, while Mexico's expanding private hospital sector is beginning to invest in cloud-based HR platforms. The CMS Rural Health Transformation Program, a USD 50 billion initiative launched in January 2026, is channeling capital into workforce technology for underserved US communities, with states like Colorado allocating USD 255.5 million specifically for telehealth and technology integration. This federal program is expected to pull previously technology-resistant rural providers into the addressable market over the forecast period.

Europe accounted for a meaningful share of market revenue in 2025, led by Germany and the United Kingdom, where mandatory digital time-tracking regulations and national health service staffing crises are converting previously paper-based HR processes into platform-enabled ones. Germany's Federal Labor Court ruling on mandatory working-hours tracking, reaffirmed by Hamburg administrative courts in August 2024, created a compliance-driven stimulus for digitized workforce management, particularly among the approximately 430,000 medical assistants, nearly 50% of whom work part-time, generating scheduling complexity that manual systems cannot accurately capture. The United Kingdom's NHS remains a major demand generator, with NHS Management reporting a 10-day reduction in time-to-hire and USD 2.2 million in new annual revenue after deploying UKG Rapid Hire. France, Italy, and the rest of Europe are at earlier stages of enterprise HR platform adoption in healthcare, offering a mid-term expansion opportunity for vendors with multilingual product configurations.

Asia-Pacific is the fastest-growing region at 13.89% CAGR through 2031, reflecting healthcare infrastructure investment, hospital digitization mandates, and a structurally under-served talent management software market. India's government-run AIIMS network reported approximately 2,316 faculty and 15,525 non-faculty vacancies as of March 2026, representing roughly 36% and 26% of sanctioned posts respectively, and the Union Health Minister linked AI-enabled diagnostics with faster faculty recruitment as co-equal priorities in February 2026, signaling that workforce technology is entering the national policy conversation. China's National Health Commission Smart Management Graded Evaluation Standard mandates digital HR modules from Level 2 certification onwards, affecting public hospitals across a system of approximately 35,000 registered facilities and driving adoption of domestic vendors such as Yanfang Software and Medrun. A January 2026 survey of healthcare leaders at the Hospital Management Asia 2025 conference identified workforce and talent management as the most prevalent systemic challenge facing the region, ahead of both financial constraints and digital transformation. The Middle East and Africa, led by Saudi Arabia and the UAE, are investing in healthcare workforce technology as part of broader Vision 2030-aligned digital transformation programs, while South America, principally Brazil, shows early-stage demand concentrated in large private hospital groups.

- Oracle Corporation

- SAP SE (SuccessFactors)

- IBM Corporation (Kenexa)

- Cornerstone OnDemand, Inc.

- Workday, Inc.

- UKG Inc.

- HealthStream Inc.

- Infor Inc.

- Cerner Corporation

- ADP Inc.

- PeopleFluent (LTG)

- HealthcareSource HR Inc.

- OnShift Inc.

- Shiftboard Inc.

- Avature

- BambooHR LLC

- iCIMS

- SmartRecruiters Inc.

- PageUp People Ltd.

- Paylocity Holding Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Acute Nursing-Staff Shortage Intensifying Competition

- 4.2.2 Clinician-burnout-led Retention Focus

- 4.2.3 Competency-tracking Mandates for Clinical Staff

- 4.2.4 Shift to Value-based Care Demanding Upskilling

- 4.2.5 AI-driven Candidate-matching Efficiencies

- 4.2.6 Telehealth Expansion Creating Remote-workforce Needs

- 4.3 Market Restraints

- 4.3.1 Fragmented IT Infrastructure in Mid-tier Providers

- 4.3.2 Data Privacy Concerns Around Staff Credential Records

- 4.3.3 Limited HR-tech Budgets in Rural Healthcare

- 4.3.4 Union Resistance to Algorithmic Performance Scoring

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Support and Maintenance Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-premise

- 5.2.3 Hybrid

- 5.3 By Application

- 5.3.1 Performance Management

- 5.3.2 Learning and Development

- 5.3.3 Succession Planning

- 5.3.4 Compensation Management

- 5.3.5 Recruitment and Talent Acquisition

- 5.3.6 Workforce Planning

- 5.3.7 Employee Engagement and Career Development

- 5.3.8 Other Talent Management Applications

- 5.4 By End User Industry

- 5.4.1 Hospitals and Health Systems

- 5.4.2 Ambulatory and Specialty Clinics

- 5.4.3 Long-Term Care and Rehab Centers

- 5.4.4 Home Healthcare Agencies

- 5.4.5 Other End User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of the Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Oracle Corporation

- 6.4.2 SAP SE (SuccessFactors)

- 6.4.3 IBM Corporation (Kenexa)

- 6.4.4 Cornerstone OnDemand, Inc.

- 6.4.5 Workday, Inc.

- 6.4.6 UKG Inc.

- 6.4.7 HealthStream Inc.

- 6.4.8 Infor Inc.

- 6.4.9 Cerner Corporation

- 6.4.10 ADP Inc.

- 6.4.11 PeopleFluent (LTG)

- 6.4.12 HealthcareSource HR Inc.

- 6.4.13 OnShift Inc.

- 6.4.14 Shiftboard Inc.

- 6.4.15 Avature

- 6.4.16 BambooHR LLC

- 6.4.17 iCIMS

- 6.4.18 SmartRecruiters Inc.

- 6.4.19 PageUp People Ltd.

- 6.4.20 Paylocity Holding Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment