|

시장보고서

상품코드

2065559

인재 인텔리전스 플랫폼 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Talent Intelligence Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

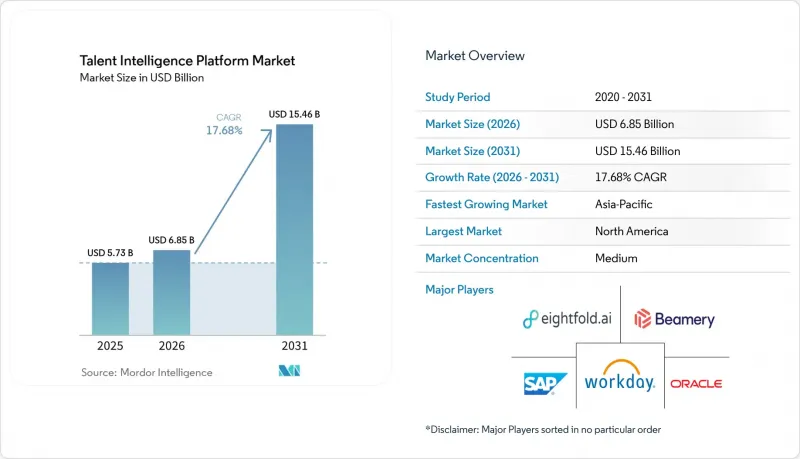

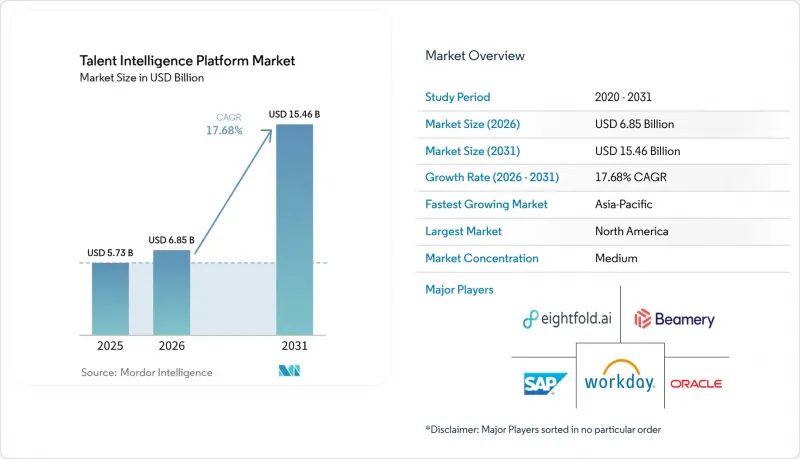

Mordor Intelligence에 의하면, 인재 인텔리전스 플랫폼 시장 규모는 2025년에 57억 3,000만 달러로 평가되었고, 2026년 68억 5,000만 달러로 추정되고, 2031년까지 154억 6,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 17.68%를 나타낼 전망입니다.

본 보고서는 구성 요소별(플랫폼 소프트웨어 및 서비스), 배포 모델별(클라우드 기반, 하이브리드형, 온프레미스형), 조직 규모별(대기업, 중소기업), 최종 사용자 산업 분야별(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 헬스케어 및 생명과학, 소매 및 전자상거래, 제조, 전문 서비스 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 인재 인텔리전스 플랫폼 시장 동향 및 인사이트

기술 기반 인재 계획으로의 전환

인재 인텔리전스 플랫폼 시장이 성장세를 보이고 있는 것은 고용주들이 직책에 기반한 계획에서 기술 기반의 인재 구성 설계로 전환하고 있기 때문입니다. Betterworks가 2026년 4월에 실시한 조사에 따르면, 인사 담당자의 73%가 지난 12개월 동안 기술 데이터 부족이 사내 배치 실패나 전략적 프로그램 지연 등 비즈니스 실패로 직접 이어졌습니다고 응답했습니다. 또한 일부 중견 기업들은 이러한 데이터 부족으로 인해 피할 수 있었던 연간 200만 달러 이상의 비용이 발생했다고 지적하고 있습니다. 또한 Betterworks의 조사에 따르면, AI를 활용한 예측형 인재 계획을 도입한 조직은 고작 16%에 불과한 것으로 나타났으며, 이는 인재 인텔리전스 플랫폼 시장의 구매자 대다수가 여전히 사후 대응형 또는 초기 단계의 모델로 운영되고 있음을 의미합니다. 인재 계획이 이제 사업 전반의 실행 속도에 영향을 미치는 상황에서 기업이 기술 인프라를 장기적인 인사 프로젝트로 다룰 수 없게 되었기 때문에 이러한 격차는 중요한 문제로 대두되고 있습니다. 따라서, 인재 인텔리전스 플랫폼 시장에서는 공급업체가 분석 기능을 독립된 기능으로 판매하는 대신, 스킬 온톨로지, 거버넌스 도구, 계획 워크플로를 동일한 제품에 통합함으로써 시장 전체에 이점을 가져다줍니다.

사내 인재 마켓플레이스 도입 확대

또한, 인재 인텔리전스 플랫폼 시장은 사내 인재 마켓플레이스의 이용 확대에 힘입어 성장하고 있습니다. 특히, 기업들이 외부에서 신규 채용을 시작하기 전에 우선 사내 인력을 재배치하려는 경향이 강해지고 있기 때문입니다. 2026년에는 기업의 채용 역량이 사내 인사 이동으로 전환되고 있으며, 이에 따라 직원을 프로젝트, 단기 업무, 부서 간 역할에 거의 실시간으로 배정할 수 있는 플랫폼에 대한 수요가 높아지고 있습니다. 더 어려운 과제는 소프트웨어 도입이 아니라 관리직의 행동에 있습니다. 왜냐하면 팀 리더는 여전히 인재를 사내에 붙잡아 두는 데 대해 보상을 받는 경우가 많은 반면, 사내에서 인재를 이동시키는 데는 보상을 받지 못하는 경우가 많기 때문입니다. 아데코 그룹의 조사에 따르면, 인력의 유연성을 확보하는 데 필요한 사내 이동 도구를 도입한 기업은 고작 50%에 불과했으며, 자신의 팀 구성원들이 미래의 기술 요건을 이해하고 있다고 확신하는 리더는 45% 미만이었습니다. 이러한 점에서 도입 후의 거부감을 완화하는 ‘도입 현황 분석’, ‘관리자 알림’, ‘업무 흐름 규칙’ 등을 갖춘 제품을 통해, 인재 인텔리전스 플랫폼 시장에는 더욱 성장할 여지가 있습니다. 마켓플레이스의 이용 현황을 재배치 속도나 인재 정착률과 연계하는 벤더는 시스템이 가동된 후에도 지속적인 가치를 발휘할 가능성이 높아집니다.

ATS, HRIS, LMS, CRM 스택 전반에 걸친 통합 과제

인재 인텔리전스 플랫폼 시장의 단기적인 주요 걸림돌은 기존 HR 기술 스택에 내재된 복잡성입니다. Truto의 보고서에 따르면, 인재 채용 담당 리더의 88%가 여러 가지 포인트 솔루션을 이용하고 있으며, 40%는 매일 4개 이상의 플랫폼을 관리하고 있는 것으로 나타났습니다. 그 결과, 핵심이 되는 직원 데이터가 서로 연동되지 않은 시스템에 분산된 채로 남아 있습니다. 이러한 파편화로 인해, 인재 인텔리전스 플랫폼의 도입이 신뢰할 수 있는 매칭, 계획 수립, 인사 이동과 관련된 성과를 창출하는 데까지 걸리는 속도가 제한되고 있습니다. 또한 Truto의 보고서에 따르면, 주요 HRIS 플랫폼 5개에 대해 네이티브 통합을 구축할 경우, 통합된 API 접근 방식에 비해 엔지니어링 시간이 70-80% 더 소요될 뿐만 아니라, 벤더 측의 API 변경으로 인해 출시 후에도 유지보수 작업이 지속적으로 발생합니다. 즉, 도입 시 라이선스 비용을 비교할 때 통합 작업이나 지속적인 데이터 매핑 비용을 고려하지 않고 판단하면, 구매자는 도입에 드는 총 비용을 과소평가하기 쉽습니다. 인재 인텔리전스 플랫폼 시장에서 인증된 커넥터를 갖추고 더 강력한 서비스 수준 보장 및 안정적인 통합 프레임워크를 보유한 벤더는 이러한 ‘숨겨진 비용’을 절감하고 가치 실현까지 걸리는 시간을 단축할 수 있습니다.

부문별 분석

2025년, 플랫폼 소프트웨어는 인재 인텔리전스 플랫폼 시장 규모의 72.41%를 차지했으며, 해당 시장에서 가장 큰 수익 구성 요소로서의 위상을 유지했습니다. 서비스 부문은 2026-2031년 연평균 성장률(CAGR) 18.68%로 확대될 것으로 예상되며, 소프트웨어가 여전히 큰 비중을 차지하고 있음에도 불구하고 서비스 부문이 더 높은 성장률을 보이는 구성 요소가 될 것입니다. 이러한 내역은 소프트웨어 계약이 여전히 지출의 기반을 이루고 있음을 보여 주지만, 인재 인텔리전스 플랫폼 시장의 진정한 과제는 대개 라이선스 계약 체결 이후에 시작됩니다. 아데코 그룹의 조사에 따르면, 직원의 역량을 파악하기 위한 데이터 인사이트에 충분한 투자를 하고 있는 기업은 고작 33%에 불과한 것으로 나타났으며, 이는 도입, 통합 및 분석 지원에 대한 지속적인 수요를 뒷받침하고 있습니다. 그 결과, 구매자들은 서비스를 판매 후의 선택적 추가 기능이 아니라, 생산적인 활용을 실현하기 위해 필수적인 요소로 인식하게 되었습니다.

이러한 동향에 따라 각 벤더사는 핵심 플랫폼을 중심으로 컨설팅, 통합 관리, 매니지드 애널리틱스를 더욱 긴밀하게 패키지화해야 하는 상황에 직면해 있습니다. 고객들은 채용 속도, 사내 인사 이동, 인재 계획의 정확성에 대해 벤더와 책임을 분담하기를 원하고 있기 때문에 성과 기반의 서비스 가격 책정이 더욱 중요해지고 있습니다. SAP가 2026년 상반기에 출시한 SuccessFactors에는 채용 및 경력 관리 워크플로우 전반에 걸쳐 더욱 강력한 역량 거버넌스, 통합된 역량 관리, Joule AI 지원 기능이 추가되었습니다. 이는 벤더가 서비스 수준 거버넌스를 소프트웨어에 직접 통합하려고 하고 있음을 보여줍니다. 인재 인텔리전스 플랫폼 업계에서 확장 가능한 소프트웨어와 체계적인 온보딩 및 변혁 지원을 결합한 제공업체일수록 계약 갱신을 확보하고 고객 가치를 확대할 가능성이 높아집니다. 이러한 경향은 소프트웨어의 기능이 모방되기 쉬워졌습니다고 하더라도, 서비스가 전략적으로 중요한 위치를 유지할 수 있음을 시사합니다.

2025년, 클라우드 기반 솔루션의 도입은 인재 인텔리전스 플랫폼 시장 규모의 68.92%를 차지한 것으로 평가되었으며, 2031년까지 연평균 성장률(CAGR) 22.73%로 확대될 것으로 전망되어, 이로 인해 해당 시장에서 클라우드의 우위가 더욱 공고해지고 있습니다. 멀티테넌트 아키텍처 덕분에 제공 비용이 절감되고, 벤더가 장기간의 로컬 업그레이드 주기를 거치지 않고도 빈번한 모델 업데이트를 추진할 수 있기 때문에 클라우드에 대한 수요는 계속해서 견조한 추세를 보이고 있습니다. 또한, 구매자가 고객 간 벤치마킹이나 새로운 AI 기능에 대한 신속한 접근을 원할 경우, 인재 인텔리전스 플랫폼 시장에서도 클라우드가 선호됩니다. 그렇긴 하지만, 데이터의 소재지 요건, 기밀성이 높은 직원 정보, 혹은 감사상의 필요성 등으로 인해 퍼블릭 클라우드 환경으로의 완전한 전환이 제한되는 업계에서는 하이브리드 구성이 여전히 중요한 역할을 하고 있습니다. 온프레미스 배포는 여전히 규모가 가장 작고 성장 속도도 가장 느린 선택지이지만, 인프라 관련 규제가 엄격한 정부 기관이나 국방 분야에서는 여전히 중요한 위치를 차지하고 있습니다.

클라우드의 성장이 가속화되는 가운데에서도 하이브리드 모델이 여전히 중요하게 여겨지는 이유 중 하나로 개인정보 보호 규제를 꼽을 수 있습니다. Cornell eCommons는 GDPR(EU 개인정보보호규정), 중국의 PIPL, 인도의 DPDP법 등 아시아태평양의 현지화 프레임워크가 기업이 인사 분야에서 AI를 관리하는 방식에 영향을 미치고 있다고 지적하고 있습니다. 특히, 기밀성이 높은 직원 데이터를 현지에서 보관하면서 모델을 일원적으로 관리해야 하는 경우, 이러한 경향은 더욱 두드러집니다. 따라서 인재 인텔리전스 플랫폼 시장에서는 많은 순수 클라우드 소프트웨어 카테고리에 비해 더 복잡한 도입 형태를 볼 수 있습니다. 사용자 경험을 저해하지 않으면서 연합 아키텍처를 지원할 수 있는 공급업체는 규제가 엄격한 고객에게 더 유리한 가격 정책을 제시할 수 있습니다. 인재 인텔리전스 플랫폼 업계에서 도입의 유연성은 단순한 기술적 세부 사항이 아니라, 구매 결정의 핵심 요인으로 자리 잡고 있습니다.

지역별 분석

2025년, 북미는 인재 인텔리전스 플랫폼 시장 점유율의 41.61%를 차지했으며, 해당 시장에서 가장 규모가 큰 지역 거점으로서의 위상을 유지했습니다. 이러한 수요의 대부분은 미국이 주도하고 있는데, 이는 기술 기반의 운영 모델과 기업의 인사 기술에 대한 투자가 다른 많은 국가들보다 더 빨리 규모를 확대했기 때문입니다. 캐나다 역시, 특히 금융 서비스 및 공공 부문의 현대화 프로그램에서 진전을 보이고 있으며, 이 분야에서 인재 계획과 역량 가시화가 보다 광범위한 디지털 전환을 뒷받침하고 있습니다. 멕시코에서는 아직 도입 초기 단계이지만, 다국적 제조 기업들은 국경을 초월한 인재 계획 및 직무 표준화를 지원하기 위해 기술 추적 도구를 활용하기 시작했습니다. 남미 시장은 여전히 규모가 작지만, 브라질과 아르헨티나에서는 전문 서비스 및 BFSI(은행 및 금융 및 보험) 기업들 수요가 나타나고 있으며, 맨파워그룹의 2026년 2분기 전망에 따르면 해당 지역 전체에서 기술 서비스 분야의 채용 의향이 지속될 것으로 지적되고 있습니다.

유럽은 인재 인텔리전스 플랫폼 시장에서 두 번째로 큰 규모를 자랑하는 지역 블록을 형성하고 있으며, 독일, 영국, 프랑스가 도입을 주도하고 있습니다. 독일의 채용 컨설팅 시장은 2024년에 3.8% 감소한 28억 2,000만 유로(30억 7,000만 달러)를 기록할 것으로 보이며, 2025년에는 1.2% 더 감소한 27억 8,000만 유로(31억 달러)로 감소할 것으로 예상되며, 이는 사내용 인텔리전스 도구로의 전환을 뒷받침하는 것입니다. 또한, 유럽에서는 규정 준수 측면에서 명확한 수요가 있습니다. EU AI법에 따라 고용주는 2026년 8월 법 시행 전후로, 고위험 고용용 AI에 대한 관리 조치를 제시할 수 있는 공급업체를 선택해야 하기 때문입니다. 프랑스에서는 국내 규모의 주요 기업들도 두각을 나타내고 있으며, 365Talents는 소시에테 제네랄, SNCF, 베올리아를 고객사로 두고 있으며, 45개 이상의 언어를 지원하며 100만 명 이상의 사용자를 보유하고 있다고 보고하고 있습니다. 한편, 러시아는 제재와 이에 따른 기술 접근 제한의 영향을 계속 받고 있습니다.

아시아태평양은 2026-2031년 연평균 성장률(CAGR) 22.41%를 기록하며 성장할 것으로 예상되며, 인재 인텔리전스 플랫폼 시장에서 가장 두드러진 성장세를 보일 것으로 전망됩니다. 이 지역의 확대는 인도, 싱가포르, 일본, 한국, 호주에서 노동력의 디지털화가 가속화되고 있기 때문이지만, 일부 시장에서는 데이터 현지화 규제로 인해 현지에서의 도입이 더욱 요구되고 있습니다. 싱가포르는 시범 운영의 주요 거점으로 자리 잡고 있으며, 아시아태평양공급업체들이 다국어 평가의 품질과 현지 노동 시장의 깊이 면에서 전 세계 기업들과 경쟁하고 있습니다. 일본은 인구 동향의 변화와 정년 연령 상향 조정으로 인해 노동력 측면에서 심각한 압박에 직면해 있으며, 대기업의 경우 인력 재배치 및 역량을 기반으로 한 인재 유동화 도구의 도입이 그 어느 때보다 시급한 과제가 되고 있습니다. 중동에서는 ‘사우디 비전 2030’이나 UAE의 디지털화 프로그램을 통해 성장세가 가속화되고 있는 반면, 아프리카는 여전히 초기 단계에 머물러 있으며, 남아프리카공화국과 나이지리아가 기업 차원의 사업 전개에 있어 주요 진출 시장으로 부상하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the talent intelligence platform market size was valued at USD 5.73 billion in 2025 and estimated to grow from USD 6.85 billion in 2026 to reach USD 15.46 billion by 2031, at a CAGR of 17.68% during the forecast period (2026-2031).

This report is Segmented by Component (Platform Software, and Services), Deployment Model (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and SMEs), End-User Industry (IT and Telecom, BFSI, Healthcare and Life Sciences, Retail and E-Commerce, Manufacturing, Professional Services, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Talent Intelligence Platform Market Trends and Insights

Shift To Skills-Based Workforce Planning

The talent intelligence platform market is gaining momentum because employers are moving away from job-title planning and toward skills-based workforce design. Betterworks found in April 2026 that 73% of HR leaders said skills data gaps had contributed directly to business failures in the prior 12 months, including missed internal placements and delayed strategic programs, and some mid-market firms linked those gaps to avoidable annual costs of USD 2 million or more. Betterworks also showed that only 16% of organizations had predictive, AI-driven workforce planning in place, which means most buyers in the talent intelligence platform market are still operating from reactive or early-stage models. This gap matters because firms can no longer treat skills infrastructure as a long-term HR project when workforce planning now affects execution speed across the business. The talent intelligence platform market, therefore, benefits when vendors combine skills ontologies, governance tools, and planning workflows in the same product rather than selling analytics as an isolated feature.

Expansion of Internal Talent Marketplace Adoption

The talent intelligence platform market is also supported by wider use of internal talent marketplaces, especially as companies try to redeploy workers before opening new external searches. Enterprise recruiting capacity is shifting toward internal mobility in 2026, and that increases demand for platforms that can match employees to projects, gigs, and lateral roles in near real time. The harder issue is not software installation but manager behavior, because team leaders are still often rewarded for holding talent rather than releasing it across the business. Adecco Group found that only 50% of companies had the internal mobility tools needed for workforce agility, and fewer than 45% of leaders believed their teams understood future skill requirements. That leaves room for the talent intelligence platform market to grow through products that include adoption analytics, manager prompts, and workflow rules that reduce resistance after deployment. Vendors that link marketplace usage to redeployment speed and talent retention are more likely to show durable value once the system goes live.

Integration Debt Across ATS, HRIS, LMS, And CRM Stacks

The main short-term drag on the talent intelligence platform market is the complexity built into legacy HR technology stacks. Truto reported that 88% of talent acquisition leaders used multiple point solutions, and 40% managed 4 or more platforms each day, which leaves core workforce data scattered across disconnected systems. That fragmentation limits how quickly a talent intelligence platform market deployment can produce reliable matching, planning, and mobility outputs. Truto also reported that building native integrations to even 5 large HRIS platforms can consume 70-80% more engineering time than a unified API approach, while vendor API changes keep adding maintenance work after launch. This means buyers often underestimate the full cost of deployment when they compare license fees without accounting for integration work and ongoing data mapping. In the talent intelligence platform market, vendors with certified connectors, stronger service-level commitments, and stable integration frameworks can reduce this hidden tax and shorten time to value.

Other drivers and restraints analyzed in the detailed report include:

- Enterprise Adoption of Generative AI And Agentic HR

- Need For Unified Internal And External Talent Data

- Algorithmic Bias, Privacy, and Employment Law Exposure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platform software accounted for 72.41% of the talent intelligence platform market size in 2025, which kept it as the largest revenue component in the talent intelligence platform market. Services are projected to expand at an 18.68% CAGR from 2026 to 2031, which makes them the faster-growing component even though software remains the larger base. This split shows that software contracts still anchor spending, but the real challenge in the talent intelligence platform market often begins after the license is signed. Adecco Group found that only 33% of companies invested adequately in data insights to understand workforce skills, which supports ongoing demand for implementation, integration, and analytics support. As a result, buyers increasingly view services as essential to reaching productive use rather than as optional post-sale add-ons.

That dynamic is pushing vendors to package consulting, integration management, and managed analytics more tightly around the core platform. Outcome-based services pricing is gaining relevance because clients want vendors to share accountability for hiring speed, internal mobility, and workforce planning accuracy. SAP's 1H 2026 SuccessFactors release added stronger skills governance, centralized skills management, and Joule AI support across hiring and career workflows, which shows how vendors are trying to embed services-grade governance directly into software. In the talent intelligence platform industry, the providers that combine scalable software with disciplined onboarding and change support are more likely to protect renewals and expand account value. The same pattern suggests that services can remain strategically important even if software features become easier to copy.

Cloud-based deployment captured 68.92% of the talent intelligence platform market size in 2025 and is projected to expand at a 22.73% CAGR through 2031, which reinforces its lead in the talent intelligence platform market. Cloud demand remains strong because multi-tenant architecture lowers delivery costs and allows vendors to push frequent model updates without long local upgrade cycles. The talent intelligence platform market also favors cloud when buyers want benchmarking across customers and faster access to new AI functions. Even so, hybrid deployment keeps a durable role in industries where data residency, classified workforce information, or audit needs limit full movement into public cloud environments. On-premises deployment remains the smallest and slowest-growing option, but it still matters in sovereign government and defense settings where infrastructure rules are strict.

Privacy rules are one reason hybrid models remain relevant even as cloud grows faster. Cornell eCommons noted that GDPR and Asia-Pacific localization frameworks such as China's PIPL and India's DPDP Act are shaping how companies manage AI in HR, especially when sensitive employee data must stay local while models are governed centrally. That gives the talent intelligence platform market a more complex deployment profile than many pure cloud software categories. Vendors that can support federated architectures without breaking the user experience can command better pricing in regulated accounts. In the talent intelligence platform industry, deployment flexibility is becoming a core buying factor rather than a technical detail.

Geography Analysis

North America held 41.61% of the talent intelligence platform market share in 2025, which kept it as the largest regional base in the talent intelligence platform market. The United States drives most of that demand because skills-based operating models and enterprise HR technology investment reached scale earlier there than in most other countries. Canada is also moving forward, especially in financial services and public-sector modernization programs, where workforce planning and skills visibility support broader digital transformation. Mexico remains earlier in adoption, but multinational manufacturers are starting to use skills-tracking tools to support cross-border workforce planning and role standardization. South America is still smaller, yet Brazil and Argentina are showing demand from professional services and BFSI firms, and ManpowerGroup's Q2 2026 outlook pointed to continued hiring intent in technology and services across the region.

Europe forms the second-largest regional block in the talent intelligence platform market, with Germany, the United Kingdom, and France leading adoption. Germany's recruitment consulting market fell 3.8% to EUR 2.82 billion (USD 3.07 billion) in 2024, and a further 1.2% decline to EUR 2.78 billion (USD 3.1 billion) was projected for 2025, which supports a shift toward in-house intelligence tooling. Europe also has a distinct compliance pull, because the EU AI Act is pushing employers toward vendors that can show high-risk employment AI controls before and after the August 2026 application point. France is also producing local scale players, and 365Talents reported more than 1 million users across Societe Generale, SNCF, and Veolia in 45+ languages, while Russia remains constrained by sanctions and related limits on technology access.

Asia-Pacific is projected to grow at a 22.41% CAGR from 2026 to 2031, making it the fastest-growing region in the talent intelligence platform market. The region is expanding because workforce digitization is accelerating in India, Singapore, Japan, South Korea, and Australia, even though data localization rules are forcing more local deployment choices in some markets. Singapore has become a strong hub for pilots, where APAC-native vendors compete with global firms on multilingual assessment quality and local labor market depth. Japan faces sharp workforce pressure from demographic change and retirement-age extension, which makes redeployment and skills-based mobility tools more urgent for large employers. The Middle East is gaining traction through Saudi Vision 2030 and UAE digitization programs, while Africa remains at an earlier stage with South Africa and Nigeria acting as the main entry markets for enterprise-wide rollouts.

- SAP SE

- Workday, Inc.

- Oracle Corporation

- Eightfold AI Inc.

- Beamery Inc.

- LinkedIn Corporation

- Gloat Inc.

- Phenom People, Inc.

- ZipStorm, Inc.

- Visier Inc.

- TechWolf BV

- Lightcast, LLC

- iCIMS, Inc.

- Cornerstone OnDemand, Inc.

- ADP, Inc.

- International Business Machines Corporation

- ServiceNow, Inc.

- SmartRecruiters, Inc.

- Degreed, Inc.

- HireVue, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Shift to Skills-Based Workforce Planning

- 4.3.2 Expansion of Internal Talent Marketplace Adoption

- 4.3.3 Enterprise Adoption of Generative AI and Agentic HR

- 4.3.4 Need for Unified Internal and External Talent Data

- 4.3.5 AI Auditability and Explainability Requirements

- 4.3.6 Task-Level Work Redesign for Human-AI Collaboration

- 4.4 Market Restraints

- 4.4.1 Integration Debt Across ATS, HRIS, LMS, and CRM Stacks

- 4.4.2 Algorithmic Bias, Privacy, and Employment Law Exposure

- 4.4.3 Skills Taxonomy Drift and Weak Data Governance

- 4.4.4 Low Utilization After Go-Live and Change-Management Failure

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Platform Software

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 Cloud-based

- 5.2.2 Hybrid

- 5.2.3 On-premises

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-User Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Retail and E-commerce

- 5.4.5 Manufacturing

- 5.4.6 Professional Services

- 5.4.7 Public Sector and Education

- 5.4.8 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Netherlands

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 Asia

- 5.5.4.1.1 China

- 5.5.4.1.2 India

- 5.5.4.1.3 Japan

- 5.5.4.1.4 South Korea

- 5.5.4.1.5 Singapore

- 5.5.4.1.6 Australia

- 5.5.4.1.7 New Zealand

- 5.5.4.1.8 Rest of Asia-Pacific

- 5.5.4.1 Asia

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Israel

- 5.5.5.4 Turkey

- 5.5.5.5 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Kenya

- 5.5.6.4 Egypt

- 5.5.6.5 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Workday, Inc.

- 6.4.3 Oracle Corporation

- 6.4.4 Eightfold AI Inc.

- 6.4.5 Beamery Inc.

- 6.4.6 LinkedIn Corporation

- 6.4.7 Gloat Inc.

- 6.4.8 Phenom People, Inc.

- 6.4.9 ZipStorm, Inc.

- 6.4.10 Visier Inc.

- 6.4.11 TechWolf BV

- 6.4.12 Lightcast, LLC

- 6.4.13 iCIMS, Inc.

- 6.4.14 Cornerstone OnDemand, Inc.

- 6.4.15 ADP, Inc.

- 6.4.16 International Business Machines Corporation

- 6.4.17 ServiceNow, Inc.

- 6.4.18 SmartRecruiters, Inc.

- 6.4.19 Degreed, Inc.

- 6.4.20 HireVue, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment