|

시장보고서

상품코드

2057474

헬스케어 분석 시장 : 컴포넌트별, 도입 모델별, 유형별, 용도별, 최종사용자별, 지역별 - 예측(-2030년)Healthcare Analytics Market by Type, Application (Claim, RCM, Fraud, Precision Health, RWE, Imaging, Supply Chain, Workforce, Population Health), End User (Payer, Hospital, ACO, ASC), AI, Market Insights, Trends - Forecast to 2030 |

||||||

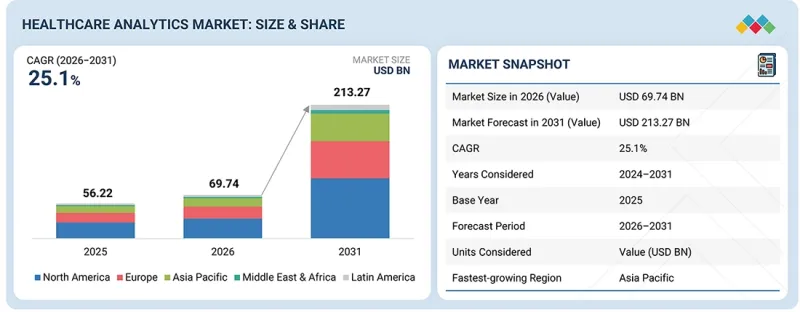

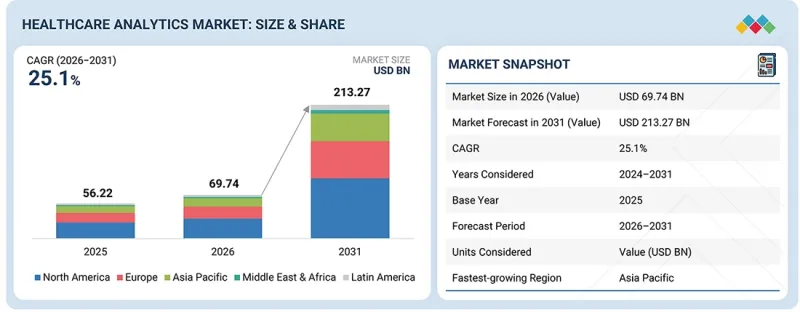

헬스케어 분석 시장 규모는 2025년 555억 2,000만 달러에서 2030년까지 1,666억 5,000만 달러로 성장하고, 예측 기간 중 연평균 복합 성장률(CAGR)은 24.6%를 나타낼 전망입니다.

전자건강기록(EHR)의 도입이 헬스케어 분석 시장의 성장을 견인하고 있습니다. 북미에서는 개업의와 연방 정부 관할 외의 급성기 병원이 EHR 시스템을 도입하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 컴포넌트별, 도입 모델별, 유형별, 용도별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카. |

‘경제 및 임상 보건을 위한 의료 정보 기술법(HITECH법)’을 통해, 전자건강기록(EHR) 시스템을 지원하기 위한 정부의 인센티브가 제공되고 있습니다. 이 시장을 견인하는 요인으로는 인공지능의 발전, 가치 기반 의료 시스템, 실세계 데이터는 물론, 의료 보험사, 의료 제공업체, 생명과학 기업 및 급성기 이후 의료 기관들의 헬스케어 분석 서비스에 대한 관심 등을 들 수 있습니다.

“용도별로는 예측 기간 동안 임상 분석 부문이 가장 높은 성장률을 보일 것으로 예측됩니다. '

용도별로 보면, 헬스케어 분석 시장은 재무 분석, 임상 분석, 업무·관리 분석, 그리고 인구 건강 분석으로 구분됩니다. 임상 분석 부문은 AI를 활용한 임상 의사결정 지원, 예측 위험 모델링, 그리고 실시간 환자 인사이트의 도입 확대에 힘입어 예측 기간 동안 가장 높은 성장률을 보일 것으로 전망됩니다. 이는 치료 성과 향상, 재입원 감소, 그리고 의료 제공업체 및 의료 시스템 전반에 걸친 가치 기반 치료 노력을 지원하기 위한 것입니다.

구성 요소별로는 예측 기간 동안 서비스 부문이 가장 높은 성장률을 보일 것으로 전망됩니다. '

구성 요소별로 보면, 헬스케어 분석 시장은 소프트웨어 및 서비스로 분류됩니다. 예측 기간 동안 임상 분석 부문이 가장 높은 성장률을 보일 것으로 전망됩니다. 이는 의료 기관들이 상호 운용성, 규정 준수 및 가치 실현까지의 시간 단축을 확보하면서 복잡한 AI 및 클라우드 기반 분석 플랫폼을 도입하려는 과정에서 구현, 시스템 통합, 데이터 관리 및 고급 분석 컨설팅에 대한 수요가 증가하고 있기 때문입니다.

“APAC 지역은 예측 기간 동안 가장 높은 연평균 성장률(CAGR)을 보일 것으로 추정됩니다. '

헬스케어 분석 시장은 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카로 분류됩니다. 아시아태평양의 헬스케어 분석 시장은 예측 기간 동안 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 이는 의료 제공업체와 보험사에서의 전자건강기록(EHR)의 급속한 보급, 클라우드 네이티브 도입, 그리고 AI/ML의 도입이 주도하고 있습니다. 정부 주도의 디지털 헬스 프로그램과 데이터 상호운용성 기준의 개선에 힘입어, 인구 건강 분석, 실세계 데이터(REW), 예측 모델링의 활용이 증가하고 있으며, 중국, 인도, 일본 및 동남아시아 전역에서 대규모 분석 도입이 가속화되고 있습니다.

Merative(미국), Optum, Inc.(미국), SAS Institute Inc.(미국), Oracle(미국), Citiustech Inc.(미국)은 헬스케어 분석 시장의 주요 기업 중 일부입니다.

본 조사에서는 헬스케어 분석 시장의 주요 기업들에 대해 기업 프로파일, 최근 동향 및 주요 시장 전략을 포함한 상세한 경쟁 분석을 수행하고 있습니다.

조사 범위

본 보고서는 헬스케어 분석 시장을 분석했습니다. 구성 요소, 유형, 용도, 최종 사용자, 지역을 기준으로 각 시장 부문 시장 규모와 향후 성장 잠재력을 추정하는 것을 목적으로 합니다. 또한, 본 보고서에서는 이 시장의 주요 기업에 대해 기업 프로파일, 제품 라인업, 최근 동향, 주요 시장 전략과 더불어 경쟁사 분석도 제공합니다.

이 보고서를 구매해야 하는 이유

본 보고서는 헬스케어 분석 시장 및 그 하위 부문의 매출에 대한 가장 정확한 추정치를 제공함으로써, 이 시장의 선도 기업과 신규 진출기업을 지원합니다. 본 보고서는 이해관계자들이 경쟁 구도를 파악하고, 자사의 비즈니스를 더 유리한 위치에 놓으며, 적절한 시장 진출 전략을 수립하는 데 필요한 추가적인 인사이트를 얻는 데 도움이 됩니다. 또한, 본 보고서는 이해관계자들이 시장 동향을 파악하는 데 도움을 주며, 주요 시장 성장 촉진요인, 억제요인, 과제 및 기회에 대한 정보를 제공합니다.

본 보고서에서는 다음 사항에 대한 인사이트를 제공합니다.

- 주요 촉진요인(전자건강기록(EHR) 도입을 위한 정부의 적극적인 노력, 스타트업에 대한 벤처 캐피털 투자 증가, 의료비 절감의 필요성, 실세계 데이터(REW)에 대한 관심 증가, 원격의료 및 원격 환자 모니터링의 부상, 규제 준수에 대한 관심 증가), 제약 요인(분석 솔루션의 높은 비용, 데이터 유출에 대한 우려 증가), 기회(가치 기반 의료에 대한 관심 증가, 의료 분야에서의 분석 활용 확대, 환자 레지스트리 증가, 소셜 미디어 및 디지털 헬스 기술의 부상), 그리고 과제(부정확하고 일관성 없는 데이터에 대한 우려, 개발도상국에서의 헬스케어 분석 솔루션 도입에 대한 소극적 태도, 의료 기록 유지 관리의 미비, 숙련된 인력 부족)에 대해, 헬스케어 분석 시장의 성장에 영향을 미치는 요인으로 분석했습니다.

- 제품 개발 및 혁신 : 헬스케어 분석 시장의 향후 기술, 연구 개발 활동, 그리고 신제품 및 서비스 출시에 관한 심층적인 인사이트

- 시장 개발: 수익성이 높은 시장에 대한 종합적인 정보. 본 보고서에서는 다양한 지역에 걸친 헬스케어 분석 시장을 분석했습니다.

- 시장의 다각화 : 헬스케어 분석 시장의 신제품 및 서비스, 미개척 지역, 최근 동향, 그리고 투자에 관한 종합적인 정보

- 경쟁사 분석 : Merative(미국), Optum, Inc.(미국), SAS Institute Inc.(미국), Oracle(미국), Citiustech Inc.(미국), Inovalon(미국), McKesson Corporation(미국), MedeAnalytics, Inc.(미국), Cotiviti, Inc.(미국), Exlservice Holdings, Inc.(미국), Wipro(인도) 등, 헬스케어 분석 시장의 주요 시장 진출기업에 대해 시장 점유율, 성장 전략, 서비스 제공 내용에 관한 상세한 평가를 수행합니다

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI의 영향, 특허, 혁신, 그리고 향후 응용

제7장 규제 상황

제8장 고객 현황과 구매 행동

제9장 헬스케어 분석 시장(컴포넌트별)

제10장 헬스케어 분석 시장(도입 모델별)

제11장 헬스케어 분석 시장(유형별)

제12장 헬스케어 분석 시장(용도별)

제13장 헬스케어 분석 시장(최종사용자별)

제14장 헬스케어 분석 시장(지역별)

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

LSHThe healthcare analytics market is expected to grow from USD 55.52 billion in 2025 to USD 166.65 billion by 2030, with a CAGR of 24.6% during the forecast period. The adoption of Electronic Health Records (EHR) is propelling the healthcare analytics market forward. In North America, office-based physicians and non-federal acute care hospitals have adopted EHR systems.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Component, Type, Application and End-user |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and Middle East Africa. |

There are government incentives available to support EHR systems through the Health Information Technology for Economic and Clinical Health Act. The forces that drive this market include advancements in artificial intelligence, value-based healthcare systems, real-world data, as well as interest in healthcare analytical services by healthcare payers, providers, life sciences companies, and post-acute organizations.

"By application, clinical analytics segment is expected to witness the highest growth during the forecast period."

Based on application, the healthcare analytics market is segmented into financial analytics, clinical analytics, operations & administrative analytics, and population health analytics. The clinical analytics segment is growing at the fastest rate during the forecast period driven by increasing adoption of AI-enabled clinical decision support, predictive risk modeling, and real-time patient insights to improve care outcomes, reduce readmissions, and support value-based care initiatives across providers and health system.

By component, services segment to witness the highest growth during the forecast period."

Based on component, the healthcare analytics market is segmented into software and services. The clinical analytics segment is growing at the fastest rate during the forecast period driven by rising demand for implementation, system integration, data management, and advanced analytics consulting as healthcare organizations seek to deploy complex AI- and cloud-based analytics platforms while ensuring interoperability, regulatory compliance, and faster time to value.

"APAC is estimated to register the highest CAGR during the forecast period."

The healthcare analytics market is segmented into North America, Europe, Asia Pacific, Latin America and Middle East and Africa. The healthcare analytics market in Asia Pacific is projected to register the highest CAGR rate during the forecast period. This is driven by rapid EHR penetration, cloud-native deployments, and AI/ML adoption across providers and payers. Increasing use of population health analytics, real-world evidence, and predictive modeling, supported by government-led digital health programs and improving data interoperability standards, is accelerating large-scale analytics implementation across China, India, Japan, and Southeast Asia.

In-depth interviews have been conducted with chief executive officers (CEOs), Directors, and other executives from various key organizations operating in the authentication and brand protection marketplace.

- By Company Type: Tier 1 - 45%, Tier 2 - 35%, and Tier 20%

- By Designation: C-level Executives - 50%, Directors - 30%, and Others - 20%

- By Region: North America- 40%, Europe - 35%, Asia Pacific- 20% and RoW- 5%

Merative (US), Optum, Inc.(US), SAS Institute Inc. (US), Oracle (US), Citiustech Inc (US) are some of the key players in the healthcare analytics market.

The study includes an in-depth competitive analysis of these key players in the healthcare analytics market, with their company profiles, recent developments, and key market strategies.

Research Coverage

The report analyses the healthcare analytics market. It aims to estimate the market size and future growth potential of various market segments based on component, type, application, end-user, and region. The report also provides a competitive analysis of the key players in this market, along with their company profiles, product offerings, recent developments, and key market strategies.

Reasons to buy this report

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the healthcare analytics market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and to plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (favorable government initiatives for electronic health record adoption, growing venture capital investments in startups, need to reduce healthcare costs, increasing focus on real-world evidence, rise of telemedicine and remote patient monitoring, growing focus on regulatory compliance), restraints (hiigh cost of analytics solutions, growing concerns about data breach), opportunities (increasing focus on value-based medicines, growing use of analytics in healthcare, rising number of patient registeries, emergence of social media and digital health technologies), and challenges (concerns regarding inaccurate and inconsistent data, reluctance to adopt healthcare analytics solutions in developing countries, lack of maintenance of medical records, shortage of skilled personnel) influencing the growth of the healthcare analytics market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the healthcare analytics market

- Market Development: Comprehensive information about lucrative markets, the report analyses the healthcare analytics market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the healthcare analytics market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players like Merative (US), Optum, Inc.(US), SAS Institute Inc. (US), Oracle (US), Citiustech Inc (US), Inovalon (US), Mckesson Corporation (US), MedeAnalytics, Inc.(US), Cotiviti, Inc. (US), Exlservice Holdings, Inc. (US), Wipro (India), among others in the healthcare analytics market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING HEALTHCARE ANALYTICS MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN HEALTHCARE ANALYTICS MARKET

- 3.2 NORTH AMERICA: HEALTHCARE ANALYTICS MARKET, BY END USER AND COUNTRY

- 3.3 HEALTHCARE ANALYTICS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Favorable government initiatives for electronic health record adoption

- 4.2.1.2 Growing venture capital investments in startups

- 4.2.1.3 Need to reduce healthcare costs

- 4.2.1.4 Increasing focus on real-world evidence

- 4.2.1.5 Rise of telemedicine and remote patient monitoring

- 4.2.1.6 Growing focus on regulatory compliance

- 4.2.2 RESTRAINTS

- 4.2.2.1 High cost of analytics solutions

- 4.2.2.2 Growing concerns about data breaches

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increasing focus on value-based medicines

- 4.2.3.2 Growing use of analytics in healthcare

- 4.2.3.3 Rising number of patient registries

- 4.2.3.4 Emergence of social media and digital health technologies

- 4.2.4 CHALLENGES

- 4.2.4.1 Concerns regarding inaccurate and inconsistent data

- 4.2.4.2 Reluctance to adopt healthcare analytics solutions in developing countries

- 4.2.4.3 Lack of maintenance of medical records

- 4.2.4.4 Shortage of skilled personnel

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 GDP TRENDS AND FORECAST

- 5.2.2 TRENDS IN GLOBAL HEALTHCARE IT INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE PRICE OF HEALTHCARE ANALYTICS SOLUTIONS, BY COMPONENT

- 5.5.2 INDICATIVE PRICING, BY REGION

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.10 IMPACT OF 2025 US TARIFF - HEALTHCARE ANALYTICS MARKET

- 5.10.1 KEY TARIFF RATES

- 5.10.2 PRICE IMPACT ANALYSIS

- 5.10.3 IMPACT ON COUNTRIES/REGIONS

- 5.10.3.1 US

- 5.10.3.2 Europe

- 5.10.3.3 Asia Pacific

- 5.10.4 IMPACT ON END-USE INDUSTRY

- 5.10.4.1 Healthcare providers

- 5.10.4.1.1 Hospitals & health systems

- 5.10.4.1.2 Physician groups & clinics

- 5.10.4.1.3 Ambulatory surgery centers (ASCs)

- 5.10.4.2 Healthcare payers

- 5.10.4.2.1 Private insurance companies

- 5.10.4.2.2 Government payers

- 5.10.4.3 Pharmacies

- 5.10.4.1 Healthcare providers

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY TECHNOLOGIES

- 6.1.1.1 Big data analytics

- 6.1.1.2 Artificial intelligence and machine learning

- 6.1.1.3 Business intelligence tools

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Cloud computing and data integration platforms

- 6.1.2.2 Interoperability frameworks and APIs

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Cloud computing

- 6.1.3.2 Internet of Things

- 6.1.1 KEY TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.3 PATENT ANALYSIS

- 6.3.1 PATENT PUBLICATION TRENDS FOR HEALTHCARE ANALYTICS MARKET

- 6.3.2 INSIGHTS: JURISDICTION AND TOP APPLICANT ANALYSIS

- 6.4 FUTURE APPLICATIONS

- 6.4.1 AI-DRIVEN PREDICTIVE ANALYTICS AND CLINICAL DECISION SUPPORT

- 6.4.2 REAL-WORLD EVIDENCE (RWE) AND CLINICAL RESEARCH TRANSFORMATION

- 6.4.3 OPERATIONAL INTELLIGENCE AND HEALTHCARE SYSTEM OPTIMIZATION

- 6.5 IMPACT OF AI/GEN AI ON HEALTHCARE ANALYTICS MARKET

- 6.5.1 MARKET POTENTIAL OF AI/GEN AI

- 6.5.2 CASE STUDIES RELATED TO AI/GEN AI IMPLEMENTATION IN HEALTHCARE ANALYTICS MARKET

- 6.5.2.1 AI-driven continuous glucose monitoring and diabetes management

- 6.5.3 IMPACT OF AI/GEN AI ON INTERCONNECTED AND ADJACENT ECOSYSTEMS

- 6.5.3.1 Clinical development & decentralized trials

- 6.5.3.2 Digital biomarkers & endpoint innovation

- 6.5.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN HEALTHCARE ANALYTICS MARKET

- 6.5.4.1 User readiness

- 6.5.4.1.1 User A: Hospitals, clinics & long-term care providers

- 6.5.4.1.2 User B: Pharma and biotech companies

- 6.5.4.2 Impact assessment

- 6.5.4.2.1 User A: Hospitals, clinics & long-term care providers

- 6.5.4.2.1.1 Implementation

- 6.5.4.2.1.2 Impact

- 6.5.4.2.2 User B: Healthcare payers

- 6.5.4.2.2.1 Implementation

- 6.5.4.2.2.2 Impact

- 6.5.4.2.1 User A: Hospitals, clinics & long-term care providers

- 6.5.4.1 User readiness

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 GOVERNMENT REGULATIONS

- 7.1.1.1 US

- 7.1.1.2 Europe

- 7.1.1.3 China

- 7.1.1.4 Japan

- 7.1.1.5 India

- 7.1.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.3 INDUSTRY STANDARDS

- 7.1.1 GOVERNMENT REGULATIONS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM END-USE INDUSTRIES

- 8.4.1 UNMET NEEDS

- 8.4.2 END-USER EXPECTATIONS

- 8.5 MARKET PROFITABILITY

9 HEALTHCARE ANALYTICS MARKET, BY COMPONENT

- 9.1 INTRODUCTION

- 9.2 SERVICES

- 9.2.1 MANAGED SERVICES

- 9.2.1.1 Analytics operations

- 9.2.1.1.1 Continuous performance monitoring reshapes managed analytics delivery models

- 9.2.1.2 Infrastructure & cloud management

- 9.2.1.2.1 Cloud-native infrastructure services underpin healthcare analytics scalability

- 9.2.1.1 Analytics operations

- 9.2.2 PROFESSIONAL SERVICES

- 9.2.2.1 Training & education

- 9.2.2.1.1 Workforce upskilling becomes critical enabler of analytics transformation

- 9.2.2.2 Implementation & integration

- 9.2.2.2.1 Interoperability mandates catalyze complex analytics integration engagements

- 9.2.2.3 Consulting

- 9.2.2.3.1 Strategic data governance consulting unlocks organizational analytics readiness

- 9.2.2.4 Support & maintenance

- 9.2.2.4.1 Post-deployment support sustains long-term analytics performance and compliance

- 9.2.2.1 Training & education

- 9.2.1 MANAGED SERVICES

- 9.3 SOFTWARE

- 9.3.1 POINT ANALYTICS SOLUTIONS

- 9.3.1.1 Targeted problem-solving drives rapid adoption of specialized analytics tools

- 9.3.2 ENTERPRISE-WIDE ANALYTICS PLATFORMS

- 9.3.2.1 Unified data platforms enable cross-continuum analytics at enterprise scale

- 9.3.1 POINT ANALYTICS SOLUTIONS

10 HEALTHCARE ANALYTICS MARKET, BY DEPLOYMENT MODEL

- 10.1 INTRODUCTION

- 10.2 ON-PREMISES

- 10.3 CLOUD-BASED

11 HEALTHCARE ANALYTICS MARKET, BY TYPE

- 11.1 INTRODUCTION

- 11.2 DESCRIPTIVE ANALYTICS

- 11.2.1 INCREASING USE IN PATIENT POPULATION MANAGEMENT AND FINANCIAL MANAGEMENT TO BOOST MARKET

- 11.3 PREDICTIVE ANALYTICS

- 11.3.1 AI-POWERED RISK MODELS TRANSFORM PROACTIVE CLINICAL AND OPERATIONAL PLANNING

- 11.4 PRESCRIPTIVE ANALYTICS

- 11.4.1 NEXT-BEST-ACTION OPTIMIZATION ELEVATES ANALYTICS FROM INSIGHT TO AUTOMATED INTERVENTION

- 11.5 DIAGNOSTIC ANALYTICS

- 11.5.1 ROOT-CAUSE INTELLIGENCE DRIVES SYSTEMATIC QUALITY AND COST PERFORMANCE IMPROVEMENT

12 HEALTHCARE ANALYTICS MARKET, BY APPLICATION

- 12.1 INTRODUCTION

- 12.2 FINANCIAL ANALYTICS

- 12.2.1 CLAIMS ANALYTICS

- 12.2.1.1 Automated claims intelligence reduces revenue leakage and administrative burden

- 12.2.2 REVENUE CYCLE MANAGEMENT

- 12.2.2.1 End-to-end revenue intelligence optimizes margins across care continuum

- 12.2.3 FRAUD, WASTE, & ABUSE ANALYTICS

- 12.2.3.1 AI-powered detection frameworks reduce healthcare fraud and improper payments

- 12.2.4 RISK ADJUSTMENT & PAYMENT INTEGRITY

- 12.2.4.1 Accurate risk coding drives financial sustainability in value-based health plans

- 12.2.1 CLAIMS ANALYTICS

- 12.3 CLINICAL ANALYTICS

- 12.3.1 CLINICAL DECISION SUPPORT

- 12.3.1.1 Real-time evidence delivery at point of care transforms clinical outcomes

- 12.3.2 QUALITY IMPROVEMENT & CLINICAL BENCHMARKING

- 12.3.2.1 National quality benchmarks propel data-driven performance accountability

- 12.3.3 MEDICAL IMAGING ANALYTICS

- 12.3.3.1 AI-augmented imaging analysis accelerates diagnostic throughput and accuracy

- 12.3.4 REMOTE PATIENT MONITORING ANALYTICS

- 12.3.4.1 Wearable data integration expands longitudinal analytics beyond clinical walls

- 12.3.5 PRECISION HEALTH ANALYTICS

- 12.3.5.1 Genomic and multi-omics data convergence enables personalized care delivery

- 12.3.1 CLINICAL DECISION SUPPORT

- 12.4 OPERATIONAL & ADMINISTRATIVE ANALYTICS

- 12.4.1 SUPPLY CHAIN ANALYTICS

- 12.4.1.1 Predictive supply intelligence mitigates healthcare cost and shortage risks

- 12.4.2 WORKFORCE ANALYTICS

- 12.4.2.1 Predictive staffing models address healthcare talent shortages and labor costs

- 12.4.3 STRATEGIC ANALYTICS

- 12.4.3.1 Real-time visibility optimizes patient flow across complex care environments

- 12.4.4 CAPACITY & WORKFLOW ANALYTICS

- 12.4.4.1 Rising adoption of capacity & workflow analytics

- 12.4.1 SUPPLY CHAIN ANALYTICS

- 12.5 POPULATION HEALTH ANALYTICS

- 12.5.1 CHRONIC DISEASE MANAGEMENT

- 12.5.1.1 Implementing predictive analytics for early identification and proactive management of high-risk chronic disease patients

- 12.5.2 PREVENTIVE CARE ANALYTICS

- 12.5.2.1 Screening gap identification drives proactive population wellness interventions

- 12.5.3 VALUE-BASED CARE ANALYTICS

- 12.5.3.1 Total cost of care intelligence enables sustainable value-based contract performance

- 12.5.4 RISK STRATIFICATION

- 12.5.4.1 Predictive scoring models enable precision targeting of high-risk individuals

- 12.5.1 CHRONIC DISEASE MANAGEMENT

- 12.6 PATIENT JOURNEY & ENGAGEMENT ANALYTICS

- 12.6.1 PATIENT COMMUNICATION & OUTREACH ANALYTICS

- 12.6.1.1 Multichannel analytics optimizes outreach precision and patient response rates

- 12.6.2 PATIENT ADHERENCE ANALYTICS

- 12.6.2.1 Behavioral data insights drive targeted interventions to improve treatment compliance

- 12.6.3 PATIENT EXPERIENCE ANALYTICS

- 12.6.3.1 Satisfaction intelligence transforms patient-centered care accountability

- 12.6.1 PATIENT COMMUNICATION & OUTREACH ANALYTICS

13 HEALTHCARE ANALYTICS MARKET, BY END USER

- 13.1 INTRODUCTION

- 13.2 HEALTHCARE PROVIDERS

- 13.2.1 HOSPITALS & HEALTH SYSTEMS

- 13.2.1.1 Enterprise analytics integration drives system-wide performance accountability

- 13.2.2 PHYSICIAN GROUPS & CLINICS

- 13.2.2.1 Value-based contracts drive analytics adoption in ambulatory care settings

- 13.2.3 AMBULATORY SURGERY CENTERS

- 13.2.3.1 Operational transparency and quality metrics drive ASC Analytics investment

- 13.2.4 OTHER PROVIDERS

- 13.2.1 HOSPITALS & HEALTH SYSTEMS

- 13.3 HEALTHCARE PAYERS

- 13.3.1 PRIVATE INSURANCE COMPANIES

- 13.3.1.1 Actuarial intelligence and member analytics sustain commercial plan competitiveness

- 13.3.2 GOVERNMENT PAYERS

- 13.3.2.1 Federal efficiency mandates accelerate analytics in public payer programs

- 13.3.3 OTHER PAYERS

- 13.3.1 PRIVATE INSURANCE COMPANIES

- 13.4 PHARMACIES

- 13.5 OTHER END USERS

14 HEALTHCARE ANALYTICS MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 14.2.2 US

- 14.2.2.1 High adoption of electronic health records to drive market

- 14.2.3 CANADA

- 14.2.3.1 Need for managing patient volumes, clinical data, and healthcare costs to favor market

- 14.3 EUROPE

- 14.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 14.3.2 GERMANY

- 14.3.2.1 Government initiatives to increase use of analytics in healthcare to drive market

- 14.3.3 UK

- 14.3.3.1 Availability of venture capital investments to drive market

- 14.3.4 FRANCE

- 14.3.4.1 Strong financial support for digital health to augment market

- 14.3.5 ITALY

- 14.3.5.1 Growing number of drug approvals to drive uptake of analytics solutions

- 14.3.6 SPAIN

- 14.3.6.1 Growing adoption of personalized medicine to drive market

- 14.3.7 REST OF EUROPE

- 14.4 ASIA PACIFIC

- 14.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 14.4.2 JAPAN

- 14.4.2.1 Rising geriatric population to drive demand for effective patient management solutions

- 14.4.3 CHINA

- 14.4.3.1 Favorable reforms and growing number of electronic health records to aid market growth

- 14.4.4 INDIA

- 14.4.4.1 Favorable government initiatives to fuel market

- 14.4.5 AUSTRALIA

- 14.4.5.1 Strong digital health ecosystem and government-led initiatives to drive healthcare analytics adoption

- 14.4.6 SOUTH KOREA

- 14.4.6.1 Favorable government initiatives and strong digital health ecosystem to fuel market growth

- 14.4.7 REST OF ASIA PACIFIC

- 14.5 LATIN AMERICA

- 14.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 14.5.2 BRAZIL

- 14.5.2.1 Growing adoption of digital solutions in healthcare to boost market

- 14.5.3 MEXICO

- 14.5.3.1 Growing prominence of startups and rising R&D activity to propel market

- 14.5.4 REST OF LATIN AMERICA

- 14.6 MIDDLE EAST & AFRICA

- 14.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 14.6.2 GCC COUNTRIES

- 14.6.2.1 Rising investments and developing healthcare infrastructure to drive market

- 14.6.3 SAUDI ARABIA

- 14.6.3.1 Strong government-led digital health transformation to fuel market

- 14.6.4 UAE

- 14.6.4.1 Strong government-led digital health transformation to drive market

- 14.6.5 REST OF GCC COUNTRIES

- 14.6.5.1 Strong government-led digital health transformation to fuel market

- 14.6.6 SOUTH AFRICA

- 14.6.6.1 Favorable government-led digital health transformation and rising disease burden to fuel market

- 14.6.7 REST OF MIDDLE EAST & AFRICA

15 COMPETITIVE LANDSCAPE

- 15.1 INTRODUCTION

- 15.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2023-2026

- 15.3 REVENUE ANALYSIS, 2021-2025

- 15.4 MARKET SHARE ANALYSIS, 2025

- 15.5 BRAND/SOFTWARE COMPARISON

- 15.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 15.6.1 STARS

- 15.6.2 EMERGING LEADERS

- 15.6.3 PERVASIVE PLAYERS

- 15.6.4 PARTICIPANTS

- 15.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 15.6.5.1 Company footprint

- 15.6.5.2 Region footprint

- 15.6.5.3 Component footprint

- 15.6.5.4 Application footprint

- 15.6.5.5 End user footprint

- 15.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 15.7.1 PROGRESSIVE COMPANIES

- 15.7.2 RESPONSIVE COMPANIES

- 15.7.3 DYNAMIC COMPANIES

- 15.7.4 STARTING BLOCKS

- 15.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 15.7.5.1 Detailed list of key startups/SMEs

- 15.7.5.2 Competitive benchmarking of key startups/SMEs

- 15.8 COMPANY VALUATION AND FINANCIAL METRICS

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES/ENHANCEMENTS/APPROVALS

- 15.9.2 DEALS

- 15.9.3 EXPANSIONS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 MERATIVE

- 16.1.1.1 Business overview

- 16.1.1.2 Products/Solutions/Services offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product launches/enhancements/approvals

- 16.1.1.3.2 Deals

- 16.1.1.4 MnM view

- 16.1.1.4.1 Right to Win

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses and competitive threats

- 16.1.2 SAS INSTITUTE INC.

- 16.1.2.1 Business overview

- 16.1.2.2 Products/Solutions/Services offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Product launches/enhancements/approvals

- 16.1.2.4 MnM view

- 16.1.2.4.1 Right to Win

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses and competitive threats

- 16.1.3 OPTUM, INC.

- 16.1.3.1 Business overview

- 16.1.3.2 Products/Solutions/Services offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Product launches and approvals

- 16.1.3.3.2 Deals

- 16.1.3.4 MnM view

- 16.1.3.4.1 Right to Win

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses and competitive threats

- 16.1.4 ORACLE

- 16.1.4.1 Business overview

- 16.1.4.2 Products/Solutions/Services offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Product launches/enhancements/approvals

- 16.1.4.3.2 Deals

- 16.1.4.4 MnM view

- 16.1.4.4.1 Right to Win

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses and competitive threats

- 16.1.5 HEALTH CATALYST

- 16.1.5.1 Business overview

- 16.1.5.2 Products/Solutions/Services offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Product launches/enhancements/approvals

- 16.1.5.3.2 Deals

- 16.1.5.4 MnM view

- 16.1.5.4.1 Right to Win

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses and competitive threats

- 16.1.6 EXLSERVICE HOLDINGS, INC.

- 16.1.6.1 Business overview

- 16.1.6.2 Products/Solutions/Services offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Deals

- 16.1.6.3.2 Other developments

- 16.1.6.4 MnM view

- 16.1.6.4.1 Right to Win

- 16.1.6.4.2 Strategic choices

- 16.1.6.4.3 Weaknesses and competitive threats

- 16.1.7 VERADIGM LLC

- 16.1.7.1 Business overview

- 16.1.7.2 Products/Solutions/Services offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Product launches/enhancements/approvals

- 16.1.7.3.2 Deals

- 16.1.7.3.3 Other developments

- 16.1.7.4 MnM view

- 16.1.7.4.1 Right to Win

- 16.1.7.4.2 Strategic choices

- 16.1.7.4.3 Weaknesses and competitive threats

- 16.1.8 CITIUSTECH INC.

- 16.1.8.1 Business overview

- 16.1.8.2 Products/Solutions/Services offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Product launches/enhancements/approvals

- 16.1.8.3.2 Deals

- 16.1.8.3.3 Expansions

- 16.1.9 CVS HEALTH

- 16.1.9.1 Business overview

- 16.1.9.2 Products/Solutions/Services offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Product launches/enhancements/approvals

- 16.1.9.3.2 Deals

- 16.1.10 INOVALON

- 16.1.10.1 Business overview

- 16.1.10.2 Products/Solutions/Services offered

- 16.1.10.3 Recent developments

- 16.1.10.3.1 Product launches/enhancements/approvals

- 16.1.10.3.2 Deals

- 16.1.10.3.3 Expansions

- 16.1.10.3.4 Other developments

- 16.1.11 MCKESSON CORPORATION

- 16.1.11.1 Business overview

- 16.1.11.2 Products/Solutions/Services offered

- 16.1.11.3 Recent developments

- 16.1.11.3.1 Deals

- 16.1.12 MEDEANALYTICS, INC.

- 16.1.12.1 Business overview

- 16.1.12.2 Products/Solutions/Services offered

- 16.1.12.3 Recent developments

- 16.1.12.3.1 Deals

- 16.1.13 COTIVITI, INC.

- 16.1.13.1 Business overview

- 16.1.13.2 Products/Solutions/Services offered

- 16.1.14 DATAVANT, INC.

- 16.1.14.1 Business overview

- 16.1.14.2 Products/Solutions/Services offered

- 16.1.14.3 Recent developments

- 16.1.14.3.1 Product launches/enhancements/approvals

- 16.1.14.3.2 Deals

- 16.1.15 DEFINITIVE HEALTHCARE, LLC

- 16.1.15.1 Business overview

- 16.1.15.2 Products/Solutions/Services offered

- 16.1.15.3 Recent developments

- 16.1.15.3.1 Product launches/enhancements/approvals

- 16.1.15.3.2 Deals

- 16.1.16 KOMODO HEALTH, INC.

- 16.1.16.1 Business overview

- 16.1.16.2 Products/Solutions/Services offered

- 16.1.16.3 Recent developments

- 16.1.16.3.1 Product launches/enhancements/approvals

- 16.1.16.3.2 Deals

- 16.1.17 ATHENAHEALTH, INC.

- 16.1.17.1 Business overview

- 16.1.17.2 Products/Solutions/Services offered

- 16.1.17.3 Recent developments

- 16.1.17.3.1 Product launches/enhancements/approvals

- 16.1.17.3.2 Deals

- 16.1.18 IQVIA

- 16.1.18.1 Business overview

- 16.1.18.2 Products/Solutions/Services offered

- 16.1.18.3 Recent developments

- 16.1.18.3.1 Product launches/enhancements/approvals

- 16.1.18.3.2 Deals

- 16.1.19 WIPRO

- 16.1.19.1 Business overview

- 16.1.19.2 Products/Solutions/Services offered

- 16.1.20 CLOUDERA, INC.

- 16.1.20.1 Business overview

- 16.1.20.2 Products/Solutions/Services offered

- 16.1.20.3 Recent developments

- 16.1.20.3.1 Product launches/enhancements/approvals

- 16.1.20.3.2 Deals

- 16.1.1 MERATIVE

- 16.2 OTHER PLAYERS

- 16.2.1 HEALTHVERITY, INC.

- 16.2.2 KYRUUS, INC.

- 16.2.3 HEALTHCORUM

- 16.2.4 LUMA HEALTH INC.

- 16.2.5 VALIDIC, INC.

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH APPROACH

- 17.1.1 SECONDARY RESEARCH

- 17.1.1.1 Key data from secondary sources

- 17.1.2 PRIMARY RESEARCH

- 17.1.2.1 Primary sources

- 17.1.2.2 Key data from primary sources

- 17.1.2.3 Breakdown of primary interviews

- 17.1.2.4 Insights from primary experts

- 17.1.1 SECONDARY RESEARCH

- 17.2 RESEARCH METHODOLOGY DESIGN

- 17.3 MARKET SIZE ESTIMATION

- 17.4 DATA TRIANGULATION

- 17.5 RESEARCH ASSUMPTIONS

- 17.6 RESEARCH LIMITATIONS

- 17.6.1 METHODOLOGY-RELATED

- 17.6.2 SCOPE-RELATED

- 17.7 RISK ASSESSMENT

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS