|

시장보고서

상품코드

2064537

남미의 농업용 드론 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)South America Agricultural Drones - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

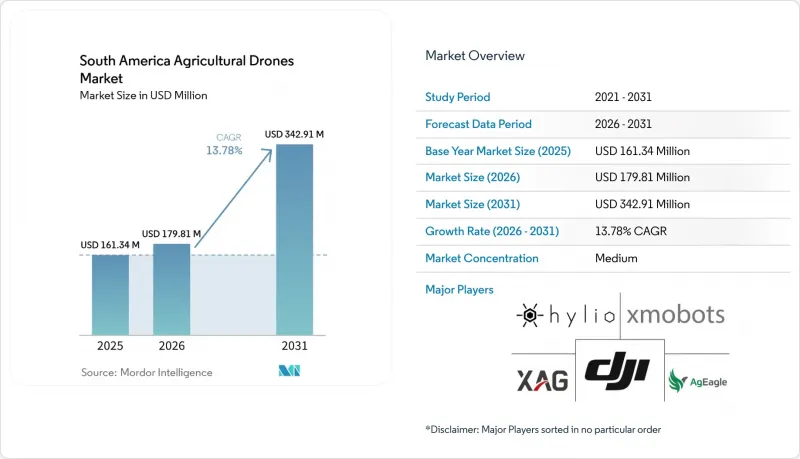

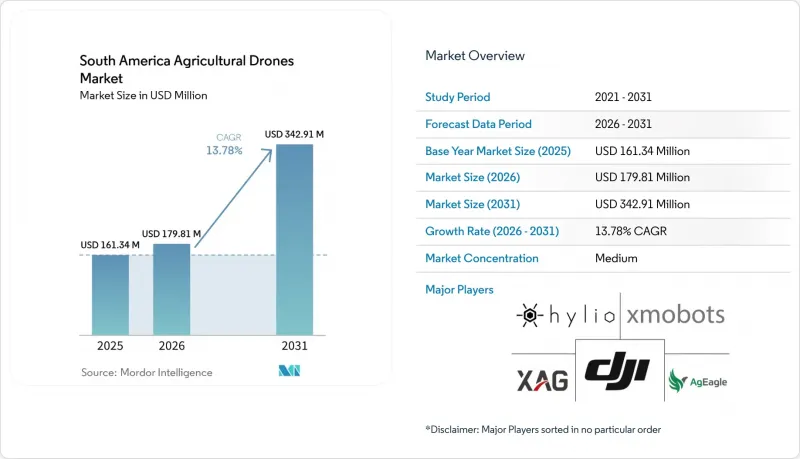

Mordor Intelligence에 의하면, 남미의 농업용 드론 시장 규모는 2025년에 1억 6,134만 달러로 평가되었습니다. 예측 기간(2026-2031년) CAGR은 13.78%를 나타내 2026년 1억 7,981만 달러에서 2031년에는 3억 4,291만 달러에 이를 것으로 추정되고 있습니다.

본 보고서는 드론의 유형(고정익, 멀티로터, 하이브리드 드론), 구성 요소(하드웨어, 소프트웨어, 서비스), 용도(농약 살포, 농지 매핑 및 측량 등), 농장 규모(대규모 상업 농장 등), 지역(브라질, 아르헨티나, 콜롬비아, 칠레, 페루 및 기타 남미)별로 분류되어 있습니다. 시장 전망치는 금액(달러) 단위로 제시되어 있습니다.

남미의 농업용 드론 시장 동향 및 인사이트

대규모 대두 및 사탕수수 재배 면적이 드론의 경제성을 뒷받침하고 있습니다.

브라질, 아르헨티나, 파라과이의 대규모 농장 구조는 소규모로 분산된 많은 농업 지역에 비해, 농업용 드론 편대를 통해 생산성이 높은 비행 시간을 제공합니다. 광활한 줄 재배 작물 및 농장 지역에서는 긴 직선 비행을 할 수 있어 더 큰 작업 구역을 확보할 수 있으므로, 경로 계획과 적재 효율이 향상됩니다. AgEagle Aerial Systems사는 2025년 7월, 브라질의 Atvos Agroindustrial S.A. 사의 사탕수수 농장(120만 에이커)에서 MicaSense S.O.D.A. 3D 카메라를 탑재한 eBee X 드론 5대를 투입하여 이 규모의 실증에 성공했습니다. 이러한 과정을 통해 3센티미터 해상도의 지도가 생성되었고, 이 지도가 농업 기계의 자동 조종 시스템에 입력됨으로써 주행 정밀도가 15센티미터 이내로 향상되었습니다. 이는 대규모 농장에서 매핑 데이터를 밭 작업에 직접 활용할 수 있음을 입증하는 것입니다. 이러한 환경에서는 도입 여부가 실험적인 활용보다는 운영자가 한 번의 임무로 충분한 면적을 커버하여 서비스 및 장비 비용을 상쇄할 수 있는지에 크게 좌우됩니다.

정밀 농업의 도입 및 투입 자재 최적화 추진

남미 전역의 생산자들은 밭 단위의 물, 농약, 노동력 관리를 개선하기 위해 드론 활용을 점점 더 늘리고 있습니다. 페루에서 진행된 동료 심사를 거친 연구에 따르면, 드론 이미지와 머신러닝 모델을 활용하여 감자 시험 재배에서 R²=0.74를 초과하는 수확량 예측 정확도를 달성한 것으로 나타났으며, 이는 단순한 밭 관찰을 넘어선 드론 주도형 작물 인텔리전스의 가치를 입증했습니다. 페루 중부에서 진행된 또 다른 동료 심사 연구에서는 49.83헥타르에 걸쳐 질소, 인, 칼륨, 유기물 및 전기 전도도에 대한 매핑이 수행되었으며, 모델의 성능도 뛰어나 정밀 시비 관리에서 드론의 역할이 더욱 공고해졌습니다. 기업의 발표도 비슷한 경향을 보이고 있으며, XAG는 브라질 농장에 이 기술을 도입함으로써 2025년에는 관개량을 헥타르당 15리터에서 10리터로 줄였다고 보고하고 있습니다(다만, 이 수치는 어디까지나 해당 회사의 주장에 불과합니다). 또한, SZ DJI Technology는 2026년 보고서에서 스팟 살포를 통해 제초제 사용량을 최대 35%까지 줄일 수 있다고 밝혔으며, 이로 인해 농산물 가격의 변동 주기가 바뀌더라도 그 가치 제안은 계속해서 유효할 것입니다.

소규모 농장에 시스템을 도입하고 충전 인프라를 구축하는 데 드는 막대한 초기 비용

남미 전역의 소규모 농가에서는 실용적인 농업용 드론을 도입하기 위해 기체 본체 외에도 많은 장비가 필요하기 때문에 계속해서 도입에 어려움을 겪고 있습니다. 콜롬비아의 2025년 ADR 조달 문서에 따르면, 운영에 필요한 패키지에는 드론 본체, 여러 개의 지능형 배터리, 발전기, 휴대용 충전기, 그리고 추가 액세서리 및 교육 요건을 포함한 지원 키트가 포함되는 것으로 나타났습니다. 이 풀 패키지는 대규모 사업자나 공유 이용 모델의 경우 경제적으로 타당하지만, 충분한 헥타르 면적을 확보해 비용을 분산할 수 없는 소규모 농가에게는 부담이 커집니다. 이것이 바로 아르헨티나에서 대출 프로그램과 리스 제도가 등장하고 있는 이유이며, 남미의 농업용 드론 시장에서 판매점이 지원하는 서비스 모델이 여전히 중요하게 여겨지는 이유이기도 합니다. 소규모 농업 지역에서 서비스 밀도가 높아지기 전까지는 많은 농장에서 드론을 직접 소유하는 것이 여전히 어려울 것입니다.

부문별 분석

고정익 드론은 가장 큰 시장 부문으로, 2025년 남미의 농업용 드론 시장 점유율의 54.8%를 차지했습니다. 이 지위는 브라질, 아르헨티나, 파라과이의 농장 구조를 반영한 것으로, 이들 국가에서는 광대한 상업용 농지에서 단거리 기동성보다는 비행 지속 시간과 광범위한 커버 능력이 더 중요시되고 있습니다. AgEagle Aerial Systems사는 2025년 7월, 브라질의 Atvos Agroindustrial S.A.사에서 자사의 eBee X 시스템이 120만 에이커에 달하는 사탕수수 밭에 도입됨으로써 이러한 추세를 입증했습니다. 이 회사는 또한 해당 시스템이 브라질에서 시야 외(BVLOS) 비행 인증을 획득했다고 밝혔습니다. 이는 더 넓은 운영 범위와 공식 승인이 필요한 대규모 농장 매핑 계약에서 중요한 요소가 됩니다. 남미의 농업용 드론 시장에서 이 점은 광활한 농지의 매핑 및 측량 업무 분야에서 고정익 플랫폼의 입지를 흔들기가 특히 어렵다는 것을 보여줍니다.

멀티로터형 드론은 가장 빠르게 성장하고 있는 부문으로, 2026년부터 2031년까지 연평균 성장률(CAGR) 14.8%로 확대될 것으로 전망됩니다. 그 기동성, 정밀 살포 능력, 그리고 기복이 있는 지형에 대한 적응성 덕분에 특수 작물, 표적 살포, 소규모 농지 작업에서 그 가치가 점점 더 높아지고 있기 때문입니다. Summit Agro Chile는 2025년 8월 DJI Agras T70P 및 T100을 출시하며, 대용량 다회전 로터 시스템이 현재 칠레의 과수원, 감귤 농장 및 포도원 운영에 활용되고 있음을 보여주었습니다. XAG도 2025년에 브라질에서 P150과 P60을 출시했으며, 한 모델은 대규모 농장을 대상으로 하고, 다른 모델은 중소규모 사용자를 대상으로 하고 있습니다. 하이브리드 드론은 특히 더 무거운 무인 시스템의 경우, 본격적인 보급을 위해 여전히 보다 명확한 운용 규칙과 광범위한 현장 검증이 필요하기 때문에 상용화의 초기 단계에 머물러 있습니다. 따라서 남미의 농업용 드론 업계는 당분간 고정익 매핑 시스템과 멀티로터 살포 시스템이 계속해서 주도할 가능성이 높다고 볼 수 있습니다.

하드웨어는 가장 큰 구성 요소로, 2025년 남미의 농업용 드론 시장 규모의 65.7%를 차지했습니다. 이 결과는 기체군, 페이로드 시스템, 충전 설비 및 현장 지원 장비의 정비 작업이 아직 진행 중인 시장 상황과 일치합니다. XMobots Aeroespacial e Defesa S.A.는 드론, 믹서, 충전 장치, 기상 관측 장치, 통신 기능, 운송용 프레임을 단일 운영 시스템으로 통합한 ‘SPAD 75’를 통해 이러한 추세를 구현했습니다. Jacto Inc.도 이와 같은 실용적인 모델을 채택하여, 단순히 기체만 판매하는 것이 아니라 장비 판매에 기술 지원, 부품, 교육, 자금 조달을 결합했습니다. 이로 인해 구매자들은 개별 기체가 아닌 완전한 운용 패키지를 필요로 하는 경우가 많기 때문에 하드웨어에 대한 지출을 높은 수준으로 유지하고 있습니다.

서비스 부문은 가장 빠르게 성장하고 있는 분야로, 2026년부터 2031년까지 연평균 성장률(CAGR) 15.1%로 확대될 것으로 전망됩니다. 이러한 변화는 자산을 직접 소유하지 않고, 계약에 따른 살포, 항공기 편대의 지원, 데이터 보고를 선호하는 생산자들에 의해 주도되고 있습니다. XMobots Aeroespacial e Defesa S.A.는 2025년에 DAASFY를 출범시켜 이동식 살포 관리, 기후 모니터링, 자동화된 기술 보고서를 제공하고 있으며, 이는 서비스 수익이 단순한 현장 작업을 넘어 확대되고 있음을 보여줍니다. 소프트웨어는 여전히 수익원 중 가장 작은 비중을 차지하고 있지만, 규제 당국과 대규모 농업 구매자들이 추적 가능성과 작업 후 문서화를 점점 더 요구함에 따라 그 중요성이 커지고 있습니다. 따라서 업계는 단순한 장비 판매에서 벗어나, 규정 준수, 분석, 운영 지원과 연계된 지속 가능한 수익 모델로 전환되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the south america agricultural drones market size was valued at USD 161.34 million in 2025 and is estimated to grow from USD 179.81 million in 2026 to USD 342.91 million by 2031, at a CAGR of 13.78% during the forecast period (2026-2031).

This report is Segmented by Drone Type (Fixed-Wing, Multi-Rotor, and Hybrid Drones), by Component (Hardware, Software, and Services), by Application (Crop Spraying, Field Mapping and Surveying, and More), by Farm Size (Large-Scale Commercial Farms and More), and by Geography (Brazil, Argentina, Colombia, Chile, Peru, and Rest of South America). Market Forecasts are Provided in Value (USD).

South America Agricultural Drones Market Trends and Insights

Large Soybean and Sugarcane Acreage Supports Drone Economics

Large-scale farm structures across Brazil, Argentina, and Paraguay provide agricultural drone fleets with more productive flight hours than in many smaller, fragmented farming regions. Broad row-crop and plantation areas allow long straight passes and larger operating blocks, improving route planning and payload efficiency. AgEagle Aerial Systems Inc. demonstrated this scale in July 2025 when it deployed 5 eBee X drones with MicaSense S.O.D.A. 3D cameras across 1.2 million acres of Atvos Agroindustrial S.A. sugarcane operations in Brazil. The same deployment produced 3-centimeter-resolution maps that fed machinery autopilot systems, improving travel accuracy to within 15 centimeters, demonstrating how large estates can connect mapping data directly to field operations. In this setting, adoption is less dependent on experimental use and more dependent on whether operators can capture enough hectares per mission to justify the service or equipment cost.

Precision Agriculture Adoption and Input Optimization Push

Growers across South America are increasingly using drones to improve control over water, agrochemicals, and labor at the field level. A peer-reviewed study in Peru showed that drone imagery and machine learning models achieved yield-prediction accuracy above R2 = 0.74 in potato trials, supporting the value of drone-led crop intelligence beyond simple field observation . A second peer-reviewed study in central Peru mapped nitrogen, phosphorus, potassium, organic matter, and electrical conductivity across 49.83 hectares with strong model performance, reinforcing the role of drones in precision input management. Company releases also point in the same direction, as XAG Co., Ltd. reported that its Brazilian farm deployment reduced water application from 15 liters per hectare to 10 liters per hectare in 2025, although that figure remains a company claim. SZ DJI Technology Co., Ltd. further stated in its 2026 report that spot spraying can reduce herbicide use by up to 35%, thereby keeping the value case active even as crop price cycles change.

High Upfront System and Charging Infrastructure Cost for Smaller Farms

Smaller farms across South America continue to face adoption barriers because a viable agricultural drone setup requires more than just the aircraft itself. Colombia's 2025 ADR procurement document showed that a working package can include the drone, multiple intelligent batteries, a generator, a portable charger, and a supporting kit with additional accessories and training requirements . That full package makes economic sense for large operators or shared-use models, but it is harder for smaller farms that cannot spread the cost over enough hectares. This is why financing programs and leasing mechanisms are emerging in Argentina, and why dealer-backed service models remain important for the South America agricultural drones market. Until service density improves in smaller agricultural regions, direct ownership will remain difficult for many farms.

Other drivers and restraints analyzed in the detailed report include:

- Brazil Regulatory Formalization Improves Legal Spraying Adoption

- Large-Farm Labor Scarcity Increases Demand for High-Output Aerial Application

- Cross-Country Compliance Complexity for Pilots, Spraying, and Airspace Use

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fixed-wing drones were the largest segment, accounting for 54.8% of the South America agricultural drones market share in 2025. Their position reflects the farm structure of Brazil, Argentina, and Paraguay, where wide commercial estates reward flight endurance and large-area coverage more than short-range maneuverability. AgEagle Aerial Systems Inc. strengthened that case in July 2025 when its eBee X system was deployed across 1.2 million acres of sugarcane at Atvos Agroindustrial S.A. in Brazil. The company also noted that the system holds beyond-visual-line-of-sight certification in Brazil, which matters for large-estate mapping contracts that require greater operating range and formal approval. In the South America agricultural drones market, this makes fixed-wing platforms especially hard to displace in mapping and surveying work over extensive crop areas.

Multi-rotor drones are the fastest-growing segment and are projected to expand at a CAGR of 14.8% during 2026-2031, as their maneuverability, precision spraying capability, and suitability for uneven terrain make them increasingly valuable for specialty crops, targeted applications, and smaller field operations. Summit Agro Chile launched the DJI Agras T70P and T100 in August 2025, demonstrating that larger-payload multirotor systems are now being positioned for Chilean fruit, citrus, and vineyard operations. XAG Co., Ltd. also launched the P150 and P60 in Brazil in 2025, with one model aimed at large farms and the other aimed at smaller and medium-scale users. Hybrid drones remain at an early commercial stage because heavier unmanned systems still need clearer operating rules and wider field proof before scale adoption. The South America agricultural drone industry is therefore likely to remain led by fixed-wing mapping systems and multi-rotor spraying systems in the near term.

Hardware was the largest component, accounting for 65.7% of the South America agricultural drones market size in 2025. That result fits a market that is still building out fleets, payload systems, charging assets, and field support equipment. XMobots Aeroespacial e Defesa S.A. illustrated this trend with the SPAD 75, which bundled the drone, mixer, charging, weather station, connectivity, and transport structure into a single operating system. Jacto Inc. followed a similar practical model by combining equipment sales with technical support, parts, training, and financing rather than selling isolated units, thereby keeping hardware spending high, as buyers often need a full operating package rather than a single aircraft.

Services are the fastest-growing segment, and are projected to expand at a 15.1% CAGR during 2026-2031. The shift is being driven by growers who prefer contracted spraying, fleet support, and data reporting without direct asset ownership. XMobots Aeroespacial e Defesa S.A. launched DAASFY in 2025 to provide mobile spraying management, climatic monitoring, and automated technical reports, which show how service revenue is moving beyond field labor alone. Software remains the smallest revenue pool, but it is gaining weight because regulators and larger farm buyers increasingly expect traceability and post-operation documentation. The industry is therefore shifting from pure equipment sales toward recurring revenue models tied to compliance, analytics, and operational support.

List of Companies Covered in this Report:

- SZ DJI Technology Co., Ltd.

- XAG Co., Ltd.

- XMobots Aeroespacial e Defesa S.A.

- Hylio, Inc.

- AgEagle Aerial Systems Inc.

- Suzhou Eavision Robotic Technologies Co., Ltd.

- Joyance Tech

- Yamaha Motor Co., Ltd.

- Beijing TT Aviation Technology Co., Ltd.

- Shandong Joyance Intelligence Technology Co., Ltd.

- Delair SAS

- Parrot Drones SAS

- AeroVironment, Inc.

- Draganfly Inc.

- Quantum Systems GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Large soybean and sugarcane acreage supports drone economics

- 4.2.2 Precision agriculture adoption and input optimization push

- 4.2.3 Brazil regulatory formalization improves legal spraying adoption

- 4.2.4 Large-farm labor scarcity increases demand for high-output aerial application

- 4.2.5 Wet-season field access constraints favor drones over ground sprayers

- 4.2.6 Financing, training, and turnkey service models reduce adoption friction

- 4.3 Market Restraints

- 4.3.1 High upfront system and charging infrastructure cost for smaller farms

- 4.3.2 Cross-country compliance complexity for pilots, spraying, and airspace use

- 4.3.3 Drift liability and contamination disputes can slow enterprise rollout

- 4.3.4 Registration and pilot-certification lag limits insurance and financing access

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Drone Type

- 5.1.1 Fixed-Wing Drones

- 5.1.2 Multi-Rotor Drones

- 5.1.3 Hybrid Drones

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.3 By Application

- 5.3.1 Field Mapping and Surveying

- 5.3.2 Crop Spraying

- 5.3.3 Crop Monitoring/Field Surveillance

- 5.3.4 Livestock Monitoring

- 5.3.5 Irrigation Management

- 5.3.6 Soil and Field Analysis

- 5.4 By Farm Size

- 5.4.1 Large-scale Commercial Farms

- 5.4.2 Small and Medium Farms

- 5.5 By Geography

- 5.5.1 Brazil

- 5.5.2 Argentina

- 5.5.3 Colombia

- 5.5.4 Chile

- 5.5.5 Peru

- 5.5.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 SZ DJI Technology Co., Ltd.

- 6.4.2 XAG Co., Ltd.

- 6.4.3 XMobots Aeroespacial e Defesa S.A.

- 6.4.4 Hylio, Inc.

- 6.4.5 AgEagle Aerial Systems Inc.

- 6.4.6 Suzhou Eavision Robotic Technologies Co., Ltd.

- 6.4.7 Joyance Tech

- 6.4.8 Yamaha Motor Co., Ltd.

- 6.4.9 Beijing TT Aviation Technology Co., Ltd.

- 6.4.10 Shandong Joyance Intelligence Technology Co., Ltd.

- 6.4.11 Delair SAS

- 6.4.12 Parrot Drones SAS

- 6.4.13 AeroVironment, Inc.

- 6.4.14 Draganfly Inc.

- 6.4.15 Quantum Systems GmbH