|

시장보고서

상품코드

2063915

아시아태평양의 학습 관리 시스템(LMS) 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Asia-Pacific Learning Management Systems (LMS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

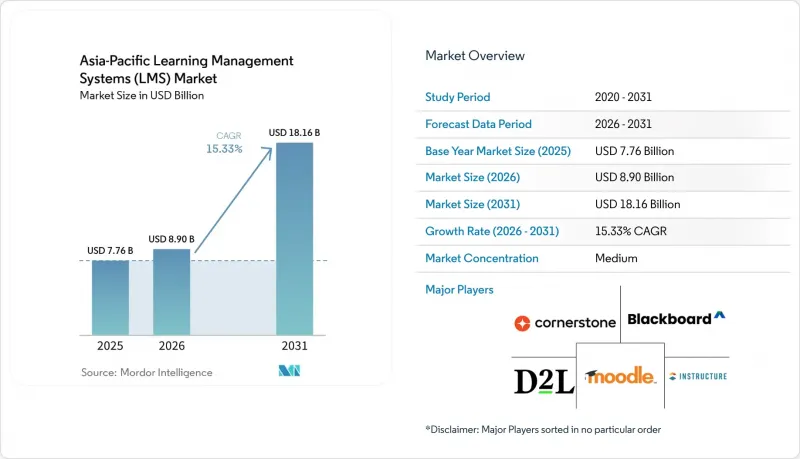

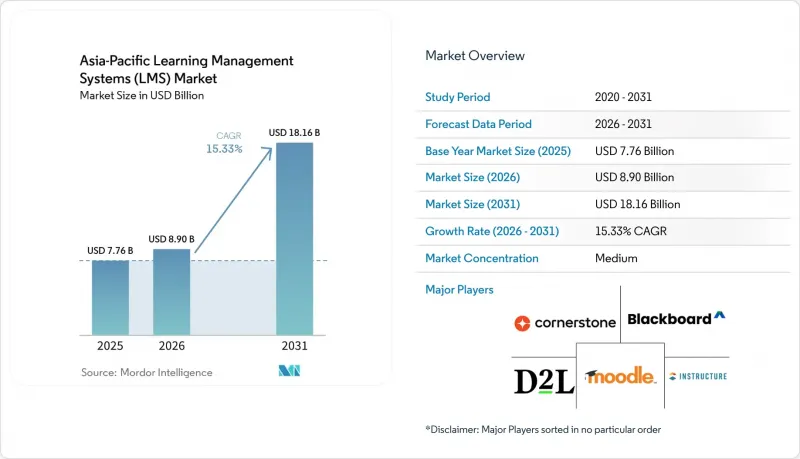

Mordor Intelligence에 의하면, 아시아태평양 학습 관리 시스템(LMS) 시장 규모는 2025년 77억 6,000만 달러에서 2026년에는 89억 달러로 확대되어 2026년부터 2031년까지 CAGR 15.33%로 성장을 지속하여, 2031년까지 181억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소(솔루션 및 서비스), 도입 형태(클라우드, On-Premise, 하이브리드), 학습 유형(학술 학습 등), 기업 규모(대기업, 중소기업), 업종(정보기술·통신 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

아시아태평양 학습 관리 시스템(LMS) 시장 동향 및 인사이트

기업들의 기술 기반 및 목표 지향적 교육으로의 전환

이 지역의 기업들은 고정된 역할 기반의 과정 라이브러리가 아닌, 기술 및 역량 요구 사항에 맞추어 학습 예산을 재편하고 있으며, 이러한 변화는 구매자들이 아시아태평양의 학습 관리 시스템 시장을 평가하는 방식을 바꿔가고 있습니다. 조달 활동은 컨텐츠, 스킬 그래프, 측정 가능한 역량 성과를 단일 시스템 내에서 연동할 수 있는 플랫폼으로 전환되고 있습니다. 세계경제포럼은 2025년 노동력 전망 보고서에서 기술 기반의 인재 배치를 노동력 관련 최우선 과제 3가지 중 하나로 꼽으며, 역량 매핑 및 기술 인텔리전스 기능을 갖춘 플랫폼에 대한 수요가 증가하고 있음을 강조했습니다. OCBC는 900명의 자산 관리 자문가를 대상으로 체계화된 LMS 과정을 통해 생성형 AI 도구 교육을 실시했을 때, 이 접근 방식의 상업적 효과를 입증했습니다. 그 결과, 3개월 이내에 수익이 50% 증가했으며, 교육을 받은 직원의 주당 고객 상담 건수는 교육을 받지 않은 동료에 비해 2배로 늘어났습니다. 이로 인해 컨텐츠의 충실도에 주로 의존하는 제공업체보다, 기술이나 온톨로지 기능을 기본적으로 갖춘 벤더가 더 매력적으로 다가오고 있습니다. Cornerstone OnDemand의 SkyHive 인수는 해당 기업의 광범위한 학습 및 인재 관리 플랫폼에 스킬 인텔리전스 기능을 추가함으로써 이러한 방향성을 한층 더 강화했습니다.

