|

시장보고서

상품코드

2065606

미국의 의료 분석 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States Healthcare Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

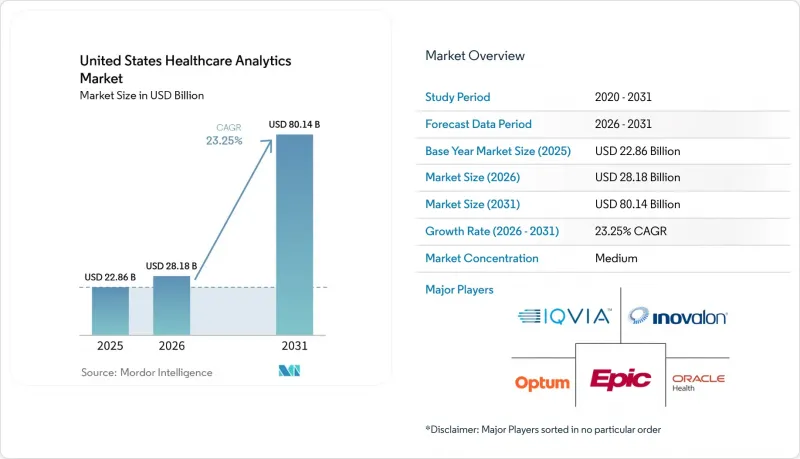

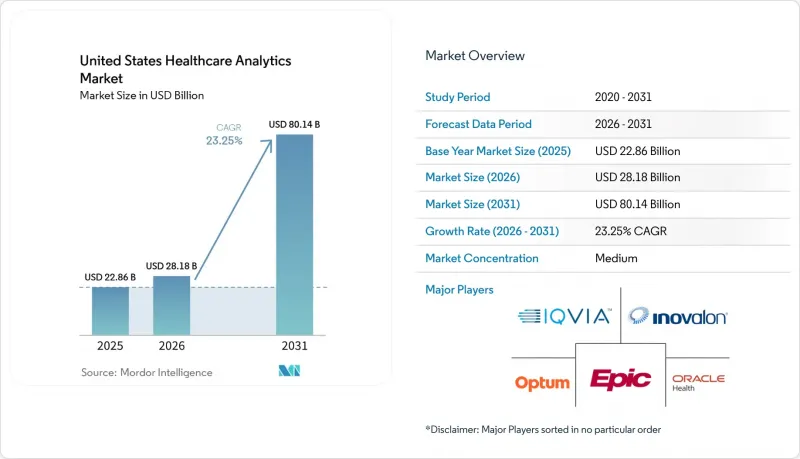

Mordor Intelligence에 의하면, 미국 의료 분석 시장 규모는 2025년 228억 6,000만 달러, 2026년 281억 8,000만 달러에서 2031년까지 801억 4,000만 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 23.25%를 나타낼 전망입니다.

본 보고서는 분석 유형(기술적, 진단적, 예측적, 처방적, 인지적/확장적), 구성 요소(하드웨어, 소프트웨어, 서비스), 제공 형태(On-Premise, 클라우드 기반, 하이브리드), 용도(임상, 재무/RCM, 운영, 집단 건강, 부정 행위, 생명과학), 최종 사용자(의료 제공업체, 보험사, 생명과학 기업, 공중보건)별로 분류되어 있습니다. 예측치는 금액(달러)으로 표시되어 있습니다.

미국 의료 분석 시장 동향과 인사이트

가치 기반 상환 및 품질 측정에 대한 설명 책임

미국의 의료 분석 시장은 메디케어 프로그램 전반에 걸쳐 비용 및 품질 성과에 관한 보다 명확한 증거를 요구하는 지불 제도 개혁에 힘입어 성장하고 있습니다. CMS의 ‘2026년 의사 보수 일정 최종 규정’에 따라, 임상 의사 수준의 성과 측정이 보상 설계의 핵심 요소로 자리 잡으면서, 조직 전반에 걸쳐 데이터를 집계하고 보다 상세한 수준에서 의료 제공업체의 보고를 지원할 수 있는 플랫폼에 대한 실무적 수요가 높아지고 있습니다. 이러한 수요는 의료 제공업체에게만 국한된 것이 아닙니다. 보험사 측도 보다 가치 중심의 계약 활동에 대비하고 있기 때문입니다. AHIP-CMS가 2026년 2월에 실시한 조사에 따르면, 응답한 건강보험 플랜의 70%가 향후 24개월 동안 APM(대체 지불 모델) 활동이 증가할 것으로 예상하고 있으며, 55%는 카테고리 3B 위험 분담 모델에서 가장 큰 성장이 예상된다고 답했습니다. 이러한 이중적인 압박으로 인해, 동일한 계약이 의료 지불 사슬의 양쪽 모두에서 분석 수요를 창출하게 되었습니다. 미국의 의료 분석 시장에서 이에 따라 보험 청구 규정 준수는 일회성 보고 업무가 아니라 소프트웨어, 서비스, 데이터 통합 분야에서 지속적인 비즈니스 기회로 변화하고 있습니다.

클라우드 네이티브 AI와 셀프 서비스 분석의 성숙도

미국의 의료 분석 시장은 도입에 드는 비용과 필요한 기술에 대한 진입 장벽을 낮추는 기술적 혁신의 혜택도 누리고 있습니다. 사전 학습된 임상 언어 모델, 로우코드 오케스트레이션 도구, FHIR 네이티브 API를 통해 중규모 의료 시스템에서도 이전에는 전담 데이터 사이언스 팀에 의존해야 했던 이용 사례를 구현할 수 있게 되었습니다. 이로 인해 기존 대형 플랫폼 업체들이 한때 누리던 우위가 서서히 사라지고 있습니다. 이는 병상 수가 400개 미만인 병원에서도 대규모 내부 분석 기능을 구축하지 않고도 예측 및 처방 기능을 이용할 수 있게 되었기 때문입니다. ONC의 2026년 연차 총회 보고서에 따르면, 현재 미국 병원의 80%가 건강 상태의 추이를 예측하기 위해 EHR(전자건강기록)에서 개발된 AI 도구를 활용하고 있으며, 58%는 청구 업무 간소화를 위해 AI를 활용하고 있습니다. 이는 2023년과 비교해 15포인트 높은 수치입니다. 미국의 의료 분석 시장에서 이러한 급속한 확산에 따라, 경쟁의 초점은 기능의 수를 대대적으로 내세우는 것보다 워크플로우와의 적합성, 거버넌스의 질, 상호운용성의 깊이로 점차 이동하고 있습니다.

연결된 생태계 전반에 걸친 사이버 보안 및 PHI 유출 위험

미국의 의료 분석 시장은 사이버 위험으로 인한 직접적인 성장 제약에 직면해 있습니다. 왜냐하면 새로운 데이터 파이프라인이 추가될 때마다 새로운 취약점의 원인이 생기기 때문입니다. 현재의 분석 환경에서는 수많은 시스템에서 임상 기록, 청구 데이터, 영상 데이터, 운영 기록이 통합되어 있으며, 이러한 상호 연결된 설계로 인해 많은 조직이 방어 체계를 강화할 수 있는 속도를 능가하는 속도로 공격 표면이 확대되고 있습니다. 2025년에는 HHS-OCR(미국 보건복지부 시민권국)에 710건의 대규모 정보 유출 사고가 보고되었으며, 6,150만 명이 피해를 입었습니다. 또한, 유출된 기록의 61.5%는 전자차트가 아닌 네트워크 서버에 저장되어 있었던 것으로 보아, 정보 유출 경로가 데이터 계층이나 미들웨어 계층을 경유하는 경우가 얼마나 빈번한지 알 수 있습니다. IBM의 보고서에 따르면, 2025년 의료 분야에서 발생한 정보 유출 사고의 평균 비용은 742만 달러에 달했으며, 이를 파악하고 차단하는 데 소요된 평균 일수는 279일이었습니다. 이는 업계 전반의 평균보다 38일 더 긴 기간입니다. 미국 의료 분석 시장에서 이러한 위험 요인은 도입 지연과 규정 준수 비용 증가를 초래하고 있으며, 비즈니스 파트너 수준에서 보다 견고한 거버넌스를 입증할 수 있는 공급업체가 우위를 점하고 있습니다.

부문별 분석

2025년, 미국 의료 분석 시장 규모 중 기술적 분석이 46.31%를 차지했습니다. 이는 많은 조직이 보다 정교한 모델 중심의 업무 흐름으로 전환하기 전에, 여전히 신뢰할 수 있는 사후 보고 체계를 구축하는 데 주력하고 있음을 보여줍니다. 미국의 의료 분석 시장에서 이러한 집중 경향은 야망의 부족이라기보다는 의료 제공업체 및 보험사의 분석 성숙도가 현재 처한 실질적인 단계를 반영한다고 할 수 있습니다. 표준화된 보고서 작성 및 대시보드는 여전히 품질 측정, 이용 현황 검토, 비용 관리 및 경영진의 의사결정 지원을 위한 운영 기반을 형성하고 있습니다. 진단형 및 처방형 도구는 그 가치가 보다 깨끗한 원본 데이터, 보다 견고한 거버넌스, 그리고 모델 산출물에 대한 높은 신뢰도에 달려 있기 때문에 여전히 보급률이 낮은 상태입니다.

예측 분석은 2031년까지 연평균 성장률(CAGR)이 25.38%로 가장 빠르게 성장하고 있는 부문이며, 이러한 성장은 순수한 기술의 혁신성보다는 상환 및 위험 노출과 밀접한 관련이 있습니다. 미국의 의료 분석 업계는 고비용 환자 집단, 의료 서비스의 격차, 그리고 이용 위험의 조기 파악으로 초점을 옮겨가고 있습니다. 이는 서술형 보고서만으로는 의무화된 위험 계약을 뒷받침할 수 없기 때문입니다. 2026년에 발표된 동료 심사를 거친 연구에 따르면, 다단계 임상 추론 및 기업 차원의 패턴 감지 능력이 향상되고 있는 것으로 나타났으며, 이에 따라 인지 분석 및 확장 분석은 이러한 변화에 새로운 차원을 더하고 있습니다. 2026년 4월 『Nature Communications』지에 발표된 ‘DxDirector’ 프레임워크는 다단계 추론 체인에 걸친 전체 과정의 임상 진단을 입증했습니다. 한편, 『npj Precision Oncology』 저널에서는 전자건강기록(EHR) 기반의 예측 모델이 26유형의 암에 대해 임상 수준의 조기 암 감지 성능을 달성했다는 증거가 발표되었습니다. 이러한 검증 결과가 축적됨에 따라, 미국의 의료 분석 시장에서는 서로 분리된 포인트 솔루션의 집합체가 아닌, 엔터프라이즈 플랫폼의 일부로서 인지 기능을 제공하는 벤더가 높이 평가받게 될 것입니다.

2025년에는 소프트웨어가 58.24%의 점유율을 차지해, 이는 기업 구매 담당자들이 분산된 개별 도구보다 미리 구축된 EHR 커넥터를 갖춘 통합 제품군을 여전히 선호하고 있음을 반영합니다. 미국 의료 분석 시장에서는 통합 과정에서 발생하는 마찰이 여전히 주요 구매 기준으로 작용하고 있기 때문에 이러한 추세는 Epic이나 Oracle Health와 긴밀한 협력 관계를 맺고 있는 벤더들에게 유리하게 작용하고 있습니다. 지출에서 하드웨어가 차지하는 비중은 줄어들었습니다. 이는 중견 기업에서 로컬 계산 부하가 높은 아키텍처에서 벗어나는 추세가 진행되면서, 물리적 인프라에 대한 추가 투자가 줄어든 데 기인합니다. 따라서 미국의 의료 분석 업계에서는 플랫폼의 소유권이 중요한 한편, 이를 뒷받침하는 지원 업무가 여전히 창출되는 가치를 좌우하는 비중을 차지하고 있는 것으로 나타납니다.

이 서비스는 2031년까지 연평균 성장률(CAGR)이 25.52%로 가장 빠르게 성장하고 있는 분야입니다. 이는 많은 의료 시스템이 데이터를 보유하고 있음에도 불구하고, 이를 대규모로 운영하기 위해 필요한 사내 팀을 여전히 갖추지 못하고 있기 때문입니다. 이는 단순한 인력 문제에 그치지 않고, 데이터 정규화, 상호 운용성, 그리고 워크플로우의 규정 준수에 수반되는 규제적 부담 또한 지속적인 서비스 수요를 창출하고 있습니다. ONC의 2026년 자료에 따르면, 2026년 1월 1일에 발효되는 USCDIv3의 요건은 94개의 데이터 요소를 포괄하고 있으며, 이에 따라 초기 소프트웨어 도입을 넘어 구현, 매핑, 거버넌스 업무에 대한 지속적인 수요가 증가하고 있습니다. 미국 의료 분석 시장에서 매니지드 애널리틱스 운영과 규정 준수 자동화를 결합한 서비스 제공업체는 프로젝트 컨설팅에만 의존하는 기업보다 고객을 더 효과적으로 유지할 가능성이 높습니다. 이로 인해 현재로서는 소프트웨어가 주도적인 위치를 유지하고 있지만, 동시에 더 광범위한 시장에서 서비스가 급속한 성장의 원동력이 되고 있는 이유도 설명되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the united states healthcare analytics market size is projected to expand from USD 22.86 billion in 2025 and USD 28.18 billion in 2026 to USD 80.14 billion by 2031, registering a CAGR of 23.25% between 2026 to 2031.

This report is Segmented by Analytics Type (Descriptive, Diagnostic, Predictive, Prescriptive, Cognitive/Augmented), Component (Hardware, Software, Services), Delivery Mode (On-Premise, Cloud-Based, Hybrid), Application (Clinical, Financial/RCM, Operational, Population Health, Fraud, Life-Sciences), and End User (Providers, Payers, Life-Sciences, Public Health). Forecasts in Value (USD).

United States Healthcare Analytics Market Trends and Insights

Value-Based Reimbursement and Quality-Measure Accountability

The US healthcare analytics market is being pushed forward by payment reform that now requires more visible proof of cost and quality performance across Medicare programs. The CMS 2026 Physician Fee Schedule Final Rule makes clinician-level performance measurement more central to reimbursement design, which increases the practical need for platforms that can aggregate data across organizations and support provider reporting at a more granular level. This demand is not limited to providers because payers are also preparing for more value-based contract activity, with 70% of health plan respondents in the AHIP-CMS February 2026 survey expecting APM activity to increase during the next 24 months and 55% expecting the greatest growth in Category 3B shared-risk models. That dual pressure means the same contract now creates analytics demand on both sides of the healthcare payment chain. In the US healthcare analytics market, this is turning reimbursement compliance into a recurring software, services, and data integration opportunity instead of a one-time reporting exercise.

Cloud-Native AI and Self-Service Analytics Maturity

The US healthcare analytics market is also benefiting from technology shifts that lower the cost and skill threshold for deployment. Pre-trained clinical language models, low-code orchestration tools, and FHIR-native APIs are allowing mid-sized health systems to launch use cases that previously depended on dedicated data science teams. This has started to erode the protection that older platform incumbents once had, because hospitals with fewer than 400 beds can now access predictive and prescriptive capabilities without building a large in-house analytics function. The ONC 2026 Annual Meeting Report stated that 80% of US hospitals now use AI from EHR-developed tools for predicting health trajectories and 58% use AI to simplify billing, which was 15 percentage points higher than in 2023. In the US healthcare analytics market, that faster adoption is redirecting competition toward workflow fit, governance quality, and interoperability depth rather than broad claims about feature count.

Cybersecurity and PHI Exposure Across Connected Ecosystems

The US healthcare analytics market faces a direct growth constraint from cyber exposure because every new data pipeline adds another point of vulnerability. Analytics environments now combine clinical, claims, imaging, and operational records from many systems, and that interconnected design widens the attack surface faster than many organizations can harden it. In 2025, 710 large breaches were reported to HHS-OCR and affected 61.5 million individuals, while 61.5% of exposed records were stored on network servers rather than in electronic medical records, which shows how often the breach path runs through data and middleware layers. IBM reported that the average healthcare breach cost reached USD 7.42 million in 2025 and required a mean of 279 days to identify and contain, which was 38 days longer than the cross-industry average. In the US healthcare analytics market, this risk is delaying deployments, raising compliance costs, and favoring vendors that can prove stronger governance at the business-associate level.

Other drivers and restraints analyzed in the detailed report include:

- Electronic Prior-Authorization API and Digital Quality Workflow Buildout

- TEFCA/FHIR-Based Cross-Enterprise Data Liquidity

- AI Validation and Governance Burden in Regulated Clinical Workflows

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Descriptive analytics held 46.31% of US healthcare analytics market size in 2025, which shows that many organizations are still building reliable retrospective reporting before moving into more advanced model-led workflows. In the US healthcare analytics market, this concentration does not show a lack of ambition as much as it reflects the practical sequence of analytics maturity across providers and payers. Standardized reporting and dashboarding still form the operational base for quality measurement, utilization review, cost management, and executive decision support. Diagnostic and prescriptive tools remain less scaled because their value depends on cleaner source data, stronger governance, and higher trust in model outputs.

Predictive analytics is the fastest-growing segment at a 25.38% CAGR through 2031, and that growth is tied more to reimbursement and risk exposure than to pure technology novelty. The US healthcare analytics industry is moving toward earlier identification of high-cost cohorts, care gaps, and utilization risk because descriptive reporting alone cannot support mandatory risk contracting. Cognitive and augmented analytics adds another layer to this shift because peer-reviewed work in 2026 showed growing capability for multi-step clinical reasoning and enterprise-scale pattern detection. The DxDirector framework published in Nature Communications in April 2026 demonstrated full-process clinical diagnosis across multi-step reasoning chains, while npj Precision Oncology published evidence that EHR-based predictive models achieved clinical-grade early cancer detection performance across 26 cancer types. As these validations accumulate, the US healthcare analytics market is likely to reward vendors that offer cognitive capability as part of an enterprise platform instead of a disconnected group of point solutions.

Software commanded a 58.24% share in 2025, reflecting how enterprise buyers continue to prefer integrated suites with pre-built EHR connectors over fragmented point tools. In the US healthcare analytics market, that pattern has favored vendors with deeper Epic and Oracle Health alignment because integration friction remains a major buying criterion. Hardware represented a smaller part of spending as more mid-tier organizations shifted away from local compute-heavy architectures and reduced incremental investment in physical infrastructure. The US healthcare analytics industry therefore shows a component mix where platform ownership matters, but surrounding enablement work still shapes realized value.

Services is the fastest-growing component at a 25.52% CAGR through 2031 because many health systems have data but still lack the internal teams needed to operationalize it at scale. This is not only a talent issue, because the regulatory burden attached to data normalization, interoperability, and workflow compliance is also creating recurring service demand. ONC's 2026 materials noted that USCDIv3 requirements effective January 1, 2026 covered 94 data elements, which increases the ongoing need for implementation, mapping, and governance work beyond initial software deployment. In the US healthcare analytics market, service providers that combine managed analytics operations with compliance automation are likely to retain clients more effectively than firms that rely on project consulting alone. This keeps software in the lead today, but it also explains why services is becoming a faster growth engine inside the broader market.

List of Companies Covered in this Report:

- Arcadia

- CitiusTech, Inc.

- Cotiviti, Inc.

- Datavant, Inc.

- Epic Systems

- Flatiron Health, Inc.

- Health Catalyst, Inc.

- Innovaccer

- Inovalon, Inc.

- IQVIA

- Komodo Health, Inc.

- MedeAnalytics

- Medidata Solutions, Inc.

- Merative, L.P.

- Microsoft

- Optum

- Oracle Health

- SAS Institute

- Socially Determined, Inc.

- Veradigm

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Value-Based Reimbursement and Quality-Measure Accountability

- 4.2.2 Rising Clinical, Claims, Imaging, and Operational Data Volumes

- 4.2.3 Margin Pressure and Revenue-Cycle Optimization Demand

- 4.2.4 Cloud-Native AI and Self-Service Analytics Maturity

- 4.2.5 Electronic Prior-Authorization API and Digital Quality Workflow Buildout

- 4.2.6 TEFCA/FHIR-Based Cross-Enterprise Data Liquidity

- 4.3 Market Restraints

- 4.3.1 Cybersecurity and PHI Exposure Across Connected Ecosystems

- 4.3.2 Legacy Integration and Semantic Interoperability Gaps

- 4.3.3 Patchwork State Privacy Rules Limiting Secondary Data Use

- 4.3.4 AI Validation and Governance Burden in Regulated Clinical Workflows

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Analytics Type

- 5.1.1 Descriptive Analytics

- 5.1.2 Diagnostic Analytics

- 5.1.3 Predictive Analytics

- 5.1.4 Prescriptive Analytics

- 5.1.5 Cognitive / Augmented Analytics

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.3 By Delivery Mode

- 5.3.1 On-Premise

- 5.3.2 Cloud-Based

- 5.3.3 Hybrid

- 5.4 By Application

- 5.4.1 Clinical Analytics

- 5.4.2 Financial & Revenue-Cycle Analytics

- 5.4.3 Operational & Administrative Analytics

- 5.4.4 Population-Health Management

- 5.4.5 Fraud Detection & Risk Analytics

- 5.4.6 Life-Sciences / R&D Analytics

- 5.5 By End User

- 5.5.1 Healthcare Providers

- 5.5.2 Healthcare Payers

- 5.5.3 Life-Science Companies

- 5.5.4 Public Health Agencies

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Arcadia

- 6.3.2 CitiusTech, Inc.

- 6.3.3 Cotiviti, Inc.

- 6.3.4 Datavant, Inc.

- 6.3.5 Epic Systems Corporation

- 6.3.6 Flatiron Health, Inc.

- 6.3.7 Health Catalyst, Inc.

- 6.3.8 Innovaccer Inc.

- 6.3.9 Inovalon, Inc.

- 6.3.10 IQVIA Holdings Inc.

- 6.3.11 Komodo Health, Inc.

- 6.3.12 MedeAnalytics, Inc.

- 6.3.13 Medidata Solutions, Inc.

- 6.3.14 Merative, L.P.

- 6.3.15 Microsoft Corporation

- 6.3.16 Optum, Inc.

- 6.3.17 Oracle Health

- 6.3.18 SAS Institute Inc.

- 6.3.19 Socially Determined, Inc.

- 6.3.20 Veradigm LLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment