|

시장보고서

상품코드

2063964

아시아태평양의 고출력 LED 패키지 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Asia-Pacific High-Power LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

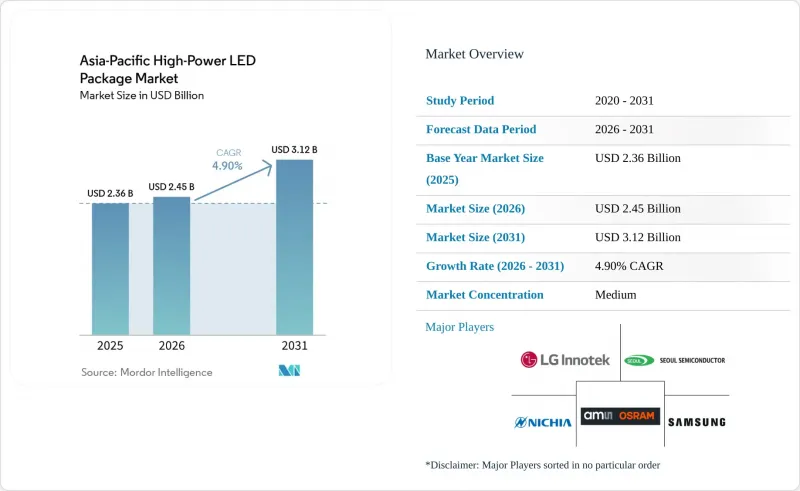

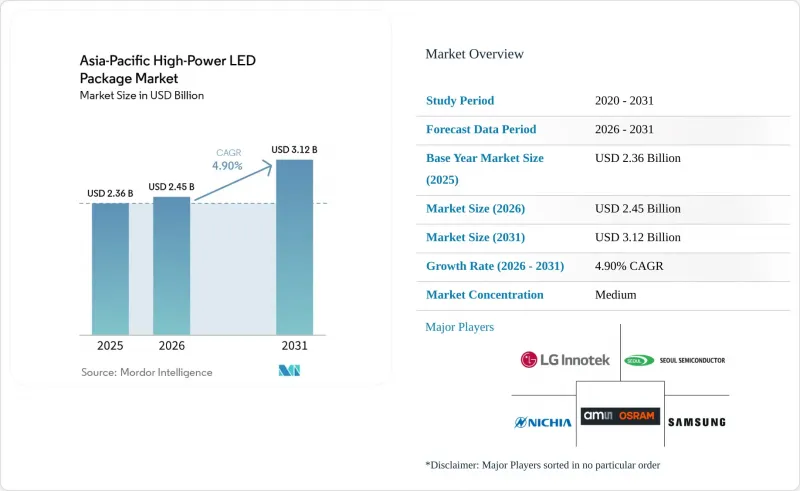

Mordor Intelligence에 의하면, 아시아태평양 고출력 LED 패키지 시장 규모는 2026년에 24억 5,000만 달러로 평가되었고 2025년 23억 6,000만 달러에서 확대해, 2031년까지 31억 2,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 4.90%를 기록할 전망입니다.

본 보고서는 출력 범위(1W-3W, 3W-10W, 10W 이상), 아키텍처(싱글 다이 패키지(SMD/디스크리트), 멀티 다이 패키지(SMD) 등), 용도(일반 조명, 자동차용 조명, 디스플레이 및 백라이트, 특수/니치), 그리고 국가(중국, 일본, 인도, 동남아시아, 기타 아시아태평양)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

아시아태평양의 고출력 LED 패키지 시장 동향 및 인사이트

프리미엄 소비자용 기기에서 Mini-LED 백라이트 채택이 급증하고 있습니다.

프리미엄 TV와 태블릿은 명암비와 로컬 디밍의 정밀도를 높이기 위해 엣지 라이트 방식에서 미니 LED 직접 백라이트 방식으로 전환되고 있으며, 이러한 추세는 색상 왜곡 없이 높은 전류 밀도를 감당할 수 있는 고출력 패키지에 대한 수요를 직접적으로 끌어올리고 있습니다. 삼성의 2026년 Neo QLED 라인업과 미디어텍의 마이크로 LED 디스플레이 엔진 전시는 소비자용 스크린을 넘어선 기술 전환을 뒷받침하고 있습니다. TrendForce의 추산에 따르면, 미니 LED 백라이트 출하량은 2024년부터 2029년까지 연평균 17%의 성장률을 보일 것으로 예상되며, 태블릿 시장에서의 보급률은 2027년까지 15%를 나타낼 것으로 전망됩니다. 3W-10W 범위의 패키지는 높은 발광 효율과 관리하기 쉬운 방열 면적을 모두 갖추고 있어, 가장 큰 이점을 누리게 됩니다. 파장 공차 5nm 미만을 유지할 수 있는 공급업체(여전히 일본과 한국에 집중되어 있음)는 OEM 제조업체들이 비닝 사양을 더욱 엄격하게 적용함에 따라 이익률 확대를 확보하고 있습니다.

동아시아 전역에서 가속화되고 있는 스마트 팩토리용 LED 개조

중국과 일본의 제조 공장에서는 에너지 절약 규제를 준수하고 머신 비전의 정확도를 높이기 위해 기존의 방전 램프를 고출력 LED 어레이로 교체하고 있습니다. 오타니 화학의 2025년 계획에 따라, 스마트 조명 제어 시스템을 ERP 시스템과 통합하여 조도 수준을 최적화함으로써 2년 이내에 투자 회수를 달성했습니다. 5W를 초과하는 패키지는 조명 기구의 수를 줄여주므로, 10년의 사용 수명 동안 설치 공수와 유지보수 주기를 단축합니다. 2024년, 중국 공업정보화부는 LED 개조를 적격한 탄소 감축 조치로 인정하는 지침을 발표했습니다. 또한, 야간 근무 시 작업 환경 개선을 위해 색온도를 조절할 수 있는 조광 가능한 백색 스펙트럼 제품에 대한 수요도 증가하고 있습니다.

2025년 이후 사파이어 기판 공급 부족

반도체 팹이 에피택시 라인을 5G 인프라용 고주파 필터 생산에 전용함에 따라 사파이어 웨이퍼 공급이 부족해졌고, 현물 가격은 전 분기 대비 20% 상승했습니다. 장기 공급 계약을 맺지 않은 중국 및 대만의 포장 제조업체들은 변동이 심한 현물 시장에서 입찰에 참여할 수밖에 없어, 매출 총이익률이 압박을 받고 있습니다. Sanan Optoelectronics와 같이 자체적으로 사파이어 성장로를 가동하는 수직 통합형 기업들은 비용 안정성을 유지하고 경쟁사보다 저렴한 가격으로 공급할 수 있기 때문에 업계 재편이 진행되고 있습니다. 2027년 이후 말레이시아와 베트남의 신규 생산 능력이 가동되기 시작하면 상황은 완화될 전망이지만, 당분간은 공급 부족이 지속될 것으로 예상되어 중소규모 기업들이 자동차 업계와 다년 계약을 체결하는 것을 주저하게 만드는 요인이 될 것입니다.

부문별 분석

2025년, 1W-3W 범위는 고출력 LED 패키지 시장의 45.51%를 차지했는데, 이는 비용에 민감한 일반 조명 분야에 기인한 것입니다. 10W를 초과하는 그룹은 2031년까지 연평균 5.39%의 성장률이 예상됩니다. 이는 모듈 수가 적은 제품보다는 고휘도 모듈을 핵심으로 한 조명 기구의 이점을 누리는 자동차 헤드램프, 산업용 하이베이 조명, 경기장용 투광등에 의해 주도되는 현상입니다. 이러한 구조적 전환이 가능해진 것은 다이아몬드 기판과 0.5K W?¹ 미만의 접합부에서 케이스까지의 저항 덕분에 패키지가 기존의 열적 한계를 뛰어넘을 수 있게 되었기 때문입니다. 각 자동차 OEM 업체들은 보다 정밀한 빔 제어와 드라이버의 간소화를 중시하고 있으며, 이는 중국의 GB 4599-2024 규격 및 인도의 AIS-199 초안에 따른 10W 초과 제품 채택 동향과 일치합니다. 첨단 소재 과학 기술을 보유하지 않은 공급업체는 이 고수익률 시장을 수직 통합형 중국 및 일본 경쟁사들에게 빼앗길 위험이 있습니다.

3W-10W 중급 시장 전망은 여전히 밝습니다. 이는 특히 공공 가로등이나 원예용 램프 등의 용도에서 루멘 출력과 설비 투자 예산의 제약을 효과적으로 조화시킬 수 있기 때문입니다. 이러한 부문들은 비용 대비 효과와 특정 요건에 대한 적합성 때문에 계속해서 이 출력 범위에 의존하고 있습니다. 그러나 고출력 등급에서 루멘당 단가의 하락은 이 등급의 중장기적인 존재 의의에 있어 잠재적인 과제가 됩니다. 스마트 팩토리로의 전환과 미니 LED 백라이트 기술의 발전이 지속된다면, 이러한 추세는 더욱 두드러질 가능성이 있습니다. 이러한 기술들은 뛰어난 발광 효율과 더욱 엄격한 비닝 기준을 중시하는 경향이 강해지고 있어, 시장의 선호도가 더 고성능인 대체품으로 이동할 우려가 있기 때문입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the asia-Pacific high-Power lED package market size was valued at USD 2.45 billion in 2026 and is projected to expand from USD 2.36 billion in 2025 to reach USD 3.12 billion by 2031, registering a 4.90% CAGR over 2026-2031.

This report is Segmented by Power Range (1W-3W, 3W-10W, Above 10W), Architecture (Single-Die Packages (SMD / Discrete), Multi-Die Packages (SMD), and More), Application (General Lighting, Automotive Lighting, Display and Backlighting, Specialty / Niche), and Country (China, Japan, India, Southeast Asia, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific High-Power LED Package Market Trends and Insights

Surge in Mini-LED Backlight Adoption in Premium Consumer Devices

Premium televisions and tablets are shifting from edge-lit designs to mini-LED direct backlighting to raise contrast ratios and local dimming precision, a move that directly lifts demand for high-power packages capable of handling elevated current densities without color-shift drift. Samsung's 2026 Neo QLED lineup and MediaTek's showcase of micro-LED display engines confirm technology migration beyond consumer screens. TrendForce estimates show that mini-LED backlight unit shipments will grow 17% annually from 2024 through 2029, with tablet penetration reaching 15% by 2027. Packages in the 3 W-10 W bracket benefit most because they combine high luminous efficacy with manageable thermal footprints. Suppliers able to maintain sub-5 nm wavelength tolerance, still concentrated in Japan and South Korea, secure margin expansion as OEMs tighten binning specifications.

Accelerated Smart-Factory LED Retrofits Across East Asia

Manufacturing plants in China and Japan are swapping legacy discharge lamps for high-power LED arrays to meet energy-efficiency mandates and improve machine-vision accuracy. Dagu Chemical's 2025 program integrated smart lighting controls with enterprise resource planning systems to optimize lux levels, achieving operational payback within 2 years. Packages above 5 W reduce luminaire counts, thereby cutting installation labor and maintenance cycles over a 10-year life. In 2024, China's Ministry of Industry and Information Technology issued guidance classifying LED retrofits as a qualified carbon-reduction measure. Demand is also rising for tunable white-spectrum products that shift color temperature for night-shift ergonomics.

Supply Tightness of Sapphire Substrates Post-2025

As semiconductor fabs reallocated epitaxy lines toward radio-frequency filters for 5G infrastructure, sapphire wafer supply tightened, and spot prices rose by 20% quarter over quarter. Chinese and Taiwanese packagers without long-term offtake contracts must bid in volatile spot markets, eroding gross margins. Vertically integrated players such as Sanan Optoelectronics, which runs captive sapphire-growth furnaces, maintain cost stability and underprice rivals, driving consolidation. Relief is likely after 2027 when new Malaysian and Vietnamese capacity becomes operational, yet near-term tightness is expected to restrict smaller firms from committing to multi-year automotive contracts.

Other drivers and restraints analyzed in the detailed report include:

- Government-Backed Automotive LED Mandates in China and India

- Thermal-Management Breakthroughs Enabling Above 5 W Single-Package Output

- IP Litigation Risks in Flip-Chip Package Designs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, the 1 W-3 W bracket captured 45.51% of the High-Power LED Package market, a position rooted in cost-sensitive general lighting. The Above 10 W group is forecast to grow 5.39% annually through 2031, propelled by automotive headlamps, industrial high bays, and stadium floodlights that benefit from luminaires built around fewer yet brighter modules. This structural pivot is possible because diamond substrates and sub-0.5 K W-1 junction-to-case resistance allow packages to exceed earlier thermal ceilings. Automotive original equipment manufacturers value tighter beam control and reduced driver complexity, aligning with Above 10 W adoption with China's GB 4599-2024 and India's Draft AIS-199 standards. Suppliers lacking advanced material science risk ceding this high-margin turf to vertically integrated Chinese and Japanese rivals.

The prospects for the 3 W-10 W middle tier remain favorable, driven by its ability to effectively balance lumen output with capital budget constraints, particularly in applications such as municipal street lighting and horticulture lamps. These segments continue to rely on this power range due to its cost-effectiveness and suitability for their specific requirements. However, the declining cost per lumen at higher power ratings poses a potential challenge to the long-term relevance of this tier. This trend could become more pronounced if advancements in smart-factory retrofits and mini-LED backlights persist, as these technologies increasingly emphasize premium efficacy and tighter binning standards, which may shift market preferences toward higher-performing alternatives.

List of Companies Covered in this Report:

- Nichia Corporation

- Samsung Electronics Co., Ltd.

- Cree LED, a SMART Global Holdings Inc. company

- OSRAM Opto Semiconductors GmbH

- Seoul Semiconductor Co., Ltd.

- Lumileds Holding B.V.

- LG Innotek Co., Ltd.

- Everlight Electronics Co., Ltd.

- Epistar Corporation

- Toyoda Gosei Co., Ltd.

- Seoul Viosys Co., Ltd.

- Lite-On Technology Corporation

- Honglitronic Co., Ltd.

- Lextar Electronics Corporation

- Foshan NationStar Optoelectronics Co., Ltd.

- Sanan Optoelectronics Co., Ltd.

- Genesis Photonics Inc.

- Edison Opto Corporation

- Dominant Opto Technologies Sdn. Bhd.

- ProLight Opto Technology Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Mini-LED Backlight Adoption in Premium Consumer Devices

- 4.2.2 Accelerated Smart-Factory LED Retrofits Across East Asia

- 4.2.3 Government-Backed Automotive LED Mandates in China and India

- 4.2.4 Thermal-Management Breakthroughs Enabling Above 5 W Single-Package Output

- 4.2.5 Rise of Vertical-Integration Models Among Chinese Packaging Houses

- 4.2.6 Advanced Driver-Assistance Systems Demanding High-Intensity Headlamps

- 4.3 Market Restraints

- 4.3.1 Supply Tightness of Sapphire Substrates Post-2025

- 4.3.2 IP Litigation Risks in Flip-Chip Package Designs

- 4.3.3 Persistent Cost Gap Versus Mid-Power Alternatives in General Lighting

- 4.3.4 Regulatory Scrutiny on Blue-Light Hazard in Public Illumination

- 4.4 Industry Value Chain Analysis

- 4.5 Technology Analysis

- 4.6 Regulatory Landscape

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Range

- 5.1.1 1 W - 3 W

- 5.1.2 3 W - 10 W

- 5.1.3 Above 10 W

- 5.2 By Architecture

- 5.2.1 Single-Die Packages (SMD / Discrete)

- 5.2.2 Multi-Die Packages (SMD)

- 5.2.3 COB (Chip-on-Board)

- 5.2.4 Other Architectures (CSP, Flip-Chip, Hybrid Modules)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

- 5.4 By Country

- 5.4.1 China

- 5.4.2 Japan

- 5.4.3 India

- 5.4.4 Southeast Asia

- 5.4.5 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Samsung Electronics Co., Ltd.

- 6.4.3 Cree LED, a SMART Global Holdings Inc. company

- 6.4.4 OSRAM Opto Semiconductors GmbH

- 6.4.5 Seoul Semiconductor Co., Ltd.

- 6.4.6 Lumileds Holding B.V.

- 6.4.7 LG Innotek Co., Ltd.

- 6.4.8 Everlight Electronics Co., Ltd.

- 6.4.9 Epistar Corporation

- 6.4.10 Toyoda Gosei Co., Ltd.

- 6.4.11 Seoul Viosys Co., Ltd.

- 6.4.12 Lite-On Technology Corporation

- 6.4.13 Honglitronic Co., Ltd.

- 6.4.14 Lextar Electronics Corporation

- 6.4.15 Foshan NationStar Optoelectronics Co., Ltd.

- 6.4.16 Sanan Optoelectronics Co., Ltd.

- 6.4.17 Genesis Photonics Inc.

- 6.4.18 Edison Opto Corporation

- 6.4.19 Dominant Opto Technologies Sdn. Bhd.

- 6.4.20 ProLight Opto Technology Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment