|

시장보고서

상품코드

2065426

북미의 디스크리트 GPU 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America Discrete GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

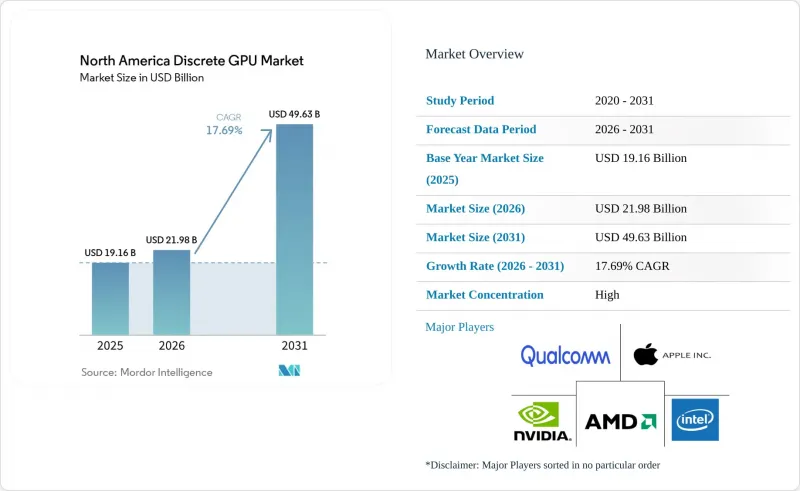

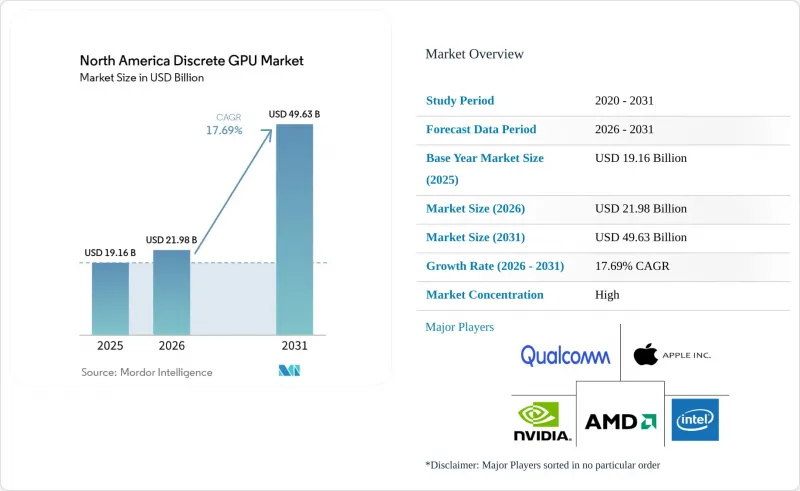

Mordor Intelligence에 의하면, 북미의 디스크리트 GPU 시장 규모는 2025년 191억 6,000만 달러로 평가되었고, 2026년 219억 8,000만 달러로 추정되고, 2031년까지 496억 3,000만 달러로 확대될 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 17.69%를 나타낼 전망입니다.

본 보고서는 디바이스 용도별(모바일 디바이스 및 태블릿, PC 및 워크스테이션, 서버 및 데이터센터용 가속기 등), 메모리 유형별(GDDR 기반 GPU 및 HBM 기반 GPU), 성능 수준별(저가형 GPU, 메인스트림 GPU, 고성능 소비자용 GPU 등), 국가별(미국, 캐나다 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

북미의 디스크리트 GPU 시장 동향 및 인사이트

데이터센터 내 AI 및 ML 워크로드의 확대

북미의 각 하이퍼스케일러 기업들은 최고급 GPU의 납품 일정을 앞당기는 멀티 기가와트 규모의 구매 체계를 운영하고 있으며, 여러 세대에 걸친 칩 할당량을 확보하고 있습니다. AMD와 Meta 간의 2026-2030년 공급 계약은 출하 마일스톤 달성에 따라 주식 워런트가 부여되는 방식으로 구성되어 있어, 공급업체의 대차대조표와 고객의 로드맵이 밀접하게 연결되어 있습니다. NVIDIA가 Groq의 LP30을 Vera-Rubin 플랫폼에 통합함에 따라, 클러스터는 고처리량 훈련용 GPU와 초저지연 추론 어레이로 분할되었으며, 경쟁사들은 순수한 FLOPS가 아닌 토큰당 비용으로 경쟁할 수밖에 없게 되었습니다. 미국 에너지부 및 미국 국립표준기술연구소(NIST)의 신규 도입을 통해 연방 정부 자금에 의한 수요 기준선이 확보되었습니다. CoreWeave를 비롯한 독립형 클라우드 제공업체들은 미국 지방 도시와 캐나다 각 주로 인프라 구축 범위를 확대하고 있으며, GPU 용량의 지역 분산이 더욱 진전되고 있습니다.

AAA급 게임 타이틀에서 실시간 레이 트레이싱에 대한 수요가 급증하고 있습니다.

RTX 50 시리즈는 멀티 프레임 생성을 가능하게 하고, 레이 트레이싱의 프레임 속도를 4배로 높임으로써 대형 타이틀에서 실시간 패스트 레이싱을 표준 기능으로 제공합니다. 인텔의 Arc Battlemage는 2세대 레이 트레이싱 코어를 탑재하고 250-400달러 가격대를 타겟으로 하며, 가격에 민감한 사용자를 위한 선택지로 브랜드를 포지셔닝하고 있지만, 소프트웨어 생태계의 부족 문제는 여전히 남아 있습니다. 클라우드 게임의 성장은 GeForce NOW와 같은 서비스가 가입자당 공유형 가상 GPU에서 전용형 가상 GPU로 전환됨에 따라 하드웨어 수요를 더욱 부추기고 있습니다. 240Hz 및 360Hz 모니터의 보급으로 인해 소비자의 업그레이드 주기가 단축되었고, 노트북 수요가 통합형 솔루션으로 이동하는 상황 속에서도 프리미엄 데스크톱 PC에 대한 지출을 뒷받침하고 있습니다.

선진 노드공급망 변동과 생산 능력 제약

TSMC의 CoWoS 패키징이 주요 병목 현상으로 작용하고 있어, HBM3 탑재 GPU의 리드타임은 6개월을 초과하고 있습니다. 애리조나주에서 파일럿 웨이퍼 생산이 시작되었지만, 국내 패키징 체계가 갖춰지지 않아 여전히 비용이 많이 드는 태평양 횡단 운송 경로를 이용할 수밖에 없는 실정입니다. 미국의 ‘국제 기술 안보·혁신 기금’은 캐나다와 멕시코의 신규 생산 라인에 자금을 지원하고 있으나, 지정학적 리스크와 수율에 대한 불확실성은 여전히 남아 있습니다. Samsung Electronics의 3nm 공정 양산 시작이 지연되면서 대체 조달처가 줄어들고, 리스크가 더욱 집중되고 있습니다.

부문별 분석

2025년, 서버 및 가속기 부문은 북미 디스크리트 GPU 시장 점유율의 40.11%를 차지한 것으로 평가되었으며, 연평균 성장률(CAGR) 18.22%를 기록하며 그 입지를 더욱 공고히할 것으로 예측됩니다. 이 하위 부문은 1조 개 매개변수 모델의 훈련이나 실시간 추론 클러스터를 위한 환경으로 여전히 가장 선호되는 선택지입니다. 그 결과 발생하는 조달 규모는 광학, 액체 냉각, 첨단 패키징 분야의 가치사슬 파트너들을 끌어들이고 있으며, 진입 장벽을 더욱 높이고 있습니다. 소비자용 PC와 워크스테이션은 여전히 큰 시장 규모를 유지하고 있지만, 애플의 통합형 GPU나 퀄컴 칩을 탑재한 슬림하고 가벼운 디자인의 기기로 인한 대체 효과에 직면해 있습니다. 이러한 디바이스는 별도의 GPU 없이도 전문가용 크리에이티브 워크로드의 대부분을 처리할 수 있습니다.

자동차용 ADAS 노드는 소형 기반에 안전 인증을 받은 코프로세서가 필요한 존형 아키텍처에 힘입어, 북미의 디스크리트 GPU 시장에서 가장 가파른 성장 곡선을 보이고 있습니다. 게임기나 휴대용 단말기는 AMD Ryzen Z1 APU와 외부 GPU 도크를 결합한 하이브리드 전략을 채택하여 부문 간의 경계를 모호하게 만들고 있지만, 디스크리트 GPU의 매출은 소폭에 그치고 있습니다. 엣지 디바이스, 산업용 드론, 화상 협업 기기는 퀄컴의 시스템 온 칩(SoC)에 대한 의존도를 높이고 있으며, 이로 인해 저전력 디스크리트 보드의 향후 판매량이 감소하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSHAccording to Mordor Intelligence, the north america discrete GPU market size is projected to expand from USD 19.16 billion in 2025 and USD 21.98 billion in 2026 to USD 49.63 billion by 2031, registering a 17.69% CAGR between 2026 to 2031.

This report is Segmented by Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, and More), Memory Type (GDDR-Based GPUs and HBM-Based GPUs), Performance Tier (Low-Cost GPUs, Mainstream GPUs, High-Performance Consumer GPUs, and More), and Country (United States, Canada, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America Discrete GPU Market Trends and Insights

Expanding AI and ML Workloads in Data Centers

North American hyperscalers are executing multi-gigawatt purchase frameworks that front-load deliveries of top-bin GPUs, locking in allocation across several silicon generations. AMD's 2026-2030 supply agreement with Meta vests equity warrants against shipment milestones, intertwining vendor balance sheets with customer roadmaps. NVIDIA's integration of Groq's LP30 into the Vera-Rubin platform splits clusters into high-throughput training GPUs and ultra-low-latency inference arrays, forcing rivals to compete on cost-per-token rather than raw FLOPS. New installations at the U.S. Department of Energy and the National Institute of Standards and Technology ensure a baseline of federally funded demand. CoreWeave and other independent cloud providers are broadening infrastructure footprints into secondary U.S. metros and Canadian provinces, further localizing GPU capacity.

Surging Demand for Real-Time Ray Tracing in AAA Gaming Titles

The RTX 50 Series enables multi-frame generation, quadrupling ray-traced frame rates, making real-time path tracing the default in big-budget titles. Intel's Arc Battlemage targets the USD 250-USD 400 band with second-generation ray-tracing cores, positioning the brand as a cost-conscious alternative, though software ecosystem gaps remain. Growth in cloud gaming compounds hardware pull-through as services such as GeForce NOW shift from shared to dedicated virtual GPUs per subscriber. Widespread adoption of 240 Hz and 360 Hz monitors compresses consumer upgrade cycles, anchoring premium desktop spend even as notebook demand migrates to integrated solutions.

Supply Chain Volatility of Advanced Nodes Capacity Constraints

TSMC's CoWoS packaging is the principal bottleneck, with HBM3 GPU lead times exceeding 6 months. Although pilot wafer output in Arizona has started, the lack of on-shore packaging still forces costly trans-Pacific loops. The U.S. International Technology Security and Innovation Fund is subsidizing new lines in Canada and Mexico, yet geopolitical and yield uncertainties persist. Samsung's delayed 3 nm ramp narrows alternative sourcing, further concentrating risk.

Other drivers and restraints analyzed in the detailed report include:

- Automotive OEM Shift to Centralized Zonal Architectures Demanding Discrete GPU Co-Processors for ADAS

- Rapid Growth of Cloud Gaming Platforms Requiring GPU Servers

- Rising ASPs Making High-End GPUs Unaffordable for Mainstream Consumers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The servers and accelerators segment accounted for 40.11% of the North America discrete GPU market share in 2025, a position it is expected to reinforce with an 18.22% CAGR. This sub-sector remains the preferred deployment target for trillion-parameter model training and real-time inference clusters. The resulting procurement scale is attracting value-chain partners in optics, liquid cooling, and advanced packaging, deepening entry barriers. Consumer PCs and workstations, while still sizeable, face a substitution effect from Apple's integrated GPUs and Qualcomm-powered thin-and-light designs that meet most professional creation workloads without discrete cards.

Automotive ADAS nodes, though starting from a smaller base, exhibit the sharpest slope within the North America discrete GPU market, helped by zonal architectures that require safety-certified co-processors. Gaming consoles and handhelds adopt hybrid strategies, such as AMD Ryzen Z1 APUs paired with external GPU docks, blurring segment lines but keeping discrete revenue modest. Edge devices, industrial drones, and video collaboration appliances increasingly rely on Qualcomm system-on-chips, trimming prospective unit volumes for low-power discrete boards.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Qualcomm Technologies Inc.

- Apple Inc.

- Imagination Technologies Ltd.

- Arm Ltd.

- Samsung Electronics Co. Ltd.

- MediaTek Inc.

- Graphcore Ltd.

- Cerebras Systems Inc.

- Tenstorrent Inc.

- Broadcom Inc.

- ASUSTeK Computer Inc.

- Micro-Star International Co. Ltd.

- Gigabyte Technology Co. Ltd.

- Sapphire Technology Ltd.

- Zotac Technology Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for Real-Time Ray Tracing in AAA Gaming Titles

- 4.2.2 Rapid Growth of Cloud Gaming Platforms Requiring GPU Servers

- 4.2.3 Expanding AI and ML Workloads in Data Centers

- 4.2.4 Increasing Penetration of High-Refresh-Rate E-Sports Monitors Raising GPU Upgrade Cycles

- 4.2.5 Government-Funded Semiconductor Initiatives Boosting Domestic GPU Manufacturing

- 4.2.6 Automotive OEM Shift to Centralized Zonal Architectures Demanding Discrete GPU Co-Processors for ADAS

- 4.3 Market Restraints

- 4.3.1 Supply Chain Volatility of Advanced Nodes Capacity Constraints

- 4.3.2 Rising ASPs Making High-End GPUs Unaffordable for Mainstream Consumers

- 4.3.3 Escalating Data Center Energy Regulations Limiting GPU Rack Density in Some U.S. States

- 4.3.4 Antitrust Scrutiny on GPU Vendor Bundling Practices Potentially Delaying Product Launches

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Application

- 5.1.1 Mobile Devices and Tablets

- 5.1.2 PCs and Workstations

- 5.1.3 Servers and Datacenter Accelerators

- 5.1.4 Gaming Consoles and Handhelds

- 5.1.5 Automotive / ADAS

- 5.1.6 Other Embedded and Edge Devices

- 5.2 By Memory Type

- 5.2.1 GDDR-Based GPUs

- 5.2.2 HBM-Based GPUs

- 5.3 By Performance Tier

- 5.3.1 Low-Cost GPUs (Less than USD 100)

- 5.3.2 Mainstream GPUs (USD 100-USD 400)

- 5.3.3 High-Performance Consumer GPUs (USD 400-USD 1,200)

- 5.3.4 Data Center / AI Accelerator GPUs (Greater than USD 1,200)

- 5.4 By Counrty

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Qualcomm Technologies Inc.

- 6.4.5 Apple Inc.

- 6.4.6 Imagination Technologies Ltd.

- 6.4.7 Arm Ltd.

- 6.4.8 Samsung Electronics Co. Ltd.

- 6.4.9 MediaTek Inc.

- 6.4.10 Graphcore Ltd.

- 6.4.11 Cerebras Systems Inc.

- 6.4.12 Tenstorrent Inc.

- 6.4.13 Broadcom Inc.

- 6.4.14 ASUSTeK Computer Inc.

- 6.4.15 Micro-Star International Co. Ltd.

- 6.4.16 Gigabyte Technology Co. Ltd.

- 6.4.17 Sapphire Technology Ltd.

- 6.4.18 Zotac Technology Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment