|

시장보고서

상품코드

2064492

의료 분야 인재 분석 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)People Analytics In Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

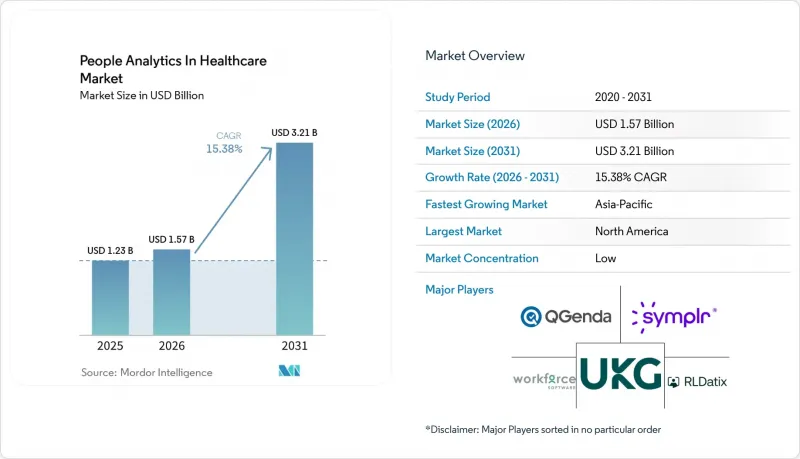

Mordor Intelligence에 의하면, 의료 분야 인재 분석 시장은 2025년 12억 3,000만 달러로 평가되었고, 2026년 15억 7,000만 달러로 추정되고, 2031년까지 32억 1,000만 달러로 확대될 전망이며, 2026-2031년 CAGR 15.38%를 나타낼 것으로 예측됩니다.

본 보고서는 구성 요소별(소프트웨어 및 서비스), 배포 모델별(클라우드 기반, 온프레미스형, 기타), 기업 규모별(대규모 의료 시스템, 기타), 솔루션 모듈별(인력 관리 및 스케줄링 분석, 기타), 최종 사용자별(병원 및 의료 시스템, 재택치료 기관, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 의료 분야 인재 분석 시장 동향 및 인사이트

의료 인건비 부담 증가

의료 분야의 인력 분석 시장은 현재, 의료 제공 기관 전체의 재무 재건 계획에서 인건비가 핵심적인 위치를 차지하고 있다는 사실로부터 혜택을 보고 있습니다. 2025년, 미국 병원의 총 경비 중 인건비가 60%를 차지했으며, 총 인건비는 1조 달러를 넘어 전년 대비 5.6% 증가하여 병원 물가 상승률을 상회했습니다. 미국의 병원 인건비는 2023년 4분기부터 2025년 4분기까지 10.1% 증가한 반면, 조정된 환자 1인당 복리후생비는 같은 기간 동안 12% 증가했습니다. 대규모 의료 시스템에서는 더욱 큰 압박을 받고 있으며, 순영업수익이 10억 달러를 넘는 기관의 경우 복리후생비만으로도 16% 증가가 보고되고 있습니다. 상환액 증가세와 임금 인플레이션 간의 이러한 괴리로 인해, 의료 시스템은 교대 단위 생산성 분석, 고비용 인력 감축, 플로트 풀 최적화 방향으로 나아가고 있습니다. 이것들은 의료 분야 인재 분석 시장에서 주로 활용되는 사례들입니다. 병원 재무 책임자의 절반이 2026년의 최우선 과제로 인건비를 꼽았으며, 이는 단순히 인사 보고의 한 차원으로 그치는 것이 아니라, 재무 관리 도구로서의 인력 분석에 대한 지속적인 투자를 뒷받침하는 것입니다.

임상 인력의 만성적인 부족과 번아웃

의료 분야 인재 분석 시장은 여러 직종에 걸친 임상 의사의 지속적인 부족으로 인해 혜택을 보고 있습니다. 예측에 따르면, 2037년까지 풀타임 환산 기준으로 18만 7,130명의 의사가 부족하고, 30만 2,440개의 LPN(준간호사) 자리가 채워지지 않을 것으로 보이며, 이는 36%의 부족분에 해당합니다. 2029년까지 간호직 종사자의 약 40%가 퇴직하거나 은퇴할 의사를 밝혔으며, 이 중 41.5%는 주요 이유로 스트레스와 번아웃을 꼽았습니다. 번아웃으로 인한 이직은 의료 시스템에 간호사 1명당 연간 최소 3만 6,918달러의 대체 비용을 발생시키는 것으로 추정되며, 이는 인재 유지와 참여도 분석의 중요성을 다시 한번 뒷받침해 줍니다. 전 세계 간호사 부족 규모는 2030년까지 410만 명으로 줄어들 것으로 예상되는데, 이는 공급 압력이 의료 분야 인재 분석 시장에서 장기적인 수요 요인으로 계속 작용할 것임을 시사합니다. 그 결과, 의료 제공업체들은 예측적 이직 추적, 인력 배치의 회복탄력성 분석, 번아웃 모니터링을 노동 효율성과 마찬가지로 돌봄의 지속성을 뒷받침하는 업무 역량으로 간주하고 있습니다.

직원 데이터 및 급여 데이터와 관련된 데이터 개인정보 보호 및 사이버 보안 위험

의료 분야 인재 분석 시장 도입에 있어, 인력 관리 플랫폼이 기밀성이 높은 직원 데이터, 급여 데이터, 자격 정보를 단일 환경에 통합한다는 점 때문에 큰 제약이 발생하고 있습니다. 의료 분야의 급여·인사 서비스 제공업체를 대상으로 한 사이버 공격은 2년 동안 400% 증가했으며, 제3자 서비스 제공업체에 의한 정보 유출은 2019년 상반기 10%에서 2023년 상반기 21%로 상승했습니다. 이러한 사고들은 건당 평균 30만 4,191명에게 영향을 미치고 있으며, 이것이 조달 팀이 인력 기술 및 공급업체에 대한 심사를 강화하고 있는 이유 중 하나입니다. 의료 분야 인재 분석 시장에서 이는 보안 심사가 더욱 철저해지고, 하청업체에 대한 감독이 더욱 세밀해지며, 구매 결정 시 공급업체에 대한 접근 통제가 더욱 중요시되고 있음을 의미합니다. 또한, 의료 서비스 제공업체들은 현재 여러 소프트웨어 계층이 직원 정보에 접근하는 경우, 규정 준수(BAA)에 부합하는 업무 제휴 계약을 체결하더라도 공급망상의 위험이 완전히 배제되지 않는다는 점을 인식하고 있습니다. 이러한 보안상의 부담은 도입을 막는 요인은 아니지만, 계약 절차를 지연시키고, 강력한 보안 거버넌스와 깔끔한 통합 아키텍처를 갖춘 공급업체의 중요성을 더욱 부각시키고 있습니다.

부문별 분석

2025년 기준으로 소프트웨어는 구성 요소별 부문에서 64.37%를 차지했으며, 의료 분야 인재 분석 시장에서 구성 요소별 최대 시장 점유율을 기록했습니다. 이러한 우위는 스케줄링 엔진, 정착률 모델, 규정 준수 대시보드, 예측 도구가 의료 기관의 인력 관련 의사 결정의 핵심을 이루는 시스템 계층을 구성하고 있다는 사실을 반영하고 있습니다. 많은 의료 기관에서 소프트웨어는 거점, 부서, 임상 의사 그룹 전체에 걸쳐 인력 현황을 표준화하는 최초의 실용적인 수단이 되었습니다. 또한, 소프트웨어 기반에는 정기적인 구독 모델, 신속한 업데이트 주기, 서비스만으로는 제공할 수 없는 급여 계산 및 인사 기록과의 긴밀한 연동과 같은 장점이 있습니다. 의료 분야 인재 분석 시장이 성숙해짐에 따라, 의료 기관들은 일반적으로 자문 및 최적화 지원 서비스를 확대하기 전에 플랫폼을 구매하기 때문에 소프트웨어는 여전히 도입의 출발점 역할을 하고 있습니다.

서비스 시장은 2026-2031년 연평균 성장률(CAGR) 16.47%로 확대될 것으로 예상되며, 소프트웨어 시장 규모는 여전히 크지만 가장 빠르게 성장하는 부문이 될 전망입니다. 이는 많은 의료 시스템이 라이선스 외에도 도입, 벤치마킹, 교육, 모델 조정 지원을 요구하게 됨에 따라 구매자의 행동에 뚜렷한 변화가 나타나고 있음을 반영합니다. 2026년에는 병원 재무 책임자의 절반이 생산성 거버넌스와 인력 벤치마킹을 최우선 과제로 삼고 있으며, 이러한 목표를 달성하기 위해서는 일반적으로 일회성 시스템 도입이 아닌 지속적인 자문 지원이 필요합니다. 중서부의 한 의료 시스템에서는 분석 중심의 지속 가능한 인재 프로그램을 통해 3년 만에 직원들의 순추천지수(NPS)를 향상시켰으며, 직원의 평균 근속 연수를 업계 평균의 3-4배 수준으로 유지했습니다. 이러한 경향은 의료 분야 인재 분석 시장에서 ‘소프트웨어 플러스 서비스’ 하이브리드 모델의 타당성을 뒷받침하고 있습니다. 이 시장에서는 플랫폼 데이터를 측정 가능한 고객 유지율, 생산성, 인력 배치 성과로 전환하는 실행 지원에 대해 구매자들이 점점 더 많은 대가를 지불하고 있습니다.

2025년, 의료 분야 인재 분석 시장에서 클라우드 기반 도입이 69.41%를 차지했으며, 주요 도입 모델로 자리 잡았습니다. 의료 시스템이 클라우드 플랫폼을 선호한 이유는 온프레미스 인프라의 부담을 줄이고, 여러 거점에 대한 가시성을 확보하며, 공급업체가 신속하게 업데이트를 제공할 수 있도록 하기 위해서입니다. 또한, 클라우드를 통한 서비스 제공은 대부분의 경우 서로 다른 시스템에 분산되어 있는 일정 관리, 급여 계산, 자격 인증, 직원 참여도 등 각 계층에 걸친 데이터를 통합해야 하는 요구 사항에도 부합합니다. 클라우드의 장점은 구매자들이 현재 대규모 인재 분석 분야에서 SaaS 기반 서비스를 가장 효율적인 방법으로 간주하고 있음을 보여줍니다. 또한, 이는 의료 분야 인재 분석 시장에서 정기적인 수동 보고서 작성 대신 지속적인 분석을 지원하는 운영 모델로 전환되는 광범위한 추세를 반영하고 있습니다.

하이브리드 시장 규모는 2026-2031년 연평균 성장률(CAGR) 17.63%로 성장할 것으로 전망됩니다. 이는 많은 조직이 레거시 시스템에서 완전한 클라우드 네이티브 아키텍처로 단번에 전환하고 있는 것은 아니라는 점을 보여줍니다. 대신, 온프레미스 EHR(전자건강기록) 및 HR(인사) 시스템을 유지하면서, 기존 환경 전반에 걸친 데이터를 통합·분석할 수 있는 클라우드 분석 계층을 추가하고 있습니다. 새로운 플랫폼은 그동안 분리되어 있던 인사, 급여, 일정 관리 데이터를 통합 모델로 연결함으로써, 하이브리드 대응 아키텍처가 왜 전략적 가치를 높이고 있는지를 보여주고 있습니다. 각국의 보건 당국 또한 인프라를 완전히 교체하는 것이 아니라 단계적인 도입 과정을 통해 노동력의 디지털화를 추진할 수 있음을 보여주고 있습니다. 데이터 기밀성이 높은 환경에서는 온프레미스 구축이 여전히 중요하지만, 의료 분야 인재 분석 시장은 모든 레거시 시스템에 즉각적인 변경을 강요하지 않으면서도 클라우드의 유연성을 추구하는 구매자들에 의해 점점 더 형성되고 있습니다.

지역별 분석

2025년, 북미는 의료 분야 인재 분석 시장 점유율의 38.43%를 차지하며 최대 지역 시장이 되었습니다. 해당 지역이 주도적인 위치를 차지하고 있는 것은 대규모 통합 의료 제공 네트워크, 탄탄한 벤더 생태계, 인력 배치의 투명화에 대한 규제 압력 증가가 복합적으로 작용한 결과이며, 이것이 주요 요인으로 꼽힙니다. 최소 인력 배치 기준에 따라, 장기 요양 서비스 제공업체에게 인력 보고는 이미 최우선 과제가 되고 있으며, 주법에 따라 이러한 요건이 병원 환경으로도 확대되고 있습니다. 벤더 시장 침투율도 높아, 미국 최대 의료 시스템의 90% 가까이가 주요 인재 분석 솔루션을 도입하고 있으며, 주요 공급업체에 따르면 4,500개 이상의 의료 기관이 이를 도입하고 있습니다. 이러한 높은 성숙도 덕분에 북미 의료 분야 인재 분석 시장은 기본적인 도입 단계에서 더 심층적인 통합, AI를 활용한 예측, 거버넌스를 중시하는 보고 단계로 점차 전환되고 있습니다.

유럽은 의료 분야 인재 분석 시장에 있어 전략적으로 중요한 두 번째 지역으로 자리매김하고 있습니다. 이는 인재 보고서와 공공 부문의 인력 배치 감독이 점차 제도화되고 있기 때문입니다. 프랑스의 전국적인 인력 보고서 체계는 공립 병원 시설 전체에 걸쳐 171개의 지표를 포괄하고 있으며, 재현성이 높고 감사에 대응할 수 있는 인력 보고서를 작성할 수 있는 시스템에 대한 수요를 뒷받침하고 있습니다. 2025년 유럽 정책 검토 보고서에 따르면, EU 회원국 33개국 중 23개국이 안전한 인력 배치에 관한 법률 또는 공식 정책을 보유하고 있었으나, 국가가 승인한 인력 배치 조사 기법을 채택한 국가는 9개국에 불과하여, 계획적 접근 방식을 표준화할 수 있는 분석 도구의 도입 여지가 남아 있습니다. 스위스의 전국적인 간호 인력 모니터링 이니셔티브 역시, 인력 분석 결과가 병원 경영의 의사결정뿐만 아니라 공공 정책 지원에도 점점 더 큰 기대를 받고 있음을 보여주고 있습니다. 따라서 이 지역에서는 인재 분석을 공식 보고서, 안전한 인력 배치 방안, 지역 데이터 거버넌스 요건과 연계할 수 있는 공급업체에 대한 안정적인 수요가 예상됩니다.

아시아태평양은 2026-2031년 연평균 성장률(CAGR) 17.89%를 기록하며 성장할 것으로 예상되며, 의료 분야 인재 분석 시장에서 가장 두드러진 성장을 보일 지역이 될 것입니다. 세계 평균으로 볼 때 인구 1만 명당 37.1명의 간호사가 배치되어 있지만, 고소득 국가와 저소득 국가 간에는 10배의 격차가 존재하며, 의료 시스템 전반에 걸쳐 인력 부족은 여전히 구조적인 과제로 남아 있습니다. 이러한 격차로 인해 고령화와 의료 종사자 공급 불균형을 배경으로 수요가 증가하는 가운데, 의료 기관들은 계획 수립, 정착률 추적, 인력 배치를 자동화해야 하는 상황에 직면해 있습니다. 의료 서비스가 확대되고 있는 지역에서는 비즈니스 기회가 가장 크지만, 인력 계획은 여전히 기본적인 업무 보고에서 예측 분석으로 전환되는 단계에 있습니다. 남미에서는 도입이 아직 초기 단계이지만, 거버넌스 개혁과 체계적인 인재 계획에 대한 필요성이 미래 수요를 위한 기반을 마련해 가고 있습니다. 중동에서도 의료 체계 확충 및 현지 인력 양성 프로그램을 통해 관심이 집중되고 있습니다. 한편, 아프리카는 여전히 초기 단계의 기회이며, 상업적 잠재력은 도시 지역의 민간 의료 시장에 집중되어 있습니다. 이 지역 전반에 걸쳐 의료 분야의 인력 분석 시장은 인력 배치에 대한 압박과 통합된 인력 데이터를 뒷받침할 수 있는 충분한 디지털 인프라를 겸비한 조직을 중심으로 먼저 확대될 것으로 보입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

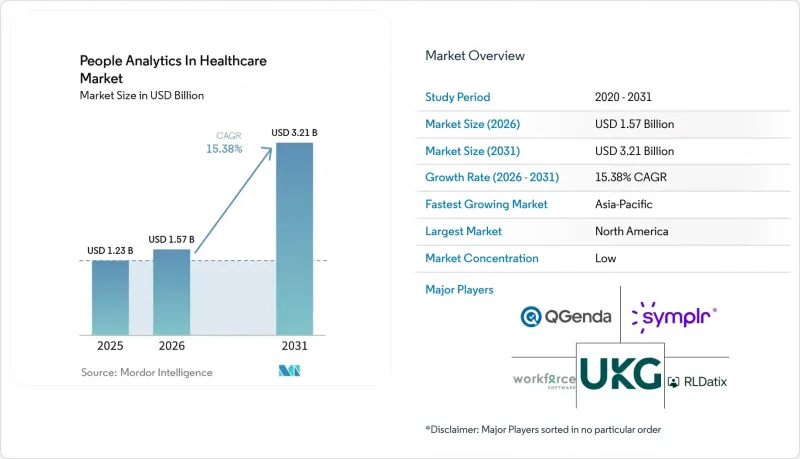

AJY 26.06.26According to Mordor Intelligence, the people analytics market in healthcare is projected to expand from USD 1.23 billion in 2025 and USD 1.57 billion in 2026 to USD 3.21 billion by 2031, registering a CAGR of 15.38% between 2026 and 2031.

This report is Segmented by Component (Software, and Services), Deployment Model (Cloud-Based, On-Premises, and More), Enterprise Size (Large Healthcare Systems, and More), Solution Module (Workforce Management and Scheduling Analytics, and More), End User (Hospitals and Health Systems, Home Healthcare Agencies, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global People Analytics In Healthcare Market Trends and Insights

Rising Healthcare Labor Cost Pressures

The people analytics in the healthcare market is benefiting from the fact that labor now sits at the center of financial recovery plans across provider organizations. Workforce costs accounted for 60% of total U.S. hospital expenses in 2025, and aggregate labor spending exceeded USD 1 trillion, up 5.6% and outpacing hospital price growth. U.S. hospital labor expenses rose 10.1% between Q4 2023 and Q4 2025, while benefits expense per adjusted patient day increased 12% over the same period. Larger systems carried even more pressure, with organizations above USD 1 billion in net operating revenue reporting 16% growth in benefits costs alone. This gap between reimbursement growth and wage inflation is pushing health systems toward shift-level productivity analysis, premium labor reduction, and float pool optimization, which are core use cases for people analytics in the healthcare market. Half of hospital finance leaders identified labor as a top 2026 priority, supporting continued investment in workforce analytics as a financial control tool rather than solely an HR reporting layer.

Persistent Clinical Workforce Shortages and Burnout

People analytics in the healthcare market is also benefiting from the continued shortage of clinicians across multiple workforce categories. Projections show a shortfall of 187,130 full-time equivalent physicians by 2037, and 302,440 LPN positions, equal to a 36% shortage, will go unfilled. By 2029, nearly 40% of the nursing workforce intends to leave or retire, with 41.5% citing stress and burnout as the main reason. Burnout-driven attrition is estimated to cost healthcare systems at least USD 36,918 per nurse each year in replacement costs, further strengthening the case for retention and engagement analytics. The global nursing shortage is expected to narrow only to 4.1 million by 2030, indicating that supply pressure will remain a long-term demand driver for people analytics in the healthcare market. As a result, providers are treating predictive turnover tracking, staffing resilience analysis, and burnout monitoring as operational capabilities that support continuity of care as much as labor efficiency.

Data Privacy and Cybersecurity Risks in Employee and Payroll Data

People analytics in the healthcare market faces a significant adoption constraint because workforce platforms consolidate sensitive employee, payroll, and credential data in a single environment. Healthcare payroll and HR vendor-related cyberattacks increased 400% over two years, while third-party vendor breaches rose from 10% in H1 2019 to 21% in H1 2023. These incidents affected an average of 304,191 individuals per breach, which helps explain why procurement teams are increasing scrutiny of workforce technology vendors. In the people analytics in healthcare market, this means security reviews are becoming more thorough, subcontractor oversight is becoming more detailed, and vendor access controls are receiving greater weight in purchase decisions. Providers also now recognize that a compliant Business Associate Agreement does not remove supply-chain exposure when multiple software layers touch employee information. This security burden does not stop adoption, but it does slow deal cycles and increase the importance of vendors with strong security governance and cleaner integration architectures.

Other drivers and restraints analyzed in the detailed report include:

- Growing Need for Regulatory Compliance and Safe Staffing Visibility

- Accelerating Cloud-Based Workforce Platform Adoption

- Complex Integration With EHR, Payroll, and Legacy HRIS Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 64.37% of the component segment in 2025, giving it the largest market share within the people analytics in healthcare market by component. This dominance reflects the fact that scheduling engines, retention models, compliance dashboards, and forecasting tools comprise the core system layer for workforce decision-making in healthcare organizations. In many provider settings, software became the first practical way to standardize labor visibility across sites, departments, and clinician groups. The software base also benefits from recurring subscription models, faster update cycles, and tighter integration with payroll and HR records than service-only engagements can provide. As the people analytics in the healthcare market has matured, software has remained the starting point for adoption because providers generally buy a platform before they scale advisory or optimization support.

Services are projected to expand at a 16.47% CAGR during 2026-2031, making them the fastest-growing component, even though software remains larger. This reflects a clear shift in buyer behavior, because many health systems now want implementation, benchmarking, training, and model-tuning support alongside their licenses. In 2026, half of hospital finance leaders prioritized productivity governance and labor benchmarking, and those goals usually require continuous advisory support rather than a one-time system launch. One Midwest health system improved employee net promoter scores over 3 years and maintained average staff tenure at 3-4 times the industry norm through a sustained analytics-led workforce program. That pattern supports hybrid software-plus-services models inside the people analytics in healthcare market, where buyers increasingly pay for execution support that helps turn platform data into measurable retention, productivity, and staffing outcomes.

Cloud-based deployment accounted for 69.41% of the people analytics market in healthcare in 2025, making it the leading deployment model. Health systems favored cloud platforms because they reduce local infrastructure burden, support multi-site visibility, and let vendors deliver updates faster. Cloud delivery also aligns with the need to unify data across scheduling, payroll, credentialing, and workforce engagement layers that are often spread across separate systems. The dominance of cloud shows that buyers now see SaaS delivery as the most efficient path for workforce analytics at scale. It also reflects the broader movement in the healthcare people analytics market toward operating models that support continuous analytics rather than periodic manual reporting.

Hybrid deployment is projected to grow at a 17.63% CAGR during 2026-2031, which indicates that many organizations are not moving in a single step from legacy systems to fully cloud-native architectures. Instead, they are keeping on-premises EHR or HR systems in place while adding cloud analytics layers that can federate and analyze data across existing environments. New platforms illustrate why hybrid-ready architectures are gaining strategic value by connecting previously separated HR, pay, and scheduling data into unified models. National health authorities have also shown that workforce digitalization can advance through staged adoption paths rather than complete infrastructure replacement. On-premises deployment remains relevant in data-sensitive environments, but the people analytics market in healthcare is increasingly shaped by buyers who want cloud flexibility without forcing immediate change across every legacy system.

Geography Analysis

North America held 38.43% of the people analytics market share in healthcare in 2025, making it the largest regional market. The region leads because it combines large integrated delivery networks, a dense vendor ecosystem, and rising regulatory pressure on staffing visibility. Minimum staffing rules have already turned workforce reporting into a high-priority issue for long-term care providers, and state legislation is extending similar expectations into hospital settings. Vendor penetration is also deep, with nearly 90% of the largest U.S. healthcare systems using leading workforce analytics solutions, and more than 4,500 healthcare organizations reported by major providers. This maturity means the people analytics in the healthcare market in North America is moving from basic adoption toward deeper integration, AI-enabled forecasting, and governance-focused reporting.

Europe remains a strategically important second-tier region for people analytics in the healthcare market because workforce reporting and public-sector staffing oversight are becoming more formalized. France's national workforce reporting framework covers 171 indicators across public hospital establishments, supporting demand for systems that can produce repeatable, audit-ready workforce reporting. A 2025 European policy review found that 23 of 33 EU member countries had legislation or formal policy on safe staffing, but only 9 used a nationally approved staffing calculation methodology, leaving room for analytics tools that can standardize planning approaches. Switzerland's national nursing staff monitoring initiative also shows that workforce analytics outputs are increasingly expected to support public policy, not only hospital management decisions. The region, therefore, offers steady demand for vendors that can align workforce analytics with public reporting, safe staffing policy, and local data governance requirements.

Asia-Pacific is projected to grow at a 17.89% CAGR during 2026-2031, which makes it the fastest-growing region in the people analytics in healthcare market. The global average stood at 37.1 nurses per 10,000 population, with a tenfold gap between high-income and low-income countries, and workforce shortages remain a structural issue across health systems. This gap is pushing providers to automate planning, retention tracking, and skills deployment as demand rises amid an aging population and uneven clinician supply. The commercial opportunity is strongest where healthcare delivery is expanding, but workforce planning is still moving from basic operational reporting toward predictive analytics. South America is still earlier in adoption, but governance reforms and institutional workforce planning needs are creating a foundation for future demand. The Middle East is also generating interest through healthcare capacity expansion and workforce localization programs, while Africa remains an early-stage opportunity with commercial potential concentrated in more urbanized private care markets. Across these regions, the people analytics in the healthcare market will expand first in organizations that can combine staffing pressure with enough digital infrastructure to support integrated workforce data.

- QGenda, LLC

- symplr software LLC

- UKG Inc.

- WorkForce Software, LLC

- RLDatix Holdings Limited

- Quinyx AB

- HUMANFORCE PTY LTD

- OnShift, Inc.

- Shiftboard, Inc.

- Visier, Inc.

- One Model Inc.

- Orgvue Limited

- Deputechnologies Pty Ltd

- Dayforce, Inc.

- Laudio, Inc.

- Axuall, Inc.

- Clinician Nexus, Inc.

- HRBench, Inc.

- SmartLinx Solutions LLC

- Connecteam Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Healthcare Labor Cost Pressures

- 4.2.2 Persistent Clinical Workforce Shortages and Burnout

- 4.2.3 Growing Need for Regulatory Compliance and Safe Staffing Visibility

- 4.2.4 Accelerating Cloud-Based Workforce Platform Adoption

- 4.2.5 Expansion of Internal Float Pools and Skills-Based Deployment Analytics

- 4.2.6 Real-Time Clinician Credential Data Networks Improving Workforce Planning

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Cybersecurity Risks in Employee and Payroll Data

- 4.3.2 Complex Integration with EHR, Payroll, and Legacy HRIS Systems

- 4.3.3 Algorithmic Bias and HR AI Governance Scrutiny

- 4.3.4 Employee Monitoring Backlash in Clinical Workflows

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Healthcare Systems

- 5.3.2 Mid-Sized Healthcare Organizations

- 5.3.3 Small Healthcare Providers

- 5.4 By Solution Module

- 5.4.1 Workforce Management and Scheduling Analytics

- 5.4.2 Labor Cost, Time and Attendance Analytics

- 5.4.3 Talent Acquisition, Retention and Internal Mobility Analytics

- 5.4.4 Learning, Skills and Workforce Capability Analytics

- 5.4.5 Workforce Productivity and Performance Analytics

- 5.4.6 Employee Engagement and Burnout Analytics

- 5.4.7 Compliance and Workforce Risk Analytics

- 5.4.8 Predictive Workforce Intelligence and Forecasting

- 5.5 By End User

- 5.5.1 Hospitals and Health Systems

- 5.5.2 Clinics and Ambulatory Care Centers

- 5.5.3 Long-Term Care and Skilled Nursing Facilities

- 5.5.4 Home Healthcare Agencies

- 5.5.5 Senior Living and Assisted Living Facilities

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Netherlands

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 QGenda, LLC

- 6.4.2 symplr software LLC

- 6.4.3 UKG Inc.

- 6.4.4 WorkForce Software, LLC

- 6.4.5 RLDatix Holdings Limited

- 6.4.6 Quinyx AB

- 6.4.7 HUMANFORCE PTY LTD

- 6.4.8 OnShift, Inc.

- 6.4.9 Shiftboard, Inc.

- 6.4.10 Visier, Inc.

- 6.4.11 One Model Inc.

- 6.4.12 Orgvue Limited

- 6.4.13 Deputechnologies Pty Ltd

- 6.4.14 Dayforce, Inc.

- 6.4.15 Laudio, Inc.

- 6.4.16 Axuall, Inc.

- 6.4.17 Clinician Nexus, Inc.

- 6.4.18 HRBench, Inc.

- 6.4.19 SmartLinx Solutions LLC

- 6.4.20 Connecteam Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment