|

시장보고서

상품코드

2065431

유럽의 디스크리트 GPU 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Discrete GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

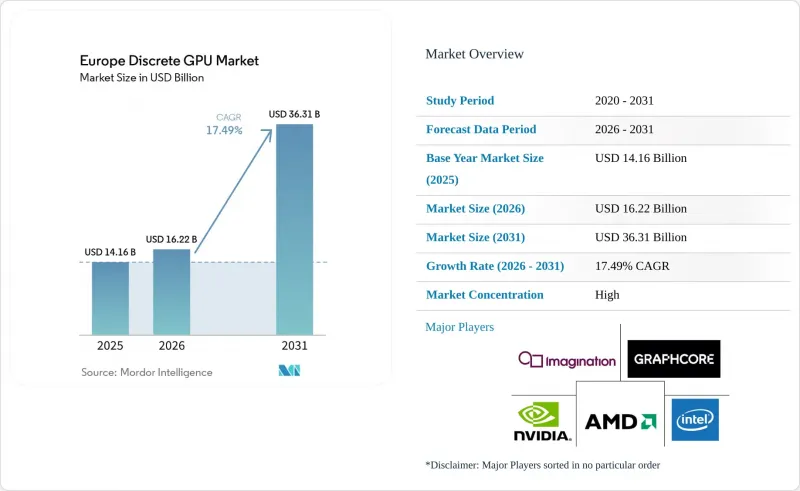

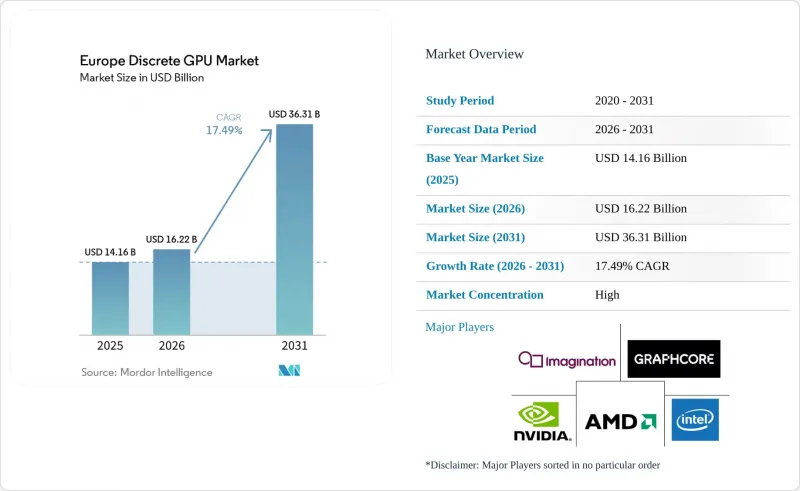

Mordor Intelligence에 의하면, 디스크리트 GPU 시장 규모는 2026년 162억 2,000만 달러로 추정되고, 2031년까지 363억 1,000만 달러로 확대될 전망이며, 2026-2031년 CAGR 17.49%를 나타낼 것으로 예측됩니다.

본 보고서는 디바이스 용도별(모바일 디바이스 및 태블릿, PC 및 워크스테이션, 서버 및 데이터센터용 가속기 등), 메모리 유형별(GDDR 기반 GPU 및 HBM 기반 GPU), 성능 수준별(저가형 GPU, 메인스트림 GPU, 고성능 소비자용 GPU 등), 국가별(독일, 영국, 프랑스 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽의 디스크리트 GPU 시장 동향 및 인사이트

유럽 데이터센터에서의 생성형 AI 워크로드 도입 확대

유럽의 하이퍼스케일러와 소버린 클라우드 제공업체들은 개인정보 보호를 중시하는 AI 추론 및 훈련 요건을 충족하기 위해 전례 없는 규모로 디스크리트 GPU를 도입하고 있습니다. 도이치 텔레콤의 ‘뮌헨 AI 팩토리’는 2026년 초에 1만 대의 Blackwell GPU를 배치하여 가동을 시작할 예정이며, 이는 지역 차원의 컴퓨팅 주권의 필요성을 보여주고 있습니다. 규제 체제의 파편화로 인해 국경을 초월한 자원 공유가 저해되고 있으며, 그 결과 GPU 1대당 요구 사항이 증가하고 구매 계약 기간이 장기화되고 있습니다. 메타(Meta)와 같은 미국 플랫폼조차 현지화 규정을 준수하기 위해 현재 유럽에서 6기가와트의 MI450 용량을 확보하고 있습니다. 앞으로 시행될 AI 책임 지침에 따라 기업들은 On-Premise 추론 스택으로의 전환을 더욱 서둘러야할 것이며, 이로 인해 향후 수년에 걸친 수요 전망이 더욱 확고해질 것입니다.

EU의 기후 목표가 전기차(EV) 및 첨단 운전자 보조 시스템(ADAS)의 연산 요구 사항을 가속화

엄격한 탄소중립 목표와 내연기관 단계적 폐지 일정에 따라, 자동차 제조업체들은 레벨 3-4 자율주행을 실현하기 위해 디스크리트 GPU를 탑재할 수밖에 없는 상황에 처해 있습니다. NVIDIA의 DRIVE Thor 시스템 온 칩은 2025년에 샘플 공급이 시작될 예정이지만, Tier 1 공급업체들은 실시간 센서 융합 처리를 위해 여전히 이를 Ada 세대의 디스크리트 GPU와 결합하여 사용하고 있습니다. 독일의 공장에서는 이미 디지털 트윈 생산 라인에 Omniverse RTX 6000 Ada 보드를 도입하여 개조를 완료한 반면, 프랑스의 각 OEM 업체들은 OTA(Over-the-Air) 업데이트를 위해 GPU를 활용한 모델 재학습을 계속해서 활용하고 있습니다. 예상되는 Euro 7의 미세먼지 규제로 인해, 2개 모델 사이클 이내에 디스크리트 GPU가 양산차에 탑재될 것으로 보입니다.

선진 노드 파운드리에서공급망 변동

유럽은 5나노미터 미만의 제조 역량에 있어 아시아의 단일 파운드리 업체에 크게 의존하고 있습니다. TSMC는 스마트폰 및 하이퍼스케일러용 ASIC의 2나노미터 수주를 우선시하고 있기 때문에 디스크리트 GPU에 할당되는 물량이 분기마다 줄어들 위험이 있습니다. 한편, 삼성은 3나노미터 공정에서 수율 문제에 어려움을 겪고 있어, 듀얼 소싱 도입에 차질을 빚고 있습니다. 게다가 첨단 CoWoS 패키징에 대한 수요가 높기 때문에 현재 수주량이 공급량을 웃돌고 있습니다. 앞으로 인텔 파운드리 서비스는 2027년까지 18옹스트롬 공정의 양산을 목표로 하고 있습니다. 그러나 HBM 통합에 관한 전문 지식이 부족한 점이 과제로 대두되고 있으며, 이는 유럽의 GPU 공급업체들에게 당분간 공급 다각화를 제한하는 요인이 되고 있습니다.

부문별 분석

서버 및 데이터센터용 가속기는 2025년에 디스크리트 GPU 시장 점유율의 39.61%를 차지한 것으로 평가되었으며, 2031년까지 연평균 성장률(CAGR) 18.11%로 성장할 전망입니다. 이러한 확장은 하이퍼스케일러 및 Mistral AI가 주도하는 8억 3,000만 유로(8억 8,810만 달러) 규모의 파리 클러스터와 같은 주권 클라우드 이니셔티브를 반영하고 있습니다. 한편, 소비자용 PC의 경우 일상적인 작업이 내장 그래픽에 맡겨져 있기 때문에 독립형 GPU는 컨텐츠 제작과 같은 특수한 틈새 시장으로 밀려나고 있습니다. 자동차 및 ADAS(첨단 운전자 보조 시스템) 수요는 규모는 작지만, 메르세데스-벤츠와 BMW가 레벨 3 자율주행 검증용으로 디스크리트 GPU를 탑재하고 있는 점에 힘입어 두 자릿수 성장을 기록하고 있습니다.

게임기 시장은 PlayStation 5와 Xbox Series X의 하드웨어 수명 주기가 2028년까지 이어짐에 따라 정체 상태를 유지하고 있습니다. 모바일 기기는 통합형 GPU에 의존하고 있기 때문에 독립형 GPU의 보급은 틈새 시장인 게이밍 태블릿으로 한정되어 있습니다. 산업용 비전 및 의료용 영상 시스템은 견조하지만 소폭의 수익을 올리고 있으나, 긴 인증 절차로 인해 성장세가 둔화되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSHAccording to Mordor Intelligence, the discrete GPU market size is projected to expand from USD 16.22 billion in 2026 to USD 36.31 billion by 2031, registering a CAGR of 17.49% over 2026-2031.

This report is Segmented by Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, and More), Memory Type (GDDR-Based GPUs and HBM-Based GPUs), Performance Tier (Low-Cost GPUs, Mainstream GPUs, High-Performance Consumer GPUs, and More), and Country (Germany, United Kingdom, France, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe Discrete GPU Market Trends and Insights

Rising Adoption of Generative AI Workloads in European Data Centers

European hyperscalers and sovereign cloud providers are deploying discrete GPUs at unprecedented scale to meet privacy-centric AI inference and training mandates. Deutsche Telekom's Munich AI Factory came online in early 2026 with 10,000 Blackwell GPUs, demonstrating the need for localized compute sovereignty. Fragmented regulatory regimes prevent cross-border pooling, inflating per-unit GPU requirements and lengthening purchase commitments. Even U.S. platforms such as Meta now provision 6 gigawatts of MI450 capacity in Europe to meet localization rules.A forthcoming AI liability directive will further push enterprises toward on-premises inference stacks, reinforcing multiyear demand visibility.

EU Climate Targets Accelerating EV and ADAS Compute Requirements

Strict net-zero and internal-combustion-phase-out timelines compel automakers to embed discrete GPUs for Level 3-4 autonomy. NVIDIA's DRIVE Thor system-on-chip samples in 2025, but tier-one suppliers still pair it with discrete Ada-generation GPUs to manage real-time sensor fusion. German plants have already retrofitted their digital twin production lines with Omniverse RTX 6000 Ada boards, while French OEMs continue to rely on GPU-accelerated model retraining for over-the-air updates. Expected Euro 7 particulate rules will push discrete GPUs into mass-market vehicles within two model cycles.

Supply Chain Volatility in Advanced Node Foundries

Europe relies heavily on a single Asian foundry for sub-5-nanometer capacity. TSMC, prioritizing 2-nanometer orders for smartphones and hyperscaler ASICs, risks quarterly cutbacks to discrete GPU allocations. Meanwhile, Samsung's struggles with yields at the 3-nanometer node have dissuaded dual sourcing. Additionally, while advanced CoWoS packaging sees high demand, it is currently oversubscribed. Looking ahead, Intel Foundry Services aims for 18-angstrom production by 2027. However, their lack of expertise in HBM integration poses challenges, restricting immediate supply diversification for GPU vendors in Europe.

Other drivers and restraints analyzed in the detailed report include:

- Subsidies Under the EU Chips Act for Local GPU Manufacturing

- Proliferation of Real-Time Ray Tracing in AAA Games

- Escalating HBM Pricing Pressures on Board OEM Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Servers and datacenter accelerators captured 39.61% of the discrete GPU market share in 2025 and will rise at an 18.11% CAGR through 2031. This expansion mirrors hyperscaler and sovereign-cloud commitments such as Mistral AI's EUR 830 million (USD 888.1 million) Paris cluster. Meanwhile, consumer PCs offload routine tasks to integrated graphics, pushing discrete GPUs into specialized content-creation niches. Automotive and ADAS demand, although smaller, records double-digit growth as Mercedes-Benz and BMW embed discrete GPUs for Level-3 autonomy validation.

Gaming consoles remain flat because PlayStation 5 and Xbox Series X hardware cycles run until 2028. Mobile devices rely on integrated GPUs, limiting discrete penetration to niche gaming tablets. Industrial vision and medical-imaging systems contribute steady but modest revenue, slowed by lengthy certification timelines.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Imagination Technologies Ltd.

- Graphcore Ltd.

- Kalray SA

- ASUStek Computer Inc.

- Micro-Star International Co. Ltd.

- GIGABYTE Technology Co. Ltd.

- Sapphire Technology Ltd.

- Palit Microsystems Ltd.

- ZOTAC Technology Ltd.

- Colorful Technology Co. Ltd.

- PNY Technologies Inc.

- ASRock Inc.

- Leadtek Research Inc.

- KFA2 (Galaxy Microsystems)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 CPU-GPU Integration Constrains Adds Stand-Alone GPU Demand

- 4.2.2 Rising Adoption of Generative AI Workloads in European Data Centers

- 4.2.2.1 Europe Discrete GPU Market

- 4.2.3 Proliferation of Real-Time Ray Tracing in AAA Games

- 4.2.4 EU Climate Targets Accelerating EV and ADAS Compute Requirements

- 4.2.5 Open-Source GPU Driver Maturity Lowering Total Cost of Ownership

- 4.2.6 Subsidies Under EU Chips Act for Local GPU Manufacturing

- 4.3 Market Restraints

- 4.3.1 Supply Chain Volatility in Advanced Node Foundries

- 4.3.2 Channel Inventory Gluts Post-Crypto Down-Cycles

- 4.3.3 Tightened EU Energy-Efficiency Regulations on Data Centers

- 4.3.4 Escalating HBM Pricing Pressures on Board OEM Margins

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Application

- 5.1.1 Mobile Devices and Tablets

- 5.1.2 PCs and Workstations

- 5.1.3 Servers and Datacenter Accelerators

- 5.1.4 Gaming Consoles and Handhelds

- 5.1.5 Automotive / ADAS

- 5.1.6 Other Embedded and Edge Devices

- 5.2 By Memory Type

- 5.2.1 GDDR-based GPUs

- 5.2.2 HBM-based GPUs

- 5.3 By Performance Tier

- 5.3.1 Low-Cost GPUs (Less than USD 100)

- 5.3.2 Mainstream GPUs (USD 100-USD 400)

- 5.3.3 High-Performance Consumer GPUs (USD 400-USD 1,200)

- 5.3.4 Data Center / AI Accelerator GPUs (Greater than USD 1,200)

- 5.4 By Geography

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Imagination Technologies Ltd.

- 6.4.5 Graphcore Ltd.

- 6.4.6 Kalray SA

- 6.4.7 ASUStek Computer Inc.

- 6.4.8 Micro-Star International Co. Ltd.

- 6.4.9 GIGABYTE Technology Co. Ltd.

- 6.4.10 Sapphire Technology Ltd.

- 6.4.11 Palit Microsystems Ltd.

- 6.4.12 ZOTAC Technology Ltd.

- 6.4.13 Colorful Technology Co. Ltd.

- 6.4.14 PNY Technologies Inc.

- 6.4.15 ASRock Inc.

- 6.4.16 Leadtek Research Inc.

- 6.4.17 KFA2 (Galaxy Microsystems)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment