|

시장보고서

상품코드

2065580

디스크리트 GPU 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Discrete GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

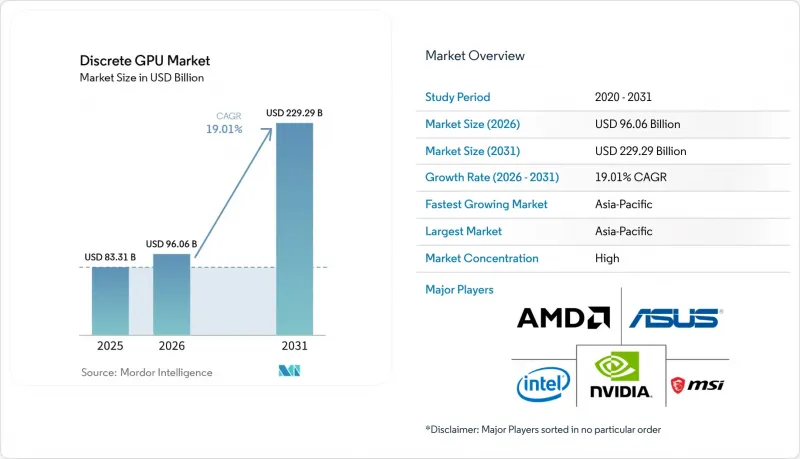

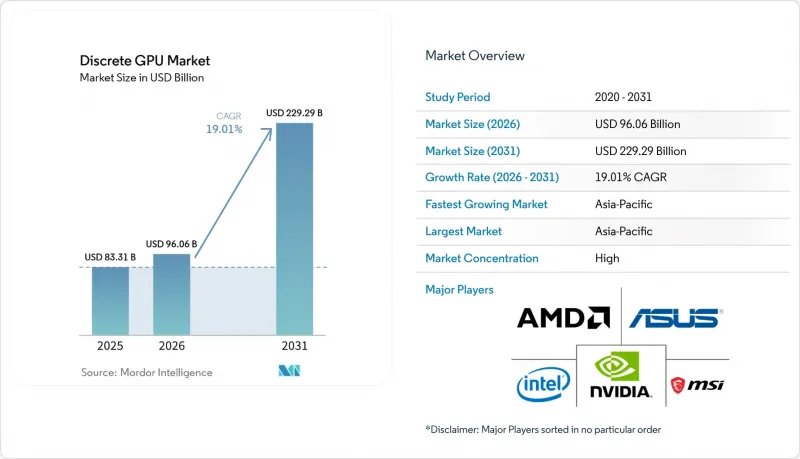

Mordor Intelligence에 의하면, 디스크리트 GPU 시장 규모는 2025년에 833억 1,000만 달러로 평가되었고, 2026년에 960억 6,000만 달러로 추정되고, 2031년까지 2,292억 9,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 19.01%로 성장할 전망입니다.

본 보고서는 기기 용도별(모바일 기기 및 태블릿, PC 및 워크스테이션, 서버 및 데이터센터용 가속기, 게임기 및 휴대용 단말기, 자동차/ADAS, 기타), 메모리 유형별(GDDR 기반 GPU 및 HBM 기반 GPU), 성능 수준별(저가형 GPU(100달러 미만), 메인스트림 GPU(100-400달러), 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 디스크리트 GPU 시장 동향 및 인사이트

디스크리트 가속기에 대한 AI 훈련 및 추론 수요

디스크리트 GPU 시장은 AI 인프라에 대한 투자로 재편되고 있으며, 실시간 추론에 대한 수요는 현재 훈련과 어깨를 나란히 할 정도로 주요 구매 요인으로 급부상하고 있습니다. NVIDIA는 2026 회계연도 총 매출 2,159억 달러 중 데이터센터 부문 매출이 1,973억 달러에 달했다고 보고했으며, 이는 AI 워크로드가 주요 공급업체의 매출 구성을 얼마나 크게 변화시켰는지를 여실히 보여주고 있습니다. 이 회사는 추론이 데이터센터 활동에서 상당한 비중을 차지하고 있음을 보여주며, 지출의 기반이 모델 구축에서 운영 환경으로의 배포로 점차 이동하고 있음을 시사하고 있습니다. AMD 역시 동일한 시장 분야를 공략하고 있으며, 이 회사의 데이터센터 부문 매출은 2026년 1분기에 57억 5,000만 달러를 기록해 전년 동기 대비 57% 증가했습니다. 이는 Instinct의 출하 및 Meta의 도입을 포함한 하이퍼스케일러들 수요에 힘입은 결과입니다. 이는 디스크리트 GPU 시장에 있어 중요한 의미를 지닙니다. 왜냐하면 추론은 극소수의 훈련 클러스터에만 의존하는 것이 아니라, 클라우드, 기업, 국가 주도의 컴퓨팅 프로그램에 걸쳐 더 광범위하고 지속적인 수요를 창출하기 때문입니다. 또한, 이는 경쟁력이 칩 자체뿐만 아니라 패키징, 시스템 설계, 상호 연결 및 소프트웨어 지원에도 크게 좌우되게 되었음을 의미합니다.

프리미엄 게이밍 및 e스포츠에서의 화질 향상

프리미엄 게이밍은 여전히 견조한 수요의 원동력이 되고 있습니다. 이는 하이엔드 제품군 구매자들이 시각적 품질과 그래픽 카드의 장기적인 활용도를 높여주는 소프트웨어 기능 모두에서 가치를 인정하고 있기 때문입니다. NVIDIA는 GeForce RTX 5090을 1,999달러, RTX 5080을 999달러, RTX 5070 Ti를 749달러, RTX 5070을 549달러에 출시하며, 게이밍 제품군의 최상위 모델 가격 기준을 확립했습니다. 또한 NVIDIA는 800개 이상의 게임 및 용도이 RTX 및 DLSS 기술을 채택하고 있다고 밝혔으며, 이는 업그레이드 수요가 하드웨어 사양뿐만 아니라 탄탄한 소프트웨어 기반에 의해 뒷받침되고 있음을 시사합니다. 디스크리트 GPU 시장에서 이 소프트웨어와의 연동이 중요한 이유는 기업들이 기능에 대한 접근성과 게임 최적화가 유지되는 플랫폼 내에서 머무르는 경향이 있기 때문입니다. 따라서 뉴럴 렌더링, 레이 트레이싱, 그리고 더욱 높은 사실성이 요구됨에 따라, e스포츠 및 게이머를 위한 게이밍 분야에서 구형 그래픽 카드의 수명이 단축되고 있습니다. AI 가속기가 매출 성장을 주도하고 있는 반면, 게이밍이 여전히 디스크리트 GPU 시장에서 중요한 위치를 차지하고 있는 이유는 게이밍이 여전히 더 광범위한 스택 전반에 걸친 개발자 도구, 드라이버 생태계 및 제품 출시 속도를 뒷받침하고 있기 때문입니다.

메모리 공급 부족과 기판 비용 상승

AI 가속기와 게이밍 보드가 중복되는 첨단 메모리 및 패키징 자원을 놓고 경쟁적으로 사용하고 있기 때문에 디스크리트 GPU 시장은 계속해서 메모리 공급 부족에 직면하고 있습니다. NVIDIA의 GeForce RTX 50 시리즈는 게이밍 그래픽 카드를 GDDR7으로 한 단계 더 발전시켰으며, 이를 통해 프리미엄 소비자용 제품의 메모리 요구 사항 기준이 한 단계 높아졌습니다. 삼성은 2026년에 AI 컴퓨팅용 HBM4의 상용 출하를 시작했는데, 이는 공급업체들이 생산 능력을 확대하고 있음을 뒷받침하는 한편, 첨단 메모리가 가속기 프로그램에 얼마나 빠르게 도입되고 있는지를 보여줍니다. HBM과 하이엔드 그래픽 메모리가 동시에 공급 부족에 빠지면, 기판 비용이 상승하여 디스크리트 GPU 시장의 하위 모델에서는 가격 책정의 유연성이 사라지게 됩니다. 이러한 압박은 대형 브랜드만큼의 구매 규모를 갖추지 못한 애드인 보드 파트너들에게 가장 큰 부담이 됩니다. 또한, 최종 수요가 견조하더라도 공급업체가 주력 제품 이외공급을 어느 정도의 속도로 확대할 수 있는지에 한계가 따릅니다.

부문별 분석

2025년, 서버 및 데이터센터용 가속기는 디스크리트 GPU 시장의 38.42%를 차지했으며, 가장 큰 디바이스 용도 부문이 되었습니다. 이러한 위상은 수요가 더 이상 모델 훈련에만 집중되어 있는 것이 아니라, 클라우드, 엔터프라이즈 및 주권 컴퓨팅 환경에서의 생산 추론과 점점 더 밀접하게 연결되어 있음을 반영합니다. NVIDIA의 2026 회계연도 데이터센터 매출은 1,973억 달러에 달했으며, 이는 지출이 이미 얼마나 가속기 시스템으로 이동하고 있는지를 보여줍니다. AMD 역시 메타를 비롯한 하이퍼스케일러 기업들의 인스팅트(Instinct) 도입에 힘입어, 2026년 1분기 데이터센터 부문 매출이 57억 7,500만 달러에 달했다고 보고했습니다. 따라서 디스크리트 GPU 시장을 주도하고 있는 것은 단일 칩뿐만 아니라, 실리콘, 패키징, 네트워크, 소프트웨어를 통합한 완전한 컴퓨팅 시스템으로서의 서버 플랫폼입니다.

PC와 워크스테이션은 프리미엄 게이밍 그래픽 카드와 엔터프라이즈용 워크스테이션이 계속해서 고가대를 유지함에 따라 여전히 두 번째로 큰 수익원입니다. 2026년 5월 레노버가 출시한 ‘ThinkStation P4’는 AMD Ryzen PRO 9000 시리즈 프로세서와 NVIDIA RTX PRO 6000 Blackwell Workstation Edition을 핵심으로 하고 있으며, 워크스테이션 수요가 단일 시스템 내의 로컬 AI 추론 및 고도화된 시각화로 이동하고 있음을 보여줍니다. 게임 콘솔과 휴대용 게임기는 여전히 광범위한 생태계 전반에 걸쳐 시각적 기대감을 형성하고 있지만, 디스크리트 GPU 업계의 대부분을 차지하는 애드인 보드 채널에는 직접적인 기여를 하지 못하고 있습니다. 차량용 컴퓨팅에 대한 수요가 증가함에 따라, 자동차 및 ADAS(첨단 운전자 보조 시스템) 용도는 소규모 기반에서 점차 확대되고 있지만, 모바일 기기, 태블릿 및 기타 임베디드 용도는 여전히 발열 및 전력 소비의 제약에 묶여 있습니다. 따라서 디스크리트 GPU 시장은 성능 밀도와 메모리 규모에 따라 추가적인 하드웨어 비용이 정당화되는 부문에 계속 집중되고 있습니다.

지역별 분석

중국은 막대한 AI 연산 수요와 최상위급 수입 가속기에 대한 접근이 제한되는 상황에서 국내 대체 제품에 대한 정책적 지원이 더해지면서 여전히 그 중심적인 위치를 차지하고 있습니다. 2026년 초에 시행된 수출 심사 변경은 복잡성을 완화하는 데 도움이 되지 않았으며, 첨단 칩 출하와 관련된 서류상의 부담이 공급업체들의 중국 시장 진출 방식에 계속해서 영향을 미치고 있습니다. 아시아태평양도 메모리 및 첨단 부품 공급에 있어 중요한 역할을 하고 있습니다. 2026년 Samsung Electronics가 상용 HBM4 출하를 시작한 것은 가속기 도입 준비에 있어 해당 지역이 지닌 중요성을 여실히 보여주었습니다. 일본과 한국은 프리미엄 게이밍 및 전문가용 시각화 분야에서 여전히 중요한 공급처인 반면, 인도와 동남아시아에서는 클라우드 GPU의 확충과 게이밍 사용자층의 확대에 따라 수요가 증가하고 있습니다.

북미는 하이퍼스케일러의 AI 투자, 프리미엄 게이밍 수요, 하이엔드 워크스테이션 구매가 모두 이 지역에 계속 집중됨에 따라, 디스크리트 GPU 시장에서 여전히 2위의 규모를 유지했습니다. NVIDIA와 인텔은 2025년 9월, NVIDIA의 RTX GPU 칩렛을 탑재한 맞춤형 데이터센터용 CPU 및 x86 시스템을 개발하기 위한 여러 세대에 걸친 제휴를 발표했으며, 이를 통해 향후 플랫폼 통합에서 북미의 역할이 더욱 강화되었습니다. 또한, NVIDIA와 코닝은 2026년 5월, 미국의 광통신 제조 역량을 확대하기 위한 다년간의 제휴를 발표하며, GPU 수요를 국내 AI 인프라 구축과 보다 직접적으로 연계했습니다. 한편, 북미 공급업체들은 여전히 국제 출하와 관련된 규정 준수 관리를 해야 했기 때문에 수출 심사 규정이 해당 지역의 채널 전략에 계속해서 영향을 미치고 있었습니다.

유럽의 디스크리트 GPU 시장은 주요 서유럽 시장의 성숙한 게이밍 및 워크스테이션 시장과, 자국 주도의 AI 연산 능력 구축을 향한 열기 사이에서 양분되어 있습니다. 중동 및 아프리카는 절대적인 규모로 보면 여전히 작지만, 걸프 국가들의 AI 인프라 투자로 인해 향후 가속기 도입에 있어 이 지역의 중요성은 높아지고 있습니다. 남미는 브라질과 아르헨티나를 중심으로, 게임 및 컨텐츠 제작 분야 수요가 가장 높은 반면, 가격에 대한 민감도는 여전히 높은 상황입니다. 이 세 지역 모두에서 디스크리트 GPU 시장은 장기적인 AI 및 하이엔드 그래픽스라는 동일한 추세의 혜택을 받고 있지만, 현지 시장의 성장은 여전히 인프라에 대한 자금 지원, 수입 조건, 그리고 하이엔드 제품의 구하기 쉬움에 크게 좌우되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.30According to Mordor Intelligence, the discrete GPU market size is projected to be USD 83.31 billion in 2025, USD 96.06 billion in 2026, and reach USD 229.29 billion by 2031, growing at a CAGR of 19.01% from 2026 to 2031.

This report is Segmented by Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive / ADAS, and More), Memory Type (GDDR-Based GPUs, and HBM-Based GPUs), Performance Tier [Low-Cost GPUs (Less Than USD 100), Mainstream GPUs (USD 100-USD 400), and More}, and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Discrete GPU Market Trends and Insights

AI Training and Inference Demand for Discrete Accelerators

The discrete GPU market is being reshaped by AI infrastructure spending, and live inference demand is now rising fast enough to stand beside training as a core buying driver. NVIDIA reported USD 197.3 billion in fiscal 2026 data center revenue out of total revenue of USD 215.9 billion, underscoring how deeply AI workloads have reshaped the revenue mix of the leading supplier. The same company indicated that inference accounted for a meaningful share of data center activity, suggesting that the spending base is shifting from model construction to production deployment. AMD is pursuing the same part of the market, as its data center segment reached USD 5.75 billion in Q1 2026, up 57% year over year, supported by Instinct shipments and hyperscaler demand, including Meta deployments. This matters for the discrete GPU market because inference creates broader, repeatable demand across clouds, enterprises, and sovereign compute programs, rather than relying on only a small number of training clusters. It also means competitive strength now depends on packaging, system design, interconnects, and software support as much as on the chip itself.

Premium Gaming and Esports Visual Fidelity Upgrades

Premium gaming remains a durable demand driver because higher-end buyers are paying for both visual quality and software features that extend the relevance of cards over time. NVIDIA launched the GeForce RTX 5090 at USD 1,999, the RTX 5080 at USD 999, the RTX 5070 Ti at USD 749, and the RTX 5070 at USD 549, which set the pricing anchor for the top end of the gaming stack. NVIDIA also stated that more than 800 games and applications use RTX and DLSS technologies, indicating that upgrade demand is supported by a deep software base rather than hardware specifications alone. In the discrete GPU market, this software tie-in matters because players tend to stay within platforms that preserve feature access and game optimization. Neural rendering, ray tracing, and higher fidelity requirements are therefore shortening the useful life of older cards in competitive and enthusiast gaming. This keeps gaming important to the discrete GPU market even while AI accelerators lead revenue growth, because gaming still supports developer tools, driver ecosystems, and product cadence across the wider stack.

Memory Supply Tightness and Rising Board Costs

The discrete GPU market continues to face memory tightness because AI accelerators and gaming boards are drawing from overlapping advanced memory and packaging resources. NVIDIA's GeForce RTX 50-series moved gaming cards further into GDDR7, which raised the baseline memory requirement for premium consumer products. Samsung began commercial HBM4 shipments in 2026 for AI computing, confirming that suppliers are expanding capacity but also showing how quickly advanced memory is being pulled into accelerator programs. When HBM and high-end graphics memory are in tight supply at the same time, board costs rise, and the lower end of the discrete GPU market loses pricing flexibility. That pressure is hardest on add-in-board partners that do not have the same purchasing scale as the largest brands. It also limits how quickly vendors can push supply beyond flagship products, even when end demand stays strong.

Other drivers and restraints analyzed in the detailed report include:

- Creator and Professional Visualization Workstation Refresh

- Laptop GPU Adoption for Portable Gaming and AI-Creation Workloads

- Integrated Graphics and Powerful Notebooks Squeezing Entry-Level GPU Demand

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Servers and datacenter accelerators accounted for 38.42% of the discrete GPU market in 2025, making them the largest device application segment. This position reflects demand that is no longer centered only on model training and is increasingly tied to production inference across cloud, enterprise, and sovereign compute environments. NVIDIA's fiscal 2026 data center revenue reached USD 197.3 billion, indicating how much spending has already shifted toward accelerator systems. AMD also reported USD 5.775 billion in Q1 2026 data center segment revenue, supported by Instinct deployments at hyperscalers, including Meta. The discrete GPU market is therefore being pulled by server platforms that combine silicon, packaging, networking, and software into full compute systems rather than by standalone chips alone.

PCs and workstations remained the second-largest revenue pool, as premium gaming cards and enterprise workstations continued to command high selling prices. Lenovo's ThinkStation P4 launch in May 2026, built around AMD Ryzen PRO 9000 Series processors and the NVIDIA RTX PRO 6000 Blackwell Workstation Edition, shows how workstation demand is moving toward local AI inference and advanced visualization in a single machine. Gaming consoles and handhelds still shape visual expectations across the wider ecosystem, but they do not contribute directly to the add-in-board channel that defines most of the discrete GPU industry. Automotive and ADAS applications are expanding from a small base as in-vehicle compute needs rise, while mobile devices, tablets, and other embedded uses remain constrained by thermal and power limits. This keeps the discrete GPU market concentrated in segments where performance density and memory scale justify the extra hardware cost.

Geography Analysis

China remains central to that position because it combines very large AI compute demand with policy support for domestic alternatives when access to the highest-end imported accelerators is restricted. The export review changes in early 2026 did not reduce complexity, and the documentary burden around advanced chip shipments continued to shape how vendors approached the China channel. Asia-Pacific also plays a critical role in supplying memory and advanced components, as Samsung's commercial HBM4 shipments in 2026 underscored the region's importance to accelerator readiness. Japan and South Korea remain important sources of premium gaming and professional visualization demand, while India and Southeast Asia are expanding through cloud GPU build-outs and a larger gaming user base.

North America remained the second-largest geography in the discrete GPU market because hyperscaler AI spending, premium gaming demand, and high-end workstation purchases all stayed concentrated in the region. NVIDIA and Intel announced a multi-generational collaboration in September 2025 to develop custom data center CPUs and x86 systems with NVIDIA RTX GPU chiplets, which reinforced North America's role in future platform integration. NVIDIA and Corning also announced a multiyear partnership in May 2026 to expand US optical connectivity manufacturing capacity, linking GPU demand more directly to domestic AI infrastructure deployment. At the same time, export review rules continued to affect regional channel strategy because North American vendors still had to manage compliance for international shipments.

Europe's discrete GPU market is split between a mature gaming and workstation base in major Western markets and a growing push toward sovereign AI compute capacity. The Middle East and Africa remain smaller in absolute size, but investment in AI infrastructure in the Gulf is improving the region's relevance to future accelerator deployment. South America is centered on Brazil and Argentina, where demand is strongest in gaming and content creation but remains highly price sensitive. Across all 3 of these regions, the discrete GPU market is benefiting from the same long-run AI and premium graphics trends, but local growth still depends heavily on infrastructure funding, import conditions, and the availability of higher-end products.

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- ASUSTeK Computer Inc.

- Micro-Star International Co., Ltd.

- GIGA-BYTE TECHNOLOGY Co., Ltd.

- ZOTAC Technology Limited

- SAPPHIRE Technology Limited

- TUL Corporation

- PNY Technologies, Inc.

- ASRock Inc.

- Colorful Technology Company Limited

- Palit Microsystems Ltd.

- InnoVISION Multimedia Limited

- Leadtek Research Inc.

- Sparkle Computer Co., Ltd.

- Moore Threads Intelligent Technology (Beijing) Co., Ltd.

- Biren Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI Training and Inference Demand for Discrete Accelerators

- 4.2.2 Premium Gaming and Esports Visual Fidelity Upgrades

- 4.2.3 Creator and Professional Visualization Workstation Refresh

- 4.2.4 Laptop dGPU Adoption for Portable Gaming and AI-Creation Workloads

- 4.2.5 Local AI Inference on Deskside Workstations

- 4.2.6 China Domestic GPU Substitution and Sovereign Stack Buildout

- 4.3 Market Restraints

- 4.3.1 Memory Supply Tightness and Rising Board Costs

- 4.3.2 Integrated Graphics and Powerful Notebooks Squeezing Entry-Level dGPU Demand

- 4.3.3 Export Controls and China-Specific Import Restrictions Distorting Product Mix

- 4.3.4 Power, Thermals, and PSU Upgrade Burden at the High End

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Application

- 5.1.1 Mobile Devices and Tablets

- 5.1.2 PCs and Workstations

- 5.1.3 Servers and Datacenter Accelerators

- 5.1.4 Gaming Consoles and Handhelds

- 5.1.5 Automotive / ADAS

- 5.1.6 Other Embedded and Edge Devices

- 5.2 By Memory Type

- 5.2.1 GDDR-based GPUs

- 5.2.2 HBM-based GPUs

- 5.3 By Performance Tier

- 5.3.1 Low-Cost GPUs (Less than USD 100)

- 5.3.2 Mainstream GPUs (USD 100-USD 400)

- 5.3.3 High-Performance Consumer GPUs (USD 400-USD 1,200)

- 5.3.4 Data Center / AI Accelerator GPUs (Greater than USD 1,200)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 South Korea

- 5.4.3.4 India

- 5.4.3.5 Southeast Asia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 Middle East

- 5.4.4.1.1 Saudi Arabia

- 5.4.4.1.2 United Arab Emirates

- 5.4.4.1.3 Turkey

- 5.4.4.1.4 Rest of Middle East

- 5.4.4.2 Africa

- 5.4.4.2.1 South Africa

- 5.4.4.2.2 Nigeria

- 5.4.4.2.3 Rest of Africa

- 5.4.4.1 Middle East

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 ASUSTeK Computer Inc.

- 6.4.5 Micro-Star International Co., Ltd.

- 6.4.6 GIGA-BYTE TECHNOLOGY Co., Ltd.

- 6.4.7 ZOTAC Technology Limited

- 6.4.8 SAPPHIRE Technology Limited

- 6.4.9 TUL Corporation

- 6.4.10 PNY Technologies, Inc.

- 6.4.11 ASRock Inc.

- 6.4.12 Colorful Technology Company Limited

- 6.4.13 Palit Microsystems Ltd.

- 6.4.14 InnoVISION Multimedia Limited

- 6.4.15 Leadtek Research Inc.

- 6.4.16 Sparkle Computer Co., Ltd.

- 6.4.17 Moore Threads Intelligent Technology (Beijing) Co., Ltd.

- 6.4.18 Biren Technology Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment