|

시장보고서

상품코드

2063486

인도네시아의 골판지 포장 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Indonesia Corrugated Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

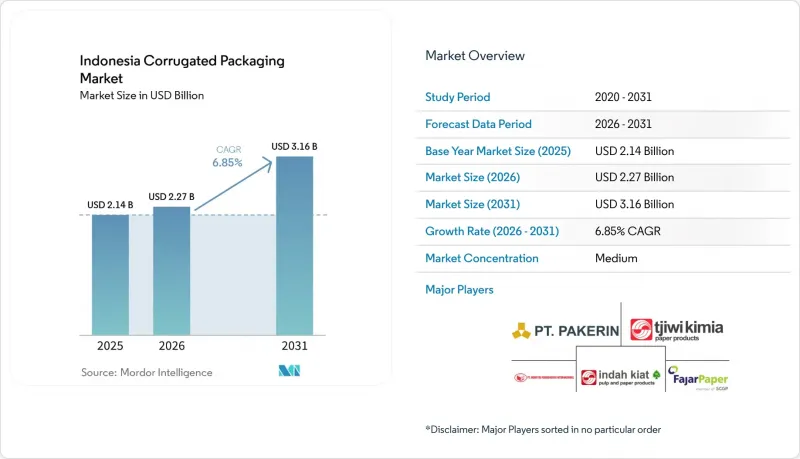

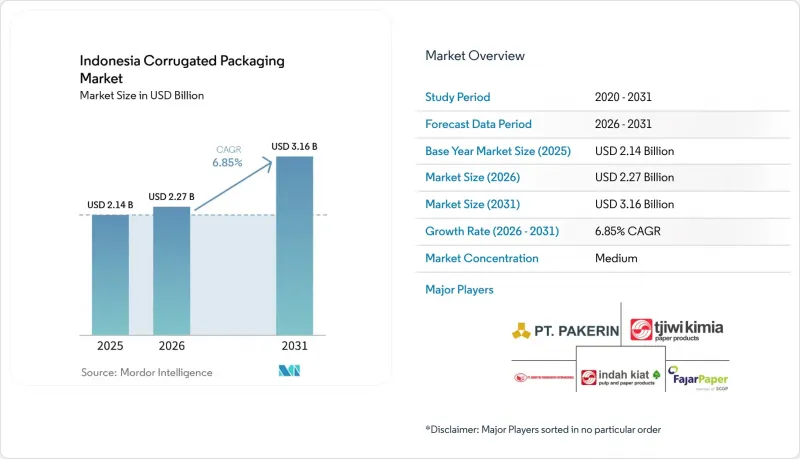

Mordor Intelligence에 의하면, 인도네시아 골판지 포장 시장 규모는 2025년 21억 4,000만 달러에서 2026년에는 22억 7,000만 달러로 확대되어 2031년까지 31억 6,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 6.85%로 성장할 전망입니다.

본 보고서는 원료(버진 크라프트 라이너보드, 재생 라이너보드, 골판지 심재 등), 플루트 유형(A 플루트 등), 포장 유형(레귤러 슬롯 컨테이너 등), 벽 구조(싱글, 더블 등), 인쇄 기술(플렉소 인쇄 등), 그리고 최종 사용자 산업(가공 식품 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

인도네시아 골판지 포장 시장 동향과 인사이트

전자상거래 출하량의 급증

인도네시아의 급성장하는 소포 경제는 플랫폼들이 부피 중량 과세를 피하고 라스트 마일 효율을 높이기 위해 포장을 최적화함에 따라 상자 디자인을 재정의하고 있습니다. 주요 소셜 커머스 채널에서의 일일 매출은 현재 수백만 건의 소량 주문을 발생시키고 있으며, 이를 위해서는 더 얇은 E-플루트 및 F-플루트, 적절한 크기의 다이컷, 그리고 신속한 디자인 변경이 요구됩니다. 풀필먼트 센터에는 빈 공간을 최대 20%까지 줄여주는 자동 커터가 도입됨에 따라, 컨버터는 기성품인 표준 슬롯 컨테이너 대신 주문형 블랭크를 제공해야만 하는 상황에 처해 있습니다. 전국적으로 통일된 재활용 기준이 존재하지 않기 때문에 국경을 넘어 판매하는 업체들의 규정 준수 절차가 복잡해지고 있으며, 이로 인해 대형 상품의 경우 반품 시 파손을 방지하기 위해 더 두꺼운 소재로 되돌아가는 경향이 있습니다. 인터넷 경제가 자바 섬을 넘어 확대되는 가운데, 지역 허브와 연계하여 적시 배송을 실현하는 컨버터야말로 전자상거래의 물결에 올라타기에 가장 유리한 위치에 있습니다.

플라스틱 감축 정책이 섬유 소재의 채택을 가속화하고 있습니다.

확대 생산자 책임(EPR) 규제와 지역별 플라스틱 사용 금지 조치로 인해, 각 브랜드는 섬유 기반 2차 포장재로 전환해야 하는 상황에 직면해 있습니다. 정부의 순환형 경제 로드맵은 2029년까지 완벽한 폐기물 관리를 실현하는 것을 목표로 하고 있으며, 이에 따라 자카르타와 발리의 소매업체들은 수축 포장 대신 골판지 트레이나 접이식 상자로 전환하고 있습니다. 다국적 기업들은 현재 공급업체에 ISO 14001 인증을 요구하고 있으며, 이로 인해 소규모 상자 제조 공장 시장 진입 장벽이 낮아지고 있습니다. 그러나 도시 주민 중 불과 60%만이 정식 폐기물 수거 서비스를 이용할 수 있기 때문에 지방 도시에서의 효과적인 재활용은 제한적이며, 도입 현황도 고르지 않습니다. 이처럼 규제가 모자이크처럼 뒤섞인 상황은 환경 보호와 지역 특유공급망을 양립시켜야 하는 컨버터 기업들에게 비즈니스 기회를 창출하고 있습니다.

중고 골판지(OCC)/펄프 가격 변동

2026년 1월, 미국에서 수출되는 중고 골판지(OCC)의 가격은 쇼트톤당 130달러에 달했으며, 인도네시아의 강제 검사로 인해 현물 구매 시 추가 비용이 발생했습니다. 2025년 하반기, 표백 활엽수 크라프트 펄프 가격은 톤당 530달러 전후로 추이했으나, 중국 수요 감소 우려로 인해 추가 하락할 우려가 있습니다. 펄프 가격이 50달러 변동할 때마다, 수직 통합을 하지 않은 가공업체의 이익 추세는 크게 변화합니다. 이러한 가격 변동으로 인해 많은 중견 기업들은 자동화나 디지털 인쇄로의 전환을 미룰 수밖에 없게 되어, 수익성이 낮은 일반 상품 분야에 얽매이게 됩니다.

부문별 분석

인도네시아 골판지 포장 시장에서 2025년 소재 매출의 61.86%를 재생 라이너보드가 차지하고 있으며, 이는 사용 후 골판지 상자 회수에 대한 국내 투자의 효과성을 입증하고 있습니다. 내습성이 요구되는 수출 지향적인 식품·의약품 제조업체에게는 버진 크래프트 등급이 여전히 필수적이지만, 탄소 보고 비용의 상승으로 인해 그 시장 점유율은 낮은 수준에 머물러 있습니다. 골판지 구조의 핵심인 중심은 각 컨버터 업체들이 상자의 내압성을 유지하면서 중량을 줄이고 있는 추세를 반영하여 연평균 성장률(CAGR) 7.20%를 나타낼 것으로 전망됩니다. 세미케미컬 플루팅은 뛰어난 강성 대 중량 비율 덕분에 여전히 고급 가전제품이나 팔레트용 케이스 시장에서 수요를 확보하고 있지만, 에너지 소비량이 많다는 점이 주류로 채택되는 데 제약을 주고 있습니다. 도시 지역의 수거 과정에서 발생하는 오염 문제로 인해 섬유 수율이 떨어졌기 때문에 제지 업체들은 현재 파열 강도 목표를 달성하기 위해 수입 스크랩과 국내 스크랩을 혼합하고 있습니다. 따라서 인도네시아의 골판지 포장 시장에서는 높은 수율과 담수 사용량 감축을 실현하는 첨단 드럼 펄퍼를 도입한 제지 업체들이 우대받고 있습니다.

이러한 2차적인 영향이 컨버터 구매 동향에 파급되고 있습니다. 스코프 3 배출 감축을 목표로 하는 다국적 기업의 입찰에서는 현재 CoC(생산 이력) 인증을 받은 라이너 보드가 요구되고 있어, 소규모 시트 공장에 대한 문서화 요건이 증가하고 있습니다. 한편, 특수 방습 코팅(코팅이 되지 않은 원지보다 10-15% 비쌈)은 국내 식품 제조업체들의 예산상의 반발이 있음에도 불구하고, 열대 지역으로의 수출 경로를 통해 시장 점유율을 확대되고 있습니다. 바이오매스 발전 및 태양광 발전 설비를 활용하는 통합형 기업들은 전기 요금 상승에 따라 비용 격차가 더욱 확대되고 있으며, 이는 인도네시아 골판지 포장 시장에서 규모의 경제와 자사 섬유 보유가 여전히 장기적인 리스크 헤지 수단이 되는 이유를 여실히 보여주고 있습니다.

C 플루트는 4mm의 두께 덕분에 면류, 식용유, 음료의 적층성과 완충성을 동시에 확보할 수 있어, 2025년 총 생산량의 42.50%를 차지했습니다. 한편, 두께 약 1.6mm인 E-플루트는 EC 거점이 소포 1개당 부피 중량 감소를 추구하는 가운데 연평균 성장률(CAGR) 8.08%로 급성장하고 있습니다. 각 디지털 프린터 업체들은 E-플루트와 F-플루트의 매끄러운 표면이 이미지 해상도를 향상시켜, 브랜드가 소셜 미디어용 그래픽을 배송용 케이스에 직접 인쇄할 수 있다는 점을 높이 평가했습니다.

소매 진열대에서 기존에 선호되던 B-플루트는 마케터들이 더 가벼운 벽면이나 골판지 구조와는 별도로 충격을 흡수하는 전용 인서트로 전환함에 따라 어려움을 겪고 있습니다. A-플루트는 깨지기 쉬운 유리 제품을 위한 틈새 시장용 보호재로서의 입지를 유지하고 있는 반면, 마이크로-플루트 설계는 그래픽과 운송 보호 기능을 결합한 접이식 골판지 하이브리드 제품에 채택되고 있습니다. E-플루트 가공에는 더 좁은 틈새와 더 청결한 라이너가 필요하기 때문에 자사 공장에서 테스트용 라이너를 생산하는 통합 제조업체는 찌그러짐으로 인한 불량품이 적어 인도네시아 골판지 포장 시장에서 경쟁력을 높이고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the indonesia corrugated packaging market size is expected to increase from USD 2.14 billion in 2025 to USD 2.27 billion in 2026 and reach USD 3.16 billion by 2031, growing at a CAGR of 6.85% over 2026-2031.

This report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, and More), Flute Type (A Flute, and More), Packaging Type (Regular Slotted Containers, and More), Wall Type (Single, Double, and More), Printing Technology (Flexographic, and More), and End-User Industry (Processed Foods, and More). The Market Forecasts are Provided in Terms of Value (USD).

Indonesia Corrugated Packaging Market Trends and Insights

Surge in E-Commerce Shipments

Indonesia's booming parcel economy is redefining box design as platforms optimize packaging to avoid dimensional-weight tariffs and improve last-mile efficiency. Daily sales on major social-commerce channels now spawn millions of micro-orders that favor thinner E and F flutes, right-sized die-cuts, and rapid art changes. Fulfillment centers are installing automated cutters that reduce void space by up to 20 percent, compelling converters to provide on-demand blanks rather than pre-made regular slotted containers. The absence of a unified national recyclability standard adds compliance complexity for cross-border sellers, so outsized parcels often revert to heavier gauges to guarantee intact returns. As the internet economy expands beyond Java, converters that synchronize just-in-time deliveries with regional hubs are best placed to ride the e-commerce wave.

Plastic-Reduction Policies Accelerating Fiber Adoption

Extended Producer Responsibility rules and localized plastic bans are nudging brands toward fiber-based secondary packaging. The government's circular roadmap aims to achieve complete waste management by 2029, prompting retailers in Jakarta and Bali to switch from shrink wrap to corrugated trays and folding cartons. Multinationals now require ISO 14001 certification from suppliers, lifting entry barriers for smaller box plants. Adoption, however, is uneven, as only 60 percent of urban residents have access to formal waste collection, limiting effective recycling in secondary cities. This regulatory mosaic creates openings for converters that pair green credentials with region-specific supply chains.

Volatility in OCC / Pulp Prices

In January 2026, old-corrugated-container exports from the United States reached USD 130 per short ton, and Indonesia's compulsory inspections added extra cost to spot purchases. Bleached hardwood kraft pulp tracked near USD 530 per tonne late in 2025, yet looming Chinese demand weakness threatens another dip. Every USD 50 swing in pulp pricing materially alters the profit trajectories of converters without vertical integration. Such volatility forces many mid-tier players to delay automation or digital-printing upgrades, locking them into low-margin commodity segments.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Indonesia's Processed Food Industry

- Growth of Domestic Pulp and Paper Capacity

- Rising Energy and Logistics Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Indonesia corrugated packaging market drew 61.86% of 2025 material revenue from recycled linerboard, validating domestic investments in old-corrugated-containers recovery. Virgin Kraft grades remain mandatory for export-oriented food and pharma shippers wanting moisture resistance, yet rising carbon reporting costs keep their share modest. Corrugating medium, the backbone of flute structure, is on track for a 7.20% CAGR, paced by converters trimming basis weight while protecting box compression. Semi-chemical fluting still secures premium appliance and pallet cases due to its superior stiffness-to-weight, though its larger energy footprint limits mainstream adoption. Mills now mix imported and local scrap to hit burst-strength targets after contamination issues reduced fiber yield in several urban collection streams. The Indonesian corrugated packaging market, therefore, rewards mills that install advanced drum pulpers that achieve higher yields and freshwater savings.

Second-order effects ripple through converter buying. Chain-of-custody-certified linerboard is now featured in bids from multinational customers seeking Scope 3 cuts, increasing documentation requirements for smaller sheet plants. Meanwhile, specialty moisture-barrier coatings, priced 10-15% above uncoated stock, gain ground in tropical export lanes despite budget pushback from domestic food producers. Integrated players leveraging biomass power and solar arrays further widen cost gaps as grid tariffs climb, underscoring why scale plus in-house fiber remains the long-term hedge within the Indonesia corrugated packaging market.

C flute supplied 42.50% of 2025 volume because its 4 mm caliper balances stacking and cushioning for noodles, oils, and beverages. E flute, at roughly 1.6 mm, is sprinting ahead at an 8.08% CAGR as e-commerce hubs chase dimensional-weight savings per parcel. Digital printers praise E and F flutes for smoother surfaces that improve image resolution, enabling brands to print social media graphics directly on shipping cases.

B flute, historically favored for retail displays, is under pressure as marketers migrate to lighter walls and engineered inserts that handle shock separately from the corrugated structure. A flute remains a niche guardrail for fragile glassware, while microflute designs slot into folding carton hybrids that merge graphics with shipping protection. Because converting E flute needs tighter gaps and cleaner liner, integrated producers with on-site testliner enjoy fewer crush rejects, sharpening their edge in the Indonesia corrugated packaging market.

List of Companies Covered in this Report:

- PT Indah Kiat Pulp & Paper Tbk

- PT Pabrik Kertas Tjiwi Kimia Tbk

- PT Pabrik Kertas Indonesia (Pakerin)

- PT Fajar Surya Wisesa Tbk

- PT Industri Pembungkus Internasional

- PT Surabaya Mekabox

- PT Satyamitra Kemas Lestari Tbk

- PT Gema Putra Abadi

- PT Sapta Warna Cemerlang

- PT Kedawung Setia Corrugated Carton Box Industrial

- PT Edpack Karunia Persada

- PT Indo Packaging

- Rengo Co., Ltd.

- Oji Holdings Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in E-Commerce Shipments

- 4.2.2 Plastic-Reduction Policies Accelerating Fiber Adoption

- 4.2.3 Expansion of Indonesia's Processed Food Industry

- 4.2.4 Growth of Domestic Pulp & Paper Capacity

- 4.2.5 Advances in Digital & Flexographic Printing for Short Runs

- 4.2.6 Investment in Automated Fulfilment Boosting Right-Sized Boxes

- 4.3 Market Restraints

- 4.3.1 Volatility in OCC / Pulp Prices

- 4.3.2 Rising Energy & Logistics Costs

- 4.3.3 Humidity-Driven Strength Loss Requiring Costly Barriers

- 4.3.4 Fragmented Scrap-Collection & Low Recycling Rates

- 4.4 Industry Ecosystem Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Kraft Linerboard

- 5.1.2 Recycled Linerboard

- 5.1.3 Corrugating Medium

- 5.1.4 Semi-Chemical Fluting

- 5.1.5 Other Materials

- 5.2 By Flute Type

- 5.2.1 A Flute

- 5.2.2 B Flute

- 5.2.3 C Flute

- 5.2.4 E Flute

- 5.2.5 F Flute

- 5.3 By Packaging Type

- 5.3.1 Regular Slotted Containers

- 5.3.2 Die-Cut Custom Boxes

- 5.3.3 Folding Cartons

- 5.3.4 Point-of-Purchase Displays

- 5.3.5 Pallet Boxes

- 5.3.6 Other Packaging Types

- 5.4 By Wall Type

- 5.4.1 Single-Wall

- 5.4.2 Double-Wall

- 5.4.3 Triple-Wall

- 5.4.4 Single Face

- 5.5 By Printing Technology

- 5.5.1 Flexographic Printing

- 5.5.2 Digital Inkjet Printing

- 5.5.3 Litho-Lamination

- 5.5.4 Screen Printing

- 5.5.5 Other Printing Technologies

- 5.6 By End-User Industry

- 5.6.1 Processed Foods

- 5.6.2 Fresh Food and Produce

- 5.6.3 Beverages

- 5.6.4 Electrical Products

- 5.6.5 Personal Care and Cosmetics

- 5.6.6 E-Commerce Fulfilment Centers

- 5.6.7 Pharmaceuticals

- 5.6.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 PT Indah Kiat Pulp & Paper Tbk

- 6.4.2 PT Pabrik Kertas Tjiwi Kimia Tbk

- 6.4.3 PT Pabrik Kertas Indonesia (Pakerin)

- 6.4.4 PT Fajar Surya Wisesa Tbk

- 6.4.5 PT Industri Pembungkus Internasional

- 6.4.6 PT Surabaya Mekabox

- 6.4.7 PT Satyamitra Kemas Lestari Tbk

- 6.4.8 PT Gema Putra Abadi

- 6.4.9 PT Sapta Warna Cemerlang

- 6.4.10 PT Kedawung Setia Corrugated Carton Box Industrial

- 6.4.11 PT Edpack Karunia Persada

- 6.4.12 PT Indo Packaging

- 6.4.13 Rengo Co., Ltd.

- 6.4.14 Oji Holdings Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment