|

시장보고서

상품코드

2063982

북미의 고출력 LED 패키지 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)North America High-Power LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

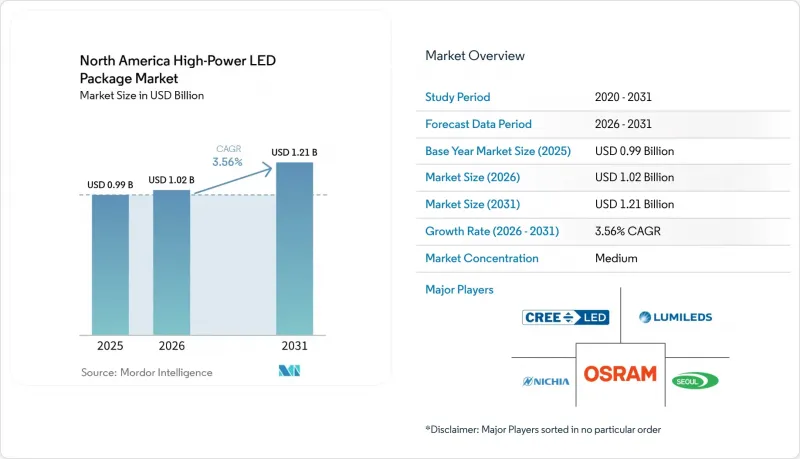

Mordor Intelligence에 의하면, 북미 고출력 LED 패키지 시장 규모는 2025년 9억 9,000만 달러, 2026년 10억 2,000만 달러에서 2031년까지 12억 1,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 3.56%를 나타낼 것으로 예측됩니다.

본 보고서는 출력 범위(1W-3W, 3W-10W, 10W 이상), 아키텍처(싱글 다이 패키지, 멀티 다이 패키지, COB, 기타), 용도(일반 조명, 자동차용 조명, 디스플레이 및 백라이트, 특수 용도), 지역(미국, 캐나다, 멕시코)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

북미 고출력 LED 패키지 시장 동향 및 인사이트

정부의 비효율적인 램프 단계적 폐지

연방 및 주 정부의 규제로 인해 백열등 및 형광등 제품은 단기간 내에 시장에서 철수할 수밖에 없게 되었으며, 기존 조명 기구의 본체 내에서 1와트당 120루멘을 달성할 수 있는 고출력 패키지에 대한 수요가 급증하고 있습니다. 2028년 7월에 발효될 미국 에너지부의 규제와 2024년부터 2027년 사이에 시행될 6개 주의 금지 조치가 이러한 변화의 원동력이 되고 있으며, 3와트에서 10와트 사이의 발광 소자가 리트로핏용 다운라이트 및 트랙 헤드의 표준적인 선택지로 자리 잡고 있습니다. 유통업체은 판매 중단 기한을 앞두고 구형 재고 처분을 진행하고 있는 반면, 조명 기구 제조업체는 발광 효율, 루멘 밀도, 색상 품질 목표를 충족하는 칩 온 보드(COB) 및 멀티 다이 모듈 개발을 서둘러 진행하고 있습니다. 자사에서 형광체 및 열 설계에 대한 전문 지식을 보유한 공급업체는 규정 준수 감사로 인해 성능이 부족한 제품이 리콜 위험에 노출되기 때문에 그 혜택을 누리고 있습니다. 그 결과, 예측 기간 중반까지 지속될 구조적인 성장의 호재가 나타나고 있습니다.

자동차 헤드램프에서 LED의 급속한 보급

어댑티브 드라이빙 빔의 승인으로 인해 전면 조명 부품 구성이 재구성되었습니다. 승용차의 LED 보급률은 이미 70%를 넘어섰으며, 새로운 헤드램프 눈부심 규제에 따라 픽셀 수준의 시스템이 고급차에서 양산 모델로 점차 확대되고 있습니다. 매트릭스 어레이는 개별적으로 제어 가능한 수십 개의 다이를 소형 기판 위에 배치한 것으로, 열 저항이 낮고 정밀한 비닝이 적용된 고출력 패키지가 선호되고 있습니다. CES 2026에서 수상한 LG이노텍의 초슬림 픽셀 모듈은 폼 팩터의 소형화와 V2X(차량과 사물 간 통신)의 전망이 조명을 안전 및 통신 자산으로 변화시키고 있음을 보여줍니다. 자동차 시장 점유율의 69.2%를 차지하는 1차 공급업체들은 특허 풀과 교차 라이선스를 활용하여 설계 채택을 확보하고 있으며, 2027년형 모델의 출시가 다가옴에 따라 향후 수년에 걸친 생산량 확대를 확실시했습니다.

1A를 초과하는 구동 전류에서의 열 관리 및 신뢰성 문제

1암페어를 초과하는 전류로 패키지를 구동하면 접합부 온도가 150°C 이상으로 상승하며, 온도가 10°C 상승할 때마다 수명이 절반으로 줄어듭니다. 설계자는 세라믹 기판, 베퍼 챔버 또는 능동 냉각 방식을 채택해야 하지만, 이러한 방식들은 비용과 무게 증가로 이어집니다. 열 강하로 인해 발광 효율은 350mA 시의 150루멘/와트에서 1.5A 시에는 120루멘/와트 가까이까지 떨어지게 되어, 발광 소자 수를 줄임으로써 얻는 이점이 상쇄되어 버립니다. 사이클에 따른 계면 재료의 열화나 솔더의 피로로 인해 보증 위험이 높아지기 때문에 많은 조명 기구에서는 정격 전류를 70%로 낮추고 있습니다. 기판 및 형광체 재료의 기술 혁신을 통해 발광원의 발열이 줄어들기 전까지는 비용 효율을 중시하는 일반 조명 분야에서 대전류 작동에 대한 비용상의 제약이 계속 남아 있을 것입니다.

부문별 분석

북미 고출력 LED 패키지 시장에서 10와트 이상 부문은 연평균 성장률(CAGR) 4.11%로 성장하고 있습니다. 이는 스포츠 시설, 창고, 도로 운영 사업자들이 패키지당 10,000루멘을 초과하는 출력을 선호하기 때문입니다. 칩 온 보드(COB) 방식이 주류를 이루고 있습니다. 이는 베어 다이(bare die)를 금속 코어 기판에 직접 실장함으로써 열저항을 2 K/W 미만으로 억제하고, 더 소형인 방열판에도 대응할 수 있기 때문입니다. 2025년에는 1와트-3와트급 제품이 47.88%의 시장 점유율을 유지하며, 기존 하우징과의 설치 공간 호환성을 중시하는 리트로핏용 다운라이트에 채택되고 있습니다.

미국 에너지부(DOE)의 광속 효율 규제와 8K 방송 계약에 따라 설계자들은 광속을 더 적은 수의 광학 지점에 집중하도록 유도받고 있으며, 이를 통해 조립 작업의 노력과 반사판의 수를 줄일 수 있어 성장세가 변화하고 있습니다. Lumileds와 같은 공급업체들은 이러한 추세를 반영하기 위해 2026년 3월에 LUXEON CS를 출시했습니다. 이 제품은 6.3mm에서 22mm까지의 LES 직경과 CRI 90 및 95 옵션을 제공합니다. 3와트-10와트 범위는 하이베이 조명 기구용의 과도기적 구분으로 남아 있지만, 양 극단의 대역이 누리고 있는 것과 같은 명확한 경제적 이점은 부족합니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the north america high-power LED package market size is projected to expand from USD 0.99 billion in 2025 and USD 1.02 billion in 2026 to USD 1.21 billion by 2031, registering a CAGR of 3.56% between 2026 to 2031.

This report is Segmented by Power Range (1 W To 3 W, 3 W To 10 W, and Above 10 W), Architecture (Single-Die Packages, Multi-Die Packages, COB, and Others), Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America High-Power LED Package Market Trends and Insights

Government-Mandated Phase-Out of Inefficient Lamps

Federal and state rules are forcing incandescent and fluorescent products off shelves on a compressed timeline, triggering a sharp pull in demand for high-power packages that can clear 120 lumens per watt within existing fixture envelopes. The U.S. Department of Energy rule, effective July 2028, and six state bans enacted between 2024 and 2027 anchor this shift, making 3-watt to 10-watt emitters the default choice for retrofit downlights and track heads. Distributors are liquidating legacy inventory ahead of cut-off dates, while luminaire brands are fast-tracking chip-on-board and multi-die modules that meet efficacy, lumen density, and color-quality targets. Vendors with in-house phosphor and thermal expertise benefit because compliance audits expose under-performing products to recall risk. The result is a structural growth tailwind that will persist through the middle of the forecast window.

Rapid LED Penetration in Automotive Headlamps

Adaptive driving beam approval is reshaping the front-lighting bill of materials. Passenger-car LED penetration already exceeds 70%, and pixel-level systems are moving from luxury to mass-market models under new regulatory headlamp glare rules. Matrix arrays place dozens of individually addressable dice onto compact substrates, favoring high-power packages with low thermal resistance and precise binning. LG Innotek's ultra-thin pixel module, which won a CES 2026 award, illustrates how shrinking form factors and vehicle-to-everything projections are turning lighting into a safety and communications asset. Tier-one suppliers holding 69.2% automotive share are leveraging patent pools and cross-licenses to secure design wins, locking in multi-year volume ramps as 2027 model launches approach.

Thermal Management and Reliability Challenges Above 1 A Drive

Driving packages at currents above 1 ampere elevates junction temperatures beyond 150 °C, cutting lifetime in half for every 10 °C rise. Designers must adopt ceramic boards, vapor chambers, or active cooling, which adds cost and weight. Thermal droop reduces efficacy from 150 lumens per watt at 350 mA to near 120 lumens per watt at 1.5 A, negating emitter-count savings. Interface material degradation and solder fatigue under cycling raise warranty exposure, so many luminaires derate to 70% of nameplate current. Until breakthroughs in substrate or phosphor materials lower heat at the source, high-current operation will remain cost-capped in cost-sensitive general lighting.

Other drivers and restraints analyzed in the detailed report include:

- 8K Sports-Broadcast Lighting Standards Lifting Lumen Demand

- Dark-Sky Regulations Driving Low-Blue NightScape Packages

- Helium Shortage Disrupting GaN Wafer Processing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The above 10 watt tier of the North America high-power LED package market size is on a 4.11% CAGR path as sports venues, warehouses, and roadway operators favor single-package outputs above 10,000 lumens. Chip-on-board formats dominate because they mount bare dice directly onto metal-core boards, delivering thermal resistance under 2 K/W and supporting smaller heatsinks. In 2025 the 1 watt-3 watt tier retained 47.88% share, serving retrofit downlights that prize footprint compatibility with legacy housings.

Growth momentum is shifting as the DOE efficacy rule and 8K broadcast contracts encourage designers to consolidate flux into fewer optical points, cutting assembly labor and reflector count. Vendors such as Lumileds introduced LUXEON CS in March 2026 to exploit this trend, offering LES diameters from 6.3 mm to 22 mm and CRI options of 90 and 95. The 3 watt-10 watt range remains a transitional bracket for high-bay fixtures but lacks the clear economic edge enjoyed by either extreme.

List of Companies Covered in this Report:

- Nichia Corporation

- ams OSRAM International GmbH

- Lumileds Holding B.V.

- Cree LED Inc.

- Seoul Semiconductor Co., Ltd.

- Samsung Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Everlight Electronics Co., Ltd.

- Citizen Electronics Co., Ltd.

- Bridgelux Inc.

- Luminus Devices Inc.

- Epistar Corporation

- Toyoda Gosei Co., Ltd.

- NationStar Optoelectronics Co., Ltd.

- Hongli Zhihui Group Co., Ltd.

- Sanan Optoelectronics Co., Ltd.

- Signify N.V.

- LITE-ON Technology Corporation

- Broadcom Inc.

- Foshan Refond Optoelectronics Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government-Mandated Phase-Out of Inefficient Lamps

- 4.2.2 Rapid LED Penetration in Automotive Headlamps

- 4.2.3 Stabilization of High-Power LED Package ASPs

- 4.2.4 8K Sports-Broadcast Lighting Standards Lifting Lumen Demand

- 4.2.5 Dark-Sky Regulations Driving Low-Blue Nightscape Packages

- 4.2.6 PoE Smart-Lighting Designs Favoring High-Voltage CSP LEDs

- 4.3 Market Restraints

- 4.3.1 Thermal Management and Reliability Challenges Above 1 A Drive

- 4.3.2 Up-Front Cost Premium Versus Mid-Power LEDs

- 4.3.3 Helium Shortage Disrupting GaN Wafer Processing

- 4.3.4 Geopolitical Risk to Rare-Earth Red Phosphors Supply

- 4.4 Technology Outlook

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Range

- 5.1.1 1 W - 3 W

- 5.1.2 3 W - 10 W

- 5.1.3 Above 10 W

- 5.2 By Architecture

- 5.2.1 Single-die Packages (SMD / Discrete)

- 5.2.2 Multi-die Packages (SMD)

- 5.2.3 COB (Chip-on-Board)

- 5.2.4 Others

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

- 5.4 By Country

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 ams OSRAM International GmbH

- 6.4.3 Lumileds Holding B.V.

- 6.4.4 Cree LED Inc.

- 6.4.5 Seoul Semiconductor Co., Ltd.

- 6.4.6 Samsung Electronics Co., Ltd.

- 6.4.7 LG Innotek Co., Ltd.

- 6.4.8 Everlight Electronics Co., Ltd.

- 6.4.9 Citizen Electronics Co., Ltd.

- 6.4.10 Bridgelux Inc.

- 6.4.11 Luminus Devices Inc.

- 6.4.12 Epistar Corporation

- 6.4.13 Toyoda Gosei Co., Ltd.

- 6.4.14 NationStar Optoelectronics Co., Ltd.

- 6.4.15 Hongli Zhihui Group Co., Ltd.

- 6.4.16 Sanan Optoelectronics Co., Ltd.

- 6.4.17 Signify N.V.

- 6.4.18 LITE-ON Technology Corporation

- 6.4.19 Broadcom Inc.

- 6.4.20 Foshan Refond Optoelectronics Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment