|

시장보고서

상품코드

2073057

중동 및 아프리카의 농업용 드론 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Middle East and Africa Agriculture Drones - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

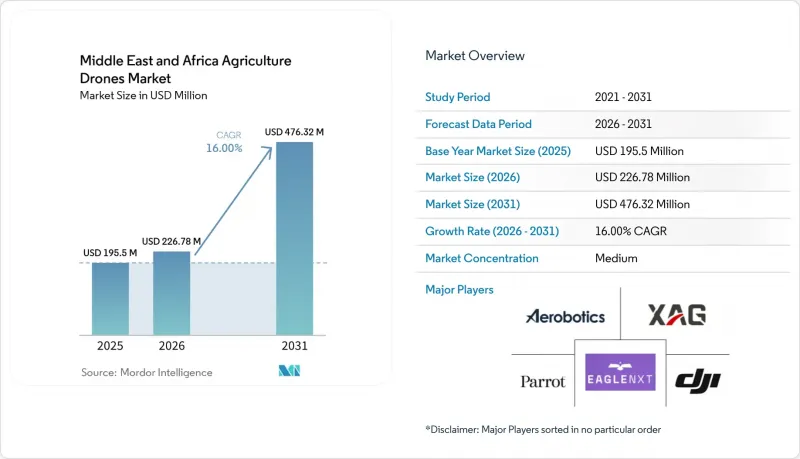

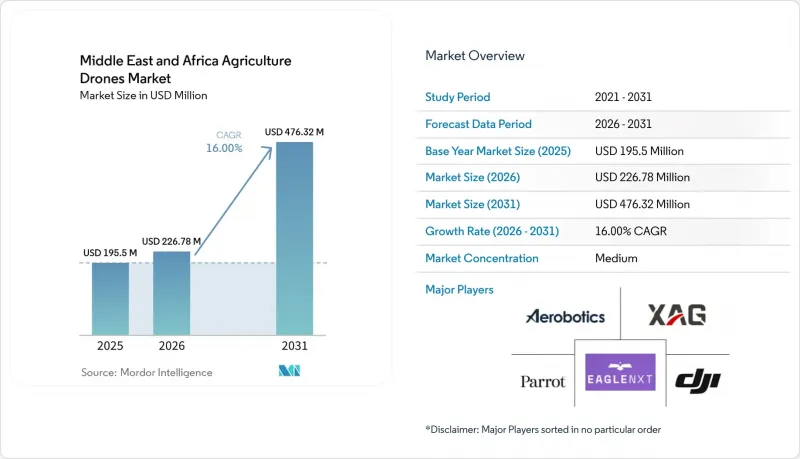

Mordor Intelligence에 의하면, 중동 및 아프리카 농업용 드론 시장 규모는 2025년 1억 9,550만 달러, 2026년 2억 2,680만 달러에서 2031년까지 4억 7,630만 달러로 확대한다고 예측되고 있어 2026-2031년까지 연평균 복합 성장률(CAGR)은 16.0%를 나타낼 전망입니다.

본 보고서는 플랫폼별(회전익, 고정익, 기타), 구성 요소별(하드웨어, 소프트웨어, 기타), 농업 환경별(야외 및 실내), 용도별(작물 모니터링, 농지 매핑, 농약 살포, 기타), 농장 규모별(대규모 상업 농장, 기타), 지역별(중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중동 및 아프리카 농업용 드론 시장 동향과 인사이트

물 부족이 촉진하는 정밀 관개

정부와 농업 관련 기업들이 정밀 관개 및 자원 최적화에 점점 더 주력하고 있는 가운데, 담수 부족은 중동 및 아프리카의 농업용 드론 시장에 있어 여전히 중요한 장기적 성장 요인으로 작용하고 있습니다. 사우디아라비아와 아랍에미리트연합(UAE) 등의 국가들은 재생 불가능한 수원에 크게 의존하고 있으며, 물 관리 및 작물 모니터링을 강화하기 위해 열화상, 다중 스펙트럼 모니터링, 정밀한 농지 평가와 같은 드론 기반 기술에 대한 수요를 주도하고 있습니다. 각국의 식량 안보 이니셔티브와 농업 현대화 프로그램을 통해, 특히 대규모 상업 농장이나 드론 편대를 대규모로 운용할 수 있는 기관 주도의 농업 프로젝트에서 드론 도입이 더욱 촉진되고 있습니다. 그 결과, 정밀 관개와 물 이용 최적화는 생산성 향상 수단에서 이 지역 농업 시장의 필수적인 운영 요건으로 자리매김하고 있습니다.

농업 인력 부족과 농약 살포 비용의 급등

중동 및 아프리카의 농업용 드론 시장은 노동력 부족과 농지 살포 비용 상승에 힘입어 성장하고 있으며, 이러한 요인들이 상업 농업 시스템에서 드론을 활용한 작업의 경제적 실현 가능성을 높이고 있습니다. 정밀 드론 살포는 기존 살포 방식에 비해 헥타르당 살포 비용을 절감하고, 살포 효율을 높이며, 농약 사용을 최적화할 수 있어 생산자와 농업협동조합 사이에서 인기가 높아지고 있습니다. 특히 고부가가치 작물 재배 분야에서 수요가 견조한 가운데, 생산자들은 수작업에 대한 의존도를 줄여나가면서 보다 적절한 살포 시기, 수관 침투성 향상, 정확한 살포량 관리를 우선시하고 있습니다. 그 결과, 이 지역 전체의 주요 상업 농업 지역에서 정기적인 드론 농업 서비스 모델이 점점 더 중요해지고 있습니다.

시야 밖(BVLOS) 및 공중 살포에 관한 규제의 불일치

중동 및 아프리카의 농업용 드론 시장에서 규제는 여전히 중대한 구조적 과제로 남아 있습니다. 각국마다 인증 및 비행 규정이 다르기 때문에 사업자가 원활하게 사업을 확장하는 데 차질이 생기고 있기 때문입니다. 2026년 1월, 사우디아라비아는 민간항공총국(GACAR) 규정 제107부를 개정하여, 유럽항공안전청(EASA)의 기준을 따르는 위험 기반 표준 시나리오를 상업용 시야 외(BVLOS) 운항에 도입했습니다. 이러한 개정으로 인해 규정을 준수하는 사업자의 경우, 승인까지 걸리는 기간이 대폭 단축될 가능성이 있습니다. 서비스 제공업체들이 국가별로 제각각인 체제로 운영되는 것이 아니라, 지역별 드론 편대를 구축하기 위해서는 예측 가능한 규제 체계가 필요하기 때문에 이러한 진전은 매우 중요합니다. 또한, CropLife Africa Middle East는 많은 아프리카 시장에서 명확하고 강제력 있는 살포 기준이 부재한 문제를 해결하기 위해, 2025년에 드론을 이용한 농약 살포에 관한 지역적 프레임워크를 발표했습니다. 그러나 더 많은 국가들이 라이선스 발급, 조종사 자격 인증, 살포 기준에 관한 규제를 조화시킬 때까지는 중동 및 아프리카의 농업용 드론 시장이 해당 지역의 드론 서비스 제공업체들에게 계속해서 추가적인 운영 비용을 부담시킬 것으로 보입니다.

부문별 분석

2025년, 중동 및 아프리카의 농업용 드론 시장에서 회전익 드론은 65.0%라는 가장 높은 점유율을 차지했습니다. 이는 호버링 능력, 저고도에서의 정밀성, 살포, 작물 모니터링, 가축 모니터링과 같은 용도에서 보여주는 운용상의 유연성 덕분입니다. 특히, 정밀한 저고도 기동성이 필수적인 과수원, 포도원, 대추야자 농장에서의 도입이 계속해서 호조를 보이고 있습니다. 반면, 고정익 플랫폼 시장은 더 넓은 농지 커버리지, 더 긴 비행 지속 시간, 헥타르당 조사 비용 절감을 원하는 대규모 농장 운영자들의 도입 확대에 힘입어, 2026년부터 2031년까지 16.5%라는 가장 높은 연평균 성장률(CAGR)을 기록하며 성장할 것으로 전망됩니다.

하이브리드 날개 시스템은 현재 총 매출에서 차지하는 비중은 작지만, 수직 이륙 능력과 더 넓은 농지에서 순항 효율을 동시에 향상시킬 수 있는 시스템을 찾는 구매자들로부터 관심을 받고 있습니다. 중동 및 아프리카의 농업용 드론 시장에서는 살포 및 단거리 모니터링에 적합하다는 점 때문에 회전익 시스템이 도입 대수 측면에서 압도적인 점유율을 차지하고 있습니다. 그러나 호버링 성능이 그다지 중요하지 않고, 더 긴 측량 거리, 더 광범위한 농지 커버리지, 더 높은 운용 효율이 요구되는 용도에서는 고정익 및 하이브리드 플랫폼이 점차 보급되고 있습니다. 앞으로 플랫폼의 도입은 용도별로 특화될 것으로 예상되며, 회전익 드론은 정밀 살포 분야에서 우위를 유지하는 한편, 고정익 시스템은 농장 매핑 및 대규모 농지 정보 수집 업무에서 그 역할을 확대해 나갈 것으로 보입니다.

2025년 중동 및 아프리카 농업용 드론 시장에서 하드웨어가 63.0%라는 가장 큰 시장 점유율을 차지했습니다. 이는 해당 시장이 현재 항공기 도입과 핵심 운영 인프라에 중점을 두고 있음을 반영한 것입니다. 이 지역의 생산자들은 고도 분석 기능으로의 확장에 앞서 항공기 플랫폼, 페이로드 시스템, 배터리, 지원 장비에 대한 투자를 우선시하고 있습니다. 반면, 서비스 시장은 Drone-as-a-Service(DaaS) 모델의 도입 확대에 힘입어 2026년부터 2031년까지 연평균 성장률(CAGR)이 17.2%에 육박하며 가장 높은 성장세를 보일 것으로 전망됩니다. 이러한 모델은 초기 투자 부담을 줄이고 운영 지원을 외부에 위탁하고자 하는 생산자들에게 매력적입니다.

시장은 하드웨어 중심의 구매에서 분석, 농업 관련 자문, 사업자 교육, 관리형 살포 서비스를 중심으로 한 지속적인 수익 모델로 점차 전환되고 있습니다. 이러한 변화로 인해 상업적 농업 운영에서 소프트웨어 통합, 농지 인텔리전스 기능, 규제 대응 지원, 신뢰할 수 있는 실행 품질의 중요성이 커지고 있습니다. 그 결과, 드론 플랫폼을 농업 서비스 및 정밀 농업 분야의 전문 지식과 통합할 수 있는 기업은 중동 및 아프리카의 농업용 드론 시장에서 경쟁력을 한층 더 강화할 것으로 예측됩니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.07According to Mordor Intelligence, the middle east and Africa agriculture drones market size is projected to expand from USD 195.5 million in 2025 and USD 226.8 million in 2026 to USD 476.3 million by 2031, registering a CAGR of 16.0% between 2026 and 2031.

This report is Segmented by Platform (Rotary Wing, Fixed Wing, and More), by Component (Hardware, Software, and More), by Farming Environment (Outdoor and Indoor), by Application (Crop Monitoring, Field Mapping, Crop Spraying, and More), by Farm Size (Large-Scale Commercial and More), and by Geography ( Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Middle East and Africa Agriculture Drones Market Trends and Insights

Water-Stress Driven Precision Irrigation

Freshwater scarcity remains a significant long-term growth driver for the agriculture drones market in the Middle East and Africa, as governments and farm operators increasingly focus on precision irrigation and resource optimization. Countries such as Saudi Arabia and the United Arab Emirates (UAE) heavily depend on non-renewable water sources, driving demand for drone-based technologies such as thermal imaging, multispectral monitoring, and precision field assessment to enhance water management and crop monitoring . National food security initiatives and agricultural modernization programs are further promoting the adoption of drones, particularly among large commercial farms and institutional farming projects capable of deploying drone fleets at scale. Consequently, precision irrigation and water-use optimization are transitioning from productivity-enhancing tools to essential operational requirements within the regional agriculture market.

Farm Labor Shortages and Spray-Cost Inflation

The agriculture drones market in the Middle East and Africa is being driven by labor shortages and rising field-spraying costs, which enhance the economic feasibility of drone-based operations in commercial farming systems. Precision drone spraying is gaining popularity among growers and farming cooperatives for its ability to reduce per-hectare spraying costs, improve application efficiency, and optimize chemical use compared to traditional spraying methods. The demand is particularly robust in high-value crop cultivation, where growers prioritize better spray timing, improved canopy penetration, and accurate dosage application while reducing reliance on manual labor. Consequently, recurring drone-based agriculture service models are becoming increasingly significant in key commercial farming areas across the region.

Fragmented Beyond Visual Line of Sight (BVLOS) and Aerial Spray Rules

Regulation remains a significant structural challenge in the Middle East and Africa agriculture drones market, as differing certification and flight rules across countries hinder seamless scaling for operators. In January 2026, Saudi Arabia updated the General Authority of Civil Aviation Regulations (GACAR) Part 107, introducing European Union Aviation Safety Agency (EASA)-aligned risk-based Standard Scenarios for commercial Beyond Visual Line of Sight (BVLOS) operations. These updates have the potential to significantly reduce approval timelines for compliant operators. This development is crucial, as service providers need predictable regulatory frameworks to establish regional drone fleets rather than operating on a fragmented, country-specific basis. Additionally, CropLife Africa Middle East published a regional framework for drone-based pesticide application in 2025 to address the lack of clear, enforceable spraying standards in many African markets . However, until more countries harmonize regulations on licensing, pilot certification, and spraying standards, the agriculture drones market in the Middle East and Africa will continue to impose additional operating costs on regional drone service providers.

Other drivers and restraints analyzed in the detailed report include:

- Food-Security Programs and Smart-Farming Incentives

- Return on Investment (ROI) on High-Value Crops and Plantation Monitoring

- High Upfront Cost and Weak Farm Financing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rotary-wing drones accounted for the largest 65.0% share of the Middle East and Africa agriculture drones market in 2025, driven by their hover capability, low-altitude precision, and operational flexibility across spraying, crop surveillance, and livestock monitoring applications. Their adoption remains particularly strong in orchard, vineyard, and date-farming operations where precise low-level maneuverability is essential. In contrast, the fixed-wing platforms market is projected to grow at the fastest CAGR of 16.5% from 2026 to 2031, supported by rising adoption among large plantation operators seeking wider field coverage, longer flight endurance, and lower per-hectare surveying costs.

Hybrid-wing systems currently contribute less to overall revenue but are attracting interest from buyers seeking vertical takeoff capabilities combined with improved cruising efficiency for larger agricultural areas. In the Middle East and Africa agriculture drones market, rotary-wing systems dominate deployment volumes due to their suitability for spraying and short-range monitoring. However, fixed-wing and hybrid platforms are gradually gaining traction in applications requiring longer survey distances, broader field coverage, and higher operational efficiency, where hover performance is less critical. Over time, platform adoption is anticipated to become more application-specific, with rotary-wing drones maintaining dominance in precision spraying, while fixed-wing systems expand their role in plantation mapping and large-scale field intelligence operations.

Hardware accounted for the largest market share, 63.0%, in the Middle East and Africa agriculture drones market in 2025. This reflects the market's current emphasis on fleet deployment and core operational infrastructure. Growers across the region are prioritizing investments in aircraft platforms, payload systems, batteries, and supporting equipment before expanding into advanced analytics capabilities. In contrast, the services market is projected to grow at the fastest CAGR of nearly 17.2% from 2026 to 2031, driven by the increasing adoption of Drone-as-a-Service (DaaS) models. These models appeal to growers seeking lower upfront investment requirements and outsourced operational support.

The market is gradually transitioning from hardware-focused purchasing to recurring revenue models centered on analytics, agronomic advisory, operator training, and managed spraying services. This shift is enhancing the importance of software integration, field intelligence capabilities, regulatory support, and reliable execution quality in commercial farming operations. Consequently, companies that can integrate drone platforms with agronomic services and precision agriculture insights are projected to strengthen their competitive position in the Middle East and Africa agriculture drones market.

Complete Report Scope:

- By Platform

- Rotary Wing

- Fixed Wing

- Hybrid Wing

- By Component

- Hardware

- Software

- Services

- By Farming Environment

- Outdoor Farming

- Indoor Farming

- By Application

- Crop Monitoring and Field Surveillance

- Field Mapping and Soil Analysis

- Crop Spraying and Spreading

- Variable Rate Application

- Livestock Monitoring

- By Farm Size

- Large-scale Commercial Farms

- Small and Medium-sized Farms

- By Geography

- Middle East

- Saudi Arabia

- United Arab Emirates (UAE)

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

List of Companies Covered in this Report:

- SZ DJI Technology Co., Ltd.

- XAG Co., Ltd.

- EagleNXT

- Parrot Drone SAS

- Aerobotics, (Pty) LTD

- Yamaha Motor Co., Ltd.

- AeroVironment, Inc.

- Trimble Inc.

- DroneDeploy, Inc.

- Hylio, Inc.

- DELair SAS

- Autel Robotics

- Sentera, Inc.

- Wingtra AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Water-stress driven precision irrigation

- 4.2.2 Farm labor shortages and spray-cost inflation

- 4.2.3 Food-security programs and smart-farming incentives

- 4.2.4 Return on Investment (ROI) on high-value crops and plantation monitoring

- 4.2.5 Drone-as-a-service expansion for grower clusters

- 4.2.6 Export-traceability and carbon-data requirements

- 4.3 Market Restraints

- 4.3.1 Fragmented Beyond Visual Line of Sight (BVLOS) and aerial spray rules

- 4.3.2 High upfront cost and weak farm financing

- 4.3.3 Rural charging, Real-Time Kinematic (RTK), and spare-parts gaps

- 4.3.4 Limited agronomic prescription data and pilot skills

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Platform

- 5.1.1 Rotary Wing

- 5.1.2 Fixed Wing

- 5.1.3 Hybrid Wing

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.3 By Farming Environment

- 5.3.1 Outdoor Farming

- 5.3.2 Indoor Farming

- 5.4 By Application

- 5.4.1 Crop Monitoring and Field Surveillance

- 5.4.2 Field Mapping and Soil Analysis

- 5.4.3 Crop Spraying and Spreading

- 5.4.4 Variable Rate Application

- 5.4.5 Livestock Monitoring

- 5.5 By Farm Size

- 5.5.1 Large-scale Commercial Farms

- 5.5.2 Small and Medium-sized Farms

- 5.6 By Geography

- 5.6.1 Middle East

- 5.6.1.1 Saudi Arabia

- 5.6.1.2 United Arab Emirates (UAE)

- 5.6.1.3 Rest of Middle East

- 5.6.2 Africa

- 5.6.2.1 South Africa

- 5.6.2.2 Egypt

- 5.6.2.3 Rest of Africa

- 5.6.1 Middle East

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 SZ DJI Technology Co., Ltd.

- 6.4.2 XAG Co., Ltd.

- 6.4.3 EagleNXT

- 6.4.4 Parrot Drone SAS

- 6.4.5 Aerobotics, (Pty) LTD

- 6.4.6 Yamaha Motor Co., Ltd.

- 6.4.7 AeroVironment, Inc.

- 6.4.8 Trimble Inc.

- 6.4.9 DroneDeploy, Inc.

- 6.4.10 Hylio, Inc.

- 6.4.11 DELair SAS

- 6.4.12 Autel Robotics

- 6.4.13 Sentera, Inc.

- 6.4.14 Wingtra AG