|

시장보고서

상품코드

2063908

스킬 인텔리전스 및 분류 플랫폼 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Skills Intelligence And Taxonomy Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

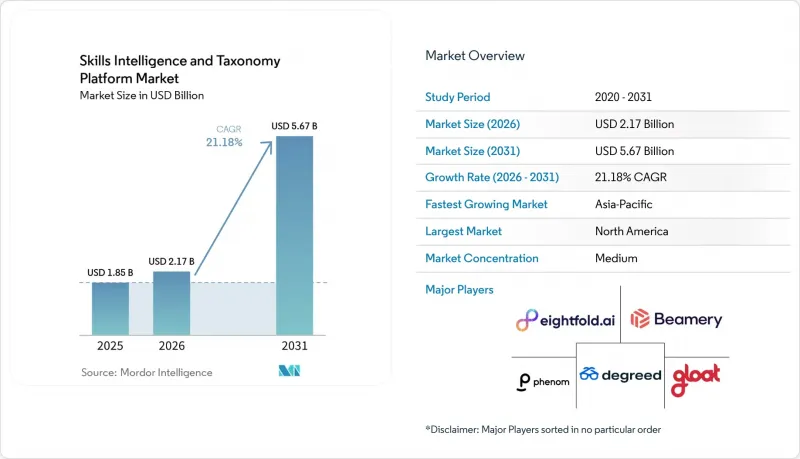

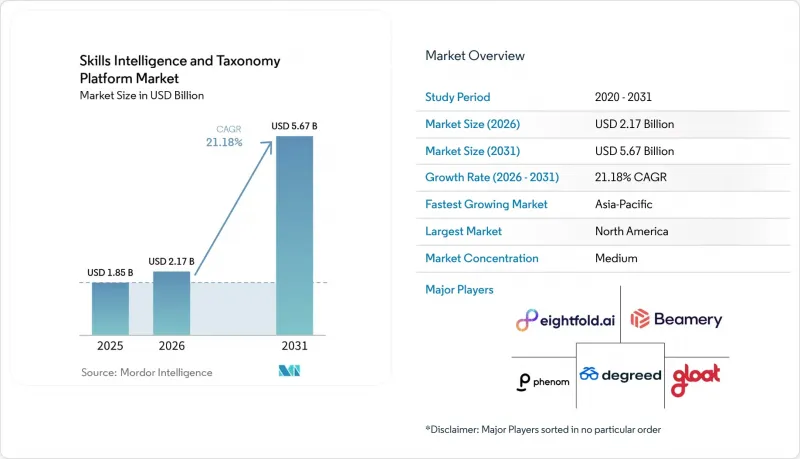

Mordor Intelligence에 의하면, 스킬 인텔리전스 및 분류 플랫폼 시장 규모는 2025년에 18억 5,000만 달러로 평가되었고, 2026년 21억 7,000만 달러로 추정되고, 2031년까지 56억 7,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 21.18%를 나타낼 전망입니다.

본 보고서는 구성 요소별(플랫폼 소프트웨어 및 서비스), 배포 모델별(클라우드, 온프레미스, 하이브리드), 최종 사용자 기업 규모별(대기업 및 중소기업), 용도별(인력 관리 및 사내 인사 이동, 기타), 최종 사용자 산업별(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 스킬 인텔리전스 및 분류 플랫폼 시장 동향과 인사이트

스킬 기반 조직 설계로의 전환이 인재 아키텍처를 재구축합니다.

조직은 고정된 직무 설명서에서 벗어나, 갱신·비교·역할 간 재배치가 가능한 역량을 기반으로 한 인재 모델을 구축해 나가고 있습니다. 이러한 압박은 명백하며, 『Future of Jobs Report 2025』에 따르면 고용주의 63%가 기술 격차를 변화의 주요 장애물로 꼽고 있어, 이로 인해 계획 수립 논의에서 정적인 역할 체계를 유지하기가 점점 더 어려워지고 있습니다. 이러한 변화로 인해, 각 부서가 독자적인 역량 목록을 관리하는 대신, 채용, 교육, 인사 이동, 프로젝트 인력 배치의 전 과정에서 공통된 역량 언어를 유지할 수 있는 플랫폼에 대한 수요가 높아지고 있습니다. 기계 판독 가능한 분류 체계가 기업 차원에서 인재 공급과 비즈니스 수요를 연결하는 운영 계층으로 자리 잡고 있어, 스킬 인텔리전스 및 분류 플랫폼 시장이 그 혜택을 누리고 있습니다. 기업이 매번 역할의 틀을 재구성하지 않고 팀, 기능, 새로운 업무 방식 모델 간에 인력을 보다 신속하게 재배치하려고 시도함에 따라, 그 필요성은 더욱 커지고 있습니다. 세계경제포럼이 2025년 전망에서 스킬 인텔리전스를 ‘경제 인프라’로 규정했던 것은 이러한 플랫폼이 단기적인 인사 부서의 실험이 아니라 장기적인 기업 예산의 대상이 되어가고 있는 이유를 정확히 짚어낸 것입니다.

사내 인사 이동과 인재 유지를 위한 투자가 플랫폼 도입을 촉진

사내 인사는 단순한 인사 관리의 실천에 그치지 않고, 재무적 의사결정의 한 요소로 자리 잡고 있습니다. 이는 기업이 외부 채용에 의존하기 전에, 기존 직원들로 더 많은 업무를 처리하고자 하기 때문입니다. 스킬 인텔리전스 플랫폼은 관리자와의 친밀도뿐만 아니라 검증되었거나 추론된 역량을 활용하여 직원을 역할, 프로젝트 및 관련 기회에 매칭함으로써 이러한 변화를 지원합니다. 2026년 4월, 365Talents가 SNCF가 AI를 활용한 역량 매칭을 통해 임시 인건비를 1억 1,300만 달러 절감했다고 보고한 것은 이를 입증하는 대표적인 사례가 되었습니다. LinkedIn의 ‘2026년 인재 이동성 보고서’ 역시 조직 중 불과 14%만이 ‘인재 이동성 리더’로 인정받고 있음을 보여주고 있으며, 이는 많은 고용주가 여전히 사내에서 인재를 효율적으로 이동시키기 위한 인프라를 갖추지 못하고 있음을 시사합니다. 이러한 격차가 플랫폼에 대한 수요를 뒷받침하고 있습니다. 왜냐하면 인재의 정착, 재배치, 노동력의 가시화가 점점 더 하나로 통합되어 자금이 지원되고 있기 때문입니다. 그 결과, 구매자들은 스킬 관리 시스템을 단순한 인사 프로세스 개선 도구로만 보는 것이 아니라, 채용에 대한 의존도를 낮추고 인력의 안정성을 높이는 수단으로 인식하게 되었습니다.

직원 데이터의 개인정보 보호 및 AI 거버넌스 부담이 도입 규모를 제한하고 있습니다.

이러한 플랫폼들은 신고된 프로파일 데이터에만 의존하는 것이 아니라, 업무 행동, 협업 패턴, 성과 지표 등을 바탕으로 직원의 역량을 추론하는 경우가 많기 때문에 개인정보 보호 의무는 여전히 실질적인 장벽으로 남아 있습니다. 이에 따라, 특히 추론된 기술이 인사 이동, 채용 또는 인재 개발 결정에 영향을 미치는 경우, EU AI법과 GDPR(EU 개인정보보호규정) 제22조에 따른 추가적인 검토가 필요합니다. 2026년 1월 와튼 스쿨과 액센츄어가 실시한 분석에서도, 직원이 '할 수 있다'고 주장하는 것과 고용주의 AI 시스템이 추론하거나 평가하는 것 사이에 괴리가 있다는 점이 지적되었으며, 이로 인해 법무 부서나 인사 부서가 무시할 수 없는 공정성 관련 우려가 제기되고 있습니다. 실제로 이는 도입 과정에서 모델 문서, 동의 워크플로우, 데이터 처리 조건, 감독 책임을 포괄하는 보다 장기적인 검토가 빈번하게 이루어진다는 것을 의미합니다. 이러한 영향은 규제 산업이나 유럽에서 가장 두드러지며, 비즈니스 케이스가 승인된 후에도 리스크 관리 팀이 도입을 지연시킬 가능성이 있습니다. 이로 인해 수요가 사라지는 것은 아니지만, 조달 주기가 길어지게 되어 초기 도입은 위험이 낮은 이용 사례로 한정될 것입니다.

부문별 분석

2025년, 스킬 인텔리전스 및 분류 플랫폼 시장 점유율의 72.41%를 플랫폼 소프트웨어가 차지했으며, 이는 분류 엔진, 온톨로지 관리, 스킬 그래프 인프라에 대한 구매자들의 선호도를 뒷받침하고 있습니다. 이러한 우위는 채용, 학습, 인사 이동, 인재 계획 등 모든 영역에 걸쳐 표준화된 기술 언어의 필요성을 반영하고 있으며, 거버넌스가 적용된 분류 체계와 추론 엔진이 지속 가능한 조직 역량의 기반을 형성하고 있습니다. 플랫폼에 대한 수요는 인간의 업무 흐름과 AI 지원형 의사결정을 모두 뒷받침하는 지속적으로 업데이트되는 기계 가독형 기술 구조와도 밀접하게 연관되어 있으며, 향후 서비스에 따라 계약 범위가 확대되더라도 소프트웨어 계층이 대부분의 기업이 구매를 시작하는 출발점이 되고 있습니다.

그러나 서비스 부문은 2026-2031년 연평균 성장률(CAGR) 23.61%를 나타낼 것으로 예측되고 있으며, 복잡한 조직 내에서 분류 체계를 운영에 적용하는 데 따르는 어려움이 부각되고 있습니다. 기업은 실제 워크플로우에서 생성된 결과물을 신뢰할 수 있게 되기 전에, 통합 설계, 분류 체계 큐레이션, 모델 훈련, 변경 관리가 필요한 경우가 많습니다. Gloat가 2026년 3월에 출시한 ‘Agentic HR Platform’(240만 개의 스킬 노드와 1,870만 개의 스킬 관계를 포함)은 온톨로지의 깊이가 전문적인 구성 및 거버넌스 지원에 대한 수요를 어떻게 주도하고 있는지를 보여줍니다. 마찬가지로, SAP, Workday, ServiceNow의 지원을 받은 TechWolf의 2024년 6월 자금 조달 라운드는 전문적인 분류 체계 인프라가 대규모 제품군 생태계에서 배제되는 것이 아니라 공존할 수 있다는 확신을 더욱 공고히 했습니다. 이러한 추세는 소프트웨어가 수익의 기반이 되는 한편, 구매자들이 시범 도입 단계에서 전사적 프로그램으로 전환함에 따라 서비스가 더욱 빠르게 성장하는 시장 구조를 뒷받침하고 있습니다.

2025년, 스킬 인텔리전스 및 분류 플랫폼 시장의 68.92%를 클라우드 기반 솔루션이 차지했으며, 이는 업데이트 속도 향상, 인프라 부하 경감, 실시간 데이터 수집에 대한 강력한 지원과 같은 운영상의 이점을 반영한 것입니다. 스킬 플랫폼의 가치는 협업, 학습, 채용, 프로젝트 데이터를 통한 빈번한 업데이트에 달려 있으므로, 클라우드 아키텍처가 특히 적합합니다. 이에 따라, 정기적인 직원 설문조사보다는 지속적인 분석을 필요로 하는 조직의 경우, 클라우드 제공 방식이 가장 실용적인 모델이 됩니다. 또한, 지역이나 사업 부문을 넘나들며 신속하게 사업을 전개할 수 있는 능력도 중요합니다. 구매자들이 현재의 예산 주기 내에서 가시적인 가치를 점점 더 요구하고 있기 때문에 신규 도입 시 온프레미스 방식보다 클라우드가 선호되는 이유도 바로 여기에 있습니다.

클라우드 도입은 2031년까지 연평균 성장률(CAGR) 24.83%로 확대될 것으로 예상되며, 이 부문은 시장 전체를 상회하는 성장세를 유지할 전망입니다. 2026년 3월 마이크로소프트가 ‘People Skills’를 확대한 것은 클라우드 제공이 이미 표준이 된 일상 업무 시스템에 스킬 인텔리전스가 어떻게 통합되어 있는지를 보여주었습니다. 반면, 데이터 관리가 이사회 차원의 요건이 되는 국방, 정부, 기밀성이 높은 의료 현장에서는 온프레미스 환경이 여전히 중요하게 여겨지고 있습니다. 하이브리드 모델은 특히 은행/금융서비스/보험, 에너지 부문에서 직원 기록에 대한 관리 권한을 완전히 포기하지 않으면서도 클라우드 추론을 도입하고자 하는 조직들 사이에서 중간적인 대안으로 부상하고 있습니다. 시간이 지남에 따라, 수동적인 업무 신호 수집과 실시간 온톨로지 업데이트 간의 균형은 계속해서 클라우드에 유리하게 작용하며, 규제와 주권이 중시되는 상황에서 하이브리드에 대한 수요가 지속되더라도 이 배포 모델이 우위를 유지할 것임을 보장합니다.

지역별 분석

2025년, 북미는 스킬 인텔리전스 및 분류 플랫폼 시장 점유율의 41.61%를 차지했으며, 세계 최대의 지역이 되었습니다. 이 지역은 엔터프라이즈 HR 기술 공급업체, 도입 파트너, 기술 기반 운영 모델을 조기에 도입한 기업들로 구성된 긴밀한 생태계의 혜택을 누리고 있습니다. 미국은 여전히 수요의 핵심 원동력으로 자리 잡고 있습니다. 이는 기술, 금융 서비스, 컨설팅 분야의 주요 고용주들이 급변하는 직무 요건과 사내 이동에 대한 기대감으로 인해 지속적인 압박에 직면하고 있기 때문입니다. 캐나다는 디지털 기술에 대한 투자와 기업의 현대화를 통해 비슷한 길을 걷고 있지만, 멕시코는 여전히 초기 단계에 머물러 있으며, 도입은 다국적 기업에 집중되어 있습니다. 스킬 인텔리전스 및 분류 플랫폼 시장에서 북미가 계속해서 주도적인 위치를 차지하고 있는 이유는 상용화 준비 상황, 소프트웨어 생태계의 깊이, 기업 예산이 다른 어떤 지역보다 밀접하게 조화를 이루고 있기 때문입니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역 부문으로, 2026-2031년 시장이 연평균 성장률(CAGR) 28.51%로 확대될 것으로 전망됩니다. 이 지역의 성장은 싱가포르, 인도, 한국의 정부 주도의 재교육 프로그램에 힘입어 이루어지고 있으며, 이러한 프로그램들은 민관 양측의 인력 이니셔티브에서 체계적인 기술 프레임워크를 표준화하고 있습니다. 정책 지원 덕분에, 고립된 내부 역량 모델이 아닌 표준화된 분류 체계 도구에 대한 고용주 수요가 창출되고 있습니다. 유럽은 여전히 주요 수익원이지만, 그 수요 패턴은 재량적인 생산성 향상 지출이라기보다는 규제와 규정 준수에 의해 더 크게 좌우되고 있습니다. 규제 활동으로 인해 지역 전체에서 감사 가능한 구조화된 인력 데이터의 중요성이 커지고 있으며, 유럽 수요 동향을 보면 인재 최적화 목표와 마찬가지로 거버넌스 및 보고 요구 사항에 따라 인력을 확보하는 경우가 늘고 있습니다.

남미는 여전히 초기 단계 시장이며, 브라질과 아르헨티나가 주요 상업적 진출 거점으로 자리 잡고 있습니다. 이 도입은 현지에서 시작된 대규모 조달이라기보다는 세계 인사 플랫폼을 지역 사업으로 확대하는 다국적 기업의 자회사가 주도하고 있습니다. 중동은 더욱 급속히 발전하고 있으며, 특히 사우디아라비아와 아랍에미리트에서는 국가 차원의 노동력 혁신 프로그램을 통해 체계적인 기술 매핑 및 현지화된 분류 체계에 대한 지원 수요가 발생하고 있습니다. 아프리카는 아직 초기 단계에 있지만, 남아프리카공화국, 나이지리아, 케냐에서는 금융 서비스, 통신, 인력 개발 분야에서 초기 성장세가 나타나고 있습니다. 이러한 신흥 지역 전반에 걸쳐, 시장은 북미에서 주류를 이루고 있는 기업 주도적 효율화 논리보다는 정책 주도적인 노동력 관련 문서화 및 현대화 과제에 의해 형성되고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the skills intelligence and taxonomy platform market size was valued at USD 1.85 billion in 2025 and estimated to grow from USD 2.17 billion in 2026 to reach USD 5.67 billion by 2031, at a CAGR of 21.18% during the forecast period (2026-2031).

This report is Segmented by Component (Platform Software, and Services), Deployment Model (Cloud, On-Premises, and Hybrid), End User Enterprise Size (Large Enterprises, and SMEs), Application (Talent Management and Internal Mobility, and More), End User Industry Vertical (IT and Telecommunications, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Skills Intelligence And Taxonomy Platform Market Trends and Insights

Shift To Skills-Based Organization Design Reshapes Talent Architecture

Organizations are moving away from fixed job descriptions and are building workforce models around skills that can be updated, compared, and redeployed across roles. The pressure is clear because 63% of employers identified skills gaps as the main barrier to transformation in the Future of Jobs Report 2025, which makes static role frameworks harder to defend in planning discussions. This shift raises demand for platforms that can maintain a common skills language across hiring, learning, mobility, and project staffing, rather than leaving each function to manage its own competency lists. The skills intelligence and taxonomy platform market is benefiting because a machine-readable taxonomy is becoming the operating layer that links workforce supply to business demand at enterprise scale. That need grows stronger as companies try to redeploy talent faster across teams, functions, and new work models without rebuilding role frameworks each time. The World Economic Forum's 2025 description of skills intelligence as economic infrastructure captures why these platforms are moving into long-cycle enterprise budgets rather than short-term HR experimentation.

Internal Mobility And Retention Investment Drives Platform Adoption

Internal mobility is becoming a financial decision, not just a talent practice, because enterprises want to fill more work with existing employees before turning to external hiring. Skills intelligence platforms support that shift by matching workers to roles, projects, and adjacent opportunities using verified or inferred capabilities instead of manager familiarity alone. A strong proof point came in April 2026, when 365Talents reported that SNCF saved USD 113 million in temporary labor costs through AI-driven skills matching. LinkedIn's 2026 Talent Velocity Report also showed that only 14% of organizations qualify as talent velocity leaders, suggesting that many employers still lack the infrastructure to move talent efficiently within the business. That gap is supporting platform demand because retention, redeployment, and workforce visibility are increasingly being funded together. As a result, buyers are treating skills systems as a way to lower hiring dependency and improve workforce stability, not only as a tool for HR process improvement.

Employee Data Privacy And Artificial Intelligence Governance Burden Constrains Deployment Scale

Privacy obligations remain a real barrier because these platforms often infer employee skills from work behavior, collaboration patterns, and performance signals rather than relying only on declared profile data. That creates additional scrutiny under the EU AI Act and GDPR Article 22, especially when inferred skills influence mobility, hiring, or development decisions. A January 2026 Wharton and Accenture analysis also highlighted gaps between what workers say they can do and what employer AI systems infer or reward, raising fairness concerns that legal and HR teams cannot ignore. In practice, that means deployments often face longer reviews covering model documentation, consent workflows, data processing terms, and oversight responsibilities. The effect is most visible in regulated industries and in Europe, where risk teams can slow a rollout even after the business case has been accepted. This does not remove demand, but it does stretch procurement cycles and narrows early deployments to lower-risk use cases.

Other drivers and restraints analyzed in the detailed report include:

- Cloud-Native Artificial Intelligence Delivery Accelerates Time-To-Value

- Regulatory Pressure Turns Skills Data Into A Compliance Asset

- Integration Complexity Across Human Capital And Learning Systems Delays ROI Realization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platform software held 72.41% of the skills intelligence and taxonomy platform market share in 2025, underscoring buyer preference for taxonomy engines, ontology management, and skills graph infrastructure. This dominance reflects the need for standardized skills language across hiring, learning, mobility, and workforce planning, with governed taxonomies and inference engines forming the backbone of durable organizational capability. Demand for platforms is also tied to continuously updated, machine-readable skill structures that support both human workflows and AI-assisted decision-making, making the software layer the starting point for most enterprise purchases, even when services later expand the deal scope.

Services, however, are projected to grow at a 23.61% CAGR from 2026 to 2031, highlighting the difficulty of operationalizing taxonomy systems inside complex organizations. Enterprises often require integration design, taxonomy curation, model training, and change management before they can trust outputs in real workflows. Gloat's March 2026 launch of its Agentic HR Platform, with 2.4 million skill nodes and 18.7 million skill relationships, illustrates how ontology depth drives demand for expert configuration and governance support. Similarly, TechWolf's June 2024 funding round, backed by SAP, Workday, and ServiceNow, reinforced confidence that specialist taxonomy infrastructure can coexist with large-suite ecosystems rather than being displaced. This dynamic supports a market structure in which software anchors revenue, while services grow faster as buyers move from pilot deployments to enterprise-wide programs.

Cloud-based deployment held 68.92% of the skills intelligence and taxonomy platform market share in 2025, reflecting operational advantages such as faster updates, lower infrastructure burden, and stronger support for real-time data ingestion. Cloud architectures are particularly well-suited to skills platforms because their value depends on frequent refreshes from collaboration, learning, recruiting, and project data. This makes cloud delivery the most practical model for organizations seeking continuous inference rather than periodic workforce surveys. The ability to roll out quickly across geographies and business units also matters, as buyers increasingly demand visible value within current budget cycles, explaining why greenfield deployments now favor cloud over on-premises alternatives.

Cloud deployments are forecast to expand at a 24.83% CAGR through 2031, keeping this segment ahead of the broader market. Microsoft's People Skills expansion in March 2026 demonstrated how skills intelligence is being embedded into daily work systems where cloud delivery is already the norm. At the same time, on-premises environments remain relevant in defense, government, and sensitive healthcare settings where data control is a board-level requirement. Hybrid models are emerging as a middle path, particularly in the banking, financial services, insurance, and energy sectors, where organizations want cloud inference without fully relinquishing control over employee records. Over time, the balance between passive work-signal capture and real-time ontology updates continues to favor the cloud, ensuring this deployment model maintains its lead even as hybrid demand persists in regulated or sovereignty-sensitive contexts.

Geography Analysis

North America held 41.61% of the skills intelligence and taxonomy platform market share in 2025, making it the largest region worldwide. The region benefits from a dense ecosystem of enterprise HR technology vendors, implementation partners, and early adopters of skills-based operating models. The United States remains the central demand engine because large employers in technology, financial services, and consulting face recurring pressure from fast-changing role requirements and internal mobility expectations. Canada is following a similar path through digital skills investment and enterprise modernization, while Mexico remains at an earlier stage, with adoption concentrated among multinational employers. In the skills, intelligence, and taxonomy platform market, North America continues to lead because commercial readiness, software ecosystem depth, and enterprise budgets are more closely aligned here than in any other region.

Asia-Pacific is the fastest-growing regional segment, with the market projected to rise at a 28.51% CAGR from 2026 to 2031. Growth in the region is supported by government-backed reskilling programs in Singapore, India, and South Korea, which are normalizing structured skills frameworks across both public and private workforce initiatives. Policy support helps create employer demand for standardized taxonomy tools instead of isolated internal competency models. Europe remains a major revenue contributor, but its demand pattern is shaped more heavily by regulation and compliance than by discretionary productivity spending. Regulatory activity has increased the importance of auditable, structured workforce data across the region, giving Europe a demand profile in which procurement is often triggered by governance and reporting needs as much as by talent-optimization goals.

South America remains an earlier-stage opportunity, with Brazil and Argentina as the main commercial entry points. Adoption is still led mainly by multinational subsidiaries extending global HR platforms into regional operations rather than by large volumes of locally originated procurement. The Middle East is developing faster, especially in Saudi Arabia and the UAE, where national workforce transformation programs are creating demand for structured skills mapping and localized taxonomy support. Africa is at the earliest stage, with South Africa, Nigeria, and Kenya showing initial momentum across financial services, telecommunications, and workforce development initiatives. Across these emerging regions, the market is being shaped more by policy-led workforce documentation and modernization agendas than by the enterprise-led efficiency logic that dominates in North America.

- Eightfold AI Inc.

- Beamery Inc.

- Degreed, Inc.

- Gloat Ltd.

- Fuel50 Limited

- TechWolf BV

- Phenom People, Inc.

- iMocha Inc.

- TalentGuard, Inc.

- Censia, Inc.

- Workera Corp.

- Textkernel B.V.

- 365Talents SAS

- Neobrain SAS

- Reejig Pty Ltd.

- ProFinda Limited

- Draup, Inc.

- TalentNeuron, LLC

- Lightcast LLC

- SkillsDB Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift To Skills-Based Organization Design Reshapes Talent Architecture

- 4.2.2 Internal Mobility And Retention Investment Drives Platform Adoption

- 4.2.3 Cloud-Native Artificial Intelligence Delivery Accelerates Time-To-Value

- 4.2.4 Regulatory Pressure Turns Skills Data Into A Compliance Asset

- 4.2.5 Agentic Workflow Procurement Increasing Demand For Machine-Readable Skills Graphs

- 4.2.6 Verifiable Credentials And Skills Wallets Improving Cross-Employer Skill Portability

- 4.3 Market Restraints

- 4.3.1 Employee Data Privacy And Artificial Intelligence Governance Burden Constrains Deployment Scale

- 4.3.2 Integration Complexity Across Human Capital And Learning Systems Delays ROI Realization

- 4.3.3 Taxonomy Drift From Rapid Emergence Of Hybrid Human-Artificial Intelligence Roles

- 4.3.4 Embedded Skills Layers In Human Capital Suites Compressing Standalone Pricing Power

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Platform Software

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By Application

- 5.4.1 Talent Management and Internal Mobility

- 5.4.2 Strategic Workforce Planning

- 5.4.3 Learning and Development (L&D)

- 5.4.4 Recruitment and Talent Acquisition

- 5.4.5 Performance and Succession Management

- 5.4.6 Skills Gap Analysis and Workforce Analytics

- 5.5 By End User Industry Vertical

- 5.5.1 Information Technology (IT) and Telecommunications

- 5.5.2 Banking, Financial Services, and Insurance (BFSI)

- 5.5.3 Healthcare and Life Sciences

- 5.5.4 Manufacturing and Industrial Operations

- 5.5.5 Retail and E-commerce

- 5.5.6 Education

- 5.5.7 Government and Public Sector

- 5.5.8 Energy and Utilities

- 5.5.9 Media and Entertainment

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 Singapore

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Nigeria

- 5.6.6.4 Kenya

- 5.6.6.5 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Eightfold AI Inc.

- 6.4.2 Beamery Inc.

- 6.4.3 Degreed, Inc.

- 6.4.4 Gloat Ltd.

- 6.4.5 Fuel50 Limited

- 6.4.6 TechWolf BV

- 6.4.7 Phenom People, Inc.

- 6.4.8 iMocha Inc.

- 6.4.9 TalentGuard, Inc.

- 6.4.10 Censia, Inc.

- 6.4.11 Workera Corp.

- 6.4.12 Textkernel B.V.

- 6.4.13 365Talents SAS

- 6.4.14 Neobrain SAS

- 6.4.15 Reejig Pty Ltd.

- 6.4.16 ProFinda Limited

- 6.4.17 Draup, Inc.

- 6.4.18 TalentNeuron, LLC

- 6.4.19 Lightcast LLC

- 6.4.20 SkillsDB Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment