|

시장보고서

상품코드

2064539

인도의 농업용 드론 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)India Agricultural Drones - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

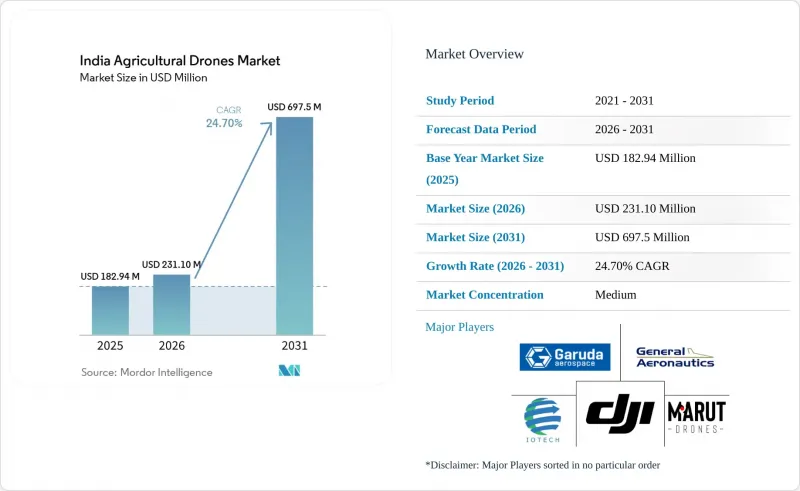

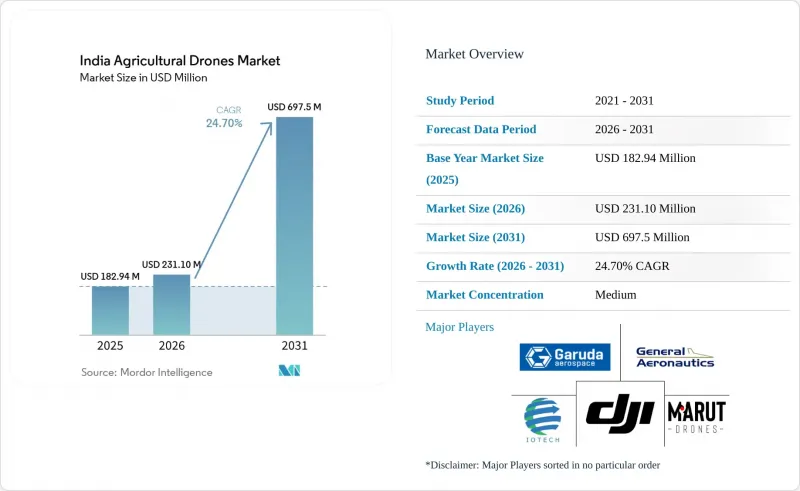

Mordor Intelligence에 의하면, 인도의 농업용 드론 시장 규모는 2025년 1억 8,294만 달러로 평가되었고, 2026년에는 2억 3,110만 달러로 추정되고, 게다가 2031년까지 6억 9,750만 달러로 확대될 전망이며, 2026-2031년 연평균 복합 성장률(CAGR)은 24.70%를 나타낼 것으로 예측됩니다.

본 보고서는 제품별(고정익 드론, 회전익 드론, 하이브리드 드론), 구성 요소별(하드웨어, 소프트웨어, 서비스), 용도별(농지 매핑 및 측량, 농약 살포 등), 그리고 농장 규모별(대규모 상업 농장, 중소규모 농장)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

인도의 농업용 드론 시장 동향 및 인사이트

농업 노동력 비용 상승과 부족

살포 적기가 제한된 기간 동안 발생하는 노동력 부족은 인도 농업 시스템 전반에 걸쳐 드론 도입의 가장 명확한 상업적 요인 중 하나입니다. 벼 흰잎마름병이나 목화나방의 방제 적기는 시간적 제약이 엄격하여, 살포가 늦어지면 농가와 자재 공급 기업 모두에게 큰 손실이 됩니다. 특히, 이미 농촌에서 도시로의 인구 유출이 심각한 주에서는 칼리프(가을 작물) 및 라비(겨울 작물)의 수확 성수기에 계약직 근로자를 확보하기가 어려워지고 있습니다. 제출된 초안에 따르면, 펀자브주와 하리야나주의 농업 노동 임금은 2022-2025년 연간 약 8%에서 12% 상승할 것으로 예상되며, 평균 농업 노동자의 일당은 4.5달러에서 6달러 가까이 될 것으로 전망되는데, 이로 인해 기계화된 살포 방식의 상대적 매력이 높아지고 있습니다. 시간당 20-30에이커를 커버할 수 있는 드론은 작업 기간을 단축합니다. 이는 특히 단위 노동 비용뿐만 아니라 처리 시점이 중요한 경우, 수동 백팩식 살포 팀으로는 실현할 수 없는 특징입니다. 농약 제조업체들도 드론 도입을 지원하고 있습니다. 더 정확한 살포는 제품의 성능을 향상시키고, 현장 팀이 더 넓은 지역을 보다 일관성 있게 관리하는 데 도움이 되기 때문입니다. 이러한 노동력 변화로 인해 농업용 드론 산업은 단순한 장비 판매에서 벗어나, 계절별 작업 품질에 따라 달라지는 정기 서비스 계약으로 그 영역을 넓혀가고 있습니다.

정부 보조금

정부의 지원은 농업용 드론 업계에 있어 여전히 가장 강력한 단기 수요 견인 요인 중 하나입니다. 이는 여러 사용자 그룹에서 동시에 진입 비용을 낮추기 위함입니다. 보조금 제도는 다층적이며, 이는 개별 농가 소유주뿐만 아니라 직접 구매자, 지역 운영자, 조직화된 농촌 단체를 지원한다는 점에서 중요합니다. ‘농업 기계화 지원 사업’은 선정된 수혜자 그룹의 드론 도입을 지원하고 있으며, ‘나모 드론 디디’ 제도는 여성이 주도하는 자조 그룹을 위한 별도의 지원 경로를 마련하고 있습니다. 이 지원 제도에서는 드론 비용의 최대 80%가 지원 대상이며, 지원 대상인 자조 그룹 1개 단체당 최대 9,524달러까지 지원됩니다. 한편, 2023-24년도부터 2025-26년도까지의 프로그램 전체 예산은 1억 5,010만 달러였습니다. 이 체계는 소유 위험을 줄여주며, 지역 단체가 드론을 개별 농가의 기계가 아닌 마을 전체의 서비스 자산으로 취급할 수 있도록 돕습니다. 또한, 체계화된 서비스 제공을 통해 현장에서 표준화된 투입 자재 프로그램을 추진하기가 쉬워지므로, 드론 활용과 비료·작물 보호 자재의 유통 경로를 연계하는 데에도 기여하게 됩니다. 이러한 조합을 통해 시장에는 일회성 자본 보조금 프로그램이 일반적으로 제공하는 것보다 더 지속 가능한 정책 기반이 마련됩니다.

분리된 드론 및 농약 규제

규제는 여전히 가장 중요한 제약 요소 중 하나입니다. 왜냐하면 운영상의 부담이 항공법 규정 준수라는 측면과 농약 사용 승인이라는 두 가지 측면으로 나뉘어 있기 때문입니다. 항공법 규제의 측면은 ‘Digital Sky’ 시스템을 통해 관리되며, 여기에는 고유 식별 번호, 조종사 자격 인증 및 허가 기반 운항이 포함됩니다. 또한, 드론 살포 규정은 제품, 제형, 지역의 권장 관행에 따라 달라질 수 있으므로, 작물 및 화학 물질별로 별도의 승인 절차가 추가됩니다. 서비스 사업자는 기술적으로는 비행 준비가 완료되었더라도, 새로운 지역에서 특정 살포 프로그램을 시작하기까지 지연이 발생할 수 있습니다. 주 경계를 넘어 사업을 확장할 경우, 새로운 지역마다 절차상 확인과 지역과의 조정이 필요하기 때문에 더욱 지연됩니다. 준법 업무는 운영 자금과 경영진의 시간을 소모하지만, 대형 사업자는 더 대규모의 항공기 편대로 그 부담을 분산할 수 있기 때문에 중소규모 사업자가 가장 큰 영향을 받습니다. 이러한 규제의 파편화로 인해, 수요 동향만으로는 예상되는 만큼 시장이 급속히 확대되지는 않고 있습니다.

부문별 분석

2025년, 회전익 드론은 제품 매출의 64.6%를 차지했으며, 플랫폼 유형별 인도 농업용 드론 시장 점유율에서 1위를 유지했습니다. 이러한 우위는 살포를 많이 사용하는 재배 패턴, 불규칙한 구획 형태, 그리고 세분화된 농지와 소규모 농가 중심의 재배 환경에서 좁은 밭에서 호버링 제어를 수행할 수 있기 때문입니다. 농가 생산자 단체 및 서비스 사업자의 보조금 지원을 받은 구매가 멀티로터의 선두 자리를 유지하는 데 기여했습니다.

하이브리드 드론은 플랜테이션이나 대규모 농지 구역에서 수직 이착륙(VTOL)의 유연성과 매핑 효율 향상을 통한 장거리 커버리지가 요구됨에 따라, 2031년까지 연평균 성장률(CAGR) 24.5%로 확대될 것으로 예상되며, 이는 제품 카테고리 중 가장 높은 성장률입니다. 이러한 이용은 연속된 광대한 농지가 장시간 비행 및 정밀 모니터링 용도를 뒷받침하는 포도, 바나나, 과수 재배 지역에서 증가하고 있습니다. 광역 측량 업무에서는 고정익 드론이 여전히 중요한 역할을 하고 있지만, 비행 거리와 운용 유연성의 균형을 고려할 때 하이브리드 플랫폼이 점점 더 선호되고 있습니다. 신제품에서는 내후성 향상, 연결성 강화, 더욱 스마트한 경로 계획과 같은 제품 개선이 여전히 두드러지게 나타납니다. 이러한 상황으로 인해, 현재도 회전익 시스템이 주류를 이루고 있는 반면, 시장에서 고정익 및 하이브리드 플랫폼의 향후 역할은 점차 확대되고 있습니다.

2025년에는 하드웨어가 구성 요소별 매출의 53.2%를 차지했으며, 인도 농업용 드론 시장에서 가장 큰 점유율을 기록했습니다. 전국적인 농업용 드론 도입 네트워크가 확대되는 가운데, 지출은 살포 시스템, 배터리, 센서, 충전 지원에 계속 집중되었습니다. 이는 자산 구매가 여전히 소프트웨어 구독료나 서비스 요금을 크게 상회하는 도입 단계를 반영한 것입니다.

협동조합, 주 정부 프로그램 및 상업 사업자들이 소유 모델에서 지속 이용 모델로 지출을 전환함에 따라, 서비스 부문은 2031년까지 연평균 성장률(CAGR) 23.1%로 가장 빠른 성장세를 보일 것으로 전망됩니다. 또한, 비행 관리, 처방 지도 작성, 작물 분석 및 기체 관리 도구가 일상적인 농업 운영에 점점 더 통합됨에 따라 소프트웨어의 중요성도 커지고 있습니다. 따라서 인도의 농업용 드론 업계는 하드웨어 중심의 도입 단계에서 장비, 소프트웨어 및 지속적인 서비스 가치가 보다 균형 있게 결합된 형태로 전환되고 있습니다. 타임스탬프가 포함된 살포 기록은 보험 서류 작성, 규정 준수 및 농업 관련 자문 업무 흐름을 지원함으로써 소프트웨어 도입을 더욱 촉진하고 있습니다. 하드웨어 가격 하락에 따라 시장 전체의 수익 구조는 서비스 및 소프트웨어 쪽으로 더욱 이동할 것으로 예측됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSH 26.06.24According to Mordor Intelligence, the india agricultural drones market size is projected to grow from USD 182.94 million in 2025 to USD 231.10 million in 2026 and further to USD 697.50 million by 2031, registering a CAGR of 24.70% between 2026 and 2031.

This report is Segmented by Product (Fixed-Wing Drones, Rotary-Wing Drones, and Hybrid Drones), by Component (Hardware, Software, and Services), by Application (Field Mapping and Surveying, Crop Spraying, and More), and by Farm Size (Large-Scale Commercial Farms and Small and Medium Farms). The Market Forecasts are Provided in Terms of Value (USD).

India Agricultural Drones Market Trends and Insights

Rising Farm-Labor Costs and Shortages

Labor scarcity during narrow spray windows has become one of the clearest commercial triggers for drone deployment across Indian farming systems. Paddy blast and cotton bollworm treatment windows are time-sensitive, and delayed spraying is costly for both farmers and input companies. Contract labor availability has tightened during peak Kharif and Rabi periods, especially in states that already face strong rural-to-urban migration. The supplied draft noted that agricultural labor rates in Punjab and Haryana rose by an estimated 8% to 12% annually between 2022 and 2025, with average farm labor wages reaching nearly USD 4.5 to USD 6.0 per day, thereby raising the relative appeal of mechanized application methods. A drone that can cover 20 to 30 acres per hour narrows the operating window, a feature manual backpack crews cannot match, especially when treatment timing matters more than unit labor cost alone. Agrochemical companies are also supporting drone deployment because more accurate application improves product performance and helps field teams manage larger territories with better consistency. This labor-driven shift is broadening the agriculture drones industry beyond equipment sales into repeat-service contracts that depend on seasonal execution quality.

Government Subsidies

Government support remains one of the strongest near-term demand anchors for the agricultural drones industry because it lowers entry costs across several user groups at the same time. The subsidy structure is layered, and that matters because it supports direct buyers, community operators, and organized rural groups rather than only individual farm owners. The Sub-Mission on Agricultural Mechanization supports drone acquisition for selected beneficiary groups, and the Namo Drone Didi scheme adds a separate route for women-led Self-Help Groups. Under the scheme, support reaches up to 80% of the drone cost, with a cap of USD 9,524 for each eligible Self-Help Group, while the broader program outlay for 2023-24 to 2025-26 stood at USD 150.1 million. This framework reduces ownership risk and helps local groups treat the drone as a village service asset instead of a single-farm machine. It also links drone access with fertilizer and crop-protection distribution channels, since organized service delivery makes it easier to push standardized input programs in the field. That combination gives the market a more durable policy base than a one-time capital subsidy program would normally provide.

Fragmented Drone and Pesticide Regulations

Regulation remains one of the most important constraints because the operating burden is split across aviation compliance and pesticide-use approval. The aviation side runs through the Digital Sky system, which covers unique identification, pilot certification, and permission-linked operations. Separate crop and chemical approvals add another layer, since drone application rules can vary by product, formulation, and local advisory practice. A service operator may be technically ready to fly but still face delays before a specific spray program can begin in a new area. Cross-state expansion becomes slower because each new operating geography can bring another round of procedural checks and local alignment. Smaller providers are affected the most because compliance work consumes working capital and management time that larger operators can spread across bigger fleets. This regulatory fragmentation keeps the market from scaling as quickly as the demand picture alone would suggest.

Other drivers and restraints analyzed in the detailed report include:

- Falling Drone Hardware Prices

- Input-Chemical Inflation Boosting Variable-Rate Spraying

- Limited Skilled Pilots and Training Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rotary-wing drones held 64.6% of product revenue in 2025, leading the India agricultural drones market share among platform types. Their lead came from spray-intensive crop patterns, irregular plot geometry, and hover control in narrow fields across fragmented agricultural landholdings and smallholder-dominated cultivation environments. Subsidy-backed purchases by Farmer-Producer Organizations and service operators kept multirotors in the lead.

Hybrid drones are forecast to expand at a 24.5% CAGR through 2031, the fastest among product categories, as plantation estates and larger field blocks seek longer-range coverage with Vertical Take-Off and Landing (VTOL) flexibility and improved mapping efficiency. Their use is rising in grapes, bananas, and orchard belts where contiguous acreage supports longer sorties and precision monitoring applications. Fixed-wing drones remain relevant for large-area surveying operations, while hybrid platforms are increasingly preferred for balancing endurance and operational flexibility. Product improvements are still evident in stronger weather protection, better connectivity, and smarter path planning in newer launches. This mix keeps rotary-wing systems dominant today while widening the future role of fixed-wing and hybrid platforms in the market.

Hardware accounted for 53.2% of component revenue in 2025, giving it the largest position in the India agricultural drones market size across components. Spending remained focused on spray systems, batteries, sensors, and charging support as agricultural drone deployment networks nationwide expanded. This reflected a deployment phase in which asset purchases still materially outweighed software subscriptions and service fees.

Services are projected to register the quickest growth at a 23.1% CAGR through 2031 as cooperatives, state programs, and commercial operators shift spending from ownership to recurring-use models. Software is also gaining relevance because flight management, prescription mapping, crop analytics, and fleet-management tools are becoming increasingly integrated into daily farm operations. The India agriculture drones industry is therefore moving from hardware-first adoption toward a more balanced mix of equipment, software, and recurring service value. Time-stamped spray logs further strengthen software adoption by supporting insurance documentation, regulatory compliance, and agronomic advisory workflows. As hardware prices decline, the overall revenue mix is estimated to tilt further toward services and software across the market.

List of Companies Covered in this Report:

- DJI

- XAG Co., Ltd.

- Yamaha Motor Co., Ltd.

- Garuda Aerospace Pvt. Ltd.

- iotechworld.com

- Rattanindia Group

- Parrot Drones SAS

- Gifu University (Terra Drone)

- Trimble Inc.

- EagleNXT

- DroneDeploy

- Kray Technologies

- Marut Drones

- Hylio Inc.

- General Aeronautics Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising farm-labor costs and shortages

- 4.2.2 Government subsidies

- 4.2.3 Falling drone hardware prices

- 4.2.4 Input-chemical inflation boosting variable-rate spraying

- 4.2.5 Carbon-credit revenue for low-input farming

- 4.2.6 Women-led cooperative models accelerating adoption

- 4.3 Market Restraints

- 4.3.1 Fragmented drone and pesticide regulations

- 4.3.2 Limited skilled pilots and training capacity

- 4.3.3 Patchy rural 4G/5G coverage

- 4.3.4 Data-sovereignty concerns among FPOs

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Fixed-wing Drones

- 5.1.2 Rotary-wing Drones

- 5.1.3 Hybrid Drones

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.3 By Application

- 5.3.1 Field Mapping and Surveying

- 5.3.2 Crop Spraying

- 5.3.3 Crop Monitoring/Field Surveillance

- 5.3.4 Livestock Monitoring

- 5.3.5 Irrigation Management

- 5.3.6 Soil and Field Analysis

- 5.4 By Farm Size

- 5.4.1 Large-scale Commercial Farms

- 5.4.2 Small and Medium Farms

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-Level Overview, Market-Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 DJI

- 6.4.2 XAG Co., Ltd.

- 6.4.3 Yamaha Motor Co., Ltd.

- 6.4.4 Garuda Aerospace Pvt. Ltd.

- 6.4.5 iotechworld.com

- 6.4.6 Rattanindia Group

- 6.4.7 Parrot Drones SAS

- 6.4.8 Gifu University (Terra Drone)

- 6.4.9 Trimble Inc.

- 6.4.10 EagleNXT

- 6.4.11 DroneDeploy

- 6.4.12 Kray Technologies

- 6.4.13 Marut Drones

- 6.4.14 Hylio Inc.

- 6.4.15 General Aeronautics Pvt. Ltd.