|

시장보고서

상품코드

2063945

LED 패키징 장비 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)LED Packaging Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

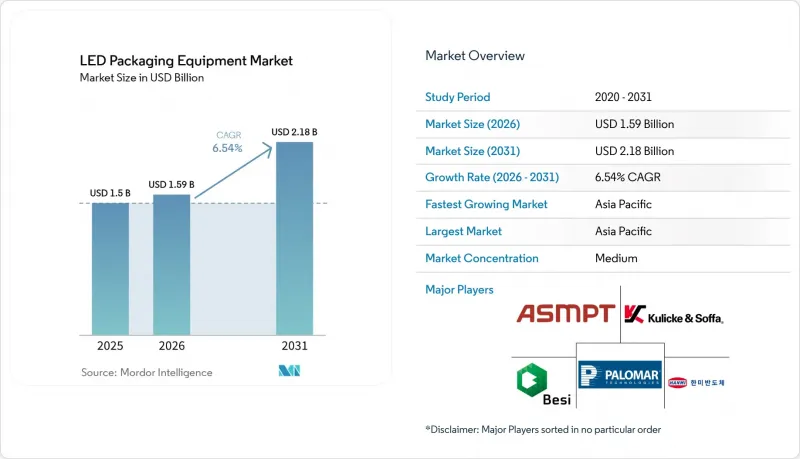

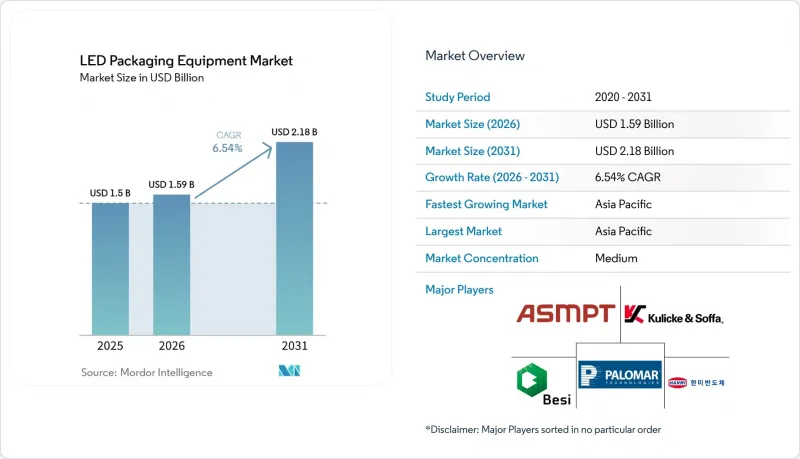

Mordor Intelligence에 의하면, LED 패키징 장비 시장 규모는 2025년 15억 달러에서 2026년에는 15억 9,000만 달러로 확대되어 2031년까지 21억 8,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 6.54%로 성장할 전망입니다.

본 보고서는 장비 유형(다이 본딩 장비, 와이어 본딩 장비, 봉지 장비 등), 패키지 유형(SMD LED 패키지, COB 패키지, CSP LED 패키지), LED 용도(일반 조명, 디스플레이, 자동차용 조명, 소비자용 전자장비) 및 지역(북미, 유럽 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 LED 패키징 장비 시장 동향 및 분석

미니 LED 및 마이크로 LED 생산 능력의 급속한 확대

각 부문의 주요 기업들은 수만 개의 미니 LED를 사용하는 풀 어레이 로컬 디밍 패널의 생산 규모를 확대하고 있으며, 장비에는 ±10 마이크로미터의 정밀도를 유지하면서 고속 칩 이송이 요구되고 있습니다. ASMPT사의 Vortex II 다이 본더는 2밀 × 4밀 크기의 다이에서 99.999%의 점등 수율을 달성하며, 첨단 디스플레이 도입을 위한 성능 기준을 한 단계 높였습니다. Kulicke and Soffa사의 LUMINEX 레이저 시스템은 선별 및 리피칭 기능을 단일 장비에 통합하여, 직접 뷰 RGB 및 백라이트의 전체 워크플로우에서 대응 가능한 기회를 확대되고 있습니다. Besi는 포토닉스 및 LED의 보급을 배경으로, 다이 어태치 시장 규모가 2026년까지 2배인 16억 달러에 달할 것으로 전망하고 있습니다. 이러한 업그레이드로 인해 라인당 자본 비용이 최대 40% 증가하여, 정부 지원을 받는 Tier 1 패널 제조업체에 규모의 경제 효과를 가져다줄 것입니다. 소규모 팹들은 처리량 확보에 어려움을 겪고 있어, 업계 재편이 가속화될 가능성이 있습니다.

자동차용 어댑티브 헤드라이트의 보급 확대

자동차 제조업체들은 눈부심이 없는 하이빔과 600미터의 조사 거리를 실현하는 매트릭스 LED 시스템으로의 전환을 추진하고 있으며, 이에 따라 패키징 공차는 Z축 방향 높이에서 ±35 마이크로미터로 더욱 엄격해졌습니다. ams OSRAM의 OSLON Compact PL 시리즈에는 절연된 열전도 패드가 채택되어 있으며, 이를 위해서는 고정밀 픽 앤 플레이스 공정과 관리된 열전도 재료가 필요합니다. 픽셀화된 이미터는 서브픽셀 단위의 배치가 요구되므로, 공급업체들은 배치 오류를 보정하기 위한 고해상도 비전 시스템과 자동 복구 루프를 탑재하고 있습니다. AEC-Q102에 따른 인증에는 24개월이 소요될 수 있으며, 검증 과정이 장기화되는 반면, 자동차 업계에서 인증받은 공정 레시피를 보유한 공급업체가 유리한 입장에 서게 됩니다. 규제 완화가 유럽에서 북미, 아시아로 확대됨에 따라, 어댑티브 모듈은 미드레인지 트림에 기본 사양으로 탑재될 전망이며, 이는 다이 본더 및 검사 장비의 수주 대수 증가로 이어질 것으로 예측됩니다.

미국 수출 통제 대상인 와이어 본더에 대한 무역 규정 준수 감사

미국 산업안보국(BIS)은 2024년 12월, 규제 대상 목록에 24개 장비 범주를 추가하고, 외국산이지만 미국산 IC를 포함하는 장비에 대해서도 ‘외국 직접 제품(FDP)’ 규정의 적용 범위를 확대했습니다. 현재 패키징 공급업체들은 라이선스 취득까지 60-90일간의 출하 지연을 겪고 있으며, 어플라이드 머티리얼즈가 2억 5,200만 달러의 합의금을 지급한 사례는 분류 오류가 초래하는 금전적 손실을 여실히 보여주고 있습니다. 일부 공급업체는 미국산 부품을 배제하기 위해 모션 제어 보드의 재설계를 검토하고 있지만, 엔지니어링 비용이 많이 들고 성능이 저하될 가능성이 있습니다. 이러한 제약을 받지 않는 중국의 장비 제조업체들은 특히 베이징이 정한 ‘설비의 50%를 현지에서 조달’해야 한다는 기준을 충족하기 위해 서두르는 팹(반도체 제조 공장)을 중심으로 시장 점유율을 확보할 절호의 기회를 포착하고 있습니다.

부문별 분석

다이본더는 2025년 매출의 35.68%를 차지하며, LED 패키징 장비 시장에서 그 핵심적인 역할을 여실히 보여주고 있습니다. 와이어 본더는 여전히 중요하지만, 상호 연결 방식이 언더범프로 전환됨에 따라 플립칩 및 CSP 설계로 인해 그 점유율은 감소하고 있습니다. 봉지 디스펜서는 공정 흐름에서 다이 배치에 이어, 실리콘이나 에폭시 수지를 UV 또는 열경화시켜 접합부를 보호합니다. 자동 패키징 시스템은 이 3가지 공정에 더해 인라인 검사를 통합한 턴키 셀로서, 택트 타임을 단축합니다. 이러한 라인은 처리량을 20-30% 향상시키고 인건비를 약 15-20% 절감하므로, 조기에 도입한 기업에게는 총소유비용(TCO) 측면에서 분명한 이점을 제공합니다. ASMPT의 ‘In-Line Linker System’은 자사의 Vortex II 본더를 전 공정 및 후 공정 스테이션과 동기화하여 생산성을 획기적으로 향상시켰음을 입증하고 있습니다. 자동화 플랫폼의 비용은 개별 장비의 2-3배이지만, 가동률이 80%를 넘으면 투자 회수 기간이 단축됩니다. 아시아의 중소 공급업체들은 현재 가격에 민감한 구매자들을 유치하기 위해 다이 본딩, 디스펜스, 비전 모듈을 묶음 판매하고 있습니다. 그 결과, 예측 기간이 끝날 무렵에는 자동화 라인이 LED 패키징 장비 시장에서 더 큰 점유율을 차지할 것으로 전망됩니다.

자동화의 급속한 확산은 데이터 추적성, 예측 유지보수, 원격 진단을 요구하는 ‘인더스트리 4.0’의 요건과 부합합니다. 유럽의 고객들은 설비 투자(CAPEX)를 줄이기 위해 재생 장비를 선호하는 반면, 북미의 팹에서는 정부의 인센티브와 연계된 추적성 규정을 준수하기 위해 새롭고 완벽하게 연결된 장비를 선호하는 경향이 있습니다. 두 지역 모두 기술자 부족에 직면한 가운데, 자체 보정 기능이 탑재된 본더와 자동 프로그래밍 AOI는 기술적 진입 장벽을 낮춰줍니다. 이러한 전환은 일률적으로 진행되지 않을 것으로 보이며, Tier 2 조립 제조업체는 여전히 반자동 작업 셀을 운영하는 반면, Tier 1 디스플레이 및 자동차 부품 공급업체는 무인화 공장으로 전환하는 경향을 보이고 있습니다. 모듈식 업그레이드를 제공할 수 있는 공급업체는 두 가지 요구 사항 모두를 충족시킬 수 있으며, 경기 순환에 따른 수익 변동을 완화할 수 있습니다.

지역별 분석

아시아태평양은 2025년에 LED 패키징 장비 시장 규모의 68.71%를 차지하며 주도적인 위치를 차지하고 있으며, 2031년까지 연평균 성장률(CAGR) 7.17%를 나타낼 것으로 전망됩니다. 중국의 국내 장비 50% 할당 제도에 따라 Naura나 JT Automation을 통한 현지 조달이 가속화되고 있으며, 합작 회사를 설립하지 않는 한 수입업체들은 소외될 수밖에 없습니다. 일본의 ‘Rapidus’ 계획에 따른 535억 엔(3억 5,500만 달러)의 보조금은 첨단 패키징 산업 재활성화를 위한 노력과 부합하며, 정밀 공구 공급업체들에게 새로운 고객 기반을 마련해 주고 있습니다. 한국의 한미 반도체는 현지화된 서비스를 바탕으로 마이크론 내 신카와(Shinkawa)사의 입지를 빼앗았습니다. 이는 설비의 가동률과 지리적 근접성이 기존 기업의 우위를 능가함을 보여줍니다.

북미와 유럽을 합치면 2025년 매출의 약 4분의 1을 차지했습니다. 이 지역의 LED 패키징 장비 시장은 엄격한 수출 규정 준수 요건과 인력 부족에 의해 형성되고 있습니다. 미국의 BIS 규정에 따라 미국산 IC가 포함된 제품의 출하가 지연되고 있으며, 일부 공급업체는 ‘미국 의존도 탈피’를 위해 제어 기판의 재설계를 서둘러야 하는 상황에 처해 있습니다. 한편, ‘CHIPS and Science Act’는 국내 첨단 패키징 라인에 대한 보조금을 유도함으로써, 규정 준수로 인한 부담을 부분적으로 상쇄하고 있습니다. 유럽에서는 인증된 리퍼비시 장비에 대한 관심이 높아지고 있으며, TOWA의 프로그램은 40-60%의 가격 할인을 제공하고 있지만, 지역 전체를 아우르는 품질 보증 마크가 없어 자금 조달에 불확실성이 발생하고 있습니다.

남미, 중동 및 아프리카의 2025년 매출 기여도는 7% 미만이었습니다. 이 회사의 주요 활동은 수입된 LED 다이를 조립하여 완제품 램프나 간판 모듈을 만드는 데 집중되어 있습니다. 정부의 전기화 계획에 따라 턴키 생산 라인이 도입되기도 하지만, 현장 기술자 부족과 예비 부품의 물류 문제가 대규모 자동화를 가로막고 있습니다. 통신 사업자가 주도하는 스마트 시티 실증 프로젝트가 진행됨에 따라, 중규모 AOI(자동 검사 장비)가 탑재된 생산 라인에 대한 수요가 국지적으로 발생할 가능성은 있지만, 그 규모는 여전히 적어 전 세계 공급업체의 로드맵에 영향을 미칠 정도는 아닙니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the lED packaging equipment market size is expected to increase from USD 1.50 billion in 2025 to USD 1.59 billion in 2026 and reach USD 2.18 billion by 2031, growing at a CAGR of 6.54% over 2026-2031.

This report is Segmented by Equipment Type (Die Bonding Equipment, Wire Bonding Equipment, Encapsulation Equipment, and More), Package Type (SMD LED Packaging, COB Packaging, and CSP LED Packaging), LED Application (General Lighting, Displays, Automotive Lighting, and Consumer Electronics), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global LED Packaging Equipment Market Trends and Insights

Rapid Mini-LED and Micro-LED Capacity Ramp-Up

Segment leaders are scaling full-array local-dimming panels that use tens of thousands of mini-LEDs, forcing equipment to deliver mass-transfer speed without compromising +-10 micrometer accuracy. ASMPT's Vortex II die bonder hits 99.999% light-up yield for 2 mil X 4 mil dies, raising the performance bar for advanced display deployment. Kulicke and Soffa's LUMINEX laser system couples sorting and re-pitching in one tool, widening addressable opportunities across direct-view RGB and backlighting workflows. Besi projects its die-attach addressable market to double to USD 1.6 billion by 2026 on the back of photonics and LED adoption. These upgrades lift capital per line by as much as 40%, creating scale advantages for tier-1 panel makers with access to state support. Smaller fabs struggle to match throughput, potentially accelerating industry consolidation.

Rising Adoption of Automotive Adaptive Headlamps

Automakers are migrating to matrix LED systems that enable glare-free high beams and 600-meter reach, pushing packaging tolerances toward +-35 micrometers in z-height. ams OSRAM's OSLON Compact PL families come with isolated thermal pads that demand precision pick-and-place and controlled thermal-interface materials. Pixelated emitters require sub-pixel placement, so equipment vendors are embedding high-resolution vision systems and auto-recovery loops for misplacement correction. Qualification under AEC-Q102 can last 24 months, elongating the validation pipeline and favoring suppliers with automotive-certified process recipes. As regulatory green lights spread from Europe to North America and Asia, adaptive modules are set to become standard on mid-range trims, stimulating higher unit orders for die bonders and inspection tools.

Trade-Compliance Audits on US Export-Controlled Wire-Bonders

The U.S. Bureau of Industry and Security added 24 tool categories to its controlled list in December 2024 and extended Foreign Direct Product rules to foreign-made gear containing U.S. ICs. Packaging suppliers now face 60-90 day shipment delays while licenses clear, and Applied Materials' USD 252 million settlement illustrates the monetary downside of mis-classification. Some vendors contemplate redesigning motion-control boards to rid U.S. content, but engineering costs are steep and performance may slip. Chinese toolmakers free of these constraints are finding an opening to capture share, particularly among fabs racing to meet Beijing's 50% local-equipment threshold.

Other drivers and restraints analyzed in the detailed report include:

- Line Yield Gains Via Inline AOI/AXI Integration

- Demand for Low-Temperature Sintered Silver Die-Attach Pastes

- Thermal Run-Away Risks in High-Power CSP Lines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Die bonders accounted for 35.68% of 2025 revenue, underscoring their central role in the LED packaging equipment market. Wire bonders remain relevant, yet flip-chip and CSP designs erode their volume share as interconnects shift under-bump. Encapsulation dispensers follow die placement in the process flow, coupling silicone or epoxy resins with UV or thermal curing to protect the junction. Automated packaging systems combine all three steps, plus inline inspection, into turnkey cells that shorten takt time. These lines command 20-30% higher throughput and cut labor by roughly 15-20%, giving early adopters a measurable cost-of-ownership edge. ASMPT's In-Line Linker System synchronizes its Vortex II bonder with upstream and downstream stations, proving the productivity jump. Although automated platforms cost two to three times more than standalone tools, payback compresses when capacity utilization tops 80%. Smaller Asian vendors are now bundling die bond, dispense, and vision modules to court price-sensitive buyers. Consequently, automated lines are projected to capture a larger share of the LED packaging equipment market by the end of the forecast period.

The surge in automation dovetails with Industry 4.0 mandates for data traceability, predictive maintenance and remote diagnostics. European customers lean on refurbished equipment to temper capex, but North American fabs often favor new, fully connected gear to comply with traceability rules tied to government incentives. As both regions wrestle with technician shortages, self-calibrating bonders and auto-programming AOI lessen the skills hurdle. The transition is unlikely to be uniform, tier-2 assemblers may still run semi-automated workcells, whereas tier-1 display and automotive suppliers gravitate toward lights-out factories. Vendors able to offer modular upgrades can cater to both profiles, cushioning revenue volatility across business cycles.

Geography Analysis

Asia-Pacific dominated with 68.71% of LED packaging equipment market size in 2025 and is on track to register a 7.17% CAGR through 2031. China's 50% domestic-equipment quota accelerates local procurement from Naura and JT Automation, marginalizing importers unless they form joint ventures. Japan's JPY 53.5 billion (USD 355 million) subsidy inside the Rapidus scheme aligns with its push to reboot advanced packaging, presenting a fresh customer base for precision tool vendors. South Korea's Hanmi Semiconductor leveraged localized service to dethrone Shinkawa at Micron, highlighting how equipment uptime and proximity override legacy incumbency.

North America and Europe together accounted for roughly one-quarter of 2025 revenue. The LED packaging equipment market here is shaped by strict export compliance and a labor crunch. The U.S. BIS rulebook slows shipments containing U.S. ICs, prompting some vendors to redesign control boards for de-Americanization. On the upside, the CHIPS and Science Act channels grants toward domestic advanced-packaging lines, partially offsetting compliance drag. Europe shows rising interest in certified refurbished gear; TOWA's program offers 40-60% price relief but operates without a region-wide quality seal, creating financing uncertainty.

South America, the Middle East and Africa contributed less than 7% of 2025 turnover. Activity centers on assembling imported LED dice into finished lamps or signage modules. Government electrification plans occasionally seed turnkey lines, yet shortage of field engineers and spare-parts logistics hampers large-scale automation. As telco-backed smart-city pilots progress, pockets of demand may emerge for mid-range AOI-equipped lines, but volumes remain too modest to sway global supplier roadmaps.

- ASM Pacific Technology Ltd.

- Kulicke and Soffa Industries Inc.

- BE Semiconductor Industries N.V.

- Hanmi Semiconductor Co., Ltd.

- Palomar Technologies Inc.

- Shinkawa Ltd.

- Toray Engineering Co., Ltd.

- Suneast Equipment Co., Ltd.

- Besi APAC Pte. Ltd.

- ASMPT Suzhou Co., Ltd.

- F&K Delvotec Bondtechnik GmbH

- Towa Corporation

- Nordson Corporation

- DIAS Automation (Suzhou) Co., Ltd.

- Hitachi High-Tech Corporation

- Nitto Denko Corporation

- Shenzhen JT Automation Equipment Co., Ltd.

- Tronstol Technology Co., Ltd.

- Datacon Technology GmbH

- Revasum Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Supply-Chain Analysis

- 4.3 Regulatory Landscape

- 4.4 Technology Outlook

- 4.5 Impact of Macroeconomic Factors

- 4.6 Market Drivers

- 4.6.1 Rapid Mini-LED and Micro-LED Capacity Ramp-Up

- 4.6.2 Rising Adoption of Automotive Adaptive Headlamps

- 4.6.3 Line Yield Gains Via Inline AOI/AXI Integration

- 4.6.4 Demand for Low-Temperature Sintered Silver Die-Attach Pastes

- 4.6.5 Government Subsidies for Domestic Packaging Lines in Asia-Pacific

- 4.6.6 Equipment Refurbishment Market Formalisation in Europe

- 4.7 Market Restraints

- 4.7.1 Trade-Compliance Audits on US Export-Controlled Wire-Bonders

- 4.7.2 Thermal Run-Away Risks in High-Power CSP Lines

- 4.7.3 Skilled Operator Shortage for Sub-10 µm Flip-Chip Bonding

- 4.7.4 CAPEX Freezes at Tier-2 Display Makers

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Equipment Type

- 5.1.1 Die Bonding Equipment

- 5.1.2 Wire Bonding Equipment

- 5.1.3 Encapsulation Equipment

- 5.1.4 Automated Packaging Systems

- 5.2 By Package Type

- 5.2.1 SMD LED Packaging

- 5.2.2 COB Packaging

- 5.2.3 CSP LED Packaging

- 5.3 By LED Application

- 5.3.1 General Lighting

- 5.3.2 Displays

- 5.3.3 Automotive Lighting

- 5.3.4 Consumer Electronics

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 Southeast Asia

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ASM Pacific Technology Ltd.

- 6.4.2 Kulicke and Soffa Industries Inc.

- 6.4.3 BE Semiconductor Industries N.V.

- 6.4.4 Hanmi Semiconductor Co., Ltd.

- 6.4.5 Palomar Technologies Inc.

- 6.4.6 Shinkawa Ltd.

- 6.4.7 Toray Engineering Co., Ltd.

- 6.4.8 Suneast Equipment Co., Ltd.

- 6.4.9 Besi APAC Pte. Ltd.

- 6.4.10 ASMPT Suzhou Co., Ltd.

- 6.4.11 F&K Delvotec Bondtechnik GmbH

- 6.4.12 Towa Corporation

- 6.4.13 Nordson Corporation

- 6.4.14 DIAS Automation (Suzhou) Co., Ltd.

- 6.4.15 Hitachi High-Tech Corporation

- 6.4.16 Nitto Denko Corporation

- 6.4.17 Shenzhen JT Automation Equipment Co., Ltd.

- 6.4.18 Tronstol Technology Co., Ltd.

- 6.4.19 Datacon Technology GmbH

- 6.4.20 Revasum Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment