|

시장보고서

상품코드

2063658

유럽의 골판지 포장 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Europe Corrugated Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

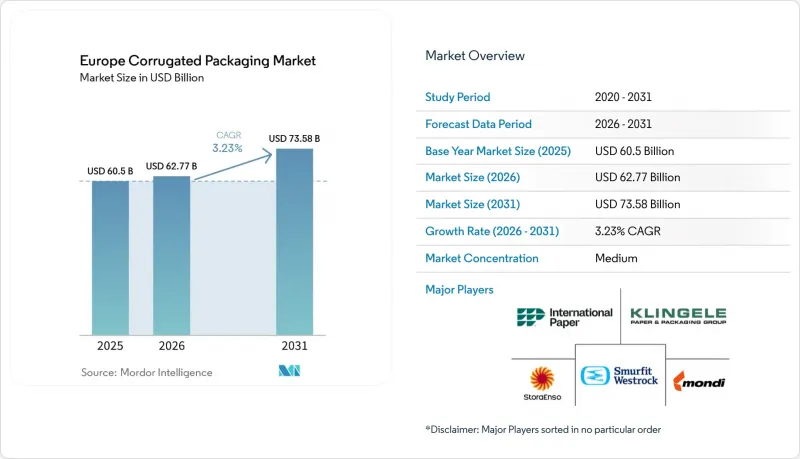

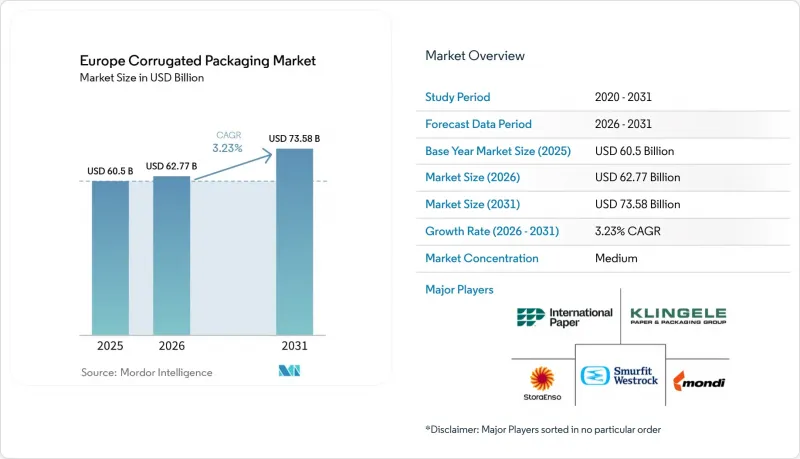

Mordor Intelligence에 의하면, 유럽 골판지 포장 시장 규모는 2025년 605억 달러에서 2026년에는 627억 7,000만 달러로 확대되어 2031년까지 735억 8,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 3.23%로 성장할 전망입니다.

본 보고서는 원료(버진 크래프트 라이너보드, 재생 라이너보드 등), 플루트 유형(A 플루트, E 플루트 등), 포장 유형(레귤러 슬롯 컨테이너 등), 벽 구조(싱글월 등), 인쇄 기술(플렉소 인쇄 등), 최종 사용자 산업(가공 식품 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽 골판지 포장 시장 동향과 인사이트

전자상거래의 급속한 성장이 경량 배송 방식에 대한 수요를 견인하고 있습니다.

현재 온라인 소매 플랫폼에서는 소포 운송 비용을 절감하면서도 자동화된 분류 공정을 여러 번 견딜 수 있는 저중량 보드가 요구되고 있습니다. 아마존과 몬디는 2025년에 연간 수백만 건의 주문을 처리할 수 있는 44그램 더 가벼워진 메일러를 출시했으며, 이를 통해 수천 톤의 라이너보드를 절감했습니다. Smurfit Westrock은 플라스틱 스트레치 필름을 대체하는 종이 팔레트 랩을 도입하여, 단위 적재물의 안정화에서 골판지의 역할을 확대했습니다. BHS Corrugated의 경량 제품군은 내압 성능을 저하시키지 않으면서 평량(g/m²)을 20g/m² 줄였습니다. 비용, 지속가능성, 그리고 스코프 3 보고에 대한 압박으로 인해, 이러한 추세는 3대 전자상거래 시장에서 가장 두드러지게 나타나고 있습니다.

FMCG 2차 포장에서의 플라스틱 대체로의 전환

각 일용소비재 제조업체들은 EU의 일회용 플라스틱 지침을 준수하기 위해 수축 포장, 트레이, 클램쉘 용기를 폐지하고 있습니다. DS Smith는 2025년까지 12억 개 이상의 플라스틱 포장재를 섬유 기반 디자인으로 대체할 것이라고 밝혔습니다. Klingele와 Maistapack의 제휴를 통해, 기존에는 폴리스티렌이 주류를 이루던 신선식품 라인에 열성형된 섬유 트레이가 도입되었습니다. 수요 증가에 따라 생산량은 늘어나고 있지만, CEPI는 2026년에 대체재 사용이 가속화되면서 재생 섬유가 수출 시장으로 유출되고 있으며, 국내 원료 공급이 부족해지고 있고, 투입 비용도 상승하고 있다고 경고했습니다.

에너지 비용 상승이 제지 공장의 영업이익률을 압박하고 있습니다.

2026년 3월, 천연가스 가격은 68유로/MWh(73달러/MWh)를 넘어섰습니다. 이탈리아는 전력 구성에서 가스 의존도가 높기 때문에 111유로/MWh(119달러/MWh)를 지불하고 있습니다. 스트라 엔소(Stora Enso)사가 3,000만 유로(3,200만 달러)를 투자해 실시한 하이노라 공장 개보수 공사를 통해 이산화탄소 배출량이 11만 3,000톤 감소했으나, 이를 위해서는 수년에 걸친 설비 투자가 필요했습니다. 에너지 가격 급등으로 인한 영향은 헤지 기능이나 열병합발전(CHP) 설비를 갖추지 않은 독립 제지 공장에서 가장 빠르게 이익률을 압박하고 있으며, 남유럽에서는 일시적인 생산 감축을 피할 수 없는 상황입니다.

부문별 분석

2025년 기준으로, 재활용 라이너보드는 유럽 골판지 포장 시장 점유율의 44.43%를 차지했습니다. 광범위한 회수 인프라와 식료품, 음료, 전자상거래 채널을 통한 안정적인 수요가 그 경쟁 우위를 뒷받침하고 있습니다. CEPI의 2024년 잠정 데이터에 따르면, 컨테이너용 판지의 생산량은 전년 대비 4.3% 증가하여 공급의 회복력이 확인되었습니다. 버진 크래프트 라이너 보드는 의약품 및 고급 식품 분야에서 더 높은 습윤 강도와 배리어 코팅과의 적합성이 요구됨에 따라, 2031년까지 연평균 5.62%의 성장률을 보일 것으로 전망됩니다. 세미케미컬 플루팅은 그램당 강성이 비용을 상회하는 삼중벽 수출용 골판지 상자에서 그 중요성이 커지고 있습니다. 유럽의 버징 등급 골판지 포장 시장은 가공업체들이 섬유 품질의 편차를 줄여감에 따라 확대될 것으로 보입니다.

폐지(OCC) 가격 변동에 따라 재생 시트와 버진 시트 간의 가격 차이는 줄어들고 있으며, 재생 라이너에 대한 비용 측면에서의 자연스러운 선호도는 점차 약화되고 있습니다. 마이어-멜른호프사는 아시아에서의 수입 압력과 스칸디나비아 지역의 과잉 생산 능력이 재생 제품의 이익률을 압박하는 요인으로 지목했습니다. 재활용 함량에 관한 규제 요건으로 인해 여전히 구매는 사용 후 섬유에 치우쳐 있지만, 기능적 제약이나 식품 접촉 규제로 인해 재활용 경로가 복잡해지는 경우, 브랜드 측에서는 버진 원료를 수용할 가능성이 있습니다. 따라서 원자재의 배합은 가격뿐만 아니라 최종 용도에서의 성능에 크게 좌우되며, 이러한 미묘한 차이가 유럽 골판지 포장 시장의 조달 형태를 재편하고 있습니다.

B 플루트는 2025년에도 총 생산량의 38.45%를 차지하며, 그 쿠션성과 무게의 균형이 높이 평가받고 있습니다. 각 브랜드 기업들은 직접 인쇄가 가능한 소매용 포장에 E-플루트를 채택하는 추세를 보이고 있으며, 이에 따라 2031년까지의 연평균 성장률(CAGR)은 5.23%로 예측됩니다. 디지털 화이트 잉크의 도입으로 기존 인쇄 품질의 격차가 해소되어, E-플루트는 화장품 및 과자류의 홍보 용도로도 적합한 선택지가 되었습니다. BHS Corrugated의 eCom 프로파일은 E-플루트 및 F-플루트 생산에 최적화되어 있으며, 압축 강도를 유지하면서 종이 사용량을 줄이고 있습니다.

C 플루트와 A 플루트는 중량물 지지용으로 적합하지만, 최대 적재 강도보다 운송 공간, 탄소 배출 목표, 선반 밀도가 더 중요시되는 분야에서는 시장 점유율을 잃고 있습니다. 규제로 인한 여유 공간의 제약 또한 슬림형 플루트의 경쟁력을 더욱 높여주고 있습니다. 왜냐하면, 용기가 너무 크면 소매업체로부터 벌금을 물게 될 위험이 따르기 때문입니다. 소매업체들이 진열 가능한 치수를 표준화하는 가운데, 컨버터들은 마이크로플루트의 생산 능력을 확대하고 콤팩트한 형태의 강도를 보장함으로써, 유럽 골판지 포장 시장 규모 전망에서 얇은 프로파일의 성장세를 유지하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the europe corrugated packaging market size is expected to increase from USD 60.50 billion in 2025 to USD 62.77 billion in 2026 and reach USD 73.58 billion by 2031, growing at a CAGR of 3.23% over 2026-2031.

This report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, and More), Flute Type (A Flute, E Flute, and More), Packaging Type (Regular Slotted Containers, and More), Wall Type (Single-Wall, and More), Printing Technology (Flexographic Printing, and More), End-User Industry (Processed Foods, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe Corrugated Packaging Market Trends and Insights

E-Commerce Boom Driving Demand for Lightweight Shipping Formats

Online retail platforms now specify lower-basis-weight boards that can withstand multiple automated sortation passes while reducing parcel freight costs. Amazon and Mondi released a 44-gram lighter mailer in 2025 that scales across millions of annual orders, saving thousands of tonnes of linerboard. Smurfit Westrock introduced a paper pallet wrap that substitutes plastic stretch film, widening corrugated's role in unit-load stabilization. Lightweight profiles from BHS Corrugated lower grammage by 20 g/m2 without sacrificing compression performance. Cost, sustainability, and Scope 3 reporting pressures make this driver most acute in the three largest e-commerce markets.

Shift Toward Plastic Substitution in FMCG Secondary Packaging

Fast-moving consumer goods owners are eliminating shrink wrap, trays, and clamshells as they work toward compliance with the EU Single-Use Plastics Directive. DS Smith reported that it would replace more than 1.2 billion plastic packs with fiber-based designs by 2025. Klingele's tie-up with Maistapack brought thermoformed fiber trays for fresh produce lines historically dominated by polystyrene. While demand lifts volume, Cepi cautioned in 2026 that accelerated substitution is draining recovered fibers to export markets, tightening domestic feedstock, and lifting input costs.

Rising Energy Costs Squeezing Mill Operating Margins

Natural-gas prices jumped above EUR 68/MWh (USD 73/MWh) in March 2026, with Italy paying EUR 111/MWh (USD 119/MWh) because of its gas-heavy power mix. Stora Enso's EUR 30 million (USD 32 million) Heinola upgrade cut emissions by 113,000 tCO2 yet required multi-year capex. Energy shocks compress margins fastest at independent mills that lack hedging or CHP capacity, prompting temporary curtailments in Southern Europe.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Recycled-Content Targets Under EU Rules

- Increasing Demand for Shelf-Ready Packaging in Retail Chains

- Volatility In Old Corrugated Container Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled linerboard owned 44.43% of Europe corrugated packaging market share in 2025. Widespread collection infrastructure and stable demand from grocery, beverage, and e-commerce channels anchor its dominance. Cepi's preliminary 2024 data showed containerboard output rising 4.3% year-on-year, confirming supply resilience. Virgin Kraft Linerboard is projected to grow at 5.62% annually through 2031, as pharmaceuticals and premium foods require higher wet-strength and greater barrier-coating compatibility. Semi-chemical fluting gains relevance in triple-wall export cartons, where stiffness per gram outweighs cost. The European corrugated packaging market for virgin grades will expand as converters mitigate fiber-quality variability.

Competitive pricing gaps between recycled and virgin sheets have narrowed due to volatile OCC costs, reducing the automatic cost preference for recycled liners. Mayr-Melnhof flagged import pressure from Asia and extra Scandinavian capacity as forces weighing on recycled margins. Regulatory recycled-content mandates still tilt purchasing toward post-consumer fibers, yet brands may accept virgin inputs when functional barriers or food-contact rules complicate recycling pathways. The material mix, therefore, hinges on end-use performance more than price alone, a nuance that reshapes procurement within the European corrugated packaging market.

B flute maintained 38.45% of overall volume in 2025, prized for its cushioning-to-weight balance. Brands are turning to E flute for direct-print retail-ready packs, propelling a 5.23% CAGR outlook through 2031. Digital white-ink launches eliminated historic print-quality gaps, making E flute viable for cosmetics and confectionery promotions. BHS Corrugated's eCom profile is optimized for E and F flute runs, reducing paper usage while maintaining compression strength.

C flute and A flute support heavy goods but lose share where freight space, carbon targets, and shelf density matter more than maximum stacking strength. Regulatory empty-space limits further favor thinner flutes because oversized containers risk retailer penalties. As retailers standardize shelf-ready dimensions, converters extend microflute capability to guarantee strength in compact forms, sustaining momentum for thin profiles in the Europe corrugated packaging market size forecasts.

List of Companies Covered in this Report:

- Smurfit Westrock plc

- Mondi plc

- International Paper Company

- Stora Enso Oyj

- Saica Group

- VPK Group NV

- Pro-Gest S.p.A.

- Klingele Papierwerke SE & Co. KG

- Model Holding AG

- Prinzhorn Holding GmbH

- Mayr-Melnhof Karton AG

- LEIPA Group GmbH

- Cartonajes International S.L.

- THIMM Group GmbH + Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-Commerce Boom Driving Demand for Lightweight Shipping Formats

- 4.2.2 Shift Toward Plastic Substitution in FMCG Secondary Packaging

- 4.2.3 Increasing Demand for Shelf-Ready Packaging in Retail Chains

- 4.2.4 Automation of Corrugator Lines Enabling Shorter Lead-Times

- 4.2.5 Rapid Growth of Meal-Kit and Grocery Delivery Services

- 4.2.6 Mandatory Recycled-Content Targets Under EU Packaging and Packaging Waste Regulation

- 4.3 Market Restraints

- 4.3.1 Volatility In Old Corrugated Container (OCC) Prices

- 4.3.2 Rising Energy Costs Squeezing Mill Operating Margins

- 4.3.3 Competition From Reusable Plastic Crates in Fresh-Produce Logistics

- 4.3.4 Limited Corrugator Capacity Additions Due to Permitting Hurdles

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Virgin Kraft Linerboard

- 5.1.2 Recycled Linerboard

- 5.1.3 Corrugating Medium

- 5.1.4 Semi-Chemical Fluting

- 5.1.5 Other Materials

- 5.2 By Flute Type

- 5.2.1 A Flute

- 5.2.2 B Flute

- 5.2.3 C Flute

- 5.2.4 E Flute

- 5.2.5 F Flute

- 5.3 By Packaging Type

- 5.3.1 Regular Slotted Containers

- 5.3.2 Die-Cut Custom Boxes

- 5.3.3 Folding Cartons

- 5.3.4 Point-of-Purchase Displays

- 5.3.5 Pallet Boxes

- 5.3.6 Other Packaging Types

- 5.4 By Wall Type

- 5.4.1 Single-Wall

- 5.4.2 Double-Wall

- 5.4.3 Triple-Wall

- 5.4.4 Single Face

- 5.5 By Printing Technology

- 5.5.1 Flexographic Printing

- 5.5.2 Digital Inkjet Printing

- 5.5.3 Litho-Lamination

- 5.5.4 Screen Printing

- 5.5.5 Other Printing Technologies

- 5.6 By End-User Industry

- 5.6.1 Processed Foods

- 5.6.2 Fresh Food and Produce

- 5.6.3 Beverages

- 5.6.4 Electrical Products

- 5.6.5 Personal Care and Cosmetics

- 5.6.6 E-commerce Fulfillment Centers

- 5.6.7 Pharmaceuticals

- 5.6.8 Other End-User Industries

- 5.7 By Geography

- 5.7.1 Germany

- 5.7.2 France

- 5.7.3 United Kingdom

- 5.7.4 Italy

- 5.7.5 Spain

- 5.7.6 Benelux

- 5.7.7 Nordic Countries

- 5.7.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit Westrock plc

- 6.4.2 Mondi plc

- 6.4.3 International Paper Company

- 6.4.4 Stora Enso Oyj

- 6.4.5 Saica Group

- 6.4.6 VPK Group NV

- 6.4.7 Pro-Gest S.p.A.

- 6.4.8 Klingele Papierwerke SE & Co. KG

- 6.4.9 Model Holding AG

- 6.4.10 Prinzhorn Holding GmbH

- 6.4.11 Mayr-Melnhof Karton AG

- 6.4.12 LEIPA Group GmbH

- 6.4.13 Cartonajes International S.L.

- 6.4.14 THIMM Group GmbH + Co. KG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment