|

시장보고서

상품코드

2064531

유럽의 농업용 드론 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2025-2031년)Europe Agricultural Drones - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2031) |

||||||

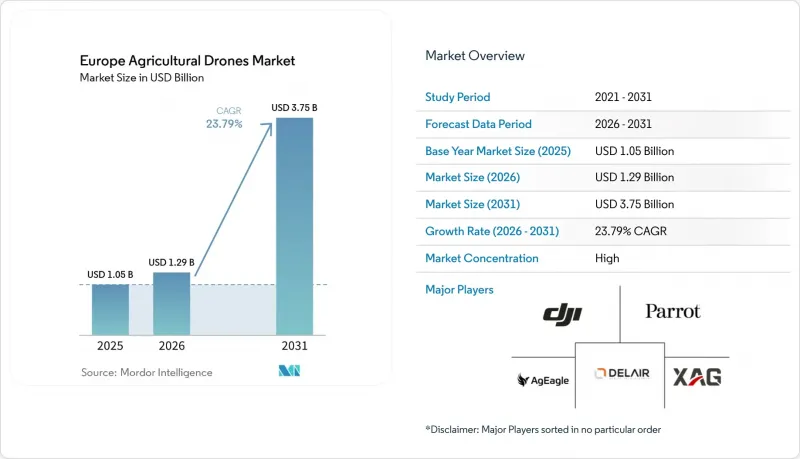

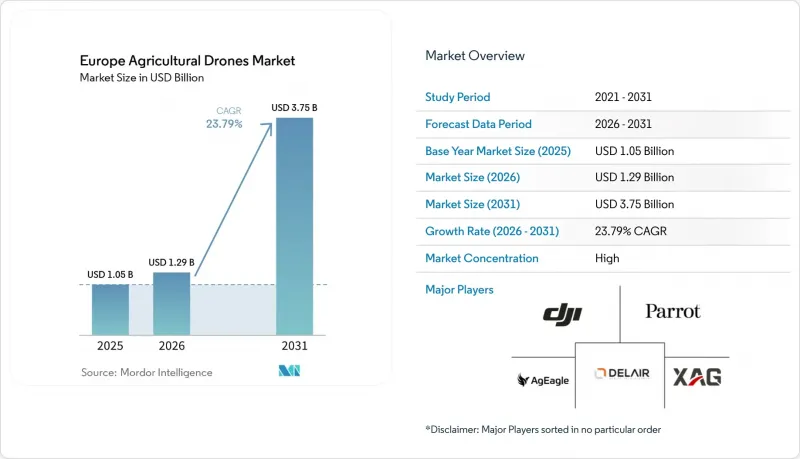

Mordor Intelligence에 의하면, 유럽의 농업용 드론 시장 규모는 2025년 10억 5,000만 달러로 평가되었습니다. 2026년 12억 9,000만 달러에서 2031년까지 37억 5,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 23.79%를 나타낼 것으로 예측됩니다.

본 보고서는 드론의 유형(고정익 드론, 회전익 드론, 하이브리드/VTOL 드론), 구성 요소(하드웨어, 소프트웨어, 서비스), 용도(농약 살포, 농지 매핑 등), 농장 규모(소규모 농장 등) 및 지역(독일, 프랑스, 영국, 이탈리아, 스페인 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽의 농업용 드론 시장 동향 및 인사이트

유럽연합(EU)의 공동농업정책에 따른 보조금 프로그램

2023년부터 2027년에 걸쳐 도입된 친환경 지원 제도에서는 정밀 농업용 하드웨어 비용의 최대 25%가 지원되어, 협동조합과 소규모 농가의 자금적 부담이 완화되고 있습니다. 2025년, 프랑스 의회는 ‘원격 조종 항공기를 활용한 농작물 병해 대응 개선’에 초점을 맞춘 법안을 가결하여, 특정 농작물에 특정 농약을 살포할 때 드론을 사용할 수 있도록 허용했습니다. 마찬가지로, 2025년에는 이탈리아 상원이 ‘간소화’ 법안(DDL)의 수정안을 승인하여, 규제된 시험 체계 하에서 농업 분야에서의 드론 사용을 허용했습니다. 코리데티가 의회 및 정부와의 협력 성과로 강조한 이러한 진전은 농업 분야의 혁신과 지속가능성을 촉진하려는 이탈리아의 전략에 부합하는 것입니다.

심화되는 노동력 부족이 농업 자동화를 가속화

노동력 부족은 유럽의 농업용 드론 시장의 중요한 성장 요인으로 작용하고 있습니다. 농업 종사자의 감소로 인해 농가에서는 드론을 활용한 살포, 포장 조사, 작물 모니터링 등의 작업 자동화를 추진하고 있기 때문입니다. 이러한 추세는 계절적인 노동력 부족과 인건비 급등에 직면한 국가들에서 특히 두드러지며, 드론을 통해 농가들은 수작업에 대한 의존도를 낮추면서도 생산성을 유지할 수 있게 되었습니다. 2025년까지 유럽의 농업 부문은 노동력의 고령화와 젊은 층의 관심 저하로 특징지어지는 심각한 노동력 부족에 계속해서 직면하게 되었으며, 그 결과 2009년부터 2024년 사이에 350만 명의 노동자가 순감소하게 되었습니다. 이러한 과제에 대응하기 위해 유럽연합(EU)은 자동화와 구조 개혁을 통해 2025년에 농업 노동 생산성을 9.2% 향상시켰으나, EU 외부에서 유입되는 계절 근로자나 이주 노동자에 대한 의존만으로는 그 격차를 완전히 메우기에는 부족합니다. 예를 들어, 네덜란드의 튤립 재배자들은 야간 민달팽이 방제를 위해 DJI Agras T50을 활용하여, 확보하기 어려운 인력에 의한 순회 조사를 효과적으로 대체하고 있습니다.

초기 하드웨어 및 소프트웨어 비용의 높음

초기 하드웨어 및 소프트웨어 비용이 높다는 점이 유럽의 농업용 드론 시장의 발목을 잡고 있습니다. 고성능 드론에는 센서, 살포 시스템, 비행 소프트웨어, 데이터 분석 도구 등 고가의 부품이 필요한 경우가 많아, 많은 중소규모 농가 입장에서는 이를 도입하는 것이 경제적으로 타당하지 않습니다. 특히, 훈련, 유지보수, 기존 농장 시스템과의 통합에 드는 추가 비용을 고려할 때, 이러한 비용은 투자 회수 기간을 연장시킬 가능성이 있습니다. 예를 들어, Sequoia+ 센서와 Pix4D 라이선스가 탑재된 senseFly eBee X와 같은 전문가용 드론 시스템은 약 2만 5,000유로(2만 6,500달러)가 듭니다. 마찬가지로, DJI nuWay의 DJI T50 컴플리트 제너레이터 키트의 가격은 약 2만 3,999달러입니다. 리스나 비행편별 요금 체계도 등장하고 있지만, 프랑스 포도 재배 업계의 가격 경쟁으로 인해 헥타르당 요금은 이미 손익분기점 근처까지 낮아졌습니다.

부문별 분석

2025년, 유럽의 농업용 드론 시장 점유율의 59%를 회전익 드론이 차지했습니다. 이는 수직 이륙이 가능하기 때문에 좁은 포도밭이나 과수원에서 살포 작업을 쉽게 수행할 수 있기 때문입니다. 한편, 200헥타르 규모의 밀밭을 90분 동안 계속 비행하기 위해서는 여전히 고정익 항공기가 필수적입니다. 스페인의 PDRA-S01은 올리브 농장을 위해 장시간 비행이 가능한 고정익기를 권장하고 있지만, 부르고뉴에서는 시야 내 비행에 제한이 있기 때문에 회전익기가 표준으로 사용되고 있습니다.

하이브리드/VTOL 드론 시장은 가장 빠르게 성장하고 있으며, 고정익 항공기의 항속 거리와 수직 이착륙 기능을 결합함으로써 2026년부터 2031년까지 연평균 성장률(CAGR) 29.0%로 확대될 것으로 전망됩니다. 제조업체들은 현재 조종사 훈련 및 예비 부품 재고를 최소화하기 위해 기체 통합을 추진하고 있습니다. MicaSense Altum-PT 클립온 센서를 대표로 하는 페이로드의 모듈화를 통해, 단일 기체로 새벽에는 매핑을 수행하고 해질녘에는 살포를 수행할 수 있게 되어 가동률이 향상됩니다. 유럽의 농업용 드론 시장에서 하이브리드 설계로 시장 점유율이 이동하고 있는 것은 플랫폼의 순수성보다 운영상의 유연성이 더 중요시되고 있음을 보여줍니다.

하드웨어는 가장 큰 부문으로, 2025년 유럽의 농업용 드론 시장 규모의 48%를 차지했습니다. 이러한 우위는 정밀 농업의 실천을 촉진하는 드론 플랫폼, 다중 스펙트럼 카메라, GPS 모듈, 센서 및 살포 시스템에 대한 수요 증가에 기인합니다. 예를 들어, 독일이나 프랑스 등의 국가 농가는 생산성을 높이고 운영 비용을 절감하기 위해 작물의 건강 상태 모니터링, 관개 관리, 농약 살포 등의 용도로 첨단 드론을 점점 더 많이 도입하고 있습니다.

서비스 부문은 가장 빠르게 성장하고 있는 분야로, 농장들이 비행, 데이터, 규정 준수 업무를 외부에 위탁함에 따라 2026년부터 2031년까지 연평균 성장률(CAGR) 31.0%를 나타낼 것으로 전망됩니다. 이러한 성장은 항공 측량, 데이터 분석, 조종사 훈련, 정비, 규제 준수 등을 포함한 드론 운영의 외주화가 농장에서 증가하고 있는 데 기인합니다. 예를 들어, 많은 중규모 농장에서는 계절별 작물 평가나 AI를 활용한 포장 보고서 작성을 위해 전문 드론 서비스 제공업체를 활용하는 방식을 선택하고 있으며, 이를 통해 초기 투자 비용을 절감하고 기술적 전문 지식을 보다 효과적으로 활용할 수 있게 되었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the europe agricultural drones market size is projected to grow from USD 1.05 billion in 2025 and USD 1.29 billion in 2026 to USD 3.75 billion by 2031, registering a CAGR of 23.79% between 2026 and 2031.

This report is Segmented by Drone Type (Fixed-Wing Drones, Rotary-Wing Drones, and Hybrid/VTOL Drones), by Component (Hardware, Software, and Services), by Application (Crop Spraying, Field Mapping, and More), by Farm Size ( Small-Scale Farms, and More), and by Geography (Germany, France, United Kingdom, Italy, Spain, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe Agricultural Drones Market Trends and Insights

Subsidy Programs Under the European Union Common Agricultural Policy

Eco-schemes introduced for 2023-2027 reimburse up to 25% of precision agriculture hardware, lowering capital barriers for cooperatives and small farms. In 2025, the French Parliament adopted a bill focused on "improving the treatment of diseases affecting plant crops using remotely piloted aircraft," enabling the use of drones to spray specific pesticides on certain crops. Similarly, in 2025, the Italian Senate approved an amendment to the "Simplifications" Bill (DDL) that allows the use of drones in agriculture under a regulated trial framework. This development, emphasized by Coldiretti as a result of collaborative efforts with Parliament and the Government, aligns with Italy's strategy to promote innovation and sustainability in agriculture.

Growing Labor Shortages Accelerating Farm Automation

Labor shortages are a significant growth driver for the European agricultural drones market, as the declining availability of farm workers is encouraging farmers to automate tasks such as spraying, scouting, and crop monitoring using drones. This trend is particularly pronounced in countries experiencing seasonal labor shortages and increasing labor costs, where drones enable farms to sustain productivity with reduced reliance on manual labor. By 2025, Europe's agricultural sector continues to face acute labor shortages, marked by an aging workforce and limited interest among younger generations, resulting in a net loss of 3.5 million workers between 2009 and 2024. To address this challenge, the European Union has achieved a 9.2% increase in agricultural labor productivity in 2025 through automation and structural reforms, although dependence on non-EU, seasonal, and migrant labor remains insufficient to fully bridge the gap. For instance, Dutch tulip growers have utilized DJI Agras T50 units for overnight slug control, effectively replacing unavailable manual scouts.

High Upfront Hardware and Software Costs

High upfront hardware and software costs pose a restraint on the Europe agricultural drone market. Advanced drones often require costly components such as sensors, spraying systems, flight software, and data analytics tools, which many small and medium-sized farms find difficult to justify. These expenses can lengthen the payback period, particularly when additional costs for training, maintenance, and integration with existing farm systems are factored in. For example, professional-grade drone systems, such as the senseFly eBee X with a Sequoia+ sensor and Pix4D license, cost approximately EUR 25,000 (USD 26,500). Similarly, the DJI nuWay DJI T50 Complete Generator Kit is priced at around USD 23,999. Leasing and per-flight models are emerging, but price wars in French viticulture have already pushed hectare fees near breakeven.

Other drivers and restraints analyzed in the detailed report include:

- Availability of Low-Cost Rotary-Wing Platforms

- Integration of Multispectral Imaging and AI Analytics

- Limited Rural 5G Coverage for Real-Time Analytics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rotary-wing drones led with 59% of Europe agricultural drones market share in 2025, owing to vertical take-off simplifying spraying in narrow vineyards and orchards. Fixed-wing units remain essential for 90-minute endurance over 200-ha wheat lots. Spain's PDRA-S01 favors long-endurance fixed wings for olive estates, while line-of-sight limits in Burgundy make rotary craft the default.

Hybrid/VTOL drones are the fastest-growing, projected to expand at a 29.0% CAGR through 2026 to 2031, combining fixed-wing range with vertical takeoff and landing. Growers now seek fleet consolidation to minimize pilot training and spares inventory. Payload modularity, exemplified by MicaSense Altum-PT clip-on sensors, enables a single airframe to map at dawn and spray at dusk, boosting utilization. The Europe agricultural drones market share shift toward hybrid designs underscores a demand for operational flexibility rather than platform purity.

Hardware was the largest segment, commanding 48% of the Europe agricultural drones market size in 2025. This dominance is attributed to the rising demand for drone platforms, multispectral cameras, GPS modules, sensors, and spraying systems that facilitate precision agriculture practices. For instance, farmers in countries such as Germany and France are increasingly adopting advanced drones for applications like crop health monitoring, irrigation management, and pesticide spraying to enhance productivity and lower operational costs.

Services are the fastest-growing segment, with a 31.0% CAGR through 2026 to 2031, as farms outsource flying, data, and compliance. This growth is driven by farms increasingly outsourcing drone operations, including aerial surveying, data analytics, pilot training, maintenance, and regulatory compliance. For instance, many medium-sized farms are opting to hire specialized drone service providers for seasonal crop assessments and AI-based field reports, enabling them to reduce upfront investments and gain access to technical expertise more effectively.

List of Companies Covered in this Report:

- SZ DJI Technology Co., Ltd.

- Parrot Drones SAS

- senseFly SA (AgEagle Aerial Systems Inc.)

- Delair SAS

- Guangzhou XAircraft Technology Co., Ltd.

- Yamaha Motor Co., Ltd.

- Trimble Inc.

- DroneDeploy Inc.

- PrecisionHawk Inc.

- Drone Volt SA

- MicaSense Inc.

- Gamaya SA

- Skydio Inc.

- Wingtra AG

- Hylio Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Subsidy programs under the European Union Common Agricultural Policy

- 4.2.2 Growing labor shortages accelerating farm automation

- 4.2.3 Availability of low-cost rotary-wing platforms

- 4.2.4 Integration of multispectral imaging and AI analytics

- 4.2.5 Carbon-credit-linked eco-drone service models

- 4.2.6 Vineyard-specific pest scouting requirements

- 4.3 Market Restraints

- 4.3.1 Fragmented airspace regulations across member states

- 4.3.2 High upfront hardware and software costs

- 4.3.3 Limited rural 5G coverage for real-time analytics

- 4.3.4 Public concerns over chemical drift from drone spraying

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Drone Type

- 5.1.1 Fixed-wing Drones

- 5.1.2 Rotary-wing Drones

- 5.1.3 Hybrid/VTOL Drones

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.3 By Application

- 5.3.1 Crop Spraying

- 5.3.2 Field Mapping and Surveying

- 5.3.3 Variable Rate Application

- 5.3.4 Livestock Monitoring

- 5.3.5 Others

- 5.4 By Farm Size

- 5.4.1 Small-scale Farms

- 5.4.2 Medium-scale Farms

- 5.4.3 Large-scale Farms

- 5.5 By Geography

- 5.5.1 Germany

- 5.5.2 France

- 5.5.3 United Kingdom

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Netherlands

- 5.5.7 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market-level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for key Companies, Products and Services, and Recent Developments)

- 6.4.1 SZ DJI Technology Co., Ltd.

- 6.4.2 Parrot Drones SAS

- 6.4.3 senseFly SA (AgEagle Aerial Systems Inc.)

- 6.4.4 Delair SAS

- 6.4.5 Guangzhou XAircraft Technology Co., Ltd.

- 6.4.6 Yamaha Motor Co., Ltd.

- 6.4.7 Trimble Inc.

- 6.4.8 DroneDeploy Inc.

- 6.4.9 PrecisionHawk Inc.

- 6.4.10 Drone Volt SA

- 6.4.11 MicaSense Inc.

- 6.4.12 Gamaya SA

- 6.4.13 Skydio Inc.

- 6.4.14 Wingtra AG

- 6.4.15 Hylio Inc.