기업 내 재교육 및 규정 준수 교육 수요 증가

아시아태평양의 학습 관리 시스템(LMS) 시장도, 특히 규제 대상 부문에서 규정 준수 및 직원 재교육 의무의 중요성이 커지고 있는 데 힘입어 호조를 보이고 있습니다. 기업들은 분산된 사업 거점 전반에 걸쳐 감사 기록, 업데이트 내역 및 표준화된 교육 이수 데이터를 필요로 하기 때문에 규정 준수 교육은 더 이상 단순한 일상적인 관리 업무로 취급되지 않습니다. 홍콩은행협회는 2025년 8월, 자금세탁 방지 및 테러 자금 조달 방지에 관한 ‘강화된 역량 프레임워크’를 개정하고, 실무자들에게 매년 10-12시간의 지속적 전문 역량 개발(CPD) 이수를 의무화했습니다. 홍콩의 ‘중요 인프라 보호 조례’가 2026년 1월 1일부터 시행됨에 따라, BFSI(은행 및 금융 및 보험), 에너지, 운송 등 각 업계에서 사이버 보안 교육 의무화 요건이 확대되면서 기업용 LMS 도입의 필요성이 더욱 커졌습니다. 여러 국가에 공장 네트워크를 보유한 제조 그룹 역시 안전 교육 및 인증을 대규모로 관리하기 위해 통합 플랫폼을 활용하고 있으며, 이것이 2025년 지역별 매출의 34.13%를 BFSI가 차지한 이유 중 하나입니다. 한편, 수요는 다른 규제 대상 업계로도 확대되고 있습니다.

아시아·태평양 신흥 시장의 디지털 인프라 불균형

인터넷 접속 환경의 불균형은 아시아태평양의 학습 관리 시스템 시장에서 일부 저소득 국가 및 신흥 시장에서 여전히 실질적인 제약 요인으로 작용하고 있습니다. 인도네시아, 캄보디아, 미얀마의 농촌 지역 및 베트남의 일부 지역에서는 광대역 및 모바일 네트워크의 불안정성이 지속되고 있으며, 이로 인해 비동기식 학습의 수료가 저해되고 기업 구매자에게 제공되는 측정 가능한 성과가 약화되고 있습니다. 학습 이수 현황이나 성과에 관한 데이터의 신뢰성이 떨어지면, 효과를 입증해야 하는 고객 입장에서는 계약 갱신 여부를 결정하기가 어려워집니다. 이로 인해 싱가포르나 호주에서 효과적인 가격 책정 및 제공 모델이, 통신 환경이 열악한 지역에는 그대로 적용할 수 없습니다는 지역 내의 ‘양극화’ 구조가 발생하고 있습니다. 그 결과, 순수한 클라우드 네이티브 설계는 이러한 환경에서 충분한 성능을 발휘할 수 없기 때문에 오프라인 우선 또는 저대역폭 이용 사례에 대응하는 벤더에게 상업적 우위가 생기고 있습니다. 아시아 재단의 ‘Go Digital ASEAN’ 프로그램은 2020년 이후 40만 명 이상을 양성해 왔으며, 참가자의 90%가 디지털 도구에 대한 자신감이 높아졌다고 보고하고 있습니다. 이는 인프라의 제약으로 인해 LMS를 완전히 도입하기에는 아직 어려운 지역이라 하더라도, 학습자들 수요가 여전히 존재하고 있음을 보여줍니다.

부문별 분석

2025년 아시아태평양의 학습 관리 시스템(LMS) 시장에서 솔루션이 80.19%를 차지했습니다. 이는 해당 지역에서 서비스 주도형 도입보다 플랫폼 주도형 조달이 계속해서 선호되고 있음을 뒷받침합니다. 기업 및 교육 기관의 구매 담당자들은 컨텐츠 관리, 학습자 추적, 분석, 관리 워크플로우를 단일 환경에서 지원하는 핵심 소프트웨어를 여전히 우선시하고 있습니다. 이러한 경향은 지역 벤더 기반의 성숙도도 반영하고 있습니다. 이는 플러그 앤 플레이 방식의 클라우드 플랫폼 덕분에, 과거에는 서비스 통합형 도입이 일반적이었던 대규모 초기 맞춤 설정이 더 이상 필요하지 않게 되었기 때문입니다. 실무적으로 볼 때, 많은 조직이 구매 주기의 초기 단계에서 바로 가동 가능한 플랫폼을 기대하게 되었으며, 그 결과 계약의 핵심이 소프트웨어 계층에 맞추어지고 있습니다. 아시아태평양의 학습 관리 시스템 시장에서는 구매자가 장기적이고 고비용의 도입 프로젝트에 의존하지 않고도 명확한 플랫폼 기능을 제공할 수 있는 공급업체가 계속해서 높은 평가를 받고 있습니다.

동시에, 이러한 플랫폼을 둘러싼 운영 환경이 복잡해짐에 따라 서비스의 중요성은 점점 더 커지고 있습니다. 설정, 통합, 컨텐츠 현지화 및 지속적인 관리에 대한 수요가 증가함에 따라, 서비스 시장은 2031년까지 연평균 성장률(CAGR) 16.24%로 확대될 것으로 전망됩니다. 규제가 엄격한 업계의 많은 구매자들은 소프트웨어 구독뿐만 아니라, 규정 준수 관련 컨텐츠 업데이트, 워크플로우 조정, 그리고 내부 보고 대응도 필요로 하고 있습니다. 다양한 인재 구성으로 인해 다국어 서비스를 제공해야 하는 경우, 특히 사내 학습 팀의 규모가 작은 경우에는 고객이 외부 지원 서비스를 이용하게 됩니다. 장기적인 변화로는 프로젝트형 업무에서 보다 광범위한 다년 계약 형태의 플랫폼 계약 내에 포함된 지속적인 매니지드 서비스로의 전환이 진행되고 있습니다. 이 모델은 구매자에게는 전환 비용을 높이는 동시에, 공급업체에게는 보다 안정적이고 지속적인 수익을 창출합니다. 2024년 5월 Cornerstone OnDemand가 SkyHive를 인수한 사례는 주요 공급업체들이 소프트웨어 제공에서 기술 인텔리전스 및 광범위한 인재 분석으로 사업을 확장하고 있음을 보여줍니다. 따라서 아시아태평양의 학습 관리 시스템(LMS) 업계에서는 서비스가 단순한 지원 수단에서 고객 유지를 강화하는 전략적 수익원으로 진화하고 있습니다. 이러한 변화가 중요하게 여겨지는 이유는 고객들이 설계, 도입, 분석, 규정 준수 관리까지 모두 지원할 수 있는 단일 공급업체를 찾는 경향이 강해지고 있기 때문입니다.

2025년 기준으로 아시아태평양의 학습 관리 시스템(LMS) 시장의 68.62%를 클라우드가 차지하고 있으며, 2031년까지 연평균 성장률(CAGR) 17.42%로 가장 빠른 성장이 예상됩니다. 이러한 조합은 클라우드가 현재의 표준일 뿐만 아니라, 가장 폭넓은 신규 구매자들을 끌어들이는 형태임을 보여줍니다. 그 매력은 예측 가능한 구독 비용, 신속한 업그레이드, 그리고 내부 인프라에 대한 의존도가 낮다는 점에 있습니다. 이러한 장점은 막대한 초기 투자 없이 엔터프라이즈급 기능을 필요로 하는 중소기업, 중규모 기관, 정부 기관에 있어 가장 중요합니다. 따라서 아시아태평양의 학습 관리 시스템 시장은 특히 조직이 신속한 도입과 지점 간 손쉬운 확장을 원할 경우, 신규 도입 시 기본 아키텍처로 클라우드로 전환되고 있습니다.

2026년 4월, Instructure가 Canvas를 Core, Plus, Next의 3가지 요금제로 간소화한 조치는 공급업체가 더 폭넓은 고객층에서의 도입을 가속화하기 위해 가격 책정 및 패키지 구성에 따른 장벽을 낮추고 있음을 보여주는 사례입니다. On-Premise형 플랫폼은 중국과 일본, 특히 정부 기관이나 규제가 엄격한 금융 업계에서 여전히 그 중요성을 유지하고 있습니다. 이러한 분야에서는 데이터 주권에 관한 규정에 따라 현지 호스팅이 계속해서 권장되고 있기 때문입니다. 또한, 클라우드를 통한 컨텐츠 배포를 원하면서도 기밀성이 높은 직원 기록에 대해서는 On-Premise 관리가 필요한 대규모 조직의 경우, 하이브리드 방식이 실용적인 가교 수단으로 자리 잡고 있습니다. 이러한 중간적인 접근 방식은 레거시 시스템의 이질성이나 국가별 규정 준수 요건을 안고 있는 기업에 유용합니다. 또한, 고객에게 별도의 라이선스나 관리의 분할을 강요하지 않으면서도 분할 아키텍처를 지원할 수 있는 벤더에게는 규모는 작지만 의미 있는 기회를 창출하고 있습니다. 아시아태평양의 학습 관리 시스템(LMS) 업계에서 경쟁 우위는 더 이상 기본적인 호스팅 옵션보다는 공급업체가 규정 준수, 가격 투명성, 시스템 유연성을 얼마나 적절하게 처리할 수 있는지에 달려 있습니다. 하이브리드 아키텍처에는 높은 수준의 기술력과 강력한 지원 체계가 요구되기 때문에 소규모 벤더들은 종종 어려움을 겪게 됩니다. 그 결과, 클라우드 네이티브 벤더들이 중소기업 및 중견 기업을 대상으로 신규 고객을 확보하고 있는 반면, On-Premise 분야에서 실적을 쌓아온 기존 벤더들은 공공 부문 및 금융 분야의 대규모 계약을 계속 유지하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the asia-Pacific learning management systems (LMS) market size is expected to increase from USD 7.76 billion in 2025 to USD 8.90 billion in 2026 and reach USD 18.16 billion by 2031, at a CAGR of 15.33% over 2026-2031.

This report is Segmented by Component (Solutions, and Services), Deployment (Cloud, On-Premises, and Hybrid), Learning Type (Academic Learning, and More), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), Industry Vertical (Information Technology and Telecommunications, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Learning Management Systems (LMS) Market Trends and Insights

Enterprise Shift Toward Skills-Based and Objective-Driven Training

Enterprises across the region are reorganizing learning budgets around skills and competency needs rather than fixed, role-based course libraries, and that shift is changing how buyers evaluate the Asia Pacific learning management systems market. Procurement is moving toward platforms that can connect content, skills graphs, and measurable capability outcomes within one system. The World Economic Forum identified skills-based talent deployment as a top-three workforce priority in its 2025 workforce outlook, underscoring the growing demand for platforms with competency-mapping and skills-intelligence features. OCBC demonstrated the commercial impact of this approach when 900 wealth advisors were trained in generative AI tools through structured LMS pathways, resulting in a 50% revenue uplift within 3 months and a doubling of weekly client appointments for trained staff compared with untrained peers. This is making vendors with native skills and ontology capabilities more attractive than providers that rely mainly on content depth. Cornerstone OnDemand's acquisition of SkyHive reinforced that direction by adding skills intelligence to its broader learning and talent stack.

Rising Corporate Reskilling and Compliance Training Demand

The Asia Pacific learning management systems market is also benefiting from the growing weight of compliance and workforce reskilling obligations, especially in regulated sectors. Compliance training is no longer treated as a routine administrative task, as firms need audit trails, renewal records, and standardized learning-completion data across dispersed operations. The Hong Kong Institute of Bankers updated its Enhanced Competency Framework for Anti-Money Laundering and Counter-Terrorist Financing in August 2025, requiring practitioners to complete 10-12 continuing professional development hours each year. Hong Kong's Protection of Critical Infrastructures Ordinance took effect on January 1, 2026, and expanded mandatory cybersecurity training requirements across BFSI, energy, and transport, strengthening the case for enterprise LMS deployment. Manufacturing groups with multi-country factory networks are also using unified platforms to manage safety training and certification at scale, which helps explain why BFSI accounted for 34.13% of 2025 regional revenue, while demand is expanding into other regulated verticals.

Patchy Digital Infrastructure Across Emerging Asia-Pacific Markets

Patchy connectivity remains a practical constraint for the Asia Pacific learning management systems market in several lower-income and frontier locations. Rural Indonesia, Cambodia, Myanmar, and parts of Vietnam continue to face broadband and mobile-network instability, which disrupts asynchronous learning completion and weakens measurable outcomes for enterprise buyers. When learning completion and performance data become unreliable, renewal decisions also become harder for clients who need proof of effectiveness. This creates a 2-speed regional structure in which pricing and delivery models that work in Singapore or Australia do not transfer cleanly to lower-connectivity environments. The result is a commercial advantage for vendors that support offline-first or low-bandwidth use cases, because purely cloud-native designs do not perform as well in these settings. The Asia Foundation's Go Digital ASEAN program has trained more than 400,000 individuals since 2020, and 90% of participants reported higher confidence in digital tools, indicating that learner demand persists even where infrastructure still limits full LMS deployment.

Other drivers and restraints analyzed in the detailed report include:

- Accelerating Cloud and Mobile-First Learning Adoption

- Expansion of Hybrid and Distance Learning Across Higher Education

- Data Localization and Cross-Border Transfer Rules Complicating Cloud Deployments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions accounted for 80.19% of the Asia-Pacific learning management systems (LMS) market in 2025, underscoring the region's continued preference for platform-led procurement over service-led implementations. Buyers across enterprises and institutions are still prioritizing core software that supports content management, learner tracking, analytics, and administrative workflows in a single environment. This pattern also reflects the maturity of the regional vendor base, because plug-and-play cloud platforms have reduced the heavy upfront customization that once made service-intensive deployments more common. In practical terms, many organizations now expect a working platform much earlier in the buying cycle, which keeps the software layer at the center of the contract. The Asia Pacific learning management systems market continues to reward vendors that can offer clear platform functionality without requiring buyers to depend on lengthy, expensive implementation projects.

At the same time, services are becoming increasingly important as the operating environment around these platforms becomes more complex. Services are projected to expand at a 16.24% CAGR through 2031, reflecting rising demand for configuration, integration, content localization, and ongoing administration. Many buyers in regulated sectors need more than a software subscription, as they also require compliance content updates, workflow tuning, and support for internal reporting. Multi-language delivery across diverse workforces also pushes clients toward external support, especially when internal learning teams are small. The longer-term shift is from project work toward recurring managed services that sit inside broader multi-year platform contracts. That model raises switching costs for buyers and creates steadier recurring revenue for vendors. Cornerstone OnDemand's May 2024 acquisition of SkyHive showed how leading providers are expanding from software delivery into skills intelligence and broader workforce analytics. The Asia Pacific learning management systems industry is therefore seeing services evolve from a supporting layer into a strategic revenue stream that strengthens retention. This shift matters because clients increasingly want a single provider that can support design, deployment, analytics, and compliance management.

Cloud accounted for 68.62% of the Asia-Pacific learning management systems (LMS) market in 2025 and is projected to grow at the fastest pace, with a 17.42% CAGR through 2031. That combination shows that cloud is not only the current standard, but also the format attracting the widest set of new buyers. The appeal comes from predictable subscription costs, faster upgrades, and lower internal infrastructure needs. These benefits matter most to SMEs, mid-sized institutions, and government agencies that need enterprise-grade functionality without a capital-intensive implementation. The Asia Pacific learning management systems market is therefore moving toward cloud as the default architecture for most new deployments, especially where organizations want quick rollout and easier scaling across locations.

Instructure's April 2026 move to simplify Canvas into Core, Plus, and Next illustrated how vendors are reducing pricing and packaging friction to speed adoption across a broader customer base. On-premises platforms remain relevant in China and Japan, especially in government and regulated finance, where data sovereignty rules continue to support local hosting. Hybrid deployment is also becoming a practical bridge for large organizations that want cloud content delivery but need on-premises control for sensitive employee records. That middle path is useful for enterprises with uneven legacy systems and country-specific compliance rules. It also creates a narrow but meaningful opportunity for vendors that can support split architecture without forcing customers into separate licenses or fragmented administration. In this part of the Asia Pacific learning management systems industry, competitive advantage is now tied less to basic hosting choice and more to how well vendors handle compliance, pricing clarity, and system flexibility. Smaller vendors often struggle here because hybrid architecture requires deeper technical capability and stronger support capacity. As a result, cloud-native vendors are winning new SME and mid-market accounts, while incumbents with on-premises history continue to defend large public-sector and financial contracts.

List of Companies Covered in this Report:

- Moodle Pty Ltd.

- Blackboard LLC

- Cornerstone OnDemand, Inc.

- Instructure Holdings, Inc.

- D2L Inc.

- Docebo Inc.

- Absorb Software Inc.

- LearnUpon Limited

- CYPHER Learning, Inc.

- itslearning AS

- Epignosis LLC

- 360LEARNING SA

- Litmos US, L.P.

- Open LMS LLC

- Schoox, LLC

- SkyPrep Inc.

- Tovuti, Inc.

- Kallidus Limited

- eloomi A/S

- iSpring Solutions, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Enterprise Shift Toward Skills-Based and Objective-Driven Training

- 4.2.2 Accelerating Cloud and Mobile-First Learning Adoption

- 4.2.3 Rising Corporate Reskilling and Compliance Training Demand

- 4.2.4 Expansion of Hybrid and Distance Learning Across Higher Education

- 4.2.5 National Micro-Credential Frameworks and Digital Badge Infrastructure

- 4.2.6 Skills-Based Internal Mobility Programs Requiring Credential-Mapped Learning Paths

- 4.3 Market Restraints

- 4.3.1 Patchy Digital Infrastructure Across Emerging Asia-Pacific Markets

- 4.3.2 Difficulty Proving Training ROI Across Disparate HR and Learning Systems

- 4.3.3 Data Localization and Cross-Border Transfer Rules Complicating Cloud Deployments

- 4.3.4 Multilingual and Pedagogical Localization Burdens Across High-Diversity Markets

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud

- 5.2.2 On-premises

- 5.2.3 Hybrid

- 5.3 By Learning Type

- 5.3.1 Academic Learning

- 5.3.2 Corporate Training

- 5.3.3 Government / Public Training

- 5.3.4 Skill Development / Certification

- 5.4 By End User Vertical

- 5.4.1 Information Technology (IT) and Telecommunications

- 5.4.2 Banking, Financial Services, and Insurance (BFSI)

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Manufacturing and Industrial Operations

- 5.4.5 Retail and E-commerce

- 5.4.6 Education

- 5.4.7 Government and Public Sector

- 5.4.8 Energy and Utilities

- 5.4.9 Media and Entertainment

- 5.5 By End User Enterprise Size

- 5.5.1 Large Enterprises

- 5.5.2 Small and Medium-sized Enterprises

- 5.6 By Geography

- 5.6.1 China

- 5.6.2 India

- 5.6.3 Japan

- 5.6.4 South Korea

- 5.6.5 Singapore

- 5.6.6 Malaysia

- 5.6.7 Thailand

- 5.6.8 Australia

- 5.6.9 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Moodle Pty Ltd.

- 6.4.2 Blackboard LLC

- 6.4.3 Cornerstone OnDemand, Inc.

- 6.4.4 Instructure Holdings, Inc.

- 6.4.5 D2L Inc.

- 6.4.6 Docebo Inc.

- 6.4.7 Absorb Software Inc.

- 6.4.8 LearnUpon Limited

- 6.4.9 CYPHER Learning, Inc.

- 6.4.10 itslearning AS

- 6.4.11 Epignosis LLC

- 6.4.12 360LEARNING SA

- 6.4.13 Litmos US, L.P.

- 6.4.14 Open LMS LLC

- 6.4.15 Schoox, LLC

- 6.4.16 SkyPrep Inc.

- 6.4.17 Tovuti, Inc.

- 6.4.18 Kallidus Limited

- 6.4.19 eloomi A/S

- 6.4.20 iSpring Solutions, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment